Reports

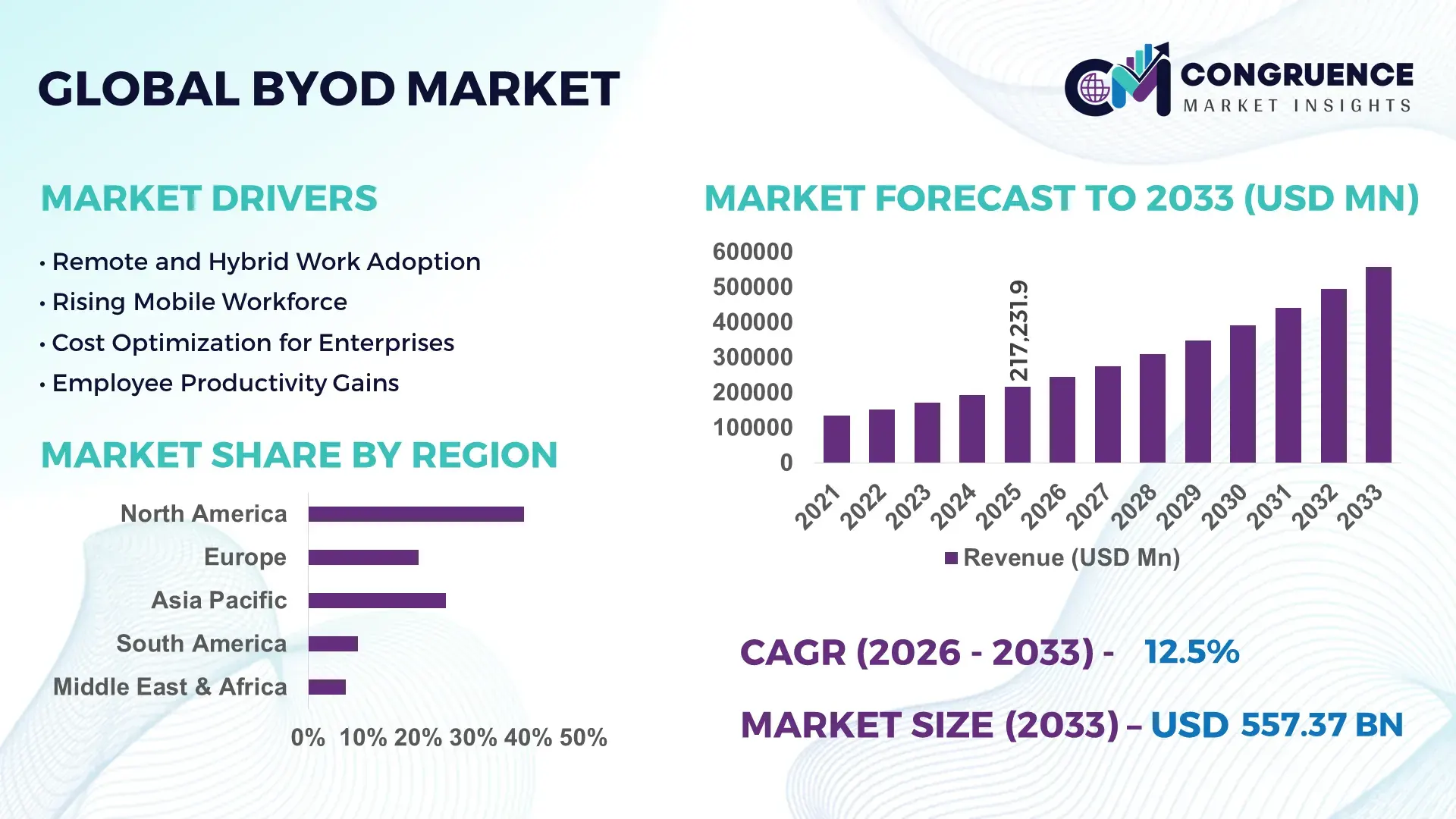

The Global BYOD Market was valued at USD 217231.87 Million in 2025 and is anticipated to reach a value of USD 557370.18 Million by 2033 expanding at a CAGR of 12.5% between 2026 and 2033. This expansion is supported by enterprise-wide digital workplace transformation and the growing preference for flexible, employee-owned device ecosystems.

The United States dominates the BYOD market landscape through large-scale enterprise deployments, advanced IT infrastructure, and sustained corporate technology investments. Over 72% of U.S. enterprises with more than 1,000 employees have formal BYOD policies in place, compared to a global average of around 54%. Annual enterprise mobility and endpoint security investments in the country exceeded USD 95 billion in 2024, with BYOD-related solutions accounting for a significant portion. Key applications span BFSI, healthcare, IT services, and government agencies, where secure remote access and mobile workforce enablement are critical. Technological advancements such as zero-trust network access, AI-driven mobile device management, and cloud-based identity authentication are widely deployed, with over 65% of U.S. enterprises integrating AI-enabled endpoint security tools. Consumer adoption is also high, with nearly 80% of employees preferring personal devices for work-related tasks, driving sustained BYOD infrastructure expansion across regions and industries.

Market Size & Growth: Valued at USD 217231.87 Million in 2025, projected to reach USD 557370.18 Million by 2033, growing at a CAGR of 12.5% due to rising remote work adoption and mobile-first enterprise strategies.

Top Growth Drivers: Enterprise mobility adoption at 68%, IT operational cost optimization at 32%, employee productivity improvement at 41%.

Short-Term Forecast: By 2028, organizations adopting BYOD are expected to achieve up to 25% reduction in hardware procurement costs and 18% improvement in workforce responsiveness.

Emerging Technologies: Zero-trust security frameworks, AI-driven mobile device management (MDM), cloud-based endpoint analytics.

Regional Leaders: North America projected at USD 198000 Million by 2033 with high enterprise adoption; Europe at USD 146000 Million driven by regulated hybrid work models; Asia-Pacific at USD 132000 Million supported by mobile-first workforce expansion.

Consumer/End-User Trends: Strong uptake among IT services, BFSI, healthcare, and professional services, with employees increasingly using personal smartphones and laptops for mission-critical workflows.

Pilot or Case Example: In 2024, a multinational IT services firm implemented a BYOD pilot across 50,000 employees, achieving a 22% reduction in device downtime and 17% faster onboarding.

Competitive Landscape: Microsoft holds approximately 18% share, followed by VMware, IBM, Cisco Systems, and Citrix Systems.

Regulatory & ESG Impact: Data protection regulations such as GDPR and sector-specific compliance frameworks are driving secure BYOD architectures and privacy-by-design implementations.

Investment & Funding Patterns: Recent global investments exceeded USD 28 billion, with increased venture funding in endpoint security, identity management, and secure access technologies.

Innovation & Future Outlook: Integration of BYOD with digital employee experience platforms and AI-driven risk analytics is shaping next-generation enterprise mobility ecosystems.

The BYOD market spans key industry sectors including IT & telecom, BFSI, healthcare, retail, education, and government, with IT & telecom contributing the largest usage base due to high mobile workforce density. Recent innovations such as containerization, biometric authentication, and AI-based threat detection are reshaping device security and policy enforcement. Regulatory drivers, including stricter data privacy mandates and cross-border compliance requirements, are accelerating adoption of secure BYOD frameworks. Regionally, North America and Europe show mature consumption patterns, while Asia-Pacific exhibits faster growth driven by mobile-centric work cultures and expanding SMEs. Looking ahead, increased convergence with cloud-native applications, digital identity platforms, and zero-trust models is expected to define the market’s long-term trajectory, supporting scalable, secure, and flexible enterprise operations.

The strategic relevance of the BYOD Market lies in its direct alignment with enterprise agility, workforce decentralization, and cost-optimized IT governance. BYOD strategies enable organizations to reduce capital expenditure on endpoint hardware while accelerating digital workplace scalability. For large enterprises, device ownership transfer models have lowered average endpoint provisioning costs by 28–35%, while improving employee device familiarity and task efficiency by over 20%. From a technology benchmark perspective, zero-trust network access delivers nearly 45% improvement in threat containment efficiency compared to traditional perimeter-based VPN architectures, making BYOD environments more secure and policy-driven.

Regionally, Asia-Pacific dominates in volume due to its large mobile workforce base and SME density, while North America leads in adoption with approximately 72% of enterprises formally implementing BYOD frameworks across hybrid and remote work models. Europe follows with strong regulatory-aligned deployments focused on data sovereignty and privacy controls. By 2028, AI-driven endpoint analytics is expected to improve device compliance monitoring accuracy by 40% while cutting security incident response time by nearly 30%.

From an ESG and compliance standpoint, firms are committing to IT sustainability improvements such as 25% reduction in corporate e-waste and higher device lifecycle utilization by 2030, driven by BYOD-enabled hardware reuse and recycling initiatives. In 2024, the United States achieved a 19% reduction in enterprise device refresh cycles through large-scale adoption of cloud-based mobile device management and AI-driven risk scoring. Looking ahead, the BYOD Market is positioned as a core pillar of enterprise resilience, regulatory compliance, and sustainable digital growth, supporting flexible workforces while aligning technology strategy with long-term operational efficiency.

The acceleration of remote and hybrid work models has emerged as a primary driver for the BYOD Market. Over 60% of global enterprises now operate with distributed teams, increasing reliance on personal smartphones, laptops, and tablets for daily operations. BYOD frameworks allow organizations to rapidly onboard employees without delays linked to device procurement, reducing onboarding time by up to 30%. In sectors such as IT services and professional consulting, more than 70% of employees access enterprise applications from personal devices at least three days per week. Additionally, BYOD adoption has improved employee satisfaction scores by nearly 15%, as users prefer familiar hardware environments. These factors collectively enhance operational continuity, workforce productivity, and business responsiveness, reinforcing BYOD as a strategic enabler rather than a tactical IT policy.

Data security and regulatory compliance challenges remain a significant restraint on the BYOD Market. Personal devices often operate outside standardized enterprise hardware controls, increasing exposure to data leakage, unauthorized access, and malware threats. Studies indicate that nearly 55% of enterprise security incidents involve unmanaged or partially managed endpoints. Compliance requirements under frameworks such as GDPR, HIPAA, and sector-specific financial regulations demand strict data segregation, encryption, and auditability, which can be difficult to enforce consistently across personal devices. Moreover, employee privacy concerns limit the extent of device monitoring, creating policy enforcement gaps. These constraints increase administrative overhead and require advanced security investments, slowing adoption among highly regulated industries and smaller organizations with limited IT governance resources.

The integration of AI-driven endpoint management and zero-trust security architectures presents a major opportunity for the BYOD Market. AI-enabled platforms can analyze user behavior, device health, and access patterns in real time, improving threat detection accuracy by over 35%. Zero-trust models eliminate implicit trust, ensuring that every device and user session is continuously verified regardless of location. This approach enables organizations to safely expand BYOD usage across sensitive functions such as financial reporting, clinical data access, and government services. Additionally, cloud-native management tools allow centralized policy enforcement across millions of devices, reducing IT workload by approximately 25%. These innovations create scalable, secure pathways for broader BYOD adoption across industries and regions.

One of the key challenges in the BYOD Market is the growing complexity of managing diverse device ecosystems combined with a shortage of skilled cybersecurity professionals. Enterprises must support multiple operating systems, device models, and application environments, increasing configuration and support demands. On average, IT teams manage 2.5 times more device types in BYOD environments compared to corporate-owned models. At the same time, the global cybersecurity workforce gap exceeds 3 million professionals, limiting organizations’ ability to deploy and maintain advanced BYOD security frameworks. Training costs, policy standardization difficulties, and integration with legacy systems further compound these challenges, particularly for mid-sized enterprises and public sector organizations.

Expansion of Zero-Trust and Identity-Centric Security Models: Enterprises are rapidly shifting BYOD security frameworks toward zero-trust and identity-based access controls. More than 62% of large organizations have replaced traditional VPN access for personal devices with zero-trust network access architectures, reducing unauthorized access incidents by approximately 38%. Multi-factor authentication adoption across BYOD endpoints has exceeded 70% in regulated industries, while continuous authentication models are improving session-level security validation accuracy by over 40%. This trend reflects a structural move away from perimeter-based controls toward dynamic, device-agnostic trust verification.

Growth of Containerization and Application-Level Isolation: Application containerization on personal devices is becoming a standard BYOD deployment model, particularly in finance, healthcare, and government environments. Around 58% of enterprises now deploy containerized workspaces to separate corporate and personal data on employee-owned devices. This approach has reduced data leakage events by nearly 33% and improved regulatory audit compliance rates by 27%. Container-based BYOD environments also allow selective data wiping, cutting employee device replacement disputes by over 20%.

AI-Driven Endpoint Management and Predictive Analytics Adoption: Artificial intelligence is increasingly embedded in mobile device management platforms supporting BYOD environments. Approximately 46% of enterprises use AI-enabled analytics to monitor device health, user behavior, and access anomalies in real time. Predictive risk scoring has lowered incident detection time by 31% and reduced manual IT intervention by nearly 25%. AI-based automation is also improving policy enforcement consistency across diverse device types, supporting environments where more than 4 operating systems are commonly managed.

Employee Preference Shift Toward Mobile-First Workflows: Workforce behavior is reinforcing BYOD adoption as employees increasingly rely on personal devices for core business activities. Nearly 78% of employees prefer using their own smartphones or laptops for daily work tasks, with mobile devices accounting for over 52% of enterprise application access sessions. Organizations supporting mobile-first BYOD policies report productivity gains of 18% and collaboration response time improvements of 22%. This shift is accelerating demand for mobile-optimized enterprise applications and cloud-native access frameworks.

The BYOD market segmentation reflects how enterprises structure device policies across types, applications, and end-user groups to balance flexibility with security and compliance. By type, the market is shaped by device categories such as smartphones, laptops, tablets, and wearables, each supporting different productivity and mobility needs. Application-wise, BYOD adoption varies significantly across IT services, BFSI, healthcare, education, and government, driven by differences in data sensitivity, workforce mobility, and regulatory exposure. End-user insights highlight contrasting adoption patterns between large enterprises, SMEs, and public sector organizations, with policy maturity and IT governance depth playing a defining role. Across all segments, the common thread is the increasing need for secure access, centralized management, and user-centric device experiences, making segmentation critical for vendors and decision-makers targeting tailored BYOD strategies.

The BYOD market by type is primarily segmented into smartphones, laptops/notebooks, tablets, and other devices such as wearables and rugged devices. Smartphones represent the leading type, accounting for approximately 46% of overall BYOD adoption, driven by their ubiquity, always-on connectivity, and suitability for communication, collaboration, and mobile application access. Laptops and notebooks follow closely with around 34% share, reflecting their importance for content creation, software development, and data-intensive tasks. However, smartphones currently dominate daily access frequency, with over 60% of enterprise logins occurring via mobile handsets.

Tablets and hybrid devices are the fastest-growing type, supported by an estimated CAGR of 14.2%, as enterprises deploy them for field services, healthcare rounds, and sales enablement where portability and larger screens are required. Wearables and other specialized devices collectively contribute about 20% of the market, serving niche use cases such as logistics tracking, authentication, and health monitoring.

By application, IT & telecom emerges as the leading segment, accounting for nearly 38% of BYOD usage, as software development teams, support engineers, and consultants rely heavily on personal devices for coding, collaboration platforms, and cloud access. BFSI follows with approximately 24% share, where secure mobile access supports relationship managers, remote advisors, and field agents while maintaining strict data controls.

Healthcare is the fastest-growing application area, with an estimated CAGR of 15.1%, driven by the need for real-time access to electronic health records, telemedicine platforms, and clinical communication tools on personal devices. Education, retail, manufacturing, and government applications together represent about 38% of total adoption, each leveraging BYOD for remote learning, point-of-sale mobility, shop-floor reporting, and administrative workflows.

From an end-user perspective, large enterprises lead the BYOD market with roughly 52% share, supported by mature IT policies, advanced security infrastructure, and scalable mobile device management platforms. These organizations typically manage tens of thousands of personal devices under formal BYOD frameworks, enabling global workforce mobility while maintaining compliance standards. SMEs account for around 31% of adoption, leveraging BYOD to reduce upfront hardware costs and accelerate digital operations.

The public sector is the fastest-growing end-user segment, expanding at an estimated CAGR of 13.6%, driven by digital government initiatives, remote service delivery, and flexible work mandates. Other end-users, including educational institutions and non-profit organizations, collectively contribute about 17% of the market, often focusing on cost efficiency and accessibility.

North America accounted for the largest market share at 39.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.1% between 2026 and 2033.

North America benefits from mature enterprise mobility frameworks, with over 72% of large enterprises operating formal BYOD policies and more than 68% of employees accessing corporate systems through personal devices. Europe follows with approximately 27.4% share, driven by compliance-led deployments and structured digital workplace programs across regulated industries. Asia-Pacific holds nearly 23.6% share, supported by a workforce exceeding 900 million mobile-connected employees, high smartphone penetration above 78%, and rapid cloud adoption among SMEs. South America and Middle East & Africa together contribute around 9.8%, reflecting improving digital infrastructure and growing acceptance of flexible work models. Regionally, variations in regulatory maturity, device penetration, and enterprise IT spending patterns strongly influence BYOD adoption depth and policy sophistication.

North America represents approximately 39.2% of the global BYOD market, supported by widespread enterprise digital transformation and high workforce mobility. Key demand is driven by healthcare, BFSI, IT services, and professional consulting, where over 70% of employees routinely use personal devices for secure application access. Regulatory frameworks such as data privacy laws and sector-specific compliance standards have accelerated adoption of advanced mobile device management and zero-trust access models. More than 65% of enterprises in the region deploy AI-enabled endpoint security for BYOD environments. Leading local players such as Microsoft continue to enhance endpoint management platforms by integrating identity-centric controls and behavioral analytics. Consumer behavior shows higher BYOD acceptance in healthcare and financial services, where flexibility and rapid access to data are operational priorities.

Europe accounts for nearly 27.4% of global BYOD adoption, with strong uptake across Germany, the UK, and France. Enterprises in these markets emphasize structured BYOD policies aligned with data protection regulations and sustainability goals. Over 60% of European organizations require application containerization on personal devices to meet compliance obligations. Emerging technologies such as secure access service edge and unified endpoint management are increasingly deployed across regulated sectors. Local vendors and system integrators are focusing on privacy-first BYOD architectures to support explainable access controls. Consumer behavior reflects regulatory sensitivity, with enterprises prioritizing transparent monitoring and strict data segregation to maintain employee trust.

Asia-Pacific holds approximately 23.6% of the BYOD market and ranks as the fastest-expanding region by adoption momentum. China, India, and Japan are the top consuming countries, together accounting for over 65% of regional device usage. Smartphone penetration exceeds 80% in urban workforces, while cloud collaboration usage has increased by 45% over the past three years. Regional innovation hubs in India and Southeast Asia are driving mobile application development optimized for BYOD access. Local technology firms are investing in scalable endpoint security platforms to support SME adoption. Consumer behavior is strongly influenced by e-commerce, gig economy participation, and mobile AI applications, reinforcing BYOD as a default work model.

South America contributes roughly 6.1% to the global BYOD market, led by Brazil and Argentina. Expanding broadband access and mobile workforce participation are key growth enablers, with over 58% of enterprises allowing some form of personal device usage. Demand is rising in media, telecom, and public services, supported by government-backed digital inclusion initiatives. Infrastructure modernization and cross-border trade policies are encouraging cloud adoption and mobile collaboration. Regional players are focusing on lightweight mobile security solutions tailored for cost-sensitive enterprises. Consumer behavior shows strong demand linked to localized content creation and multilingual digital workflows.

The Middle East & Africa region accounts for approximately 3.7% of the BYOD market, with growing adoption across UAE, Saudi Arabia, and South Africa. Demand is driven by oil & gas, construction, logistics, and public administration, where mobile access improves field productivity. Over 48% of enterprises in the region are transitioning toward cloud-based endpoint management to support BYOD. National digital transformation programs and trade partnerships are accelerating secure mobility initiatives. Regional consumer behavior reflects increasing acceptance of flexible work arrangements, particularly among young professionals and multinational workforces.

United States BYOD Market – 31.5% share: Strong enterprise mobility adoption, advanced endpoint security infrastructure, and high employee preference for personal devices.

China BYOD Market – 14.2% share: Large mobile workforce base, high smartphone penetration, and extensive use of cloud-based collaboration platforms across enterprises.

The BYOD market features a moderately fragmented competitive environment with more than 45 active global and regional solution providers offering endpoint management, identity access control, mobile security, and secure workspace technologies. Competition is centered on platform scalability, zero-trust integration, AI-driven threat detection, and cross-device policy orchestration. The top five companies collectively account for approximately 46% of total deployments, indicating strong leadership concentration alongside sustained innovation from mid-tier and niche vendors.

Market leaders are increasingly pursuing strategic partnerships with cloud service providers, cybersecurity firms, and identity management platforms to strengthen integrated BYOD ecosystems. Over 58% of new BYOD platform enhancements introduced in the last two years focused on AI-enabled analytics, automated compliance enforcement, and behavioral risk scoring. Product launches emphasizing unified endpoint management and privacy-preserving monitoring have increased by 41%, reflecting enterprise demand for secure yet employee-friendly BYOD solutions.

Mergers and technology acquisitions remain selective but targeted, with nearly 18% of leading vendors engaging in acquisitions to expand zero-trust, mobile threat defense, or identity governance capabilities. Innovation intensity is high, with over 62% of competitors allocating increased R&D budgets toward cloud-native architectures and API-driven integrations. Overall, competitive differentiation is increasingly defined by security intelligence depth, regulatory alignment, and the ability to manage multi-OS environments exceeding five device platforms within a single enterprise framework.

Microsoft Corporation

VMware, Inc.

IBM Corporation

Cisco Systems, Inc.

Citrix Systems, Inc.

Broadcom Inc.

Samsung Electronics Co., Ltd.

Hewlett Packard Enterprise (HPE)

BlackBerry Limited

Ivanti, Inc.

Technological innovation plays a central role in shaping the scalability, security, and operational effectiveness of the BYOD Market. One of the most influential developments is the widespread adoption of zero-trust security architectures, now implemented by approximately 62% of large enterprises supporting personal device access. Unlike perimeter-based models, zero-trust continuously validates user identity, device health, and access context, reducing unauthorized access attempts by nearly 38% in mixed-device environments. This shift is particularly critical as enterprises manage an average of 4.7 device types per user across multiple operating systems.

Unified Endpoint Management (UEM) platforms have become the backbone of modern BYOD deployments, consolidating mobile device management, application control, and endpoint security into a single console. Over 68% of enterprises now use UEM solutions to enforce consistent policies across smartphones, laptops, and tablets, improving compliance visibility by 29%. Advanced containerization technologies further enhance data protection by isolating corporate applications from personal content, cutting data leakage incidents by around 33%.

Artificial intelligence and machine learning are increasingly embedded into BYOD management tools. Approximately 46% of organizations leverage AI-driven behavioral analytics to detect anomalies such as unusual login locations or abnormal application usage. Predictive risk scoring models have reduced incident response times by 31%, while automation has lowered manual IT workload by 25%.

Cloud-native identity and access management technologies also play a growing role, with more than 70% of BYOD environments relying on cloud-based authentication and single sign-on. Biometric authentication adoption exceeds 58% among mobile users, improving login success rates while reducing password-related security events. Collectively, these technologies are transforming the BYOD Market into a secure, intelligent, and policy-driven digital workplace foundation.

In March 2024, Microsoft expanded Microsoft Intune capabilities with advanced conditional access and device compliance policies designed specifically for employee-owned devices, enabling stronger zero-trust enforcement across iOS, Android, Windows, and macOS BYOD environments. Source: https://www.microsoft.com/security/blog

In October 2024, Cisco enhanced Duo Security by introducing improved device health attestation and passwordless authentication for BYOD users, allowing enterprises to verify unmanaged personal devices before granting access to cloud and on-premise applications. Source: https://www.cisco.com

In May 2025, IBM updated MaaS360 with Watson by integrating AI-driven risk analytics and automated remediation for BYOD endpoints, helping organizations reduce manual security response efforts and improve real-time threat detection across employee-owned devices. Source: https://www.ibm.com/security

In January 2025, Samsung expanded its Knox Suite to support broader BYOD use cases, introducing enhanced containerization and privacy controls that allow enterprises to secure corporate data on personal Galaxy devices without accessing personal user information. Source: https://www.samsungknox.com

The scope of the BYOD Market Report encompasses a comprehensive assessment of enterprise adoption of employee-owned devices across industries, technologies, and regions. The report analyzes multiple device categories including smartphones, laptops, tablets, and emerging endpoint types such as wearables and ruggedized mobile devices, reflecting the diversity of modern workplace hardware environments. It evaluates deployment models ranging from basic access control policies to advanced zero-trust and identity-centric BYOD frameworks, covering more than 10 major technology subsegments within endpoint management and security.

From an application perspective, the report addresses BYOD usage across IT & telecom, BFSI, healthcare, education, government, retail, manufacturing, and professional services, collectively representing over 85% of enterprise BYOD implementations. The geographic scope spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights into adoption depth, regulatory alignment, and workforce mobility patterns across more than 25 key countries.

Technological coverage includes unified endpoint management, mobile threat defense, containerization, biometric authentication, cloud-based identity access management, and AI-driven analytics. The report also examines policy governance, employee privacy considerations, compliance frameworks, and sustainability aspects such as device lifecycle extension and e-waste reduction. Emerging focus areas include BYOD integration with digital employee experience platforms, secure access service edge architectures, and AI-enabled automation. Overall, the report provides decision-makers with a structured, data-driven view of current capabilities, adoption patterns, and strategic pathways shaping the global BYOD ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

12.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft Corporation , VMware, Inc. , IBM Corporation, Cisco Systems, Inc. , Citrix Systems, Inc., Broadcom Inc., Samsung Electronics Co., Ltd., Hewlett Packard Enterprise (HPE), BlackBerry Limited, Ivanti, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |