Reports

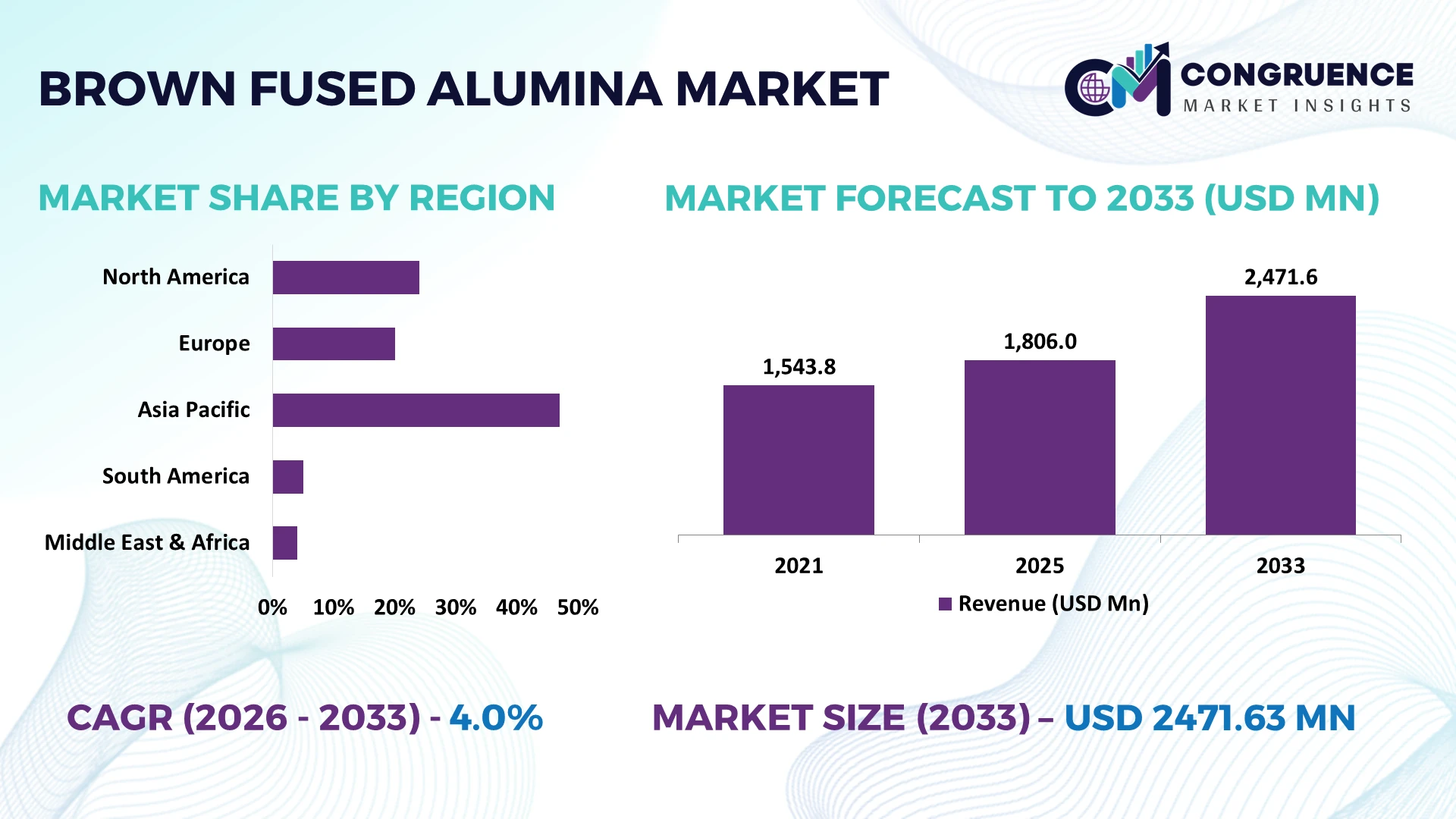

The Global Brown Fused Alumina Market was valued at USD 1806 Million in 2025 and is anticipated to reach a value of USD 2471.63 Million by 2033 expanding at a CAGR of 4% between 2026 and 2033. Rising deployment of high-performance abrasives, refractory modernization in steel production, and precision surface-finishing technologies are accelerating brown fused alumina consumption across industrial manufacturing.

China accounts for nearly 60% of global brown fused alumina production capacity through its integrated abrasives and refractory manufacturing ecosystem, supported by continuous furnace modernization and export-oriented operations. India has expanded production capacity by approximately 11% since 2024 through industrial investments, while Japan remains focused on premium-grade materials for precision engineering applications. Ongoing global supply-chain diversification in 2026 has further strengthened regional sourcing strategies across Asia.

Manufacturers investing in energy-efficient production, diversified sourcing, and premium-quality product portfolios are positioned to secure stronger long-term industrial contracts.

Market Size & Growth: Valued at USD 1806 Million in 2025 and projected to reach USD 2471.63 Million by 2033 at a CAGR of 4%, supported by expanding advanced abrasives and refractory manufacturing.

Top Growth Drivers: Steel production modernization (+9%), precision grinding demand (+11%), and industrial ceramics adoption (+8%) continue strengthening global market expansion.

Short-Term Forecast: By 2027, automated production systems are expected to reduce manufacturing costs by around 10% while increasing production efficiency by approximately 13%.

Emerging Technologies: AI-enabled process monitoring, automated electric furnaces, and advanced particle classification improve product consistency by nearly 15%.

Regional Leaders: Asia-Pacific leads at approximately USD 1.30 Billion, Europe reaches nearly USD 480 Million, and North America approaches USD 390 Million through industrial automation and localized manufacturing.

End-User Trends: More than 55% of premium abrasive manufacturers prioritize high-purity brown fused alumina for superior machining precision and longer product life.

Industrial Deployment: During 2026, digital furnace optimization projects improved energy efficiency by nearly 14% while reducing production variability across manufacturing facilities.

Competitive Landscape: The leading manufacturer controls approximately 18% of the market, with Saint-Gobain, Imerys, Washington Mills, CUMI, and Yichuan Zhongbang maintaining strong global positions.

Regulatory & ESG Impact: Energy-efficiency initiatives have lowered electricity consumption by nearly 9%, supporting cleaner industrial production and improved operational sustainability.

Investment Activity: More than USD 420 Million in expansion investments continues supporting capacity additions, localization strategies, and advanced production technologies amid global supply-chain realignment.

Innovation & Future Outlook: Smart manufacturing, premium refractory materials, and digital quality control are expected to improve production consistency by over 16%, strengthening long-term industrial competitiveness.

Brown fused alumina demand continues expanding across bonded abrasives, coated abrasives, refractory linings, blasting media, and precision ceramics as manufacturers prioritize durability and process efficiency. Advanced furnace automation and digital quality monitoring have improved product consistency by nearly 15%, while 2026 industrial supply-chain diversification is encouraging regional production expansion and greater procurement resilience, setting the stage for broader strategic market evaluation.

The Brown Fused Alumina Market is becoming strategically important as manufacturers prioritize material reliability, energy efficiency, and supply-chain control across abrasives, refractories, and precision manufacturing. The shift toward localized sourcing after global logistics disruptions has encouraged producers in China, India, and Europe to strengthen domestic processing capabilities and secure industrial supply continuity.

Advanced production technologies are reshaping competitiveness, with automated furnace monitoring improving operational efficiency by nearly 13% compared with conventional manual control systems. China maintains scale advantages through high-volume production, while Germany and Japan focus on premium-grade materials with advanced quality standards and specialized applications.

Companies are investing in energy-efficient furnaces, digital process controls, and long-term supply partnerships to improve consistency and reduce operational exposure. For example, Indian manufacturers are expanding export-focused facilities to support growing demand from automotive components and industrial machinery producers. Over the next 2–3 years, competitive advantage will depend on production optimization, sustainable manufacturing practices, and the ability to deliver customized alumina grades for high-value industrial applications.

Rising demand from steel, automotive, and precision engineering industries is strengthening brown fused alumina adoption. Steel production upgrades in China and India have increased refractory material requirements, while advanced grinding applications have expanded premium abrasive consumption by nearly 10%. Automated manufacturing processes are improving material utilization by approximately 12%, encouraging companies to invest in modern production lines. Chinese producers are upgrading furnace technologies, while Indian manufacturers are expanding export capabilities through capacity investments. The key strategic shift is the movement from commodity-grade alumina supply toward customized, performance-focused products that improve machining efficiency and reduce replacement frequency for industrial users.

High electricity consumption and raw material price volatility remain major constraints for brown fused alumina producers. Energy expenses represent nearly 30%–35% of production costs, creating profitability pressure during periods of power-price instability. China’s energy policy adjustments and tighter industrial emission controls have increased operational compliance requirements for manufacturers. Supply disruptions in bauxite availability have also influenced procurement strategies, increasing inventory management complexity. Companies are reducing exposure through diversified sourcing agreements, energy-efficient furnace investments, and localized supply networks. The major operational challenge is maintaining competitive pricing while meeting stricter environmental and production efficiency requirements.

Digital transformation is creating new opportunities through intelligent production systems, predictive maintenance, and automated quality control. AI-based monitoring solutions can improve furnace efficiency by approximately 15% and reduce production inconsistencies by nearly 12%. Growing demand for low-impact industrial materials is encouraging manufacturers to develop cleaner processing technologies and energy-saving production methods. India, Vietnam, and Southeast Asian manufacturing hubs are emerging as attractive expansion locations due to increasing industrial investments. Companies are strengthening competitiveness through R&D partnerships, advanced material development, and customized product offerings. A key opportunity lies in supplying specialized alumina grades for electric vehicle components, aerospace manufacturing, and high-precision industrial applications.

Scaling advanced brown fused alumina production while maintaining consistent quality remains a critical industry challenge. Premium-grade applications require strict particle-size control, where production variations of 5%–8% can affect downstream performance. Manufacturers face increasing pressure to integrate automation systems, upgrade infrastructure, and develop skilled technical teams. European producers emphasize quality compliance, while Asian manufacturers focus on cost-efficient large-scale production models. The growing adoption of digital manufacturing requires significant capital allocation and operational restructuring. Companies must overcome technology integration barriers, workforce capability gaps, and sustainability requirements to maintain long-term competitiveness in high-value industrial markets.

Smart Furnace Integration: Brown fused alumina producers are accelerating digital furnace adoption, with automated temperature controls improving energy efficiency by 12% and reducing process variation by nearly 10%. Chinese and Indian manufacturers are integrating predictive monitoring systems to optimize electricity usage, improve quality consistency, and strengthen competitiveness amid rising industrial energy costs.

Premium Grade Shift: Demand is moving toward high-performance alumina grades, with premium abrasive applications increasing adoption by approximately 9% and precision industries requiring tighter particle control by nearly 15%. Companies are restructuring product portfolios toward customized grades for automotive, aerospace, and advanced machining applications to capture higher-value contracts.

Supply Chain Localization: Global procurement strategies are changing as manufacturers increase local inventory and supplier diversification, reducing raw material disruption exposure by nearly 20%. European and Asian producers are expanding regional partnerships and improving logistics networks after recent supply-chain pressures, creating more resilient industrial sourcing models.

Sustainable Processing Upgrade: Environmental compliance and energy optimization are influencing production methods, with newer processing systems lowering electricity consumption by around 8% and improving resource utilization by 11%. Manufacturers are investing in cleaner furnace technologies and operational automation to meet evolving industrial sustainability expectations while maintaining cost efficiency.

Macro Grit represents the leading segment of the Brown Fused Alumina Market, accounting for approximately 38% share due to its extensive use in heavy-duty grinding wheels, abrasive tools, and industrial surface treatment. Its dominance comes from strong durability, scalable production, and cost advantages in large-volume manufacturing. Companies are expanding macro grit capacity to support demand from metalworking and steel processing industries, where consistent performance remains critical.

Micro Grit is emerging as the fastest-growing type, supported by precision machining requirements and advanced finishing applications, with adoption increasing by nearly 12%. Powder and refractory grade materials maintain strategic importance in ceramics and furnace lining applications, while abrasive grade products continue serving mature industrial users. Manufacturers are increasingly investing in classification technologies and customized particle sizes to improve performance differentiation.

Grinding & Polishing is the largest application segment, contributing nearly 42% of overall demand due to extensive usage in metal fabrication, automotive components, and industrial machinery finishing. Its dominance is supported by high-volume consumption, operational reliability, and compatibility with automated machining systems. Companies are improving abrasive formulations to extend tool life by approximately 10% and reduce material waste.

Precision Lapping is the fastest-growing application area, expanding by nearly 13% as semiconductor, aerospace, and high-accuracy engineering industries require superior surface finishing. Refractory Materials, Surface Preparation, and Sandblasting remain important applications, with demand patterns shifting toward specialized performance requirements. Manufacturers are increasing automation adoption and developing application-specific solutions to improve productivity and reduce processing time.

The Steel Industry remains the leading end-user segment with approximately 35% market share due to continuous refractory requirements, furnace maintenance, and high-temperature processing needs. Large steel producers in China and India are increasing investments in durable refractory materials, with advanced solutions improving operational cycles by nearly 10%. Companies are developing long-term supply agreements to ensure stable material availability.

Aerospace is emerging as the fastest-growing end-user, with demand rising by around 14% due to increasing requirements for precision finishing and lightweight component manufacturing. Automotive, Metalworking, and Foundries continue generating stable demand through machining, casting, and surface treatment applications. Suppliers are focusing on customized product development, technical partnerships, and regional expansion strategies to capture specialized industrial requirements.

Asia-Pacific accounted for the largest market share at 58% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Advanced Manufacturing and Industrial Reshoring Shift

North America is strengthening its position in the Brown Fused Alumina Market through demand from metalworking, aerospace, automotive, and industrial equipment sectors. The region contributes nearly 14% of global consumption, supported by specialized abrasive applications and domestic manufacturing expansion. The United States remains the primary demand center due to high adoption of precision machining and automated fabrication systems. Manufacturers are investing in localized supply agreements and upgraded processing capabilities to reduce dependence on imported materials. Recent industrial modernization programs have increased demand for high-performance abrasives by nearly 8%, particularly across aerospace component production and advanced manufacturing facilities.

United States Market Outlook: The United States market benefits from strong aerospace, automotive, and defense manufacturing infrastructure. More than 40% of regional brown fused alumina consumption is linked to precision machining and metal processing activities. Companies are prioritizing supplier diversification, automation integration, and premium-grade abrasive solutions to improve operational reliability.

Sustainable Production and High-Precision Applications

Europe’s Brown Fused Alumina Market is shaped by strict industrial sustainability standards, advanced engineering applications, and demand for premium-quality abrasive materials. The region represents approximately 16% of global consumption, with Germany, France, and Italy driving demand through automotive, machinery, and specialty manufacturing sectors. Energy efficiency requirements have encouraged producers to adopt improved furnace technologies, reducing production energy intensity by nearly 9%. European manufacturers are focusing on customized alumina grades, recycling initiatives, and strategic supplier partnerships to maintain competitiveness. Increasing automation in industrial processing is also strengthening demand for consistent particle-size materials.

Germany Market Outlook: Germany remains the leading European market due to its advanced automotive and industrial machinery ecosystem. Over 35% of domestic demand comes from precision engineering and metal fabrication applications. Manufacturers are expanding digital quality monitoring and sustainable processing systems to support higher-value industrial production.

Production Scale and Export-Oriented Expansion

Asia-Pacific dominates the Brown Fused Alumina Market with nearly 60% of global production capacity, supported by China’s large-scale manufacturing base and India’s growing industrial expansion. Strong demand from steel, refractory, automotive, and abrasive industries continues driving regional deployment. China maintains significant cost advantages through integrated raw material supply chains, while India is increasing export capacity through new production investments. Manufacturers are upgrading electric furnace operations and automation systems, improving productivity by approximately 12%. The region’s supply-chain restructuring trend is encouraging companies to develop diversified production networks and strengthen international partnerships.

China Market Outlook: China remains the largest producer with nearly 60% of global brown fused alumina capacity, supported by extensive refractory and abrasive manufacturing infrastructure. The country’s industrial clusters enable cost-efficient production, while companies are investing in cleaner furnace technologies and advanced material classification systems.

Industrial Modernization and Mining Sector Demand

South America represents an emerging market for brown fused alumina, supported by mining, metal processing, construction, and industrial manufacturing activities. Brazil leads regional demand due to its strong metallurgy sector and infrastructure development requirements. The region accounts for approximately 6% of global consumption, with adoption concentrated in grinding, surface preparation, and refractory applications. Industrial modernization projects have increased demand for durable abrasive materials by nearly 7%, although logistics limitations and import dependency remain operational challenges. Companies are improving regional distribution networks and forming supply partnerships to enhance availability and reduce delivery constraints.

Brazil Market Outlook: Brazil holds the strongest position in South America due to its mining and steel production capabilities. More than 45% of regional industrial abrasive demand originates from metal processing and mining-related activities. Companies are focusing on local partnerships and inventory expansion to support growing industrial requirements.

Industrial Diversification and Infrastructure Development

The Middle East & Africa Brown Fused Alumina Market is gaining momentum through infrastructure expansion, metal production growth, and industrial diversification programs. The region contributes nearly 5% of global demand, with Saudi Arabia, UAE, and South Africa representing key consumption centers. New steel and manufacturing investments are increasing demand for refractory and abrasive materials, while industrial facilities are adopting improved surface preparation technologies. Infrastructure modernization projects have supported approximately 8% growth in abrasive material usage across selected industrial sectors. Companies are exploring regional distribution hubs and strategic partnerships to improve supply reliability.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a significant market due to industrial diversification initiatives and expanding metallurgy investments. Steel and construction-related industries represent over 50% of domestic abrasive material demand. Manufacturers are strengthening supply networks and targeting industrial expansion projects through localized partnerships.

The Brown Fused Alumina Market features competition between global material specialists, regional cost-focused producers, and vertically integrated abrasive suppliers. Leading players such as Saint-Gobain, Imerys, Washington Mills, and CUMI compete against Chinese manufacturers focused on scale and pricing advantages. The top five companies collectively control approximately 45% of market share, creating a moderately consolidated structure. Competition is driven by production cost optimization, furnace efficiency, product customization, and supply reliability. Advanced processing technologies improve energy efficiency by 10%–15%, while automated quality control increases consistency by nearly 12%. Companies are expanding capacity, forming supply partnerships, and investing in cleaner production systems to strengthen positioning. The competitive shift is moving toward sustainable manufacturing, premium-grade materials, and localized supply chains. High energy requirements, technical expertise, and established customer relationships create entry barriers. Winning players will combine cost leadership, technology integration, and reliable global supply capabilities.

Saint-Gobain

Imerys

Washington Mills

CUMI (Carborundum Universal Limited)

Electro Abrasives

Yichuan Zhongbang Abrasives

Orient Abrasives

Henan Ruishi Renewable Resources Group

Zhengzhou Haixu Abrasives

LKAB Minerals

SPARX Abrasives

White Fused Alumina Company

Bosai Minerals Group

Motim Electrocorundum

Brown fused alumina production is shifting from conventional furnace operations toward automated electric furnace systems with real-time monitoring. Modern process controls improve energy efficiency by approximately 12% and reduce production variation by nearly 10% compared with manual operations. Companies are integrating sensors, predictive analytics, and digital quality management platforms to maintain consistent grain size and chemical composition across industrial batches.

Emerging technologies include AI-based furnace optimization, automated material classification, and advanced recycling processes. AI-driven monitoring systems achieve nearly 15% improvement in operational efficiency, while automated classification increases product accuracy by around 13%. Adoption is strongest among large-scale producers in China, India, and Europe, where manufacturers are upgrading facilities to meet premium abrasive and refractory requirements.

Between 2026 and 2028, disruptive advancements will focus on low-energy processing, smart manufacturing integration, and sustainable production models. New automated systems outperform legacy methods by improving productivity nearly 20% while reducing operational waste. Cost-focused producers benefit from scale and automation, while premium manufacturers gain competitive advantages through customized high-performance alumina grades. Companies adopting digital manufacturing early will strengthen supply reliability, improve margins, and capture demand from advanced industrial applications.

June 2025 Hindalco Industries expanded its specialty alumina portfolio through the acquisition of AluChem Companies for USD 125 million, adding advanced alumina capabilities and three US manufacturing facilities. The move strengthens high-value material supply chains and supports premium industrial applications.

May 2026 Carborundum Universal Limited announced expansion projects including an integrated fused alumina furnace facility and grain processing upgrades with approximately INR 400 crore investment. The expansion improves manufacturing capacity, supports thermal spray applications, and strengthens its abrasive material portfolio. Source:https://www.nseindia.com

March 2025 Hindalco Industries announced a strategic investment commitment of INR 45,000 crore across aluminium, copper, and specialty alumina businesses. The initiative targets advanced materials growth, strengthens integrated production capabilities, and improves competitiveness in technology-driven alumina applications.

July 2025 Washington Mills maintained its position as a major fused mineral producer with more than 120,000 short tons of crude fused alumina annual fusion capacity across North American operations. The capacity base supports abrasive and refractory customers requiring stable regional supply. Source: https://www.usitc.gov

The Brown Fused Alumina Market report covers comprehensive segmentation across Macro Grit, Micro Grit, Powder, Refractory Grade, and Abrasive Grade types, along with applications including Grinding & Polishing, Refractory Materials, Surface Preparation, Sandblasting, and Precision Lapping. The study evaluates demand patterns across Metalworking, Foundries, Steel Industry, Automotive, and Aerospace end-users with detailed analysis of major industrial markets.

The report examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa dynamics, highlighting production concentration, technology adoption, supply-chain strategies, and competitive positioning. With analysis of automation, furnace modernization, sustainable processing, and advanced material development trends, the report supports investment planning, expansion decisions, supplier evaluation, and strategic positioning from 2026 to 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1806 Million |

Market Revenue in 2033 | USD 2471.63 Million |

CAGR (2026 - 2033) | 4% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Saint-Gobain, Imerys, Washington Mills, CUMI (Carborundum Universal Limited), Electro Abrasives, Yichuan Zhongbang Abrasives, Orient Abrasives, Henan Ruishi Renewable Resources Group, Zhengzhou Haixu Abrasives, LKAB Minerals, SPARX Abrasives, White Fused Alumina Company, Bosai Minerals Group, Motim Electrocorundum |

Customization & Pricing | Available on Request (10% Customization is Free) |