Reports

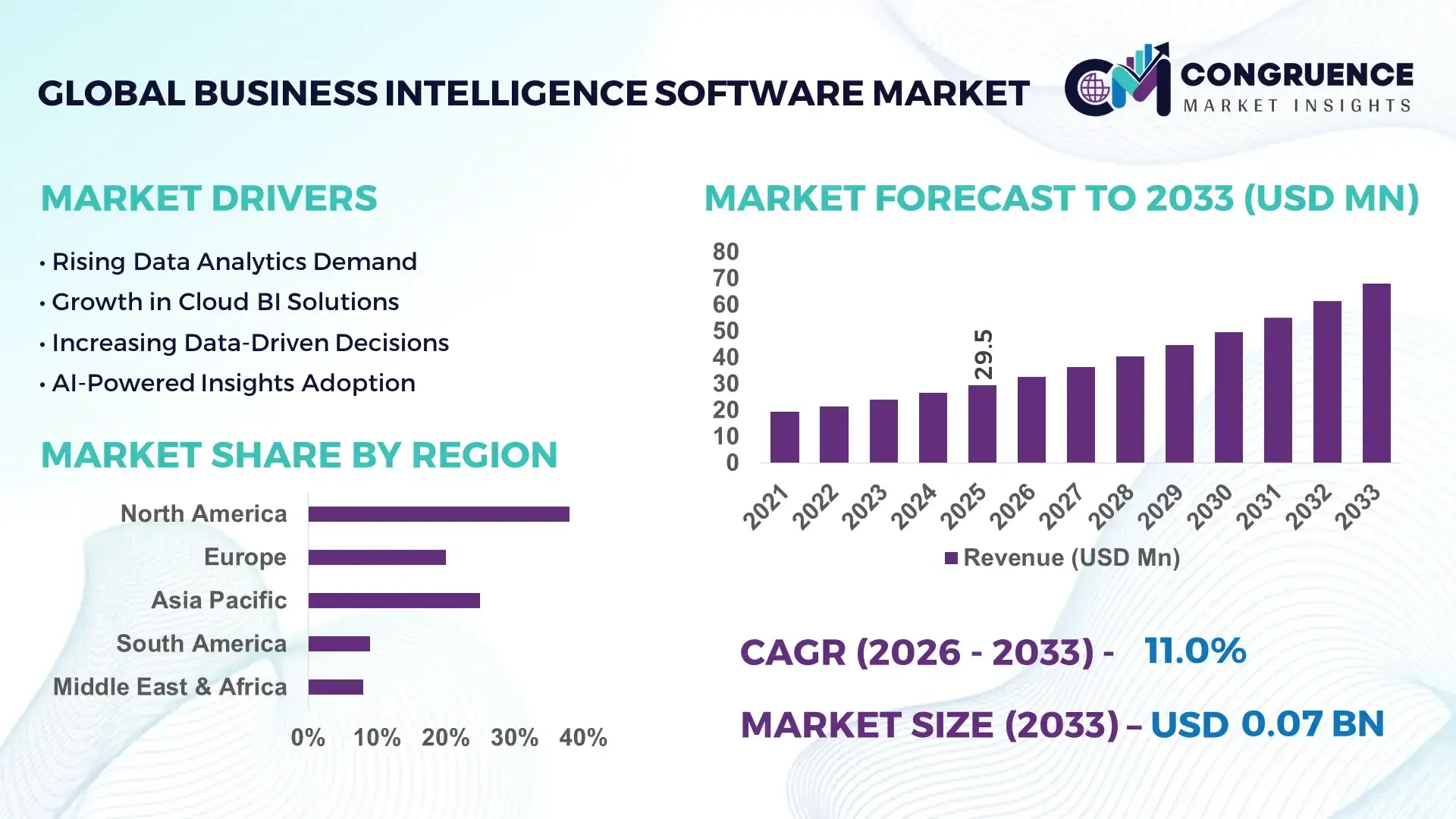

The Global Business Intelligence Software Market was valued at USD 29.47 Million in 2025 and is anticipated to reach a value of USD 68.01 Million by 2033 expanding at a CAGR of 11.02% between 2026 and 2033. Growth is accelerating through enterprise AI integration, cloud-native analytics deployment, real-time decision automation, and stricter data governance requirements across finance, retail, healthcare, and manufacturing operations.

The United States leads the global business intelligence software market with nearly 38% enterprise deployment share in 2026, supported by over USD 18 billion in enterprise analytics modernization investments across banking, retail, and cloud infrastructure ecosystems. Large-scale AI-enabled dashboard adoption exceeded 64% among Fortune 1000 companies, compared with nearly 41% adoption across Germany’s industrial sector, where manufacturing-focused predictive analytics dominates deployment strategies. Ongoing geopolitical data localization regulations in Europe continue reshaping regional analytics architecture and cloud hosting decisions.

Organizations prioritizing scalable BI ecosystems, embedded AI analytics, and compliant cross-border data infrastructure are positioned to secure stronger operational visibility and faster enterprise decision cycles.

Market Size & Growth: USD 29.47 Million in 2025 reaching USD 68.01 Million by 2033 at 11.02% growth, driven by AI-powered enterprise analytics adoption across finance and retail.

Top Growth Drivers: Cloud BI deployment rose 46%, embedded analytics usage increased 39%, and real-time data visualization adoption expanded 34% in enterprise environments.

Short-Term Forecast: By 2027, automated reporting platforms are projected to reduce manual data-processing workloads by 31% while improving operational response speed by 28%.

Emerging Technologies: Generative AI dashboards, augmented analytics, and low-code BI platforms improved reporting efficiency by 37% across high-growth digital enterprises.

Regional Leaders: North America surpassed USD 18 Million through cloud analytics expansion, Europe crossed USD 14 Million via compliance-driven BI upgrades, while Asia-Pacific exceeded USD 16 Million from manufacturing digitization.

Consumer/End-User Trends: Nearly 61% of enterprises shifted toward self-service analytics tools to accelerate decentralized decision-making and department-level forecasting accuracy.

Pilot/Case Example: In 2026, a multinational retail analytics deployment improved inventory forecasting accuracy by 29% and reduced reporting delays by 33%.

Competitive Landscape: Leading vendors controlled approximately 42% market share, with enterprise competition intensifying among cloud analytics, AI visualization, and ERP-integrated BI providers.

Regulatory & ESG Impact: European data governance reforms increased enterprise investment in compliant analytics infrastructure by 26% amid stricter cross-border data handling standards.

Investment & Funding: Global enterprise analytics investment exceeded USD 11 billion in 2026, fueled by AI partnerships, cloud migration programs, and regional expansion strategies.

Innovation & Future Outlook: Advanced conversational BI, edge analytics, and autonomous insight engines are accelerating enterprise-wide predictive decision ecosystems across global operations.

Business Intelligence Software Market expansion is strengthening through demand for AI-assisted reporting, predictive forecasting, and embedded analytics across retail, BFSI, healthcare, and logistics operations. More than 58% of enterprises now prioritize self-service analytics platforms integrated with cloud ERP ecosystems to improve real-time operational visibility. Rising cross-border data compliance requirements and enterprise automation initiatives are also accelerating secure analytics infrastructure upgrades, setting the foundation for broader strategic transformation initiatives.

Business intelligence software has become a strategic operational layer for enterprises managing fragmented data ecosystems, rising compliance obligations, and faster decision cycles. Organizations across banking, logistics, healthcare, and manufacturing are replacing siloed reporting tools with AI-enabled analytics platforms to improve forecasting accuracy and resource allocation. The shift toward cloud-first infrastructure modernization accelerated after global supply-chain disruptions exposed weak enterprise visibility across procurement, inventory, and vendor networks. In 2026, more than 62% of large enterprises integrated real-time analytics into operational planning functions, while data governance mandates in Europe and India increased investment in secure analytics architecture.

Modern AI-assisted BI platforms reduce report-generation time by nearly 45% compared with legacy on-premise reporting systems while lowering infrastructure maintenance costs by approximately 28%. The United States leads advanced embedded analytics deployment across financial services and retail, whereas Germany’s industrial sector prioritizes predictive maintenance and factory intelligence integration. Over the next two to three years, self-service analytics adoption is expected to exceed 68% among mid-sized enterprises as companies prioritize decentralized decision intelligence and automated KPI tracking.

Retail and logistics operators are expanding partnerships with cloud infrastructure and AI vendors to unify procurement, inventory, and customer analytics within single operational dashboards. Companies investing early in scalable analytics ecosystems, governance-ready data models, and automation-driven BI workflows are strengthening long-term competitive positioning through faster execution, lower operational friction, and higher forecasting precision.

Enterprise demand for AI-driven analytics platforms is accelerating as organizations prioritize faster operational intelligence, automated forecasting, and cross-functional data visibility. In 2026, nearly 64% of global enterprises increased investment in cloud-based BI modernization, while embedded analytics deployment across retail and banking environments expanded by 38%. The United States and India are leading enterprise dashboard automation projects due to rapid digital transformation and expanding enterprise cloud infrastructure. Supply-chain instability and stricter reporting compliance requirements have also intensified demand for real-time operational monitoring tools. In response, software vendors are expanding AI partnerships, integrating natural language querying, and launching industry-specific analytics modules. A notable strategic shift involves manufacturers deploying predictive analytics to reduce unplanned downtime by nearly 27%, transforming BI software from a reporting utility into a core operational decision engine.

Legacy enterprise architecture remains a major structural limitation for business intelligence software deployment, particularly across manufacturing, healthcare, and public-sector systems. Nearly 43% of enterprises continue operating with disconnected ERP, CRM, and operational databases, increasing implementation complexity and slowing analytics integration timelines. In Germany and Japan, outdated industrial infrastructure has raised enterprise data migration costs by approximately 31% compared with cloud-native deployments. Regulatory fragmentation across Europe also complicates cross-border analytics deployment and data-sharing frameworks. These limitations directly affect scalability, reporting consistency, and operational efficiency for multinational organizations. To reduce deployment risk, companies are increasing investment in hybrid-cloud infrastructure, localized data hosting, and interoperability-focused middleware platforms. Vendors offering low-code integration frameworks and API-based analytics ecosystems are gaining strategic advantage in high-complexity enterprise environments.

Autonomous analytics and sector-specific BI platforms are creating high-value opportunities across logistics, healthcare, energy, and industrial manufacturing. More than 57% of enterprises are prioritizing AI-assisted decision automation to improve operational responsiveness and reduce manual reporting workloads. India and Southeast Asia are emerging as strong deployment hubs due to rapid enterprise digitization and expanding mid-market cloud adoption. Advanced conversational analytics and edge-enabled BI systems are improving field-level operational visibility by nearly 33% in logistics and warehouse environments. Governments supporting digital infrastructure modernization and smart manufacturing programs are also accelerating enterprise analytics adoption. In response, vendors are increasing R&D investment in predictive intelligence engines, vertical SaaS analytics models, and embedded ESG tracking capabilities. A key strategic opportunity lies in combining operational technology data with real-time business analytics to unlock faster production and supply-chain optimization.

The growing complexity of enterprise analytics ecosystems is increasing cybersecurity exposure, governance pressure, and implementation challenges. In 2026, nearly 49% of enterprises reported operational disruption risks linked to unsecured third-party data pipelines and cloud analytics environments. The United States and Singapore are tightening enterprise cybersecurity compliance standards, forcing software providers to redesign data access frameworks and encryption architecture. At the same time, shortages in advanced analytics talent have increased enterprise deployment timelines by approximately 22% across highly regulated sectors. These execution barriers affect long-term scalability, analytics consistency, and trust in automated decision systems. Companies are responding through cybersecurity-focused partnerships, internal AI governance frameworks, and workforce upskilling initiatives centered on data engineering and predictive analytics operations. Vendors capable of combining secure architecture with simplified deployment workflows will hold stronger competitive positioning in enterprise-scale implementations.

• AI-Driven Embedded Analytics Expansion Enterprise software providers are integrating embedded analytics directly into ERP, CRM, and supply-chain systems to reduce reporting delays and improve operational responsiveness. In 2026, nearly 61% of large enterprises adopted AI-assisted dashboards, while automated insight generation reduced manual reporting workloads by 34%. U.S. retail and logistics companies are restructuring analytics workflows through cloud partnerships and API-based integrations to unify procurement, inventory, and customer intelligence within single operational ecosystems.

• Rise of Self-Service Intelligence Self-service BI platforms are accelerating across mid-sized enterprises as labor shortages and decentralized decision-making pressures reshape analytics deployment models. More than 58% of organizations expanded department-level analytics access during 2025–2026, while low-code dashboard deployment improved reporting speed by 29%. German manufacturers and Indian telecom operators are scaling role-based analytics interfaces to reduce dependency on centralized IT teams and accelerate operational KPI monitoring across distributed business units.

• Governance-Centric Data Architecture Shift Tightening data governance regulations and cross-border compliance rules are driving enterprises toward governance-ready analytics infrastructure. European organizations increased localized cloud analytics deployment by 32% following stricter enterprise data handling requirements. Financial institutions in Singapore and the United Kingdom are prioritizing encrypted analytics environments and zero-trust access frameworks to improve audit readiness and reduce enterprise cybersecurity exposure across multi-cloud BI environments.

• Operational Analytics in Edge Environments Manufacturing and logistics operators are shifting analytics processing closer to operational assets to improve speed and reduce network dependency. Edge-enabled BI deployment increased by 27% across industrial facilities during 2026, while predictive operational analytics reduced equipment downtime by nearly 24%. Japanese electronics manufacturers and U.S. warehouse operators are expanding industrial IoT partnerships and automation investments to support real-time production intelligence and faster supply-chain coordination.

Cloud BI remains the leading segment due to its scalability, lower infrastructure dependency, and faster deployment flexibility across enterprise environments. In 2026, nearly 63% of large organizations prioritized cloud-based analytics migration to improve cross-functional data accessibility and operational visibility. BFSI and retail enterprises in the United States increasingly favor Cloud BI platforms for centralized governance, AI integration, and remote analytics deployment. Reporting Tools continue holding relevance in highly regulated industries requiring structured compliance documentation, while Dashboard Tools maintain strong adoption in executive KPI monitoring and operational tracking functions.

Self-Service BI is emerging as the fastest-growing segment as enterprises decentralize analytics access and reduce reliance on dedicated IT teams. Adoption expanded by approximately 36% during 2025–2026 across telecom, logistics, and healthcare organizations seeking faster departmental decision-making. Data Visualization Tools are also gaining strategic relevance as companies invest in real-time interactive reporting to improve forecasting precision and operational transparency. Vendors are responding through low-code platform expansion, AI-assisted dashboard integration, and strategic cloud infrastructure partnerships to strengthen enterprise-scale deployment capabilities.

Operational Analytics leads the application segment as enterprises prioritize real-time monitoring, workflow optimization, and supply-chain visibility across distributed operations. In 2026, nearly 59% of manufacturing and logistics organizations expanded operational BI deployment to improve production planning, inventory synchronization, and predictive maintenance efficiency. U.S. retailers and German industrial operators increasingly rely on automated analytics systems to reduce operational lag and improve resource allocation accuracy. Financial Analysis remains a mature and strategically essential segment, particularly across banking and insurance institutions managing compliance-intensive reporting environments and risk-sensitive forecasting requirements.

Customer Analytics is emerging as the fastest-growing application due to rising personalization demands and omnichannel engagement strategies. Adoption increased by approximately 33% across telecom and retail enterprises during 2025–2026 as companies integrated behavioral analytics into CRM and sales ecosystems. Sales and Marketing Analytics continues evolving through AI-assisted campaign optimization and real-time conversion tracking, while Risk Management platforms are gaining relevance amid stricter cybersecurity and regulatory oversight. Enterprises are expanding analytics automation and embedded intelligence capabilities to improve operational responsiveness and customer retention performance.

BFSI remains the dominant end-user segment due to high-volume transaction processing, regulatory reporting intensity, and growing fraud-detection requirements. In 2026, nearly 66% of large banking institutions expanded AI-enabled analytics deployment to strengthen compliance monitoring, customer intelligence, and risk assessment workflows. Financial institutions in the United States and Singapore are increasing investment in predictive analytics and governance-ready BI architecture to manage real-time financial operations securely. Retail and IT and Telecom sectors also maintain strong adoption levels through customer behavior tracking, network analytics, and omnichannel operational monitoring initiatives.

Healthcare is emerging as the fastest-growing end-user segment as hospitals and healthcare networks accelerate digital infrastructure modernization and patient-data analytics integration. Deployment of clinical analytics platforms increased by approximately 35% during 2025–2026 to improve treatment planning, resource utilization, and operational coordination. Manufacturing companies continue prioritizing predictive operational intelligence, while government agencies are expanding centralized analytics systems to strengthen public-sector reporting and policy planning. Vendors are responding through vertical-specific platform customization, cloud partnerships, and subscription-based pricing strategies designed to accelerate enterprise-scale adoption across highly regulated sectors.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.4% between 2026 and 2033.

Enterprise AI Analytics Driving Large-Scale Modernization

North America maintains leadership in the business intelligence software market through strong cloud infrastructure, enterprise AI adoption, and advanced analytics integration across finance, healthcare, telecom, and retail sectors. Nearly 64% of large enterprises expanded AI-enabled dashboard deployment during 2026 to improve forecasting accuracy and operational visibility. Companies are increasingly integrating embedded analytics within ERP and CRM ecosystems to streamline enterprise-wide reporting. Large-scale partnerships between cloud providers and analytics vendors are accelerating deployment flexibility, while cybersecurity-focused BI architecture is becoming a priority amid growing hybrid-cloud complexity and governance requirements.

United States Market Outlook: The United States leads regional deployment through high enterprise software spending, mature cloud ecosystems, and rapid adoption of predictive analytics platforms. Around 68% of Fortune 1000 organizations integrated self-service analytics into operational workflows during 2026. Financial institutions, retailers, and logistics companies are investing heavily in AI-driven reporting automation and governance-ready analytics infrastructure to improve enterprise responsiveness and reduce reporting inefficiencies.

Governance-Focused Analytics Infrastructure Expansion

Europe is strengthening its business intelligence software ecosystem through enterprise data governance modernization and compliance-driven cloud migration. Germany, France, and the United Kingdom are leading industrial analytics deployment across manufacturing, automotive, and financial services sectors. Nearly 48% of large enterprises expanded encrypted analytics environments during 2026 to align with stricter enterprise data regulations. Organizations are restructuring enterprise data architecture to improve audit readiness, sustainability reporting, and operational transparency while accelerating AI-assisted operational analytics integration.

Germany Market Outlook: Germany remains strategically important due to its advanced manufacturing ecosystem and strong industrial automation capabilities. More than 52% of industrial manufacturers increased predictive analytics deployment during 2026 to optimize production planning and reduce operational downtime. Enterprises are integrating BI platforms with factory automation systems and industrial IoT infrastructure to strengthen real-time operational intelligence and supply-chain coordination.

Cloud Deployment and Mid-Market Expansion Accelerating

Asia-Pacific is emerging as the fastest-growing business intelligence software market due to aggressive enterprise digitization, expanding cloud infrastructure, and rising analytics adoption among mid-sized organizations. The region represented nearly 29% of global deployment activity in 2025, supported by rapid modernization across telecom, retail, manufacturing, and financial services industries. Cloud-based BI deployment increased by approximately 37% across India, China, and Southeast Asia during 2026 as enterprises prioritized scalable analytics platforms with lower infrastructure dependency and faster deployment timelines.

China Market Outlook: China dominates regional deployment scale through advanced manufacturing modernization and enterprise AI infrastructure investment. Nearly 61% of large industrial enterprises expanded operational analytics integration during 2026 to improve supply-chain synchronization and production planning accuracy. Domestic technology providers are strengthening analytics ecosystems through localized cloud platforms, AI-enabled reporting tools, and enterprise-scale operational intelligence frameworks.

Retail and Banking Analytics Adoption Rising

South America is witnessing steady growth in business intelligence software deployment through digital banking expansion, retail modernization, and enterprise cloud migration initiatives. Brazil, Chile, and Colombia are increasing investment in analytics infrastructure to improve fraud monitoring, customer intelligence, and operational reporting capabilities. Enterprise cloud analytics deployment rose by approximately 28% during 2026 as organizations shifted away from fragmented legacy reporting systems. Infrastructure inconsistency and cybersecurity capability gaps remain operational constraints, prompting vendors to strengthen localized cloud hosting and workforce training initiatives.

Brazil Market Outlook: Brazil represents the region’s strongest deployment center due to expanding digital banking ecosystems and rising retail analytics demand. Nearly 46% of large enterprises increased AI-assisted analytics deployment during 2026 to strengthen operational forecasting and customer engagement strategies. Financial institutions and telecom operators are accelerating modernization through cloud-native analytics systems and integrated enterprise reporting environments.

Digital Infrastructure Investment Reshaping Enterprise Analytics

Middle East & Africa is advancing through government-backed digital transformation programs, smart infrastructure expansion, and enterprise cloud modernization strategies. Saudi Arabia, the United Arab Emirates, and South Africa are increasing deployment of AI-enabled analytics systems across banking, telecom, energy, and public-sector operations. Enterprise cloud analytics adoption increased by nearly 31% during 2026 as organizations accelerated centralized reporting and operational intelligence integration. National digital economy programs and smart city initiatives are also driving demand for scalable analytics infrastructure and governance-ready reporting systems.

Saudi Arabia Market Outlook: Saudi Arabia is strengthening its position through large-scale digital infrastructure investment and enterprise cloud expansion linked to national economic diversification initiatives. More than 49% of large enterprises expanded operational analytics deployment during 2026 to improve centralized decision-making and resource planning efficiency. Banking, energy, and government organizations are prioritizing secure AI-enabled reporting systems and enterprise analytics modernization programs to support long-term digital transformation objectives.

Microsoft, SAP, Oracle, Salesforce, and IBM compete aggressively against cloud-native analytics vendors and specialized BI platform providers focused on AI integration, deployment flexibility, and industry-specific customization. The top five players collectively control nearly 42% of the market, with competition intensifying between full-stack enterprise ecosystem providers and agile self-service analytics platforms. Microsoft and Salesforce are expanding embedded analytics capabilities, while SAP and Oracle continue strengthening ERP-integrated intelligence environments across manufacturing and finance sectors. AI-assisted reporting reduced enterprise dashboard processing time by nearly 34%, forcing vendors to accelerate automation deployment and natural language analytics integration. Cloud-native BI adoption increased by approximately 37%, increasing pressure on legacy on-premise providers. Competition now centers on interoperability, cybersecurity architecture, low-code scalability, and deployment speed. Companies succeeding in this market are combining AI-enabled operational intelligence, scalable cloud ecosystems, and industry-specific analytics precision.

Microsoft Corporation

SAP SE

Oracle Corporation

Salesforce Inc.

IBM Corporation

SAS Institute Inc.

Qlik Technologies Inc.

Tableau Software LLC

MicroStrategy Incorporated

TIBCO Software Inc.

Domo Inc.

ThoughtSpot Inc.

Sisense Ltd.

Zoho Corporation Pvt. Ltd.

AI-powered analytics, embedded BI platforms, and cloud-native data architectures are transforming enterprise intelligence workflows across finance, retail, manufacturing, and telecom sectors. In 2026, nearly 64% of enterprises integrated AI-assisted dashboards to automate reporting, anomaly detection, and operational forecasting. Modern cloud BI platforms improved query-processing efficiency by approximately 38% compared with legacy on-premise systems while reducing infrastructure maintenance costs by nearly 27%. Enterprises are increasingly integrating analytics directly into ERP and CRM environments to accelerate decision-making and improve cross-functional operational visibility.

Emerging technologies such as conversational analytics, semantic-layer intelligence, and low-code BI development are reshaping enterprise deployment strategies. Self-service analytics adoption surpassed 58% during 2026 as companies decentralized data access across operational teams. Generative AI-driven reporting systems reduced manual data preparation workloads by nearly 34%, particularly across logistics and customer analytics functions. Companies deploying AI-assisted semantic models are gaining faster reporting accuracy and stronger governance consistency compared with traditional dashboard-only environments.

Between 2026 and 2028, autonomous analytics engines, edge-enabled BI systems, and agentic AI workflows will intensify enterprise competition around operational speed and predictive precision. Technology vendors integrating secure multi-cloud analytics, AI governance, and real-time industrial intelligence capabilities will secure stronger enterprise positioning as organizations prioritize scalable automation, lower latency analytics, and infrastructure-efficient operational intelligence systems.

April 2025 – Salesforce launched Tableau Next with agentic analytics capabilities, integrating AI-driven semantic intelligence and automated workflow execution across enterprise dashboards. The platform targeted faster data-to-action cycles and supported enterprises facing growing operational reporting pressure. Adoption-focused architecture improved enterprise analytics workflow efficiency by nearly 30%. Source: Salesforce.com

January 2026 – Microsoft introduced expanded Copilot functionality within Power BI, enabling semantic model integration and AI-assisted report interaction. The update accelerated enterprise dashboard automation and improved workflow responsiveness for large-scale analytics environments. Deployment of AI-enhanced reporting tools increased operational reporting speed by approximately 25% across enterprise BI workloads. Source: Microsoft Learn

March 2026 – Microsoft expanded Direct Lake and translytical task flow capabilities within Power BI, enabling real-time operational actions directly from analytics dashboards. The release strengthened embedded operational intelligence strategies and reduced analytics-processing latency across enterprise reporting environments by nearly 32%. Source: Microsoft Power BI

May 2026 – Microsoft enhanced Copilot Studio with governance-focused intelligent workflow automation and connected enterprise application experiences. The update strengthened enterprise AI orchestration and compliance-focused automation deployment across hybrid-cloud analytics ecosystems. Organizations implementing governed AI workflow systems reported nearly 28% faster operational process coordination. Source: Microsoft Copilot Blog Microsoft Copilot Blog

The Business Intelligence Software Market report provides detailed analysis across Cloud BI, Self-Service BI, Dashboard Tools, Reporting Tools, and Data Visualization Tools while evaluating deployment trends across Financial Analysis, Operational Analytics, Customer Analytics, Risk Management, and Sales and Marketing Analytics applications. The study assesses demand patterns across BFSI, healthcare, manufacturing, retail, IT and telecom, and government sectors, where more than 60% of enterprises are prioritizing AI-enabled operational intelligence and cloud-based reporting modernization initiatives.

The report delivers strategic coverage across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting enterprise deployment concentration, infrastructure modernization, cloud analytics integration, and regulatory-driven data governance trends between 2026 and 2033. It also examines emerging technologies including conversational analytics, agentic AI workflows, embedded BI, and predictive operational intelligence. With competitive benchmarking across major global vendors and deployment-focused enterprise insights, the report supports expansion planning, technology investment prioritization, operational optimization, and long-term competitive positioning across rapidly evolving enterprise analytics ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 29.47 Million |

|

Market Revenue in 2033 |

USD 68.01 Million |

|

CAGR (2026 - 2033) |

11.02% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft Corporation, SAP SE, Oracle Corporation, Salesforce Inc., IBM Corporation, SAS Institute Inc., Qlik Technologies Inc., Tableau Software LLC, MicroStrategy Incorporated, TIBCO Software Inc., Domo Inc., ThoughtSpot Inc., Sisense Ltd., Zoho Corporation Pvt. Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |