Reports

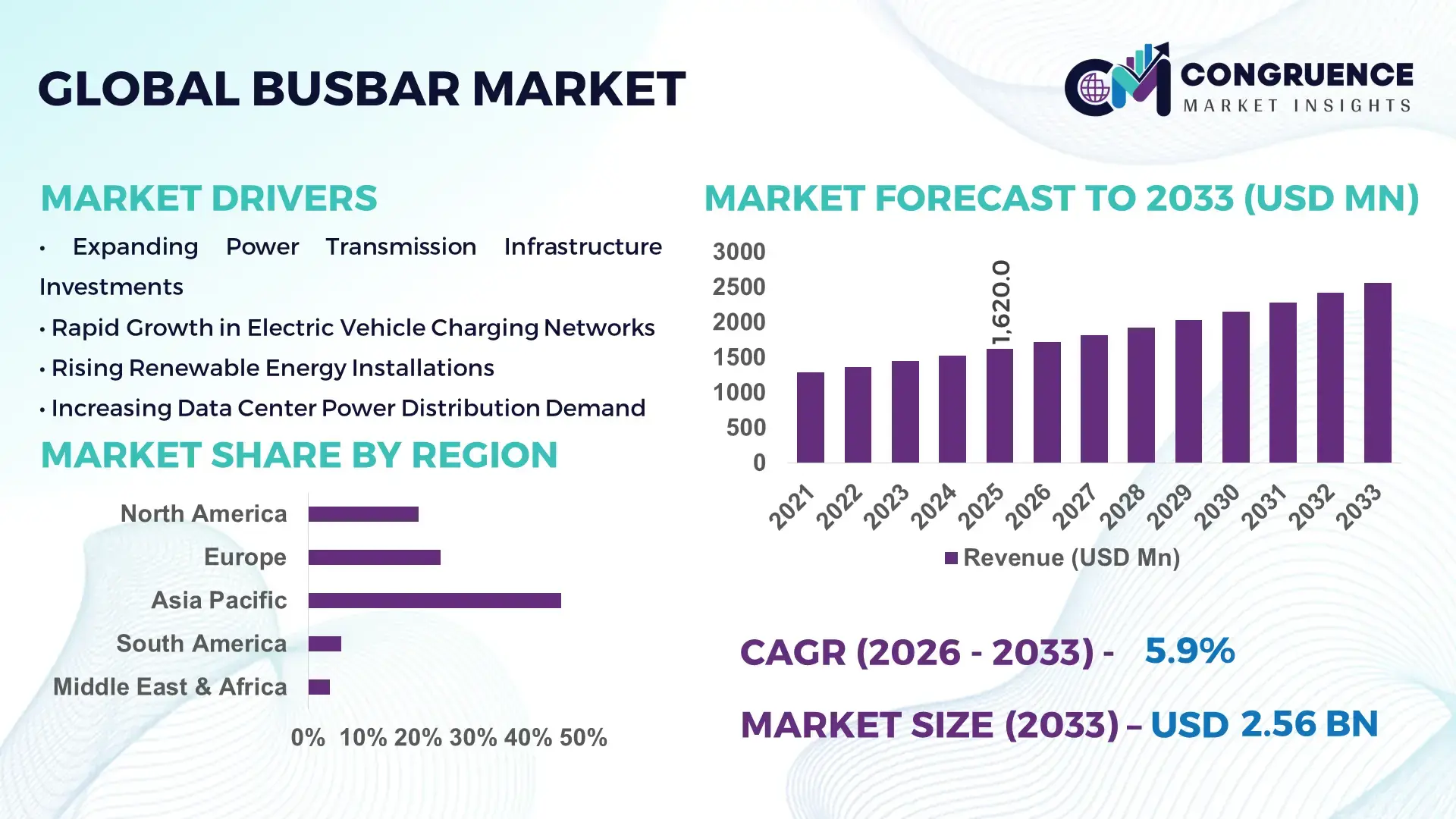

The Global Busbar Market was valued at USD 1,620.0 Million in 2025 and is anticipated to reach a value of USD 2,558.7 Million by 2033 expanding at a CAGR of 5.88% between 2026 and 2033, according to an analysis by Congruence Market Insights. Rising electrification across industrial, commercial, and renewable energy sectors is accelerating demand for efficient and compact power distribution systems.

China represents the dominant country in the Busbar Market in terms of manufacturing scale and industrial deployment. The country accounts for over 30% of global copper processing capacity and produces more than 11 million metric tons of refined copper annually, supporting large-scale busbar fabrication. China’s annual power generation capacity exceeds 2,900 GW, creating significant demand for low- and medium-voltage busbar systems across substations, industrial plants, and commercial infrastructure. Investments exceeding USD 100 billion annually in grid modernization and ultra-high-voltage (UHV) transmission projects have strengthened domestic production capabilities. Electric vehicle production surpassed 9 million units in 2023, increasing demand for laminated and high-conductivity busbars in battery packs and power electronics. Advanced automation in manufacturing clusters such as Jiangsu and Guangdong has improved production precision by nearly 20%, reinforcing China’s position as a high-volume and technology-integrated busbar production hub.

Market Size & Growth: Valued at USD 1,620.0 Million in 2025, projected to reach USD 2,558.7 Million by 2033 at 5.88% CAGR, driven by grid expansion and renewable integration.

Top Growth Drivers: Renewable energy integration (38%), industrial electrification (42%), EV adoption growth (35%).

Short-Term Forecast: By 2028, smart busbar monitoring systems are expected to reduce power losses by 12% and maintenance costs by 15%.

Emerging Technologies: Laminated busbars for EVs, IoT-enabled thermal monitoring, and aluminum alloy lightweight conductors.

Regional Leaders: Asia Pacific projected at USD 1,050 Million by 2033 with strong grid expansion; North America at USD 620 Million driven by data centers; Europe at USD 540 Million supported by renewable retrofits.

Consumer/End-User Trends: Utilities account for over 40% of installations, followed by industrial manufacturing and commercial data centers with rising compact system adoption.

Pilot or Case Example: In 2024, a smart substation project in Asia reduced downtime by 18% through integrated busbar thermal sensors.

Competitive Landscape: Siemens holds approximately 14% share, followed by Schneider Electric, ABB, Eaton, and Mitsubishi Electric.

Regulatory & ESG Impact: Energy efficiency mandates targeting 20% reduction in transmission losses by 2030 are accelerating advanced conductor deployment.

Investment & Funding Patterns: Over USD 3.5 Billion invested globally in grid modernization and electrification projects during 2023–2025.

Innovation & Future Outlook: Integration with smart grids, AI-based load balancing, and recyclable aluminum conductors are shaping long-term scalability.

Power utilities contribute nearly 40% of demand, followed by industrial plants at 30% and commercial infrastructure at 20%. Laminated copper busbars improve thermal efficiency by up to 15%, supporting EV and inverter applications. Stringent grid-efficiency regulations targeting 10–20% transmission loss reduction are accelerating adoption in Asia Pacific and Europe. Increasing renewable penetration beyond 30% of installed capacity in several economies is reinforcing compact, high-capacity busbar integration.

The Busbar Market holds strategic relevance as industries transition toward electrified, decentralized, and digitally monitored power ecosystems. Busbars serve as the backbone of power distribution in substations, industrial facilities, renewable energy plants, electric vehicle charging hubs, and hyperscale data centers. With global electricity demand projected to rise by over 25% by 2030, infrastructure resilience and energy efficiency have become executive-level priorities. Advanced laminated busbar technology delivers 15%–20% thermal efficiency improvement compared to traditional cable-based distribution systems, enhancing reliability in high-load environments.

Asia Pacific dominates in volume due to extensive infrastructure expansion, while North America leads in adoption with over 60% of new data centers integrating smart monitoring-enabled busbar systems. By 2028, AI-based predictive load management integrated with busbar systems is expected to cut unscheduled downtime by 18% and improve energy efficiency by 12%. Firms are committing to ESG metrics such as 25% carbon footprint reduction by 2030 through recyclable aluminum conductors and optimized material utilization.

In 2024, Germany achieved a 17% improvement in substation efficiency through digital busbar monitoring initiatives integrated with smart grid programs. As electrification accelerates across mobility, manufacturing, and renewable energy, the Busbar Market is positioned as a pillar of resilience, compliance, and sustainable growth, supporting next-generation power distribution frameworks.

The Busbar Market is shaped by expanding electrification, grid modernization, renewable energy integration, and increasing demand for compact power distribution systems. Industrial automation, EV charging infrastructure, and data center expansion are intensifying the need for high-conductivity copper and aluminum busbars. Thermal management efficiency, space optimization, and installation speed are key procurement criteria for utilities and industrial operators. Global renewable energy capacity surpassed 3,700 GW, increasing the requirement for efficient internal power routing components. Additionally, the rise in medium-voltage installations in urban infrastructure projects is strengthening demand for insulated and sandwich-type busbars. Supply chain localization efforts and metal price volatility continue to influence procurement strategies and manufacturing economics within the Busbar Market.

Renewable energy installations now exceed 30% of global installed power capacity, necessitating efficient internal power collection and transmission components. Solar farms above 100 MW capacity require compact, low-loss distribution systems, where busbars reduce installation space by nearly 25% compared to traditional cabling. Wind turbine nacelles increasingly utilize laminated copper busbars to enhance vibration resistance and reduce heat buildup by up to 18%. Battery energy storage systems (BESS) installations grew by over 40% in recent years, requiring high-current busbars capable of handling 4,000–6,000 amperes. As governments expand clean energy corridors and smart substations, busbars are becoming integral to scalable, high-capacity renewable infrastructure.

Copper prices have fluctuated by more than 20% annually in recent trading cycles, directly impacting busbar manufacturing costs. Aluminum alternatives offer weight advantages but may require up to 1.6 times larger cross-sectional area to match copper conductivity, increasing material usage. Supply chain disruptions and export controls in major mining economies affect procurement timelines. Fabrication costs can increase by 10–15% during peak commodity cycles, limiting margins for small and mid-scale manufacturers. Furthermore, high purity requirements for electrical-grade copper restrict substitution flexibility, creating pricing pressure across procurement contracts and long-term supply agreements.

Global EV production surpassed 9 million units annually, accelerating demand for laminated busbars in battery packs, inverters, and charging systems. Fast-charging stations rated above 150 kW require high-current distribution components capable of sustaining elevated thermal loads. Laminated busbars reduce inductance by up to 30%, improving power electronics efficiency. Urban charging infrastructure projects across Asia and Europe are expanding at double-digit rates, creating sustained demand for compact, high-performance busbar assemblies. Additionally, lightweight aluminum busbars can reduce overall EV battery pack weight by nearly 8%, enhancing vehicle range and system efficiency.

Busbars operating above 4,000 amperes generate significant heat, requiring advanced insulation and cooling mechanisms. Inadequate thermal design can increase failure rates by 12–15% in high-load installations. Differing voltage standards across regions necessitate customized engineering, raising production complexity. Compliance with IEC and IEEE safety standards demands rigorous testing cycles that extend project timelines. Moreover, integration into compact urban substations requires space-optimized configurations, increasing design and installation challenges. Managing electromagnetic interference (EMI) in high-frequency inverter systems further complicates engineering specifications.

Rapid Expansion of Data Center Electrification: Hyperscale data centers now consume over 3% of global electricity, with power densities exceeding 15 kW per rack. Nearly 65% of new large-scale facilities are deploying high-capacity busbar trunking systems to reduce cable clutter and improve airflow efficiency by 10%–14%. Modular power distribution using overhead busbars reduces installation time by approximately 20% compared to traditional wiring systems.

Growth in Laminated Busbar Adoption for EVs: Laminated busbars are increasingly integrated into EV battery packs and inverters, reducing inductance by up to 30% and improving thermal dissipation by 18%. Over 70% of new-generation EV platforms are shifting toward compact laminated configurations, supporting higher voltage architectures exceeding 800V systems.

Smart Monitoring and IoT Integration: Around 45% of newly installed industrial busbar systems now incorporate IoT-enabled temperature and load sensors. Predictive monitoring reduces unexpected downtime by nearly 18% and extends component lifespan by 12%. Digital twin integration in substations enhances load balancing accuracy by 15%.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Busbar Market. Approximately 55% of new commercial and industrial projects report cost benefits through prefabricated busbar trunking systems. Pre-engineered sections reduce on-site labor requirements by 25% and accelerate commissioning timelines by nearly 30%, particularly in Europe and North America where construction efficiency targets are stringent.

The Busbar Market is segmented by type, application, and end-user, reflecting the diverse performance, voltage, and industry requirements across power distribution ecosystems. By type, the market primarily includes copper busbars, aluminum busbars, and laminated or insulated busbar systems. Copper remains widely preferred due to its 99% conductivity rating and superior thermal performance, while aluminum alternatives are increasingly adopted for lightweight and cost-optimized installations.

By application, utilities and power generation facilities represent the largest deployment segment due to high-current substation and transmission needs, followed by industrial manufacturing plants, commercial infrastructure, and electric vehicle (EV) systems. Increasing installation of renewable energy plants exceeding 100 MW capacity has significantly boosted medium- and high-voltage busbar usage.

From an end-user perspective, utilities, industrial facilities, commercial real estate, data centers, and EV manufacturers collectively account for the majority of installations. Growing electrification targets, grid upgrades exceeding 20% capacity expansion in several economies, and the shift toward compact distribution systems are shaping procurement strategies across these segments.

Copper busbars currently account for approximately 58% of total adoption due to superior conductivity, lower resistive losses, and high mechanical strength. Aluminum busbars hold nearly 27% share, primarily driven by weight reduction benefits and lower material costs in large infrastructure projects. Laminated and insulated busbars collectively represent around 15%, gaining traction in high-frequency and EV power electronics applications. While copper busbars dominate in volume, aluminum variants are witnessing faster penetration in infrastructure and renewable installations due to 40% lower weight compared to copper. However, laminated busbars are the fastest-growing type, expanding at an estimated CAGR of 8.9%, driven by EV battery integration, inverters, and compact data center power modules. Laminated systems reduce inductance by up to 30% and improve thermal management by nearly 18%, making them suitable for high-density applications. Other niche types such as flexible busbars and sandwich-type trunking systems contribute a combined 10% share, primarily used in commercial and modular construction settings requiring quick installation and scalability.

In 2025, the International Energy Agency highlighted that EV battery manufacturing capacity exceeded 3,000 GWh globally, significantly increasing the integration of laminated copper busbars in high-voltage battery modules.

Power transmission and distribution applications account for nearly 42% of total busbar installations, reflecting the ongoing grid expansion and modernization initiatives worldwide. Industrial manufacturing plants represent approximately 28%, while commercial infrastructure including data centers contributes around 18%. Electric vehicle systems and charging infrastructure account for roughly 12% but are expanding rapidly. While utilities lead in deployment volume, EV and charging infrastructure applications are the fastest-growing segment, advancing at approximately 9.5% CAGR due to increasing adoption of 800V architectures and fast-charging networks above 150 kW. Data center applications are also expanding as facilities exceeding 20 MW capacity require high-current, space-efficient busbar trunking systems. In 2025, more than 35% of global enterprises reported upgrading power distribution frameworks to smart busbar systems for predictive maintenance integration. Additionally, over 60% of new hyperscale data centers are implementing overhead busbar trunking to reduce airflow obstruction and improve energy efficiency.

In 2024, the U.S. Department of Energy reported that grid modernization projects across 30 states included advanced busbar-based switchgear upgrades to enhance transmission resilience and reduce outage duration by up to 15%.

Utilities remain the leading end-user segment, accounting for approximately 40% of total installations due to ongoing substation expansion and renewable grid integration. Industrial manufacturing represents about 30%, including heavy industries, automotive plants, and chemical processing facilities. Commercial infrastructure and data centers contribute roughly 20%, while EV manufacturers and charging network operators collectively hold near 10%. Although utilities dominate in overall deployment, EV manufacturers are the fastest-growing end-user segment, expanding at an estimated CAGR of 10.2% due to rapid electrification targets and increasing battery production volumes exceeding 9 million units annually. Industrial facilities are investing in smart busbar monitoring, with nearly 38% of large enterprises piloting IoT-based thermal management systems in 2025. Over 45% of new commercial buildings in developed markets are adopting prefabricated busbar trunking to shorten installation timelines by 20%–25%.

In 2025, the European Commission’s smart grid initiative reported integration of advanced busbar assemblies in over 120 urban substations, improving operational reliability and enabling real-time load balancing capabilities.

Asia Pacific accounted for the largest market share at 46% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

Asia Pacific benefits from installed power capacity exceeding 1,500 GW in China alone and industrial output growth above 5% annually in India and Southeast Asia. Europe holds approximately 24% share, supported by renewable installations surpassing 700 GW across member states. North America represents nearly 20%, driven by over 35 GW of annual solar and wind additions and more than 2,000 active data centers. South America and the Middle East & Africa collectively account for around 10%, with grid electrification rates exceeding 95% in Brazil and infrastructure investments surpassing USD 50 billion annually in GCC nations.

This region accounts for nearly 20% of global busbar installations, driven by data centers exceeding 2,000 operational facilities and large-scale renewable integration. The U.S. leads deployment, supported by federal grid resilience funding programs exceeding USD 10 billion. Utilities are upgrading substations with smart monitoring-enabled busbars to reduce outage frequency by 15%. Industrial demand from automotive EV plants producing over 1 million electric vehicles annually strengthens laminated busbar adoption. Eaton, a key regional player, has expanded its power distribution portfolio with modular busway systems to address hyperscale infrastructure needs. Enterprise adoption is particularly high in healthcare and financial sectors, where nearly 50% of new facilities deploy prefabricated busbar trunking systems.

Europe accounts for roughly 24% of market share, with Germany, France, and the UK leading installations. Renewable penetration exceeds 40% in several countries, increasing demand for efficient transmission components. Regulatory initiatives targeting 20% energy efficiency improvements by 2030 are accelerating adoption of insulated busbar systems. Advanced manufacturing clusters in Germany emphasize automation, improving fabrication precision by 18%. Schneider Electric has enhanced compact busway offerings tailored for green buildings and smart grids. Regional buyers prioritize recyclable aluminum conductors, with over 35% of commercial developments integrating sustainable electrical systems due to regulatory pressure.

Asia Pacific leads global consumption with 46% share, driven by China, India, and Japan. China’s installed capacity exceeds 2,900 GW, while India’s renewable additions surpassed 15 GW annually. Manufacturing hubs in Jiangsu and Guangdong have improved busbar production efficiency by 20% through automation. Mitsubishi Electric continues expanding compact busway solutions for industrial and rail infrastructure. Urban infrastructure projects across Southeast Asia have increased medium-voltage busbar adoption by nearly 12% annually. Consumer demand is heavily influenced by industrial growth and expanding EV production exceeding 9 million units regionally.

South America accounts for approximately 6% of global installations, with Brazil and Argentina as primary contributors. Brazil’s electrification rate exceeds 95%, and renewable energy contributes over 45% of power generation. Infrastructure modernization programs emphasize transmission upgrades and compact substation systems. Local manufacturers are collaborating with utilities to enhance aluminum busbar production for cost-sensitive installations. Industrial mining and oil processing facilities drive high-current system demand. Adoption patterns show rising interest in modular busbar systems for industrial parks to reduce installation timelines by 18%.

The region contributes nearly 4% of global share, led by the UAE and South Africa. GCC infrastructure investments exceed USD 50 billion annually, focusing on smart cities and renewable power integration. Oil & gas facilities demand high-capacity copper busbars capable of handling above 5,000 amperes. Regional modernization programs emphasize digital substations and IoT-enabled monitoring systems. Local demand trends indicate growing adoption of prefabricated trunking systems in commercial developments, with installation time reductions nearing 20%. Trade partnerships with Asian manufacturers support supply chain continuity.

China – 32% Market Share: Dominates due to high production capacity exceeding 11 million metric tons of refined copper annually and extensive grid expansion projects.

United States – 18% Market Share: Strong position supported by over 2,000 operational data centers and large-scale renewable energy and EV infrastructure deployment.

The Busbar Market exhibits a moderately fragmented structure with over 60 active global and regional competitors. The top five companies collectively account for approximately 48% of total market presence, reflecting strong brand positioning and diversified product portfolios. Competition is driven by product innovation, customization capability, and integration of smart monitoring technologies.

Leading players focus on expanding laminated and insulated busbar systems to address EV and renewable power requirements. Strategic initiatives include mergers, joint ventures, and capacity expansions across Asia and North America. Over 25% of new product launches between 2023 and 2025 emphasized compact, modular trunking systems. Companies are investing in automation technologies that enhance fabrication precision by up to 20%, improving operational efficiency and delivery timelines. Competitive differentiation increasingly centers on ESG compliance, recyclable materials, and digital integration features.

Eaton

Mitsubishi Electric

Legrand

General Electric

Larsen & Toubro

C&S Electric

Rittal

Godrej Electricals

Powell Industries

Method Electronics

Oriental Copper

Technological advancements in the Busbar Market are centered on efficiency optimization, digital monitoring, lightweight materials, and compact system architecture. Laminated busbars are increasingly utilized in EV battery systems operating above 800V, reducing inductance by 30% and improving heat dissipation by nearly 18%. Aluminum alloy conductors now achieve conductivity levels above 60% IACS, offering weight reductions of up to 40% compared to copper.

IoT-enabled thermal sensors embedded within busbar trunking systems provide real-time temperature and load monitoring, reducing unexpected downtime by 15%–20%. Digital twin integration allows predictive maintenance planning and load balancing optimization, improving operational efficiency by nearly 12%. Advanced insulation materials such as epoxy-coated and heat-shrink systems enhance dielectric strength beyond 1 kV/mm.

Automated CNC bending and laser cutting technologies have improved dimensional accuracy by approximately 20%, supporting modular construction and faster installation cycles. Integration with smart grid frameworks and AI-based power analytics is reshaping large-scale industrial and utility deployments, positioning busbars as intelligent components within future-ready energy ecosystems.

• In 2025, Siemens expanded its SIVACON 8PS busbar trunking portfolio with the new LI system capable of handling 800 A to 6300 A for industrial and infrastructure power distribution, offering enhanced flexibility and space-efficient design. Source: www.siemens.com

• In 2024–2025, Schneider Electric unveiled its EcoStruxure™ Foresight Operation platform, an AI-powered energy and power systems platform that enhances visibility and predictive insight across power distribution infrastructure, supporting improved operational efficiency for built environments (relevant to integrated busbar system performance). Source: www.prnewswire.com

• Siemens continues to promote its SIVACON 8PS busbar trunking systems on its official site, highlighting cost efficiency, flexible planning, and faster installation versus traditional cable systems. Source: www.siemens.com

• Schneider Electric’s official newsroom lists multiple 2025 press activities including energy and sustainability technology announcements (indirectly linked to the busbar distribution ecosystem), demonstrating the company’s continued innovation focus that supports integrated busbar solutions. Source: www.se.com

The Busbar Market Report provides comprehensive coverage across product types including copper, aluminum, laminated, insulated, and flexible busbars. It evaluates deployment across power transmission, industrial manufacturing, commercial infrastructure, renewable energy plants, EV systems, and data centers. The report assesses voltage classifications ranging from low-voltage systems below 1 kV to high-capacity installations exceeding 5,000 amperes.

Geographically, the study spans North America, Europe, Asia Pacific, South America, and Middle East & Africa, analyzing consumption patterns across more than 25 major economies. It incorporates insights into smart grid modernization, renewable capacity integration surpassing 3,700 GW globally, and EV production exceeding 9 million units annually.

The scope further examines technological advancements such as IoT-enabled monitoring, AI-driven predictive maintenance, recyclable aluminum conductors, and modular trunking systems reducing installation time by up to 30%. Industry focus areas include regulatory compliance, ESG targets involving 20% efficiency improvements, and supply chain localization strategies. The report is designed to support decision-makers with actionable intelligence on procurement trends, competitive positioning, and infrastructure investment priorities shaping the Busbar Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,620.0 Million |

| Market Revenue (2033) | USD 2,558.7 Million |

| CAGR (2026–2033) | 5.88% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Siemens; Schneider Electric; ABB; Eaton; Mitsubishi Electric; Legrand; General Electric; Larsen & Toubro; C&S Electric; Rittal; Godrej Electricals; Powell Industries; Method Electronics; Oriental Copper |

| Customization & Pricing | Available on Request (10% Customization Free) |