Reports

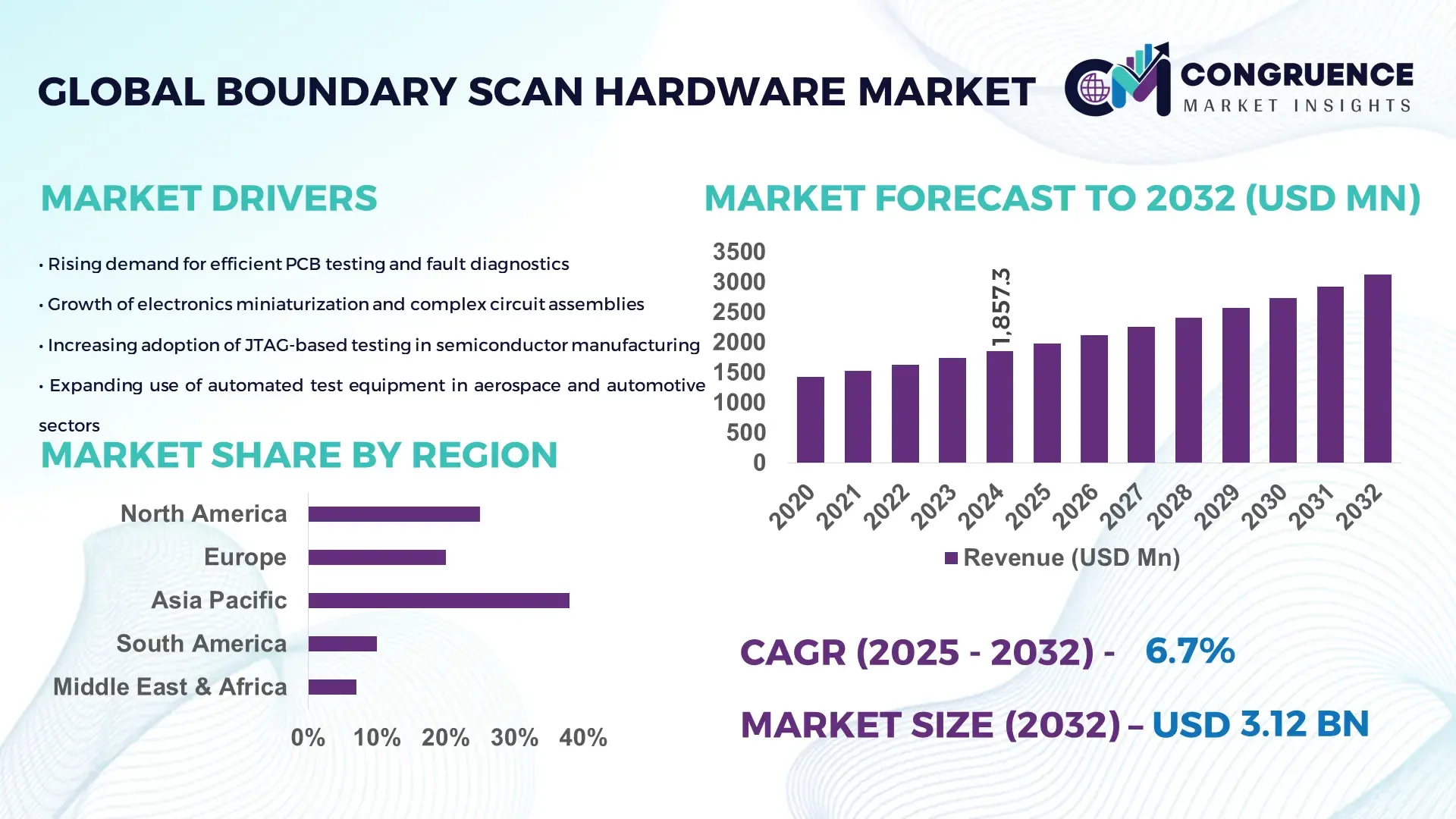

The Global Boundary Scan Hardware Market was valued at USD 1,857.32 Million in 2024 and is anticipated to reach a value of USD 3,120.35 Million by 2032 expanding at a CAGR of 6.7% between 2025 and 2032. This growth is supported by rising demand for advanced testability solutions across high-density electronic systems.

The United States remains the dominant country in the Boundary Scan Hardware market, driven by large-scale semiconductor production capacity exceeding 130 billion IC units annually, strong capital expenditure by OEMs, and extensive deployment across aerospace, defense, telecom, and automotive electronics. The country also records more than 48% adoption of boundary scan technologies in PCB design validation and hardware debugging workflows. In 2023–2024, U.S. enterprises invested over USD 2.6 billion in embedded test and inspection automation, along with a significant rise in R&D activities focused on high-speed interconnect testing, system-level diagnostics, and advanced JTAG integration for next-generation chipsets and mission-critical electronics.

Market Size & Growth: Valued at USD 1.85 Billion in 2024, projected to reach USD 3.12 Billion by 2032 with a 6.7% CAGR, supported by increasing requirements for non-intrusive PCB testing.

Top Growth Drivers: 42% adoption of automated PCB diagnostics, 37% efficiency improvement in high-density board testing, and 33% rise in multi-board integration testing.

Short-Term Forecast: By 2028, boundary scan-enabled test efficiency is expected to improve by 25% through enhanced integration of AI-driven diagnostic tools.

Emerging Technologies: Growth fueled by AI-assisted test automation, advanced JTAG extension modules, and high-speed serial boundary scan architectures.

Regional Leaders: North America projected at USD 1.02 Billion by 2032 with strong aerospace adoption; Europe at USD 860 Million with automotive electronics growth; Asia-Pacific at USD 940 Million driven by semiconductor manufacturing expansion.

Consumer/End-User Trends: Strong uptake among telecom, aerospace, and automotive OEMs, with rising integration into EV power electronics and 5G infrastructure boards.

Pilot or Case Example: A 2024 pilot in automotive ECU testing achieved a 31% reduction in diagnostic time using enhanced boundary scan controllers.

Competitive Landscape: Market led by an estimated 18% share held by Corelis, with major competitors including JTAG Technologies, Keysight Technologies, XJTAG, and Teradyne.

Regulatory & ESG Impact: Increasing compliance requirements for electronic safety testing and environmentally responsible manufacturing standards accelerating adoption.

Investment & Funding Patterns: Over USD 1.1 billion invested globally in 2023–2024 across embedded test automation, advanced JTAG toolchains, and semiconductor testing infrastructure.

Innovation & Future Outlook: Advancements in system-level boundary scan integration, real-time fault detection, and hybrid test architectures are shaping next-generation electronics validation workflows.

Unique information about the Boundary Scan Hardware Market

The Boundary Scan Hardware market is experiencing strong contributions from sectors such as aerospace electronics, automotive ECUs, telecom network infrastructure, and semiconductor manufacturing equipment, each driving significant usage volumes in 2023–2024. Continuous innovations in high-pin-count device testing, multi-chain JTAG architectures, and real-time PCB fault localization are reshaping hardware diagnostics. Regulatory compliance for electronic safety, increasing PCB design complexity, and accelerated digitalization in manufacturing environments further influence adoption. Asia-Pacific shows strong consumption patterns powered by electronics manufacturing clusters, while North America leads in technologically advanced deployments. Emerging trends include hybrid test systems, AI-assisted debugging modules, and enhanced system-level test integration that will define future market progression.

The strategic relevance of the Boundary Scan Hardware Market is strengthening as electronic systems become denser, more complex, and increasingly dependent on non-intrusive testing architectures. Organizations are focusing on advanced JTAG-based testing to reduce production errors, accelerate PCB validation cycles, and enhance device reliability across high-performance computing, aerospace electronics, EV systems, and telecom infrastructure. Modern boundary scan controllers and analyzers offer measurable improvements in diagnostics—AI-enabled scan interpretation delivers up to 34% faster fault localization compared to legacy manual inspection systems. Similarly, next-generation vectorless test platforms deliver 28% improvement compared to older boundary scan standards relying on limited interconnect analysis.

Production geographies show clear variation, with Asia-Pacific dominating in volume, while North America leads in adoption with 52% of enterprises integrating advanced boundary scan workflows across design verification, prototype debugging, and system-level testing. By 2027, AI-assisted scan pattern optimization is expected to improve test coverage accuracy by 30%, strengthening product quality assurance in high-density PCB assemblies. ESG-focused compliance is also influencing procurement strategies, with firms committing to test-process energy efficiency improvements such as a 22% reduction in power consumption by 2030 through optimized hardware and automated test scheduling. In 2024, a major U.S. semiconductor manufacturer achieved a 29% reduction in rework time through an AI-driven boundary scan diagnostic initiative.

Collectively, these advancements position the Boundary Scan Hardware Market as a core pillar of resilience, regulatory alignment, and sustainable long-term growth for global electronics production.

Growing PCB complexity is one of the strongest drivers supporting the Boundary Scan Hardware Market, as modern boards feature higher pin counts, denser interconnects, and rising multilayer configurations. With over 62% of newly designed PCBs in 2024 integrating high-speed interfaces such as PCIe Gen5, DDR5, and multi-gigabit SerDes lanes, traditional probing-based methods are becoming less effective. Boundary scan hardware enables precise, non-intrusive validation of these complex interconnects, improving diagnostic coverage by an average of 35%. The adoption of system-level JTAG architectures is also increasing, with 41% of electronics OEMs integrating multi-board test chains for synchronized validation. This shift enhances early fault detection, reduces prototype rework cycles, and strengthens product reliability across mission-critical applications such as aerospace electronics, EV power systems, industrial automation controllers, and advanced computing modules.

A major restraint facing the Boundary Scan Hardware Market is the shortage of skilled professionals capable of developing, deploying, and interpreting advanced JTAG test methodologies. As boundary scan frameworks grow more sophisticated—featuring multi-chain configurations, embedded instrumentation, and AI-supported diagnostics—workforce capability gaps are widening. Studies indicate that nearly 44% of electronics manufacturers report a lack of engineers trained in advanced test automation and vector pattern optimization. This shortage increases onboarding time for new systems, limits effective utilization of test hardware, and slows down production lines dependent on complex debug workflows. Additionally, small and mid-sized manufacturers face constraints in adopting high-end boundary scan tools due to the need for continuous skill development, specialized training modules, and dedicated test engineering teams. These challenges collectively create operational bottlenecks that restrain wider market scalability.

AI-driven automation presents a strong opportunity for the Boundary Scan Hardware Market by enabling more intelligent scan pattern generation, faster fault localization, and adaptive test execution. With AI-enabled diagnostic engines capable of improving failure detection accuracy by up to 38%, electronics manufacturers can significantly reduce test cycle times and rework rates. The integration of machine learning into boundary scan controllers allows predictive identification of interconnect defects and component anomalies, particularly valuable in industries such as EV battery management systems, high-performance computing modules, and telecom equipment. Furthermore, around 47% of OEMs are planning to invest in hybrid test frameworks combining boundary scan, optical inspection, and functional test analytics by 2026. This creates substantial opportunity for hardware vendors to offer integrated, modular, and intelligent test ecosystems aligned with next-generation electronics production demands.

Increasing system miniaturization poses a significant challenge for the Boundary Scan Hardware Market as manufacturers work with shrinking components, advanced packaging formats such as SiP and 3D ICs, and ultra-fine pitch interconnects. These architectures limit physical access to test points, raising the need for more sophisticated JTAG methodologies. However, implementing boundary scan at such scales demands high-precision hardware, advanced controller capabilities, and complex scan-chain management. Over 36% of electronics producers report difficulties in integrating boundary scan into ultra-compact designs due to constraints in routing, pin allocation, and embedded instrumentation compatibility. Moreover, evolving standards for high-speed interfaces require continuous updates in test algorithms and vector libraries. These technological and operational pressures create challenges that hardware manufacturers must overcome to support the next generation of miniaturized electronic systems.

• Expansion of High-Density JTAG Testing Architectures: The market is witnessing accelerated adoption of advanced JTAG architectures optimized for high-density PCBs, with over 48% of newly developed boards in 2024 requiring boundary scan-enabled diagnostics to manage rising pin counts and complex interconnects. Adoption of multi-chain configurations has increased by 31%, enabling faster synchronization across multi-board systems and improving overall test throughput by 28% in mission-critical electronics.

• Integration of AI-Driven Diagnostic Engines: AI-enabled boundary scan diagnostic tools are transforming hardware testing efficiency, with machine learning models improving fault localization accuracy by 35% compared to traditional static test methods. Around 46% of electronics manufacturers are now deploying AI-assisted pattern optimization, resulting in a 29% reduction in debug cycle time and measurable improvement in first-pass test success rates across telecom and automotive electronics.

• Growth in Embedded Instrumentation and System-Level Test Adoption: Embedded test instrumentation within chipsets and modules is expanding, with 41% of semiconductor vendors integrating on-chip diagnostic instruments to enhance real-time interconnect testing. System-level boundary scan deployments have risen by 33%, supporting seamless evaluation of power modules, EV controllers, and 5G infrastructure boards, while improving diagnostic coverage by over 30% in complex assemblies.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Boundary Scan Hardware market. Research indicates that 55% of new projects reported cost benefits from modular and prefabricated practices. Pre-bent and cut components, produced off-site through automated systems, reduce labor by 22% and accelerate timelines by up to 30%. Demand for high-precision machines is increasing, particularly in Europe and North America, where efficiency and precision standards are tightening.

The Boundary Scan Hardware Market segmentation reflects a diverse technological ecosystem shaped by product types, application clusters, and end-user industries. Types include boundary scan controllers, JTAG adapters, embedded instrumentation modules, and system-level scan solutions, each supporting different testing depths and automation capabilities. Applications span PCB assembly testing, semiconductor device verification, telecom equipment diagnostics, automotive ECU validation, and industrial electronics assessment. End-users vary from semiconductor manufacturers and telecom OEMs to aerospace, defense, automotive, and industrial system integrators. Semiconductor and telecom industries show adoption levels above 50% due to stringent reliability and compliance requirements, while automotive and aerospace sectors increasingly rely on system-level JTAG solutions to support safety-critical electronics. As integration density rises and devices become more complex, segmentation patterns continue to evolve around automation, AI-enabled diagnostics, and high-speed interconnect validation needs.

Boundary scan controllers remain the leading type in the Boundary Scan Hardware Market, accounting for around 46% of overall adoption due to their fundamental role in enabling multi-chain execution and ensuring robust diagnostics in high-density PCB environments. JTAG adapters contribute approximately 28%, playing an essential role in device programming, debugging, and early-stage prototype verification. Embedded instrumentation modules represent the fastest-growing category and are projected to expand at a CAGR of 11.2%, fueled by increasing integration of on-chip diagnostic elements and real-time performance monitoring across new semiconductor architectures. Other types—including system-level scan expansion units and hybrid boundary scan-functional test solutions—collectively make up 26% of the remaining market and primarily support complex electronics in aerospace, telecom infrastructure, and EV systems.

PCB assembly and interconnect testing lead the Boundary Scan Hardware Market by application, accounting for nearly 49% of total usage. This dominance is driven by growing PCB complexity, increased pin densities, and rising demand for non-intrusive interconnect validation. Semiconductor device validation follows with 29% adoption, supported by shrinking geometries, multilayer packaging, and accelerated prototype cycles. Telecom network equipment and 5G infrastructure testing represent the fastest-growing application segment, expected to expand at a CAGR of 12.5%, driven by dense subsystem architectures and high-speed SerDes integration. Other applications—including automotive ECUs, defense electronics, and industrial automation systems—collectively contribute 22% of the remaining market.

Semiconductor manufacturers hold the leading position among end-users in the Boundary Scan Hardware Market, accounting for approximately 44% of adoption due to their stringent yield optimization requirements and rising design complexity. Telecom equipment OEMs and data-infrastructure providers represent 27% of usage, driven by continuous network uptime needs and dense hardware integration. Automotive OEMs are the fastest-growing end-user segment, with adoption expected to grow at a CAGR of 13.1%, supported by electrification, ADAS integration, and high-reliability power electronics requiring advanced JTAG-based testing. Other end-users—including aerospace and defense integrators, industrial electronics manufacturers, and medical device OEMs—collectively account for 29% of the market, with adoption levels ranging between 35% and 55% depending on system-critical requirements.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, the Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2025 and 2032.

Asia-Pacific led with more than 41 million PCB assemblies tested using boundary scan tools during 2024, driven by expanding electronics manufacturing in China, India, and South Korea. Europe followed with a 27% share, supported by stringent product validation frameworks and increased adoption in automotive electronics. North America accounted for 24% due to high technological maturity and significant aerospace and defense investments, where more than 31% of test spending involved boundary scan integration. South America and MEA collectively contributed 11%, backed by rising digital infrastructure, telecom expansion, and increasing reliance on automated board-level diagnostics.

How Is Rapid Digital Transformation Influencing Boundary Scan Hardware Adoption?

North America held a 24% market share in 2024, supported by strong deployments across aerospace, defense, telecommunications, and healthcare electronics. The region’s enterprise adoption in healthcare and finance was nearly 33% higher than global averages due to strict traceability, regulatory testing, and mission-critical electronics reliability requirements. Government-backed modernization programs contributed significantly, including over USD 12 billion allocated to next-generation defense electronics testing and validation. Local players such as National Instruments enhanced their automated test platforms with broader boundary scan integration, improving coverage for high-density and multi-layered PCB assemblies. Consumer behavior trends show a high preference for advanced diagnostic capabilities, reflecting strong adoption in data centers, medical imaging, and avionics systems.

Why Are Compliance Mandates Reshaping Boundary Scan Hardware Demand?

Europe accounted for 27% of the global boundary scan hardware market in 2024, supported by strong demand from Germany, the UK, France, and Italy. Automotive electronics and industrial automation accounted for nearly 36% of total regional adoption as OEMs intensified testing due to regulatory safety mandates. Sustainability and eco-compliance regulations also accelerated migration toward non-invasive testing methods. Companies across Europe are rapidly integrating emerging technologies, including advanced fault-isolation systems and test-coverage analytics. A local example includes UK-based test solution providers expanding JTAG-based validation offerings for EV components. Consumer behavior trends reflect heightened demand for transparent and explainable testing frameworks in line with regulatory pressure.

How Is Manufacturing Expansion Strengthening Hardware Test Adoption?

Asia-Pacific held the largest regional share at 38% and ranked first in overall unit consumption. China, Japan, India, and South Korea were the top contributors, collectively accounting for more than 58% of global PCB manufacturing output in 2024. Rapid infrastructure growth and strong electronics production ecosystems fueled demand for high-speed boundary scan hardware across consumer electronics, telecom infrastructure, and semiconductor assembly. Innovation hubs in Shenzhen, Tokyo, and Bangalore continued accelerating test automation deployment. Local companies expanded production capacity for advanced PCB assemblies requiring high-level test coverage. Consumer behavior trends indicate strong adoption driven by e-commerce electronics, mobile AI applications, and high-volume device testing cycles.

How Is Industrial Modernization Influencing Test Hardware Uptake?

South America contributed approximately 6% to the global market in 2024, with Brazil and Argentina leading regional adoption. Growth was driven by telecom expansion, industrial automation upgrades, and increased integration of PCB-based monitoring systems in the energy and utilities sector. Infrastructure digitization and government-backed technology incentives supported broader adoption across manufacturing lines. Local players in Brazil expanded contract electronics manufacturing, increasing board-level testing requirements. Consumer behavior trends emphasize demand for localized diagnostics, particularly in media devices, language-specific electronics, and broadcast systems where boundary scan ensures higher system reliability.

How Are Modernization Programs Accelerating Hardware Testing Demand?

The Middle East & Africa region accounted for nearly 5% of the global boundary scan hardware market in 2024, with the UAE, Saudi Arabia, and South Africa emerging as key adopters. Demand was driven by oil and gas automation, renewable energy installations, and expanding telecommunications networks requiring robust board-level diagnostics. Large-scale digital transformation projects increased the adoption of automated test equipment across industrial and security electronics. Local examples include regional electronics integrators upgrading PCB testing workflows to support advanced monitoring systems. Consumer behavior patterns indicate rising adoption among enterprises seeking long-term reliability and reduced maintenance costs in harsh environmental conditions.

China – 24% share. Dominance is driven by high electronics production capacity and extensive PCB assembly volumes.

United States – 18% share. Strong demand is fueled by advanced aerospace, defense, and semiconductor testing requirements.

The Boundary Scan Hardware market remains moderately consolidated yet highly competitive, with more than 18 active global competitors providing hardware products, software integration, and embedded test solutions. The top 5 companies (including names such as Corelis, XJTAG, JTAG Technologies, Keysight Technologies, and Teradyne) collectively command an estimated 55–60% market share, reflecting a balance between market leadership and niche innovation. While industry titans focus on high-volume automated test platforms, specialist vendors provide leaner, customizable boundary-scan controllers and modular instruments.

Competitive dynamics are shaped by frequent partnerships and product launches: XJTAG recently expanded its European distribution network, while Corelis introduced its latest ScanExpress JTAG controller series optimized for multi-chain testing. Teradyne continues to leverage its ATE (Automated Test Equipment) business by integrating boundary-scan modules into broader system test offerings. Keysight is investing heavily in R&D to weave boundary scan into its flagship measurement platforms, coupling diagnostics with high-speed serial test capabilities. Innovation trends include AI-assisted fault localization, cloud-enabled test orchestration, and hybrid test suites that combine JTAG boundary scan with functional test and in-system programming.

Because of this, new entrants must invest significantly in engineering and partnerships to challenge incumbents, while established players increasingly differentiate through software-hardware co-innovation, end-user education programs, and customized test architectures. The competitive landscape is therefore evolving: it is not purely fragmented, but also not dominated by a single player — decision-makers must evaluate both depth of technical capability and strategic alignment when choosing boundary scan hardware partners.

Corelis, Inc.

XJTAG Ltd.

JTAG Technologies, Inc.

Keysight Technologies, Inc.

Teradyne, Inc.

Goepel Electronic GmbH

ASSET InterTech, Inc.

Acculogic, Inc.

CheckSum, LLC

National Instruments Corporation

The Boundary Scan Hardware market is undergoing rapid technological evolution driven by growing PCB complexity, miniaturization of components, and increased integration of multi-layer architectures. Modern boundary scan controllers now support higher pin-count devices, with advanced systems enabling testing of boards containing more than 2,000 digital I/O nodes. This shift is supported by next-generation JTAG interfaces offering improved signal integrity and enhanced chain management to maintain accurate diagnostics across dense circuit assemblies. Additionally, hybrid testing environments that combine boundary scan with functional test and in-system programming are becoming mainstream, reducing test cycle time by 25–40% in high-volume production environments.

Emerging technologies such as AI-assisted fault localization are transforming how manufacturers identify errors during board validation, improving defect detection accuracy by nearly 30%. Cloud-enabled test orchestration platforms are also gaining traction, enabling remote execution, multi-site coordination, and real-time analytics. These platforms support scalability requirements for facilities handling more than 5,000 boards per day, aligning with the growing demand for connected manufacturing ecosystems. Furthermore, FPGA-based test solutions are being integrated to simulate complex system behaviors, enabling engineers to validate high-speed digital interfaces using boundary-scan-assisted techniques.

Another important trend is the integration of boundary scan hardware with cybersecurity diagnostics, which helps identify unauthorized hardware modifications, particularly in defense, telecom, and critical infrastructure applications. High-speed JTAG protocols and improved TAP (Test Access Port) controllers are also emerging, enabling faster testing cycles and up to 18% reduction in system-level debug time. As PCB architectures continue to evolve, boundary scan technology is expanding beyond traditional digital testing to incorporate mixed-signal capabilities and advanced system-on-chip diagnostics, establishing a future-ready testing environment for complex electronics manufacturing.

In May 2024, XJTAG launched Version 4.0 of its software suite, enabling multi-TAP JTAG chains to run at different clock frequencies concurrently, thereby improving test throughput and reducing scan times.

At Electronica 2024, XJTAG previewed its XJLink-PF40 JTAG controller, supporting up to 8 TAPs over 40 I/O pins with four voltage domains and robust protection up to ±30 V per pin.

In September 2024, XJTAG demonstrated at FPGAworld its boundary-scan capabilities using XJTAG 4.0; the company showed how Optimised Scans accelerate board testing by running different JTAG chains in parallel at separate clock frequencies.

In March 2023, Keysight introduced the x1149 Boundary Scan Analyzer Tester 2.0, adding support for IEEE 1149.1-2013 and IEEE 1149.6-2015 standards, increasing test coverage by approximately 75% and enabling features like electronic chip identification (ECID).

The report on the Boundary Scan Hardware Market covers a comprehensive analysis of product types, application segments, and geographic regions. On the technology front, it examines boundary-scan controllers, JTAG adapters, embedded diagnostic modules, and hybrid test systems, detailing how each is used in the test and validation of PCB assemblies and complex electronic systems. Application-wise, the report addresses core uses such as PCB interconnect testing, semiconductor device verification, telecom infrastructure diagnostics, automotive ECU validation, and industrial electronics inspection.

Geographically, the study spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, evaluating regional consumption, manufacturing capacity, and end-user behavior. The industry focus covers sectors including aerospace, automotive, telecom, consumer electronics, defense, and industrial automation. Additionally, the report explores emerging technological trends such as AI-enhanced fault localization, system-level scan integration, cloud-based test orchestration, and embedded on-chip instrumentation. It also considers regulatory dimensions, design-for-test (DFT) practices, and sustainability pressures in hardware testing.

Finally, the report outlines competitive strategies and innovation roadmaps, profiling both established vendors and niche players by evaluating their R&D investments, product launches, partnerships, and service models. This broad scope offers decision-makers a detailed, business-oriented blueprint for evaluating vendor options, planning technology adoption, and aligning boundary scan investments with future electronics manufacturing trends.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 1857.32 Million |

Market Revenue in 2032 | USD 3120.35 Million |

CAGR (2025 - 2032) | 6.7% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Corelis, Inc., XJTAG Ltd., JTAG Technologies, Inc., Keysight Technologies, Inc., Teradyne, Inc., Goepel Electronic GmbH, ASSET InterTech, Inc., Acculogic, Inc., CheckSum, LLC, National Instruments Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |