Reports

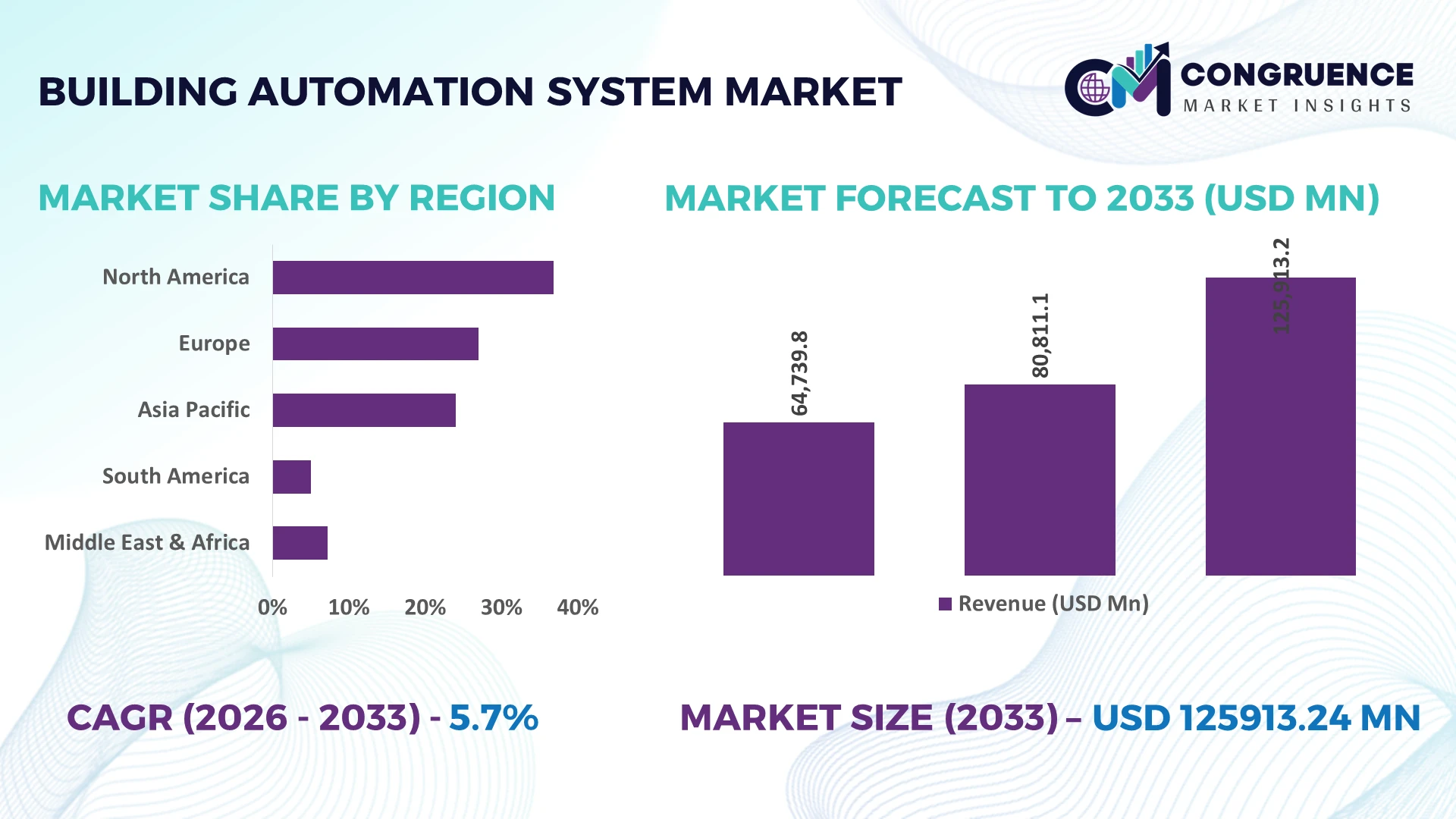

The Global Building Automation System Market was valued at USD 80811.1 Million in 2025 and is anticipated to reach a value of USD 125913.24 Million by 2033 expanding at a CAGR of 5.7% between 2026 and 2033. The global Building Automation System Market is expanding through AI-enabled energy management, stricter building efficiency regulations, and large-scale investments in intelligent commercial infrastructure modernization.

The United States leads the global Building Automation System Market with nearly 31% market share, supported by more than USD 90 billion in annual commercial construction investment and widespread deployment of intelligent HVAC, lighting, and security systems across healthcare, offices, and data centers. Compared with Germany's manufacturing-driven automation adoption, the U.S. maintains broader smart building integration, while post-European energy security initiatives continue accelerating digital building upgrades across developed economies.

Organizations investing in interoperable, cybersecurity-focused automation platforms are strengthening operational efficiency while positioning assets for long-term regulatory compliance and digital transformation.

Market Size & Growth: USD 80,811.1 million in 2025, projected to reach USD 125,913.24 million by 2033 at a CAGR of 5.7%, driven by AI-powered energy optimization and smart infrastructure modernization.

Top Growth Drivers: Smart building adoption (+32%), energy efficiency investments (+27%), and IoT-enabled facility modernization (+24%) continue accelerating market expansion.

Short-Term Forecast: By 2028, predictive automation solutions reduce building energy consumption by 18% while improving maintenance efficiency by 22%.

Emerging Technologies: AI analytics, digital twins, edge computing, and IoT-enabled controllers enhance operational visibility, automation accuracy, and predictive maintenance.

Regional Leaders: North America exceeds USD 38 billion, Europe surpasses USD 31 billion, and Asia-Pacific reaches USD 34 billion through accelerated smart infrastructure deployment.

Consumer/End-User Trends: More than 61% of enterprise facilities prioritize integrated platforms combining HVAC, lighting, occupancy monitoring, and security management.

Pilot/Case Example: In 2025, a commercial smart campus project lowered energy consumption by 21% while reducing maintenance response time by 29%.

Competitive Landscape: The leading vendor controls approximately 13% market share, while Siemens, Schneider Electric, Honeywell, Johnson Controls, and ABB maintain strong global positions.

Regulatory & ESG Impact: Advanced building efficiency regulations improve operational performance by over 20%, supporting decarbonization targets and compliance initiatives worldwide.

Investment & Funding: More than USD 14 billion supports smart building projects through strategic partnerships, digital infrastructure expansion, and supply-chain regionalization.

Innovation & Future Outlook: Autonomous building intelligence, AI-driven optimization, and cybersecurity-first automation platforms are reshaping next-generation facility management strategies.

The Building Automation System Market is witnessing strong demand across commercial buildings, healthcare facilities, industrial sites, educational campuses, and data centers where integrated automation enhances operational performance and sustainability. AI-powered analytics, cloud-based management platforms, and digital twin technologies are improving facility efficiency by over 20%, while evolving energy regulations and regional supply-chain diversification continue accelerating deployment, setting the stage for deeper strategic market analysis.

The Building Automation System Market has become a strategic priority as organizations seek measurable reductions in operating costs while complying with increasingly stringent building efficiency regulations and digital infrastructure standards. Large-scale commercial retrofits, AI-enabled facility management, and supply-chain localization for electronic components are reshaping competitive positioning. Intelligent automation platforms now influence investment decisions across healthcare, manufacturing, commercial offices, data centers, and public infrastructure where operational continuity has become a board-level priority.

Modern AI-enabled building automation platforms reduce energy consumption by nearly 20% and lower unplanned maintenance costs by approximately 25% compared with conventional standalone control systems through predictive analytics and real-time monitoring. The United States continues leading enterprise-scale deployments across commercial assets, while Japan emphasizes high-density intelligent buildings with advanced occupancy optimization and energy resilience. During the next two to three years, integrated cloud-based building management platforms are expected to exceed 65% adoption among newly developed premium commercial facilities.

A modern hospital campus integrating HVAC, lighting, security, and occupancy analytics has demonstrated double-digit efficiency improvements while strengthening regulatory compliance and asset utilization. Vendors are expanding software ecosystems, strengthening cybersecurity partnerships, and increasing investment in interoperable platforms to accelerate deployment. Companies establishing scalable, data-driven automation portfolios will secure stronger operational resilience, long-term customer retention, and sustainable competitive differentiation.

Mandatory building efficiency standards, AI-driven facility management, and rising electricity costs are accelerating Building Automation System deployment across commercial and industrial infrastructure. More than 60% of newly constructed premium commercial buildings now integrate centralized automation platforms, while predictive maintenance reduces equipment downtime by nearly 30% and energy optimization lowers operating costs by approximately 20%. The United States continues investing in digital public infrastructure, while India's smart city initiatives are increasing demand for integrated building intelligence. In response, leading companies are expanding cloud-native platforms, acquiring software capabilities, and forming ecosystem partnerships to deliver interoperable automation solutions. Organizations combining energy optimization with real-time analytics are achieving stronger asset performance and long-term operational efficiency.

Integration challenges remain significant as nearly 45% of commercial buildings continue operating with legacy HVAC and control infrastructure that lacks compatibility with modern automation platforms. System integration expenses can increase project implementation costs by 15–20%, while fragmented communication protocols delay deployment across multi-site facilities. Germany and several mature European markets continue facing modernization constraints within aging building portfolios despite strong sustainability targets. Companies are reducing implementation risks through open-protocol architectures, localized engineering support, and phased modernization contracts that preserve existing infrastructure. Organizations unable to simplify interoperability face longer deployment cycles, reduced project scalability, and increased operational complexity during digital transformation.

Artificial intelligence, digital twins, and edge computing are transforming Building Automation Systems into intelligent operational platforms that extend beyond conventional energy management. AI-enabled optimization improves space utilization by nearly 18%, while digital twin simulations reduce commissioning time by approximately 25%. Saudi Arabia and Singapore are expanding smart infrastructure programs that prioritize integrated digital buildings with advanced sustainability performance. Companies are increasing R&D investment, strengthening software partnerships, and developing subscription-based building management platforms that generate recurring service revenue. The emerging opportunity lies in combining operational intelligence, carbon management, and predictive analytics into unified digital ecosystems that deliver measurable long-term business value.

Expanding connectivity across intelligent buildings increases cybersecurity exposure as more than 70% of automation platforms now connect with enterprise cloud environments and operational technology networks. At the same time, shortages of skilled automation engineers extend deployment timelines by nearly 20% across complex commercial projects. The United States continues strengthening critical infrastructure cybersecurity requirements, increasing compliance expectations for intelligent building operators. Companies must invest in secure software architectures, workforce training, and continuous monitoring while collaborating with cybersecurity specialists and technology partners. Successfully balancing digital connectivity with operational resilience will determine long-term competitiveness and deployment consistency across increasingly complex building automation environments.

AI-Driven Facility Intelligence: Building operators are accelerating AI-enabled predictive maintenance and occupancy analytics, with intelligent monitoring reducing equipment downtime by nearly 30% and maintenance costs by 18%. More than 48% of newly commissioned premium commercial facilities now integrate AI-assisted automation platforms. Rising skilled labor shortages and increasing operational expenditure are encouraging vendors to expand cloud analytics, strengthen software partnerships, and automate asset performance management across enterprise portfolios.

Open Protocol Integration: Enterprises are replacing proprietary building controls with interoperable automation architectures supporting BACnet, KNX, and Modbus standards. Open-platform deployments have increased by approximately 35%, while system commissioning time has declined by 22% through standardized integration. Large commercial property owners are prioritizing phased modernization instead of full infrastructure replacement, prompting technology providers to develop modular solutions that protect legacy investments while improving long-term operational flexibility.

Cybersecure Smart Buildings: Connected building infrastructure is driving cybersecurity investments as more than 70% of enterprise automation systems now exchange operational data through cloud-enabled platforms. Advanced zero-trust security frameworks reduce operational vulnerabilities by nearly 25%, particularly across healthcare and government facilities. Companies are embedding secure device authentication, encrypted communication, and continuous monitoring into automation platforms while expanding strategic cybersecurity alliances to strengthen digital resilience.

Energy Optimization Expansion: Intelligent energy management is becoming a standard deployment priority as automated optimization reduces electricity consumption by over 20% and peak demand by approximately 15%. Building owners are responding to stricter energy performance regulations through real-time monitoring, automated load balancing, and digital carbon reporting. Automation vendors are expanding integrated energy management portfolios and strengthening ecosystem partnerships to support enterprise sustainability targets while improving long-term operating efficiency.

HVAC Control remains the dominant segment as it delivers the highest operational value through centralized climate management, predictive maintenance, and energy optimization across commercial and industrial facilities. Nearly 56% of integrated Building Automation System deployments prioritize HVAC Control because heating and cooling account for the largest share of building energy consumption. AI-enabled HVAC platforms reduce electricity usage by around 20% while lowering maintenance interventions by nearly 25%, making them the preferred investment for enterprise facility owners. Energy Management is emerging as the fastest-growing segment as organizations strengthen carbon reduction strategies and implement real-time energy analytics. Vendors are expanding AI-driven optimization software, edge controllers, and cloud-based monitoring platforms to improve lifecycle performance and regulatory compliance.

Lighting Control continues gaining traction through occupancy sensing and daylight harvesting technologies that reduce lighting energy consumption by approximately 18%. Security Systems are evolving toward unified surveillance and biometric access management, while Fire & Safety remains essential due to stricter compliance requirements and intelligent emergency response integration. Companies are increasingly delivering interoperable automation platforms that combine all control systems into a unified ecosystem, simplifying deployment while improving operational efficiency and long-term asset utilization.

Energy Management represents the leading application because organizations increasingly prioritize operational efficiency, sustainability, and utility cost optimization across commercial facilities. Around 60% of new Building Automation System deployments incorporate advanced energy monitoring and intelligent load management, improving electricity efficiency by more than 20% while reducing peak demand by nearly 15%. Fire & Safety is the fastest-growing application as enterprises strengthen regulatory compliance and deploy intelligent emergency monitoring integrated with centralized building platforms. Technology providers are expanding digital energy optimization capabilities alongside automated compliance reporting and predictive analytics.

HVAC Control continues supporting occupant comfort and equipment reliability, while Lighting Control advances through adaptive illumination and occupancy-based automation. Security Systems are becoming more tightly integrated with access management, video analytics, and centralized command centers, improving enterprise-wide operational visibility. Vendors are increasingly developing unified application platforms that reduce system complexity, improve facility responsiveness, and deliver measurable operational efficiencies across diverse building environments.

Commercial Real Estate remains the largest end-user because office buildings, retail complexes, mixed-use developments, and business parks require continuous monitoring of energy consumption, occupant comfort, and operational performance. More than 62% of premium commercial developments now deploy centralized Building Automation Systems, reducing operating expenses by approximately 18% while improving equipment utilization by nearly 20%. Healthcare is the fastest-growing end-user as hospitals accelerate investments in intelligent environmental controls, infection-sensitive ventilation, and mission-critical infrastructure monitoring. Suppliers are expanding healthcare-focused automation portfolios through specialized software and integrated digital platforms.

Manufacturing continues increasing automation deployment to optimize utility consumption and production environments, while Government and Education institutions modernize aging infrastructure with intelligent energy and security management. Hospitality operators are adopting integrated guest-room automation and predictive maintenance to enhance customer experience while controlling operational costs. Companies are responding with industry-specific automation packages, flexible deployment models, and long-term service partnerships that strengthen customer retention across high-value end-user segments.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 6.8% CAGR between 2026 and 2033.

Enterprise Digital Building Modernization Drives Market Leadership

North America maintains the largest share of the Building Automation System Market through widespread deployment across commercial real estate, healthcare facilities, data centers, educational campuses, and industrial infrastructure. Nearly 68% of newly developed Class A commercial buildings integrate advanced building automation platforms, reflecting strong enterprise investment in intelligent energy optimization, predictive maintenance, and cybersecurity-enabled facility management. The region continues benefiting from large-scale retrofit activity and stricter building performance standards, while cloud-based automation deployments have increased by approximately 30% across multi-site enterprises. Technology providers are strengthening software ecosystems, expanding managed service offerings, and developing interoperable platforms that improve operational efficiency while supporting long-term sustainability objectives.

United States Market Outlook: The United States remains the operational center of the regional market through extensive smart building deployment, advanced software development, and continuous commercial infrastructure modernization. More than 70% of Fortune 500 corporate campuses utilize integrated building management platforms to optimize HVAC, lighting, and security operations. Strong investments in digital infrastructure, hyperscale data centers, and healthcare modernization continue strengthening enterprise demand for AI-enabled automation and intelligent facility management solutions.

Regulatory Modernization Accelerates Intelligent Infrastructure

Europe continues strengthening its Building Automation System Market through ambitious energy efficiency regulations, sustainable building renovation programs, and widespread digital infrastructure upgrades. Commercial buildings, manufacturing facilities, and public infrastructure increasingly deploy integrated automation systems to improve operational performance while meeting environmental compliance objectives. Nearly 58% of major commercial retrofit projects now incorporate centralized building management platforms, while intelligent energy optimization improves facility efficiency by over 18%. Vendors are expanding interoperable solutions and strengthening software integration capabilities to support increasingly complex regulatory and operational requirements across mature infrastructure portfolios.

Germany Market Outlook: Germany leads the regional market through advanced manufacturing capabilities, strong industrial automation expertise, and comprehensive building modernization initiatives. Commercial enterprises increasingly integrate intelligent HVAC, energy management, and security platforms to support operational efficiency and sustainability targets. More than 60% of newly certified green commercial developments incorporate advanced building automation technologies, reinforcing Germany's position as a leading innovation hub for intelligent building infrastructure.

Large-Scale Infrastructure Deployment Reshapes Regional Expansion

Asia-Pacific represents the fastest-expanding Building Automation System Market as rapid urbanization, commercial construction, industrial expansion, and smart city investments accelerate intelligent building deployment. The region accounts for a significant share of new commercial construction, while integrated automation installations have increased by approximately 34% across premium office developments and industrial facilities. Governments continue supporting digital infrastructure modernization alongside energy-efficient building programs, encouraging technology providers to expand manufacturing capacity, regional partnerships, and localized software development. Large-scale enterprise adoption continues strengthening long-term deployment opportunities across both developed and emerging economies.

China Market Outlook: China dominates regional deployment through extensive commercial construction, manufacturing leadership, and government-backed smart city development. Intelligent building technologies are increasingly integrated into business districts, hospitals, transportation hubs, and industrial parks. More than 65% of newly developed large-scale commercial complexes incorporate centralized automation platforms, while domestic technology companies continue strengthening AI-enabled building management capabilities through sustained research and industrial collaboration.

Commercial Infrastructure Modernization Supports Demand

South America continues expanding Building Automation System adoption through commercial real estate modernization, healthcare infrastructure upgrades, and growing investment in energy-efficient facilities. Building owners increasingly implement integrated automation to reduce operating costs, improve equipment reliability, and strengthen security management across large commercial properties. Intelligent energy management deployments have increased by approximately 22% in major urban developments, while multinational technology providers continue expanding regional partnerships and engineering support capabilities. Although infrastructure investment remains uneven, enterprise demand for integrated building management continues strengthening across high-value commercial projects.

Brazil Market Outlook: Brazil remains the largest regional market through ongoing investment in commercial developments, corporate facilities, healthcare infrastructure, and retail modernization. Enterprise organizations increasingly deploy centralized automation platforms to improve operational efficiency and reduce long-term utility expenses. Smart commercial buildings in major metropolitan areas continue expanding adoption of integrated HVAC, lighting, and security management, supported by increasing digital transformation initiatives across private-sector enterprises.

Smart Infrastructure Investment Strengthens Market Transformation

The Middle East & Africa Building Automation System Market continues advancing through smart city initiatives, commercial megaprojects, hospitality expansion, and public infrastructure modernization. Intelligent building technologies are increasingly deployed across airports, hospitals, premium commercial properties, and mixed-use developments to improve operational performance and sustainability outcomes. More than 28% of newly announced large-scale commercial developments now specify integrated automation platforms during project planning. Vendors are expanding regional partnerships, engineering capabilities, and digital service networks to support increasingly sophisticated infrastructure requirements across high-investment markets.

Saudi Arabia Market Outlook: Saudi Arabia leads regional deployment through large-scale smart city programs, commercial real estate expansion, and strategic infrastructure investment. Advanced building automation is becoming a core requirement across hospitality, healthcare, government facilities, and mixed-use developments supporting national modernization initiatives. Intelligent energy management and centralized building control systems continue gaining momentum as developers prioritize operational efficiency, digital integration, and long-term infrastructure resilience across flagship construction projects.

Global leaders including Siemens, Schneider Electric, Honeywell, Johnson Controls, and ABB compete directly through integrated automation platforms, while regional system integrators challenge them with lower-cost customization and localized deployment. Technology innovators increasingly compete against traditional hardware-focused OEMs by delivering AI-enabled software and cloud-based building management solutions. The top five companies collectively account for approximately 46% of the market, reflecting moderate consolidation with strong enterprise preference for proven platforms. Competition centers on interoperability, cybersecurity, lifecycle services, and deployment speed, with AI-enabled optimization improving operational efficiency by nearly 20% and predictive maintenance reducing service costs by approximately 25%. Leading vendors continue expanding through software acquisitions, strategic partnerships, edge-computing innovation, and vertical integration across sensors, controllers, and cloud platforms. The competitive landscape is shifting toward digital service ecosystems rather than standalone hardware, increasing pressure on companies lacking software capabilities. High certification requirements, integration expertise, and long-term customer relationships create substantial entry barriers. Sustainable competitive advantage depends on interoperable platforms, AI-driven intelligence, cybersecurity leadership, and enterprise-scale implementation capabilities.

Siemens AG

Schneider Electric SE

Honeywell International Inc.

Johnson Controls International plc

ABB Ltd.

Legrand SA

Delta Electronics Inc.

Bosch Building Technologies

Cisco Systems Inc.

Carrier Global Corporation

Lutron Electronics Co., Inc.

Beckhoff Automation GmbH

Crestron Electronics, Inc.

Artificial intelligence, IoT sensors, edge computing, and cloud-native building management platforms are redefining intelligent facility operations. More than 58% of newly deployed enterprise Building Automation Systems now integrate AI-driven analytics for predictive maintenance and energy optimization. Smart control algorithms reduce energy consumption by approximately 20%, while predictive diagnostics lower unexpected equipment failures by nearly 30%. Enterprises increasingly integrate HVAC, lighting, security, and occupancy analytics into unified digital platforms, strengthening operational visibility and accelerating automated decision-making across commercial infrastructure.

Digital twins, edge intelligence, and interoperable open-protocol architectures represent the next phase of technology adoption. Compared with conventional standalone control systems, AI-enabled integrated platforms improve operational efficiency by nearly 25% while reducing commissioning time by approximately 22%. Open communication standards including BACnet and KNX continue accelerating deployment across multi-vendor environments, with adoption exceeding 45% among premium commercial developments. Global technology leaders benefit through scalable software ecosystems, while specialized providers compete by delivering flexible integration and industry-specific automation capabilities.

Between 2026 and 2028, autonomous building operations, real-time digital twins, cybersecurity-first architectures, and generative AI-assisted facility management will become strategic differentiators. Intelligent automation platforms will support faster maintenance planning, stronger energy optimization, and improved asset utilization across complex facilities. Organizations investing early in interoperable AI-enabled ecosystems will strengthen operational resilience, reduce lifecycle costs, and secure competitive advantage as intelligent buildings become the enterprise infrastructure standard.

January 2024 – Honeywell launched its Advance Control building management platform, enabling deployment over existing building wiring while enhancing cybersecurity and AI-driven energy management. The solution supports up to 38% lower installation costs, accelerating retrofit adoption across commercial facilities. Source: honeywell.com

August 2024 – Honeywell and Cisco expanded their collaboration by integrating Honeywell Forge Sustainability+ with Cisco Spaces to optimize HVAC using real-time occupancy analytics. The AI-powered solution helps reduce building energy consumption by up to 20%, strengthening enterprise sustainability and operational efficiency. Source: Honeywell News

December 2024 – Honeywell secured a contract to deploy building automation technologies at Exide Energy's 80-acre lithium-ion gigafactory campus in Bengaluru, improving energy management, safety, and incident response while supporting advanced battery manufacturing infrastructure. Source: honeywell.com

February 2026 – Honeywell and Tata Consultancy Services announced a strategic partnership combining AI-powered building automation with cloud and IT modernization to accelerate autonomous building operations, enabling real-time predictive intelligence and enterprise-wide operational optimization. Source: TCS

The report delivers comprehensive analysis across Building Automation System types including HVAC Control, Lighting Control, Security Systems, Energy Management, and Fire & Safety while evaluating applications, end-user industries, deployment trends, and competitive positioning. It assesses market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level operational insights. More than 60% of enterprise smart building deployments emphasize integrated automation platforms, reflecting accelerating digital infrastructure adoption and intelligent facility management.

The study examines technology evolution including AI-enabled analytics, IoT connectivity, cloud-native building management, edge computing, digital twins, and cybersecurity integration. It evaluates deployment patterns, enterprise adoption strategies, competitive developments, and innovation priorities while profiling major industry participants. The report supports expansion planning, investment evaluation, product positioning, partnership strategies, and long-term business decisions by identifying high-opportunity segments, emerging deployment models, evolving customer requirements, and strategic market direction between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 80811.1 Million |

|

Market Revenue in 2033 |

USD 125913.24 Million |

|

CAGR (2026 - 2033) |

5.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens AG, Schneider Electric SE, Honeywell International Inc., Johnson Controls International plc, ABB Ltd., Legrand SA, Delta Electronics Inc., Bosch Building Technologies, Cisco Systems Inc., Carrier Global Corporation, Lutron Electronics Co., Inc., Beckhoff Automation GmbH, Crestron Electronics, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |