Reports

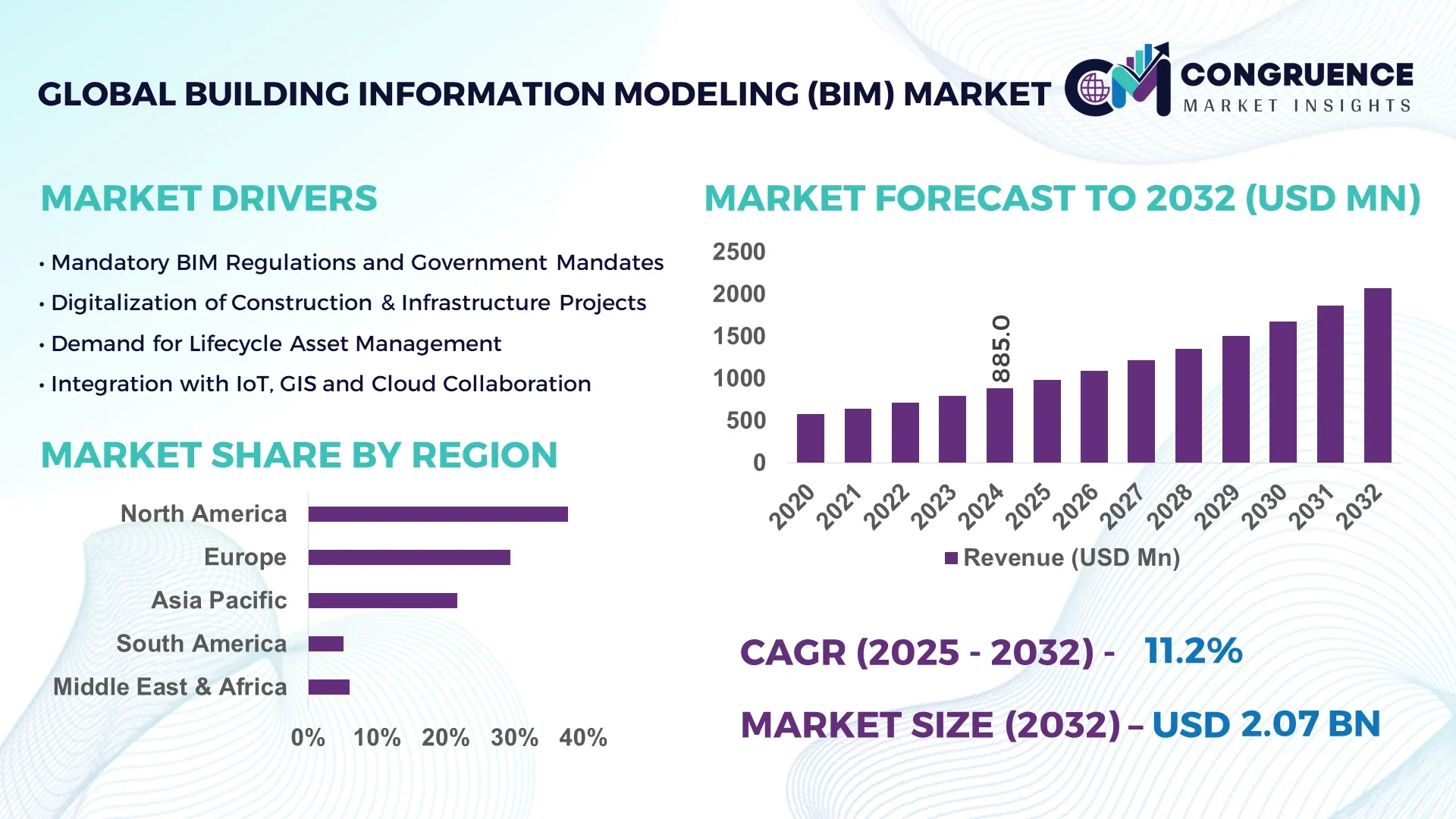

The Global Building Information Modeling (BIM) Market was valued at USD 885.0 Million in 2024 and is anticipated to reach a value of USD 2,069.1 Million by 2032 expanding at a CAGR of 11.2% between 2025 and 2032.

The United States holds a leading position in the Building Information Modeling (BIM) Market due to its extensive investment in digital infrastructure, large-scale commercial construction projects, and widespread integration of BIM software in public infrastructure initiatives. U.S.-based firms actively deploy advanced 5D and 6D BIM systems across industrial, institutional, and residential construction sectors, supported by ongoing federal investment in smart cities and transportation upgrades.

The Building Information Modeling (BIM) Market continues to experience significant growth driven by its adoption across multiple sectors including commercial construction, infrastructure development, and industrial facilities. Governments globally are mandating the use of BIM in public construction, particularly in Europe and Asia-Pacific. Technological innovations, such as cloud-based collaboration platforms and real-time design simulation, have improved stakeholder coordination and reduced project overruns. Advanced visualization tools and integration with IoT and AR/VR are enhancing data-driven decision-making. Regulatory frameworks focused on green building standards and energy efficiency are further driving BIM integration into sustainable design processes. Economically, the shift toward digital construction workflows is helping firms reduce project lifecycle costs. Regional growth is most notable in Asia-Pacific due to urbanization and smart city investments, while Europe remains focused on interoperability and open BIM standards. Emerging trends, such as BIM-as-a-Service (BIMaaS) and digital twins, are poised to redefine long-term asset management and operational modeling. The market outlook remains optimistic, fueled by continuous R&D, expanding application scope, and strong policy backing.

Artificial Intelligence (AI) is playing a transformative role in the Building Information Modeling (BIM) Market by enhancing design automation, predictive analytics, and real-time decision-making processes across the project lifecycle. AI algorithms enable BIM systems to detect design clashes, optimize resource allocation, and generate alternative construction scenarios with greater efficiency. Through machine learning, historical project data is now being leveraged to forecast construction timelines, reduce rework rates, and improve cost estimation accuracy. AI-enabled BIM platforms can also simulate energy consumption, environmental impacts, and safety scenarios before ground is broken, providing greater value during pre-construction planning.

Furthermore, integration of AI-driven generative design allows architects and engineers to automatically produce thousands of design iterations based on functional goals and site constraints. This is particularly advantageous in urban development and infrastructure planning where space, cost, and sustainability requirements are critical. Computer vision, combined with AI, helps in progress monitoring by analyzing on-site images and updating BIM models in near real-time, reducing human error and enhancing transparency. As digital twins become more prevalent, AI is increasingly being used for facilities management, predictive maintenance, and lifecycle analysis, ensuring buildings operate at peak efficiency. Overall, AI is helping firms streamline workflows, enhance collaboration, and deliver smarter construction solutions in the Building Information Modeling (BIM) Market.

“In early 2025, a U.S.-based construction technology firm deployed an AI-powered BIM platform capable of reducing clash detection time by over 70% across a 1.2 million square foot hospital project. The platform processed over 25,000 model components and automatically resolved 12,000 design conflicts within 48 hours, significantly cutting down coordination meetings and rework delays.”

The Building Information Modeling (BIM) Market is undergoing a paradigm shift driven by digitization, regulatory enforcement, and an urgent need for cost-effective construction practices. Rapid urbanization and smart infrastructure demands are pushing firms to adopt BIM as a critical planning and operations tool. The convergence of BIM with other technologies like GIS, digital twins, and cloud platforms is enhancing end-to-end visibility across construction and facility management stages. Increasing government mandates for BIM usage in public tenders, especially in the UK, Germany, and South Korea, are accelerating adoption. Meanwhile, rising emphasis on sustainable buildings and energy-efficiency compliance continues to position BIM as an essential enabler of green construction strategies.

Government directives around the world are a major driver behind the growth of the Building Information Modeling (BIM) Market. Countries such as the United Kingdom, Singapore, and the UAE have mandated the use of BIM for public infrastructure projects, compelling contractors and developers to implement digital workflows. In India, the National BIM Strategy is promoting standardized implementation across transportation, water, and smart city projects. In Japan, the Ministry of Land, Infrastructure, Transport and Tourism has adopted BIM in public works to improve cost transparency and operational efficiency. These initiatives are supported by increased funding for digital infrastructure, making BIM adoption not only a compliance requirement but a competitive advantage.

Despite the accelerating adoption of BIM, a significant restraint is the shortage of skilled professionals proficient in BIM technologies. Many small to medium-sized enterprises (SMEs) struggle to find architects, engineers, and technicians trained in advanced BIM platforms like Revit, ArchiCAD, or Tekla Structures. The learning curve associated with these tools, combined with limited formal education programs, results in inconsistent model quality and delays in project execution. This shortage is particularly acute in developing regions, where educational institutions have yet to incorporate BIM training into civil and architectural engineering curriculums. The absence of standardized certification programs further limits workforce scalability in the Building Information Modeling (BIM) Market.

The integration of BIM with digital twins and Internet of Things (IoT) technologies presents a substantial opportunity in the Building Information Modeling (BIM) Market. Digital twins offer real-time monitoring and simulation of buildings using data collected via IoT sensors. This facilitates predictive maintenance, energy management, and space optimization, all while enhancing long-term asset value. For instance, airports and healthcare facilities are increasingly adopting BIM-IoT integration to manage complex infrastructure efficiently. By embedding IoT-enabled devices into BIM models, facility managers can monitor equipment performance, track usage trends, and pre-empt system failures, thereby reducing operational downtime and extending asset lifecycles.

One of the key challenges in the Building Information Modeling (BIM) Market is the lack of seamless interoperability between different BIM software platforms. While open standards such as Industry Foundation Classes (IFC) exist, many proprietary software solutions use unique file formats, which can hinder collaboration and data exchange across project teams. This limitation often forces firms to rely on manual conversions, which introduces errors and delays. Multi-vendor project environments further exacerbate this issue, particularly in large-scale infrastructure developments where numerous subcontractors operate with varied digital tools. As a result, inconsistent data workflows and duplicated efforts continue to impede full BIM implementation and efficiency.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Building Information Modeling (BIM) Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical. BIM integration enables manufacturers to simulate and optimize prefabrication workflows, ensuring tighter quality control and improved logistics management during installation.

Cloud-Based BIM Collaboration Platforms: The increasing deployment of cloud-native BIM tools is facilitating real-time collaboration among architects, engineers, and construction managers. These platforms support remote access to design models, enhance data sharing, and reduce file transfer bottlenecks. Cloud-based solutions have gained traction especially in multi-location projects across Asia-Pacific and Latin America. Improved version control, secure data encryption, and mobile compatibility are key features driving adoption among mid-sized firms and public sector clients.

Sustainability-Driven BIM Features: Environmental regulations and corporate ESG goals are fueling demand for BIM features that support lifecycle carbon analysis and green building certifications. Tools integrated into BIM platforms now allow simulation of embodied energy, thermal performance, and daylight optimization. These features are increasingly being adopted in new commercial and institutional builds, particularly in Western Europe and Canada, to meet net-zero emission targets. Regulatory agencies are also beginning to recognize BIM outputs in permitting and sustainability audits.

AI and Automation in Construction Documentation: AI tools embedded within BIM software are streamlining the generation of construction documentation by automatically tagging components, generating sections, and checking for code compliance. This significantly reduces the time spent on manual documentation tasks while improving accuracy. In 2025, AI-powered BIM documentation systems are being used in over 40% of new infrastructure projects in technologically advanced markets such as South Korea, Germany, and the United States, enabling faster project approvals and cost savings during the design phase.

The Building Information Modeling (BIM) Market is segmented based on type, application, and end-user, each revealing critical insights into evolving industry demands and technological integration. Types range from software and services to cloud-based platforms, each catering to different phases of the building lifecycle. Applications span across planning, design, construction, and operations, reflecting the multifaceted use of BIM across the project timeline. End-user segmentation highlights adoption trends across architects, engineers, contractors, and facility managers. These divisions are essential to understanding where innovation and demand are intensifying. Notably, technological maturity, user needs, and regional adoption policies significantly influence these segments. As the construction industry pivots toward digital transformation, stakeholders across all segments are experiencing a paradigm shift toward automation, visualization, and integrated workflows that enhance productivity, reduce costs, and improve decision-making accuracy throughout a building's life cycle.

The Building Information Modeling (BIM) Market includes several key types: Software, Services, and Cloud-Based Solutions. Software remains the leading segment, driven by widespread adoption of design and modeling tools such as 3D visualization, clash detection, and digital twin platforms that streamline project planning and coordination. The increased demand for robust modeling tools among architects and designers significantly contributes to this dominance.

Cloud-Based Solutions represent the fastest-growing segment, propelled by the global shift to remote collaboration and real-time project accessibility. Cloud platforms facilitate seamless data sharing, improve interoperability, and reduce infrastructure costs—key benefits that are accelerating their uptake, especially among small and medium-sized enterprises and geographically dispersed teams.

Services, including consulting, implementation, and support, play a vital role in enabling BIM adoption, particularly among new users. Although smaller in market share, this segment remains critical for onboarding, training, and customization support, which in turn fosters broader market penetration and user satisfaction.

Applications of BIM are wide-ranging and include Planning & Modelling, Asset Management, Construction, and Sustainability Management. Among these, Planning & Modelling is the leading application area due to the integral role it plays in early-stage project development, where visual clarity and data accuracy are crucial. The ability to preempt design flaws and improve stakeholder coordination makes it indispensable for modern construction projects.

Sustainability Management is emerging as the fastest-growing application segment. As green building regulations tighten globally, BIM tools that support energy analysis, carbon footprint monitoring, and lifecycle assessments are gaining traction. These tools enable developers to design sustainable structures while ensuring regulatory compliance.

Other applications such as Asset Management and Construction benefit from increased demand for integrated building lifecycle management. These areas rely on BIM to track asset performance, schedule maintenance, and optimize operational workflows—factors increasingly important in commercial and infrastructure developments worldwide.

The end-user landscape of the Building Information Modeling (BIM) Market includes Architects, Engineers, Contractors, and Facility Managers. Architects currently lead the market, as they are primary users of BIM software during the concept and design phases. Their preference for high-detail visualization and spatial planning tools has driven early and widespread adoption across the architectural community.

Contractors are the fastest-growing end-user group, owing to BIM's effectiveness in real-time construction monitoring, resource allocation, and clash detection. These capabilities help reduce rework, manage timelines efficiently, and mitigate cost overruns—benefits that have become indispensable in large-scale construction projects.

Engineers and Facility Managers, while comparatively smaller in share, contribute significantly to operational continuity and post-construction utility. Engineers rely on BIM for structural, mechanical, and electrical planning, whereas Facility Managers utilize BIM models for building operation, maintenance scheduling, and renovation planning—extending BIM’s utility beyond project completion.

North America accounted for the largest market share at 37.8% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.5% between 2025 and 2032.

North America’s dominance is supported by early digital adoption, mandatory BIM usage in public infrastructure projects, and strong investment in construction tech. Conversely, Asia-Pacific’s surge is driven by massive urban infrastructure developments, growing construction budgets, and government-mandated digital transformation initiatives in countries like China and India. Europe also plays a significant role, influenced by sustainability directives and standardized BIM protocols across the EU. Meanwhile, South America and the Middle East & Africa regions are witnessing emerging adoption trends supported by infrastructural reforms and increasing demand for cost-efficient construction methods. These regional dynamics are shaping global BIM adoption, emphasizing the need for localized strategies and solutions tailored to specific market conditions and regulations.

North America held the largest share of the global Building Information Modeling (BIM) Market in 2024, accounting for approximately 37.8% of the total market. The region’s dominance stems from a strong construction sector and well-established engineering and architectural industries. The U.S. is the primary contributor, supported by federal initiatives promoting BIM adoption for public infrastructure. Key sectors driving demand include commercial real estate, transportation, and industrial construction. Regulatory frameworks such as the U.S. General Services Administration’s BIM requirements have accelerated industry-wide compliance. Additionally, North America leads in cloud BIM tools, AI integration, and automation of construction processes—setting the global benchmark for BIM-driven project execution and lifecycle management.

Europe captured around 29.4% of the global BIM market in 2024, with key contributors being Germany, the United Kingdom, and France. The regional market is propelled by stringent sustainability initiatives and regulations—such as the EU Green Deal and national mandates for BIM in public projects. Countries like the UK have long required BIM compliance for government-funded construction, influencing broader adoption in the private sector. The market benefits from mature construction ecosystems and advanced digital infrastructure. Europe is also witnessing rising demand for 5D and 6D BIM models, especially in energy-efficient building design and maintenance planning. Technological innovation and environmental compliance continue to reinforce Europe’s leadership in digital construction practices.

Asia-Pacific ranks as the fastest-growing regional market in 2024, holding 21.7% of global volume and showing rapid expansion potential. China, India, and Japan are the primary consumers, driven by increasing smart city initiatives, urban renewal programs, and large-scale infrastructure developments. Public sector mandates requiring BIM in projects—such as India’s Smart Cities Mission and China's digital construction policies—are pushing adoption. Rapid digitization across the construction supply chain, growing emphasis on green buildings, and robust investment in infrastructure are also fueling market momentum. The region is emerging as a hotbed for BIM innovation, with local startups and tech hubs driving cloud integration, AR/VR applications, and digital twin adoption in construction.

South America is witnessing increasing BIM adoption, with Brazil and Argentina emerging as the leading markets. The region accounted for around 5.1% of the global BIM market share in 2024. Growth is driven by government-led infrastructure reform, particularly in transportation, housing, and energy projects. Brazil’s emphasis on digital construction practices for public procurement and Argentina’s urban development initiatives are key enablers. Additionally, the private sector is beginning to recognize the cost benefits of BIM in reducing delays and rework. Although technology penetration remains relatively low, foreign investment, regional collaboration, and increasing awareness are catalyzing the digital transformation of South America’s construction sector.

The Middle East & Africa region held an estimated 6.0% of the global BIM market share in 2024, with the UAE, Saudi Arabia, and South Africa leading demand. The region is undergoing rapid construction transformation, particularly in smart cities, oil & gas infrastructure, and hospitality sectors. UAE Vision 2030 and Saudi Arabia’s NEOM project are notable examples where BIM integration is crucial. Regional growth is supported by modernization efforts, including automation in design and project management workflows. Local governments are increasingly promoting BIM usage through national construction guidelines. As infrastructure investment continues to rise, BIM is being recognized as a critical tool to ensure project efficiency, cost control, and regulatory compliance.

United States – 33.2% Market Share

High BIM adoption in public infrastructure and advanced digital construction ecosystem support its market leadership.

China – 15.8% Market Share

Rapid urbanization and strong government push for digital transformation in construction projects drive demand for BIM solutions.

The Building Information Modeling (BIM) Market is characterized by a moderately consolidated competitive environment with over 70 active global and regional players. Industry leaders are continuously strengthening their market positions through strategic mergers, acquisitions, and long-term partnerships. Key players are heavily investing in R&D to enhance BIM functionalities with AI, machine learning, and cloud capabilities. The competition is also fueled by a growing emphasis on interoperability, data security, and platform integration across design and construction phases. Several firms are expanding their offerings beyond 3D modeling to include 4D (scheduling), 5D (cost), and even 7D (facility management) BIM solutions. Open BIM standards and increased adoption of SaaS-based solutions are redefining customer expectations and competitive dynamics. Additionally, firms are engaging in collaborations with governments and construction firms to gain access to high-value infrastructure projects. Innovation in digital twin integration, generative design, and mobile BIM applications continues to influence market competition, raising the entry threshold for new players while pushing incumbents toward continuous evolution.

Autodesk Inc.

Bentley Systems, Incorporated

Trimble Inc.

Dassault Systèmes

Nemetschek Group

Hexagon AB

AVEVA Group plc

RIB Software SE

Asite Solutions Ltd

Graphisoft SE

Technological innovation is a driving force behind the evolution of the Building Information Modeling (BIM) Market. Modern BIM platforms are now increasingly powered by cloud infrastructure, allowing for real-time collaboration across globally distributed teams. These cloud-based solutions support continuous data synchronization and enable users to work on shared models simultaneously, enhancing efficiency and reducing errors.

Artificial Intelligence (AI) and Machine Learning (ML) are being integrated into BIM platforms to automate clash detection, optimize design alternatives, and predict maintenance needs. Augmented Reality (AR) and Virtual Reality (VR) are enhancing design visualization, allowing stakeholders to immerse themselves in building designs before construction begins.

The adoption of 4D, 5D, and 6D BIM technologies is gaining traction. 4D BIM supports timeline simulation, 5D adds cost estimation capabilities, and 6D is focused on sustainability and energy efficiency management. Additionally, digital twin technology is increasingly being paired with BIM to offer real-time operational monitoring of built assets post-construction.

Mobile BIM apps are also enabling on-site collaboration and data access, reducing response times for issue resolution. Furthermore, open BIM standards are improving interoperability between different tools and systems, making it easier for stakeholders to collaborate across project phases and disciplines.

In February 2024, Trimble launched its new Trimble Connect AR module, enabling contractors and designers to overlay 3D BIM models onto the real-world environment using smartphones and tablets, boosting site accuracy and design verification.

In May 2024, Autodesk announced the integration of AI-assisted features in Autodesk Construction Cloud to streamline data tagging, clash detection, and RFIs, improving BIM coordination across project teams.

In August 2023, Bentley Systems introduced Infrastructure IoT within its iTwin platform, combining BIM with sensor data analytics to support predictive maintenance for critical infrastructure assets.

In November 2023, Nemetschek Group expanded its open BIM ecosystem by acquiring a mobile BIM collaboration platform, enhancing on-site data accessibility and project transparency for construction professionals.

The Building Information Modeling (BIM) Market Report offers a comprehensive assessment of the global BIM landscape, encompassing key segments such as types (software, services, and solutions), applications (commercial, residential, industrial, and infrastructure), and end-users (architects, engineers, contractors, and facility managers). The report spans across five major geographic regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—highlighting regional adoption patterns, regulatory dynamics, and technological maturity.

This report evaluates the adoption and evolution of advanced BIM functionalities, including 3D, 4D, 5D, and 6D modeling, as well as the integration of technologies like cloud computing, AI/ML, AR/VR, and digital twins. It examines market growth drivers such as smart city initiatives, government BIM mandates, and demand for sustainable construction practices.

Additionally, the report covers emerging trends such as mobile BIM usage on construction sites, open BIM protocols for interoperability, and the integration of BIM in facility and asset lifecycle management. Niche segments such as BIM for modular construction, prefabricated buildings, and small-scale residential projects are also explored. This wide-ranging scope makes the report a vital resource for stakeholders aiming to understand both the current and future directions of the BIM market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 885.0 Million |

| Market Revenue (2032) | USD 2,069.1 Million |

| CAGR (2025–2032) | 11.2 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Autodesk Inc., Bentley Systems, Incorporated, Trimble Inc., Dassault Systèmes, Nemetschek Group, Hexagon AB, AVEVA Group plc, RIB Software SE, Asite Solutions Ltd, Graphisoft SE, Archidata Inc. |

| Customization & Pricing | Available on Request (10 % Customization is Free) |