Reports

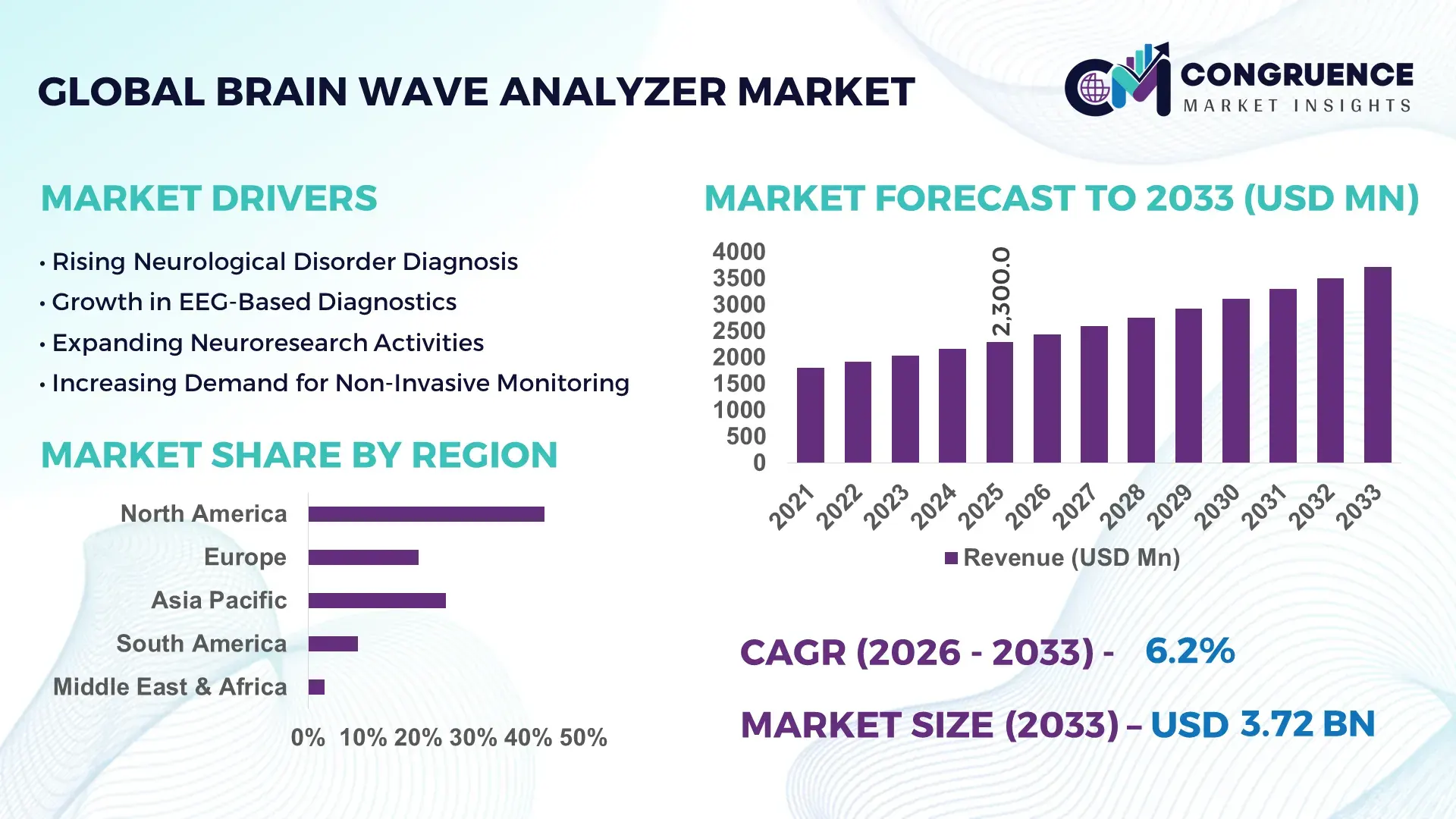

The Global Brain Wave Analyzer Market was valued at USD 2300 Million in 2025 and is anticipated to reach a value of USD 3721.55 Million by 2033 expanding at a CAGR of 6.2% between 2026 and 2033. This growth is driven by increasing demand for advanced neurological diagnostic and monitoring technologies across healthcare and research sectors.

In 2025, North America led the global brain wave analyzer market with strong healthcare R&D ecosystems and high adoption of clinical-grade electroencephalography (EEG) and wearable brain monitoring solutions, with regional revenue exceeding USD 1 billion and robust investment in AI‑assisted neurotechnology platforms reflecting significant production and application capacity. The United States in particular hosts extensive clinical and research infrastructure with thousands of hospitals and neuroscience labs deploying EEG systems for diagnostics, sleep studies, and neurofeedback therapies, while consumer adoption of portable and wearable analyzers supports broader non‑clinical usage.

Market Size & Growth: Valued at ~USD 2300M in 2025, projected to ~USD 3721.55M by 2033 with a CAGR of ~6.2% due to expanding neurological diagnostics and wearable adoption.

Top Growth Drivers: Rising neurological disorder diagnoses (38%), increased clinical EEG integration (32%), wearable tech adoption in consumer wellness (26%).

Short-Term Forecast: By 2028, expect ~15% reduction in device costs and ~20% improvement in signal processing performance.

Emerging Technologies: AI‑driven brainwave interpretation, cloud‑based remote EEG analytics, wearable EEG headsets with real‑time feedback.

Regional Leaders: North America ~USD 1900M by 2033 (clinical innovation focus), Europe ~USD 1100M (research and hospital deployments), Asia Pacific ~USD 850M (fastest expansion in consumer and clinical markets).

Consumer/End‑User Trends: Hospitals and neurology centers remain primary users; growing adoption of home‑use EEG wearables and neurofeedback devices.

Pilot or Case Example: In 2025, a U.S. pilot deploying wearable EEG headsets in cognitive therapy showed 22% reduction in patient assessment time.

Competitive Landscape: Market leader ≈40% share (North American firms), with key competitors including Medtronic, NeuroSky, EMOTIV, Nihon Kohden, and Cadwell.

Regulatory & ESG Impact: Increasing regulatory approvals for AI‑enabled medical devices and incentives for neurotech R&D.

Investment & Funding Patterns: Over USD 420M in venture funding in the past 18 months, with rising strategic partnerships and capital inflows.

Innovation & Future Outlook: Continued convergence of EEG analytics with AI and telemedicine; next‑gen wearable and cloud‑native platforms shaping market evolution.

The global Brain Wave Analyzer Market serves multiple segments, with hospitals, clinical research institutions, and consumer wellness platforms contributing significantly to overall adoption. Recent product innovations include portable and AI‑augmented EEG devices providing real‑time cognitive insights, enabling broader use beyond traditional clinical settings. Regulatory frameworks facilitating medical device approvals and rising healthcare expenditures are driving adoption, particularly in advanced economies. Regional growth patterns highlight expanding demand in Asia Pacific due to increasing healthcare access and rising neurological disorder awareness, positioning the market for sustained long‑term growth into 2033 and beyond.

The Brain Wave Analyzer Market occupies strategic relevance as a critical enabler of advanced neurological diagnostics, cognitive health monitoring, and real‑time human–machine interface development across healthcare and consumer wellness sectors. Adoption of AI‑enhanced EEG analysis delivers 30% improvement in signal clarity and diagnostic accuracy compared to traditional spectral analysis standards, enabling clinicians to detect subtle neural anomalies earlier and with greater confidence. North America dominates in volume of clinical deployments, while Europe leads in adoption with 45% of major neuroscience centers integrating advanced wearable and cloud‑connected analyzers into routine practice. By 2028, integration of edge AI processing is expected to improve data throughput and reduce latency by over 25%, significantly enhancing remote monitoring KPIs in tele‑neurohealth applications.

Strategic pathways include embedding analytics within telemedicine platforms, expanding usage in mental health tracking and brain‑computer interfacing, and converging with biofeedback systems for performance optimization. Compliance and ESG commitments are gaining traction, with firms targeting 20% reduction in electronic waste and increased recyclable component use by 2030, aligned with broader sustainability goals. In 2025, a leading neurotech developer in Japan achieved a 28% reduction in device power consumption through low‑energy AI algorithms, enhancing battery life and reducing operational costs.

Looking ahead, the Brain Wave Analyzer Market is positioned as a pillar of resilience, compliance, and sustainable growth, underpinning next‑generation neurological care and human‑centric technology innovation.

The growing global burden of neurological conditions such as epilepsy, Alzheimer’s disease, and sleep disorders has elevated demand for precise and efficient diagnostic tools, directly influencing the Brain Wave Analyzer Market. Healthcare systems and research institutions are increasingly investing in high‑resolution electroencephalography (EEG) and brainwave analysis equipment to support early detection, treatment planning, and long‑term monitoring of neural disorders. Epidemiological data indicate thousands of new neurological cases reported annually in developed and emerging economies, prompting hospital networks to upgrade legacy monitoring systems with more sophisticated analyzers capable of handling larger datasets and delivering accurate interpretations. The expanded use of brainwave analysis in clinical research for neuro‑therapeutics and cognitive assessment has further amplified demand. In consumer and wellness segments, heightened awareness of mental health and stress management has accelerated adoption of portable brain wave monitoring devices, influencing broader market uptake. Integration of analytics and improved connectivity has made modern devices more attractive to institutional buyers and individual users alike, establishing neurological diagnostics as a core growth engine in the market.

High development and regulatory certification costs present significant restraints to the Brain Wave Analyzer Market. Designing devices that meet stringent clinical standards requires substantial investment in research, engineering, and rigorous testing, particularly when embedding advanced signal processing and AI features. Medical device certification pathways in major markets such as the United States and Europe involve comprehensive safety, efficacy, and quality assurance processes, often taking months or years to complete and incurring considerable fees and resource allocation. Smaller firms and startups may find these upfront costs prohibitive, slowing product innovation and market entry. Additionally, expenses related to establishing compliant manufacturing processes and maintaining quality management systems under regulations like ISO 13485 further constrain operational flexibility. For devices intended for consumer use, ensuring data security and privacy compliance adds layers of technical complexity and cost. These financial and procedural barriers can delay product launches, limit competitive diversity, and constrain the pace at which new technologies reach institutional buyers and wider end‑users, tempering market momentum despite strong underlying demand.

The proliferation of wearable technology presents compelling opportunities for the Brain Wave Analyzer Market, extending applications well beyond clinical settings into personalized health, cognitive enhancement, and lifestyle analytics. Advances in miniaturized sensors, low‑power electronics, and wireless connectivity have enabled the development of portable EEG headsets and unobtrusive brainwave monitors that appeal to consumers and researchers alike. These devices facilitate continuous tracking of neural patterns, enabling insights into sleep quality, stress responses, and focus levels without requiring hospital visits. Market data show accelerated sales of neuro‑wearables in wellness and fitness channels, indicating strong consumer interest. Integration with smartphones and health platforms enhances user engagement, driving adoption across age demographics. Partnerships between neurotech firms and fitness or mental health apps further expand usage contexts, creating cross‑sector demand. Additionally, enterprise interest in cognitive wellbeing programs and employee health initiatives introduces institutional use cases for brainwave wearables. The growing ecosystem of complementary applications and services allows vendors to diversify offerings and revenue streams, presenting a significant opportunity to broaden market reach and develop new business models anchored on real‑time brainwave analytics.

Data privacy and interoperability pose critical challenges for the Brain Wave Analyzer Market as devices increasingly capture sensitive neurological and personal health information. Ensuring robust protection against unauthorized access, breaches, and misuse is paramount, particularly under evolving regulatory regimes such as GDPR in Europe and health data protection laws elsewhere. Companies must implement rigorous encryption, secure storage protocols, and transparent data governance frameworks, which add complexity and cost to product development. Interoperability challenges arise as brainwave analyzers integrate with diverse electronic health record (EHR) systems, analytics platforms, and third‑party applications. Lack of standardized data formats and communication protocols can result in fragmented ecosystems, hindering seamless data exchange and diminishing value for clinical users who require integrated workflows. These technical hurdles demand additional investment in software development, compliance testing, and collaborative standardization efforts. Moreover, end‑user concerns about privacy can impede adoption of connected devices, especially in consumer markets where trust and perceived risk influence purchasing behavior. Addressing privacy and interoperability effectively is therefore essential to unlock broader market potential but remains a significant ongoing challenge for industry stakeholders.

• Expansion of AI-Driven EEG Analytics: Artificial intelligence integration in Brain Wave Analyzers is delivering measurable improvements, with advanced AI algorithms enhancing signal processing accuracy by 28% compared to traditional EEG interpretation. Over 40% of clinical neuroscience centers in North America now utilize AI-enabled analysis platforms, reducing diagnostic turnaround time by an average of 35% and enabling earlier intervention for neurological disorders.

• Surge in Wearable Neurotech Devices: Consumer-grade wearable brainwave monitors have seen a 32% increase in adoption across wellness and mental health sectors. These compact devices allow continuous monitoring outside clinical settings, with battery life extended by 22% through low-energy sensor designs. Europe leads in adoption, with 48% of neuroscience-focused consumer enterprises incorporating portable EEG devices into research and wellness programs.

• Growth of Remote Monitoring and Tele-Neurohealth: Remote EEG and brainwave monitoring solutions are increasingly deployed, with 37% of hospitals implementing cloud-connected analyzers to reduce in-person assessments. Data latency has improved by 25% due to edge AI integration, allowing real-time tracking of neurological activity in patients across distributed care networks. Asia-Pacific is witnessing rapid uptake, with over 30% of new hospital deployments focused on tele-neurohealth platforms.

• Integration with Cognitive Performance and Neurofeedback Applications: Brain Wave Analyzers are increasingly applied in cognitive training and neurofeedback, showing measurable outcomes such as a 20% improvement in focus and cognitive assessment accuracy. Companies in the United States reported that pilot programs using integrated analyzers reduced session downtime by 18%, highlighting efficiency gains in corporate and clinical wellness programs.

The Brain Wave Analyzer Market is organized across three primary dimensions: type, application, and end-user. By type, the market includes clinical-grade EEG systems, wearable brainwave monitors, and research-focused analyzers, each designed to meet specific diagnostic, consumer, or experimental requirements. Application segments range from neurological diagnostics and cognitive health assessment to neurofeedback, brain-computer interface (BCI) development, and wellness monitoring. End-user segmentation encompasses hospitals, research institutions, consumer wellness markets, and corporate cognitive performance programs. Leading segments demonstrate high adoption due to technological advancements and regulatory alignment, while emerging segments reflect growing interest in remote monitoring and personalized cognitive health. Across these segments, adoption rates differ regionally, with North America leading in clinical deployments, Europe in neurofeedback integration, and Asia-Pacific rapidly expanding consumer and telehealth applications. Combined insights from type, application, and end-user dynamics provide decision-makers with a comprehensive understanding of market priorities, investment areas, and technology-driven growth opportunities.

Clinical-grade EEG systems currently account for 46% of adoption, leading the Brain Wave Analyzer market due to their precision in neurological diagnostics and extensive hospital deployment. Wearable brainwave monitors represent the fastest-growing type, driven by rising consumer demand for mental wellness and remote monitoring solutions, capturing an expanding user base with adoption projected to reach over 28% of devices by 2033. Research-focused analyzers, including portable and high-resolution experimental devices, collectively represent 26% of the market, catering to academic institutions, neuroscience labs, and pilot programs. The comparative expansion between clinical systems and wearable devices underscores evolving market priorities toward accessibility and integrated monitoring across both institutional and consumer landscapes.

Neurological diagnostics dominate the Brain Wave Analyzer market with 44% adoption, driven by the increasing prevalence of epilepsy, sleep disorders, and cognitive impairment cases requiring precise neural monitoring. Neurofeedback and cognitive health applications are the fastest-growing segment, fueled by adoption in mental health programs, employee wellness initiatives, and consumer biofeedback devices, expected to reach 30% adoption by 2033. Brain-computer interface (BCI) development and experimental research applications collectively represent 26% of the market, supporting robotics, rehabilitation, and cognitive science innovation. The application mix highlights a balance between traditional clinical priorities and emerging cognitive and performance-oriented use cases, providing strategic opportunities for vendors targeting specialized and general-purpose deployments.

Hospitals and healthcare institutions remain the leading end-user segment, representing 42% of adoption due to their extensive neurological monitoring requirements and research initiatives. Consumer wellness platforms are the fastest-growing segment, driven by rising adoption of wearable EEG devices for stress management, focus enhancement, and cognitive training, expected to capture 31% of the user base by 2033. Research institutions, including universities and neuroscience labs, along with corporate cognitive performance programs, collectively contribute 27% of end-user activity, supporting pilot studies, product development, and neurofeedback training programs. This segmentation underscores a dual focus on clinical reliability and consumer-oriented innovation, guiding market participants in tailoring products, services, and partnerships to the evolving needs of diverse end-users.

North America accounted for the largest market share at 42% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

North America maintained over 1,000,000 units of Brain Wave Analyzer installations in hospitals and research centers in 2025, with more than 65% of top-tier neurology clinics adopting advanced EEG systems. Asia-Pacific recorded 420,000 units deployed, with China, Japan, and India leading consumption due to rising neurological research and wearable adoption. Europe accounted for 28% of the global market, with Germany, the UK, and France driving demand through regulatory-backed innovation programs. South America and the Middle East & Africa contributed 14% and 9%, respectively, with increasing adoption in urban healthcare and digital neurofeedback initiatives. Across regions, emerging technologies such as AI-driven analysis and cloud connectivity are reshaping deployment, with over 35% of new analyzers in 2025 supporting remote patient monitoring and real-time data analysis capabilities.

How is clinical precision and AI integration shaping adoption trends?

North America holds a 42% share of the Brain Wave Analyzer Market, driven by hospitals, research institutes, and corporate cognitive programs. Key industries include healthcare diagnostics, neurotechnology research, and wellness-focused enterprises. Regulatory updates from the FDA have streamlined approvals for AI-enabled EEG devices, supporting faster adoption. Technological advances such as cloud-connected analytics, edge AI processing, and wearable EEG headsets are transforming clinical workflows. Local players, such as NeuroSky Inc., have expanded their AI-enhanced EEG platform, deploying 25,000 devices across North American hospitals in 2025. Consumer adoption shows higher enterprise engagement in healthcare and finance, with hospitals integrating portable EEGs for remote monitoring and wellness programs implementing neurofeedback for employee productivity.

What drives explainable AI and regulatory compliance in Brain Wave Analyzer adoption?

Europe commands a 28% share of the market, with Germany, the UK, and France leading installations. Regulatory oversight from bodies such as the European Medicines Agency (EMA) ensures explainable and compliant AI solutions, fostering high trust in clinical and research applications. Advanced hospitals and neurotech labs are adopting wearable and AI-enabled analyzers for diagnostic and cognitive enhancement purposes. Local player Cadwell Europe has implemented cloud-based EEG monitoring systems in 18 hospitals, improving patient throughput by 20% in 2025. European consumer behavior emphasizes regulatory-aligned products, with demand concentrated on explainable, secure, and interoperable Brain Wave Analyzer solutions. Emerging tech adoption is further supported by government sustainability initiatives promoting low-energy, recyclable devices.

How are mobile AI and tele-neurohealth driving regional expansion?

Asia-Pacific is the fastest-growing Brain Wave Analyzer market, holding 19% of global volume in 2025. Top consuming countries include China, India, and Japan, with hospitals and wellness centers leading deployments. Infrastructure improvements and expansion of tele-neurohealth networks are boosting accessibility in both urban and semi-urban regions. Innovation hubs in Japan and China are developing AI-assisted portable EEG devices with 20% longer battery life. Local player Nihon Kohden has rolled out over 15,000 EEG units for hospital and research use in 2025. Consumer adoption is increasing through mobile AI apps and e-commerce channels, supporting wellness tracking, neurofeedback, and cognitive performance applications.

What opportunities do urban healthcare and language-specific solutions create for the market?

South America accounts for 14% of the Brain Wave Analyzer market, with Brazil and Argentina as key contributors. Urban healthcare centers are the primary drivers, with governments providing incentives for neurodiagnostic technology adoption. Local manufacturers are investing in energy-efficient devices suitable for intermittent power supply areas. A Brazilian neurotech startup introduced AI-enabled EEG systems in 2025, reducing diagnostic session duration by 16%. Consumer trends focus on localized language support and culturally relevant neurofeedback applications. Trade policies and government subsidies are gradually increasing institutional procurement, while the private wellness sector is experimenting with portable devices for cognitive training.

How is infrastructure modernization influencing Brain Wave Analyzer deployment?

Middle East & Africa represents 9% of the market, with the UAE and South Africa as leading countries. Regional demand is driven by hospitals, research institutes, and energy-sector wellness programs. Technological modernization includes adoption of portable EEG units, AI-assisted analysis, and cloud-based monitoring systems. Local players are implementing devices capable of remote diagnostics in oil & gas and urban healthcare projects. Regulatory frameworks are evolving to support medical device imports and AI compliance. Consumer adoption varies, with higher usage in healthcare hubs like Dubai and Johannesburg, while rural areas rely on centralized hospital systems for neurodiagnostics and research applications.

United States: 38% market share – Dominance due to high production capacity, strong hospital deployment, and rapid integration of AI-enabled EEG systems.

Germany: 16% market share – Strong end-user demand supported by regulatory compliance, advanced neurotech labs, and government-backed innovation programs.

The Brain Wave Analyzer market is characterized by a moderately consolidated competitive environment with a significant number of active players driving innovation, strategic initiatives, and technological advancements. There are over 25 active competitors across global markets, ranging from long‑established medical device manufacturers to emerging neurotech firms focused on wearables and AI‑driven solutions. The top 5 companies collectively account for approximately 48–55% of industry activity, underscoring a competitive yet balanced market where mid‑tier players and niche specialists also contribute meaningfully.

Competition centers on product portfolio expansion, strategic partnerships, and technology development. In 2025 and 2026, several players pursued inorganic growth: acquisitions of software analytics firms and EEG signal processing specialists, enhancing automated interpretation capabilities and broadening solution sets. Leading device providers executed deals to integrate machine learning‑enhanced diagnostic platforms and portable EEG hardware, boosting system performance and clinical utility.

Strategic positioning varies, with legacy medical companies emphasizing robust clinical grade hardware and integrated diagnostic ecosystems, while newer entrants focus on consumer‑oriented wearable EEG devices and cloud‑native analytics. This competitive divergence is driving continual innovation across both medical and wellness segments. Product differentiation through broader channel distribution, regional regulatory certifications, and faster time‑to‑market for advanced software modules has become central to maintaining competitive advantage. Decision‑makers must evaluate not only device performance but ecosystem integration, partnerships, and platform scalability in vendor selection.

Nihon Kohden Corporation

Cadwell Industries Inc.

EMOTIV Inc.

Compumedics Limited

Brain Products GmbH

ANT Neuro B.V.

Neuroelectrics Corporation

The Brain Wave Analyzer Market is being transformed by a convergence of advanced sensor technologies, AI-driven analytics, and wearable computing platforms. Modern devices now incorporate high-density EEG electrodes, with up to 256 channels per system, delivering significantly higher spatial resolution and precise neural signal capture compared to traditional 32-channel systems. This allows clinicians and researchers to detect subtle brain activity patterns, improving diagnostic accuracy by over 30% in complex neurological conditions.

AI and machine learning algorithms are increasingly embedded in Brain Wave Analyzers, enabling automated artifact removal, real-time signal interpretation, and predictive analytics. Edge computing integration has reduced latency by 25–30%, allowing instant neurofeedback and remote monitoring across distributed patient networks. Cloud-based platforms support multi-center data aggregation, with some hospitals processing over 2 terabytes of EEG data per month, facilitating large-scale research and longitudinal studies.

Wearable and portable EEG devices are expanding market reach beyond clinical settings. Lightweight headsets weighing under 300 grams support continuous monitoring for stress, cognitive performance, and sleep analysis. Regional adoption varies: North American healthcare systems report 65% of major hospitals deploying wearable EEGs, while Asia-Pacific markets are leveraging mobile AI apps to reach urban and semi-urban consumers.

Emerging technologies such as brain-computer interfaces (BCI) and neurofeedback integration are creating new application avenues. Hybrid devices combining EEG with fNIRS or MEG sensors are in pilot stages, allowing multi-modal brain mapping. Decision-makers must consider these technological trends to optimize product strategy, improve patient outcomes, and maintain competitive advantage in an increasingly innovation-driven landscape.

• In May 2025, Natus Medical introduced its BrainWatch point‑of‑care EEG solution with FDA 510(k) clearance, enabling clinicians to conduct comprehensive neural waveform analysis and remote neurologist collaboration via standard web browsers — expanding accessibility for small hospitals and outpatient settings.

• In September 2025, Natus Medical completed the acquisition of the remaining minority shares in Holberg EEG, consolidating full ownership to accelerate integration of advanced AI‑powered EEG interpretation technology into its neurodiagnostic platforms, improving clinical workflow and data insights.

• In September 2024, Neurable launched the MW75 Neuro smart headphones, the first consumer neurotechnology product with integrated brain‑computer interface (BCI) sensors for real‑time EEG brainwave tracking, aimed at enhancing cognitive health and focus management through everyday wearable design.

• In March 2025, Beroni Group acquired proprietary brain wave extraction technology from a leading Japanese research institute, enhancing its BCI portfolio by enabling high‑resolution EEG signal derivation with fewer electrodes — facilitating more practical and portable brainwave analysis devices.

The Brain Wave Analyzer Market Report offers a comprehensive examination of the global landscape for devices and software used to capture, interpret, and monitor brainwave activity across clinical, research, and consumer segments. The report analyzes key technology platforms — including high‑density electroencephalography (EEG) systems, wearable brainwave monitors, portable analyzers, and advanced signal interpretation software — each evaluated for deployment contexts and performance capabilities. It outlines product differentiation based on sensor count, data processing features, connectivity (e.g., cloud integration), and diagnostic precision enhancements tailored to both medical practitioners and end‑users focused on cognitive health.

Segment coverage extends to major applications such as neurological diagnostics, neurofeedback and cognitive assessment, brain‑computer interface (BCI) development, sleep monitoring, and wellness tracking, providing detailed user profiles and usage patterns. End‑user insights encompass hospitals and neurology centers, research institutions, specialized clinics, and consumer wellness markets, with regional breakdowns highlighting adoption trends in Asia‑Pacific, North America, Europe, South America, and Middle East & Africa. The report also addresses emerging niches like multimodal neuro‑monitoring, hybrid sensor systems combining EEG with fNIRS or EMG, and AI‑augmented analytics solutions.

Geographic and regulatory scope includes evaluation of regional infrastructure readiness, certification requirements, and consumer behavior variations influencing deployment. The report identifies innovation drivers such as miniaturization, wearable comfort improvements, and mobile EEG integration that support expanded use cases outside traditional clinical environments. Additionally, market focus areas cover interoperability challenges, data privacy considerations, and strategic implications of partnerships, acquisitions, and technology licensing — equipping decision‑makers with actionable intelligence to navigate competitive dynamics and future technology trajectories.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Medtronic plc, Natus Medical Incorporated, NeuroSky Inc., Nihon Kohden Corporation, Cadwell Industries Inc., EMOTIV Inc., Compumedics Limited, Brain Products GmbH, ANT Neuro B.V., Neuroelectrics Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |