Reports

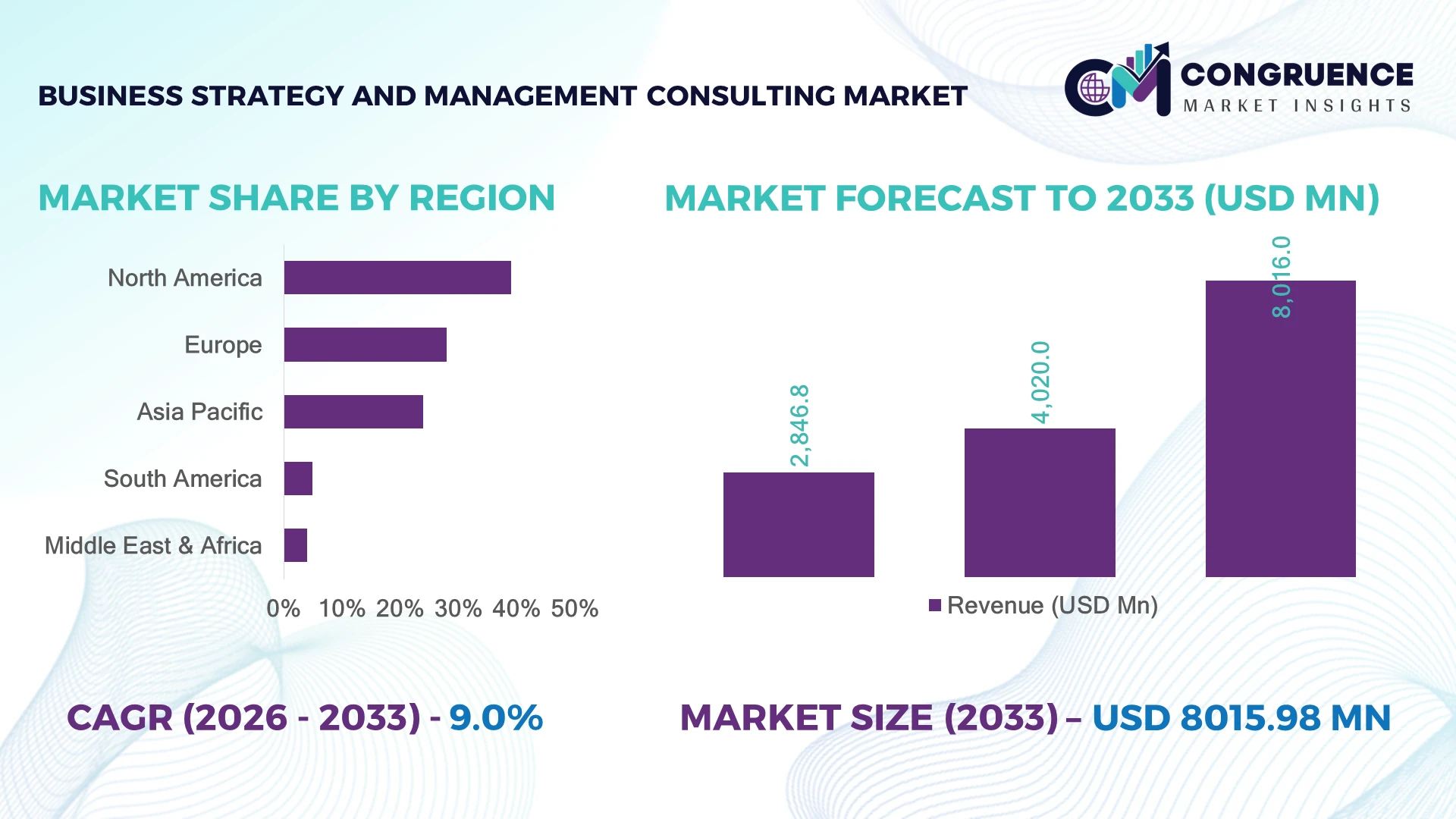

The Global Business Strategy and Management Consulting Market was valued at USD 4,020.0 Million in 2025 and is anticipated to reach a value of USD 8,016.0 Million by 2033 expanding at a CAGR of 9.01% between 2026 and 2033. Growth is being driven by enterprise-wide AI transformation programs, supply-chain redesign following Red Sea shipping disruptions, and rising demand for data-backed operating model optimization across manufacturing, financial services, and healthcare.

The United States dominates the global market with approximately 38% share, supported by over USD 120 billion in annual corporate transformation spending and strong adoption across technology, banking, and healthcare sectors. Large enterprises report AI-assisted consulting deployment in 52% of strategic initiatives, compared with 34% in Germany. Federal infrastructure modernization and reshoring programs continue to accelerate advisory engagement across North American industries.

Strategic implication: Firms that combine AI-enabled analytics with sector-specific execution capabilities are securing stronger board-level influence and longer-duration transformation mandates.

Market Size & Growth: USD 4,020.0 million in 2025, projected to reach USD 8,016.0 million by 2033 at 9.01% CAGR, driven by enterprise AI transformation and operating model redesign.

Top Growth Drivers: AI-enabled strategy programs (+52%), supply-chain restructuring (+41%), and regulatory compliance modernization (+33%).

Short-Term Forecast: By 2028, organizations are expected to reduce strategic planning cycle times by 30% and improve decision accuracy by 22%.

Emerging Technologies: Generative AI, process mining, digital twins, and advanced automation are becoming core consulting delivery tools.

Regional Leaders: North America (~USD 3.0B) leads digital transformation; Europe (~USD 2.2B) advances ESG and compliance advisory; Asia-Pacific (~USD 1.9B) accelerates manufacturing and infrastructure consulting.

Consumer/End-User Trends: 58% of large enterprises now prioritize AI governance, cost optimization, and resilience planning in consulting engagements.

Pilot/Case Example: In 2025, a global manufacturer’s AI-enabled network redesign reduced inventory holding costs by 18% and improved service levels by 11%.

Competitive Landscape: Top-tier firms collectively hold roughly 45% share, led by McKinsey & Company, Boston Consulting Group, Bain & Company, Deloitte, and Accenture.

Regulatory & ESG Impact: ESG disclosure and AI-governance mandates increased compliance-related advisory demand by 27% across major economies.

Investment & Funding: More than USD 18 billion in digital-transformation partnerships, capability expansion, and analytics platform investments was announced across the consulting ecosystem.

Innovation & Future Outlook: Autonomous decision-support platforms, industry-specific AI agents, and outcome-based consulting contracts are reshaping competitive positioning and global delivery models.

The Business Strategy and Management Consulting Market is increasingly focused on AI-led enterprise transformation, supply-chain resilience, and regulatory readiness across manufacturing, healthcare, and financial services. Generative AI and process-mining platforms are shortening diagnostic cycles, while 58% of large enterprises now prioritize data-driven operating model redesign. Recent Red Sea logistics disruptions have intensified network optimization projects, reinforcing the market’s shift toward execution-oriented, technology-enabled strategic advisory solutions and setting the stage for the broader strategic discussion.

The Business Strategy and Management Consulting Market has become a critical lever for competitive positioning as companies confront digital disruption, supply-chain restructuring, and tighter regulatory oversight. Boards are increasingly using external advisors to accelerate AI adoption, redesign operating models, and improve capital allocation. The shift toward resilient sourcing networks after recent global logistics disruptions has elevated consulting from a periodic planning function to a continuous transformation capability.

Technology-enabled consulting is delivering measurable operational gains. AI-assisted analytics platforms can reduce strategic assessment time by 35% and lower project delivery costs by 20% compared with traditional manual benchmarking approaches. North America leads large-scale enterprise transformation programs, while Asia-Pacific is expanding faster in manufacturing modernization and infrastructure advisory. Over the next 2–3 years, AI-governance, cybersecurity, and supply-chain optimization engagements are expected to account for a growing share of consulting mandates.

A practical example is the deployment of digital control-tower advisory programs that integrate procurement, logistics, and demand forecasting into a unified decision framework. Companies are responding by increasing investments in analytics capabilities, regional delivery centers, and technology partnerships. The strongest long-term advantage will belong to firms that combine deep industry expertise with AI-enabled execution, creating faster decision cycles, stronger resilience, and more defensible competitive positions.

Enterprise-wide digital transformation has become the strongest structural driver for the Business Strategy and Management Consulting Market as organizations accelerate AI adoption, operating model redesign, and resilience planning. More than 61% of Fortune 500 companies have expanded AI-led business transformation initiatives, while nearly 48% of executives prioritize enterprise-wide productivity programs over isolated technology investments. The introduction of stricter AI governance frameworks in the United States and the EU AI Act has increased demand for governance, compliance, and operating-model advisory services. This shift is pushing consulting firms to establish dedicated AI transformation practices, acquire specialist analytics companies, and expand cloud partnerships. A notable strategic outcome is the convergence of strategy consulting with implementation services, enabling firms to secure longer-duration engagements while delivering measurable operational improvements.

Persistent shortages of experienced strategy consultants and AI specialists continue to constrain project scalability and delivery quality. Industry estimates indicate that over 44% of consulting firms face difficulties recruiting advanced analytics and digital transformation experts, while employee attrition in consulting remains above 18% in several developed markets. Simultaneously, evolving privacy regulations and cross-border data governance requirements complicate multinational consulting engagements, particularly for global financial institutions operating across the United States and Europe. These structural pressures increase project costs, extend implementation timelines, and reduce resource utilization. To mitigate these challenges, firms are expanding offshore capability centers in India, strengthening internal digital academies, and adopting standardized consulting frameworks that improve deployment consistency while reducing dependence on scarce specialist talent.

Significant opportunity is emerging through sector-focused consulting platforms designed for healthcare, manufacturing, energy, and financial services. Nearly 57% of mid-sized enterprises are increasing investments in digital operating models, while AI-enabled workflow automation has demonstrated productivity improvements exceeding 30% across enterprise transformation programs. Japan's industrial modernization initiatives and India's expanding digital public infrastructure are creating new advisory opportunities beyond traditional multinational clients. Consulting firms are responding by developing proprietary AI accelerators, forming cloud ecosystem partnerships, and investing in industry-specific intellectual property rather than relying solely on labor-intensive advisory models. A distinctive strategic advantage lies in subscription-based transformation platforms that provide continuous performance monitoring, strengthening long-term client relationships while expanding recurring advisory engagements.

The rapid integration of generative AI into consulting workflows introduces significant execution complexity despite its productivity advantages. Approximately 53% of enterprises identify data governance as the primary barrier to enterprise AI deployment, while 41% report concerns regarding model transparency and decision accountability. As organizations increasingly expect faster, technology-enabled consulting engagements, maintaining analytical accuracy, cybersecurity resilience, and regulatory compliance becomes more demanding. In countries such as Germany and the United States, heightened scrutiny of AI-assisted business decisions is increasing quality assurance requirements. Consulting firms must therefore invest in explainable AI, secure data architectures, workforce upskilling, and strategic technology alliances to ensure scalable delivery without compromising client trust, competitive differentiation, or long-term operational credibility.

AI-Native Consulting Delivery – Consulting firms are embedding generative AI, knowledge graphs, and autonomous research assistants into core engagement workflows. More than 56% of strategy projects now incorporate AI-assisted analysis, reducing proposal development time by 35% while improving data synthesis accuracy. Following enterprise AI governance initiatives in the United States and Europe, firms are expanding proprietary AI platforms, establishing technology alliances, and standardizing digital delivery models to increase consultant productivity without proportionally expanding headcount.

Outcome-Based Commercial Models – Clients increasingly prefer performance-linked consulting contracts over traditional time-based engagements. Nearly 42% of large transformation programs now include milestone-based pricing, while measurable operational KPIs have improved project accountability by approximately 24%. Global manufacturers responding to continuing supply-chain restructuring are demanding execution-focused advisory services, prompting consulting firms to integrate implementation, analytics, and change management into unified transformation offerings.

Sector-Specific Advisory Expansion – Consulting providers are replacing generic methodologies with industry-specialized solutions for healthcare, financial services, energy, and advanced manufacturing. Approximately 49% of enterprise clients now prioritize advisors possessing sector-specific digital expertise, while customized transformation frameworks reduce implementation delays by 21%. Firms are responding through strategic acquisitions, specialized delivery teams, and industry-focused technology partnerships that strengthen competitive differentiation and long-term client retention.

Global Capability Center Growth – India has become a strategic hub for consulting operations as firms expand Global Capability Centers supporting analytics, research, cybersecurity, and digital engineering. Nearly 38% of new consulting capability investments target integrated delivery centers, while hybrid consulting models improve project scalability by 27%. This operational restructuring enables continuous client support across time zones, accelerates knowledge transfer, and strengthens enterprise resilience against ongoing labor-market and operational cost pressures.

Technology Advisory represents the leading segment, accounting for nearly 34% of consulting engagements as enterprises accelerate AI deployment, cloud modernization, cybersecurity enhancement, and digital operating model transformation. Organizations increasingly require integrated technology roadmaps aligned with business objectives, making technology-led advisory central to enterprise strategy. Strategy Advisory continues to maintain strong demand among board-level clients managing mergers, market expansion, and portfolio optimization, while Operations Advisory remains essential for manufacturing efficiency and supply-chain redesign initiatives. Financial Advisory is emerging as the fastest-growing segment as organizations strengthen capital allocation, restructuring, and risk management capabilities amid changing regulatory requirements. Approximately 46% of multinational enterprises now integrate financial transformation with enterprise technology programs, while HR Advisory gains momentum through workforce transformation, leadership development, and AI-enabled talent strategies. Consulting firms are investing in proprietary digital platforms, industry accelerators, and strategic partnerships to deliver integrated advisory solutions, reflecting a clear shift from standalone consulting engagements toward end-to-end business transformation services.

BFSI remains the largest application segment, contributing approximately 29% of overall consulting demand due to continuous regulatory compliance, digital banking modernization, cybersecurity investment, and operational risk management. Financial institutions increasingly rely on external advisors to optimize operating models, implement AI governance frameworks, and strengthen customer experience strategies. Manufacturing continues to expand consulting adoption through smart factory deployment and supply-chain optimization, while Government & Public Sector engagements are increasing alongside infrastructure modernization and digital public service initiatives. Healthcare & Life Sciences represent the fastest-growing application segment as providers accelerate digital health adoption, operational efficiency programs, and data-driven care delivery. Nearly 54% of large healthcare organizations are prioritizing enterprise transformation initiatives, while IT & Telecommunications firms continue expanding cloud-native infrastructure and AI-enabled service models. Retail & Consumer Goods companies are deploying predictive analytics and omnichannel operating strategies to improve customer retention and inventory optimization. Consulting providers are strengthening industry-specific delivery teams and expanding ecosystem partnerships to address increasingly specialized enterprise transformation requirements.

Large Enterprises dominate the Business Strategy and Management Consulting Market, representing approximately 72% of total consulting engagements due to complex organizational structures, multinational operations, and continuous transformation requirements. These organizations invest heavily in strategic planning, digital modernization, ESG implementation, cybersecurity governance, and post-merger integration. More than 60% of Fortune 500 companies maintain long-term consulting relationships spanning strategy, implementation, and operational optimization, enabling consulting firms to expand multidisciplinary service portfolios and establish multi-year transformation partnerships. Small & Medium Enterprises (SMEs) constitute the fastest-growing end-user segment as affordable cloud technologies and AI-powered consulting platforms reduce barriers to accessing high-value advisory services. Around 47% of mid-sized businesses are increasing external consulting investments to accelerate digital transformation, improve operational resilience, and enhance competitive positioning. Consulting firms are responding through modular service offerings, subscription-based advisory models, and scalable digital consulting platforms tailored to SME budgets. This shift is expanding market accessibility while creating new recurring engagement opportunities beyond traditional enterprise clients.

North America accounted for the largest market share at 39.0% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2026 and 2033.

North America remains the largest contributor to the Business Strategy and Management Consulting Market, supported by high enterprise technology spending, mature corporate governance frameworks, and strong adoption of AI-enabled transformation programs. The region contributes approximately 39% of global market demand, with consulting engagements concentrated across financial services, healthcare, technology, and advanced manufacturing. More than 60% of Fortune 500 companies maintain long-term consulting partnerships for digital modernization, cybersecurity, and operational restructuring. Increased federal infrastructure programs, cloud migration initiatives, and enterprise AI governance requirements continue to accelerate strategic advisory deployments. Consulting firms are expanding specialized AI, ESG, and cybersecurity practices while strengthening alliances with cloud platform providers to improve implementation capabilities and enterprise-scale execution.

United States Market Outlook: The United States represents the largest national market owing to its concentration of multinational corporations, digital-first enterprises, and innovation-driven industries. Nearly 52% of large enterprises have integrated AI-assisted strategic planning into business transformation initiatives, while continued investments in semiconductor manufacturing, infrastructure modernization, and cloud adoption are expanding consulting opportunities. Leading consulting firms continue strengthening industry-focused digital practices, analytics capabilities, and implementation partnerships to support increasingly complex enterprise transformation programs.

Europe continues to expand through regulatory modernization, sustainability initiatives, and industrial digitalization. The region accounts for nearly 28% of global consulting demand, supported by manufacturing, automotive, financial services, and energy industries. ESG reporting requirements, the EU AI Act, and enterprise decarbonization strategies are increasing demand for governance, compliance, and organizational transformation advisory services. More than 45% of large industrial enterprises are integrating digital operating models with sustainability objectives. Consulting firms are responding by expanding ESG advisory teams, regulatory compliance practices, and digital transformation partnerships to support long-term modernization across complex industrial ecosystems.

Germany Market Outlook: Germany remains Europe's strategic consulting hub due to its advanced manufacturing base, engineering leadership, and strong Industry 4.0 adoption. Automotive, industrial automation, and industrial software sectors continue investing heavily in operational excellence and digital transformation programs. Approximately 48% of large German manufacturers have accelerated AI-enabled production planning and supply-chain optimization initiatives, creating sustained demand for technology strategy, operational consulting, and organizational transformation expertise.

Asia-Pacific is the fastest-expanding regional market, driven by industrial modernization, digital infrastructure investment, and enterprise technology adoption across emerging economies. The region represents approximately 24% of global market activity, with rapid consulting deployment across manufacturing, telecommunications, financial services, and public infrastructure. Enterprise cloud migration and AI implementation continue accelerating, while digital government initiatives strengthen advisory demand. More than 43% of new enterprise transformation projects incorporate AI-enabled business process redesign. Global consulting firms are expanding delivery centers, innovation hubs, and regional partnerships to support increasing project volumes and sector-specific transformation requirements.

India Market Outlook: India has emerged as a global consulting and digital transformation powerhouse supported by its extensive technology workforce, expanding Global Capability Centers, and nationwide digital public infrastructure. More than 1,800 Global Capability Centers now support multinational organizations through analytics, engineering, cybersecurity, and consulting services. Continued investments in Digital India, manufacturing modernization, and AI adoption are strengthening India's position as both a high-value consulting market and a strategic global delivery hub.

South America continues strengthening consulting demand through enterprise modernization, financial sector digitalization, and infrastructure investment despite macroeconomic volatility. The region contributes approximately 5% of global consulting activity, with increasing advisory engagements across mining, agriculture, banking, and energy industries. Large organizations are prioritizing operational efficiency, digital customer experience, and supply-chain resilience to improve competitiveness. Public-private partnerships supporting transportation and energy infrastructure are also expanding strategic consulting opportunities. Consulting firms are localizing service delivery, strengthening regional partnerships, and deploying cloud-based advisory platforms to improve project accessibility and execution consistency.

Brazil Market Outlook: Brazil remains the largest consulting market in South America owing to its diversified industrial economy and accelerating enterprise digital transformation initiatives. Financial institutions, agribusiness companies, and energy organizations continue investing in operational optimization and AI-enabled decision support. Around 44% of large Brazilian enterprises have expanded digital transformation programs, encouraging consulting firms to establish regional innovation centers and deepen technology partnerships supporting enterprise modernization.

The Middle East & Africa market is expanding through economic diversification, infrastructure modernization, and public-sector transformation initiatives. The region accounts for roughly 4% of global consulting demand, with government-led investment programs creating sustained opportunities across smart cities, energy transition, healthcare, and digital government. Major national development strategies continue accelerating enterprise restructuring, organizational modernization, and digital governance projects. Consulting firms are increasing regional office networks, forming public-sector partnerships, and investing in specialized advisory capabilities to support complex national transformation agendas and long-term economic diversification objectives.

Saudi Arabia Market Outlook: Saudi Arabia represents the region's most strategically significant consulting market due to large-scale national transformation programs under Vision 2030. Public investment initiatives across tourism, renewable energy, logistics, and smart infrastructure continue generating substantial advisory requirements. More than 60% of large government transformation programs involve international consulting expertise, while expanding private-sector participation is encouraging consulting firms to establish permanent regional headquarters, specialized delivery teams, and long-term strategic partnerships.

The market is led by McKinsey & Company, Boston Consulting Group (BCG), Bain & Company, Accenture, and Deloitte, which collectively control approximately 46% of global consulting activity. Competition primarily exists between strategy specialists (McKinsey, BCG, Bain) and integrated consulting providers (Accenture, Deloitte), while regional firms compete through localized expertise and lower-cost delivery. Competitive advantage increasingly depends on AI-enabled consulting platforms, implementation capability, and industry specialization rather than pricing alone. AI-assisted delivery has reduced project analysis time by nearly 35%, while outcome-based commercial models now represent over 40% of large transformation engagements. Firms are expanding through cloud partnerships, AI acquisitions, Global Capability Centers, and industry-focused digital platforms. The market is shifting from advisory-only engagements toward technology-enabled execution and recurring transformation services. Strong brand reputation, proprietary intellectual property, enterprise relationships, and highly specialized consulting talent remain significant entry barriers. Winning requires combining strategic insight, scalable AI capabilities, measurable business outcomes, and industry-specific execution with trusted long-term client relationships.

Boston Consulting Group (BCG)

Accenture

Bain & Company

Deloitte

PwC

EY

KPMG

Capgemini

IBM Consulting

Oliver Wyman

Roland Berger

Kearney

L.E.K. Consulting

Artificial intelligence has become the defining technology shaping consulting engagements. Generative AI, agentic AI, predictive analytics, and knowledge graph platforms are automating research, benchmarking, and strategic scenario modeling. More than 60% of leading consulting firms have embedded AI into proposal generation and project delivery, while AI-assisted workflows improve consultant productivity by approximately 35% and reduce research effort by 40%. Cloud-native collaboration platforms and process mining solutions further accelerate enterprise transformation by integrating operational and strategic data into unified advisory environments.

Traditional consulting relied heavily on manual benchmarking, interviews, and spreadsheet-based analysis. Modern AI-enabled consulting platforms reduce strategic assessment cycles by nearly 30%, improve decision-support accuracy by over 25%, and enable continuous performance monitoring instead of one-time recommendations. Global consulting leaders with proprietary AI platforms benefit through stronger client retention, faster implementation, and outcome-based commercial models, while smaller firms leverage specialized automation tools to compete through agility and niche expertise.

Between 2026 and 2028, autonomous business agents, enterprise digital twins, explainable AI, and multimodal decision-support systems will redefine consulting delivery. Organizations are expected to expand AI-enabled transformation programs beyond pilot deployments, increasing enterprise adoption above 70% for digital strategy initiatives. Companies investing now in proprietary AI capabilities, secure data architectures, and industry-specific automation platforms will secure lasting operational differentiation and stronger competitive positioning.

February 2026 – McKinsey & Company: Joined OpenAI's Frontier Alliances to accelerate enterprise AI deployment with forward-deployed engineering support, enabling faster production-scale implementation across corporate environments. The initiative targets 100% enterprise-scale deployment readiness rather than pilot programs. Business impact: stronger AI transformation capabilities. Source: www.eweek.com

April 2026 – Accenture: Expanded its strategic partnership with Google Cloud through the Gemini Enterprise Acceleration Program, combining thousands of AI-skilled engineers with industry specialists to deploy enterprise AI agents at scale. Business impact: accelerated AI implementation and industry-specific transformation delivery.

April 2026 – Boston Consulting Group: Expanded its partnership with Google Cloud to help enterprises move beyond AI pilots toward production-scale agentic transformation. The initiative focuses on enterprise-wide AI adoption with measurable operational outcomes. Business impact: stronger execution capability and scalable AI transformation services.

March 2026 – Accenture: Launched the Accenture Databricks Business Group with support from more than 25,000 Databricks-trained professionals to accelerate enterprise AI applications and agent deployment. Business impact: strengthened data modernization, AI implementation capacity, and global consulting delivery.

The report delivers comprehensive analysis across five service types, seven application sectors, two end-user groups, and five major geographic regions, providing strategic coverage of the evolving Business Strategy and Management Consulting Market. It evaluates Technology Advisory, Strategy Advisory, Operations Advisory, Financial Advisory, and HR Advisory while examining enterprise demand across BFSI, manufacturing, healthcare, IT & telecommunications, retail, government, and other industries. The assessment incorporates deployment trends, AI adoption patterns, digital transformation priorities, consulting delivery evolution, and competitive positioning across mature and emerging markets.

The study further examines enterprise purchasing behavior, regional investment patterns, technology integration, and operational transformation strategies between 2026 and 2033. It profiles leading consulting providers, evaluates AI-enabled consulting platforms, cloud-based advisory models, process automation, and emerging digital transformation ecosystems. The report supports investment planning, market expansion, competitive benchmarking, partnership evaluation, portfolio optimization, and long-term strategic decision-making by identifying high-opportunity segments, technology shifts, evolving client requirements, and sustainable competitive advantages across the global consulting landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,020.0 Million |

| Market Revenue (2033) | USD 8,016.0 Million |

| CAGR (2026–2033) | 9.01% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | McKinsey & Company; Boston Consulting Group (BCG); Accenture; Bain & Company; Deloitte; PwC; EY; KPMG; Capgemini; IBM Consulting; Oliver Wyman; Roland Berger; Kearney; L.E.K. Consulting |

| Customization & Pricing | Available on Request (10% Customization Free) |