Reports

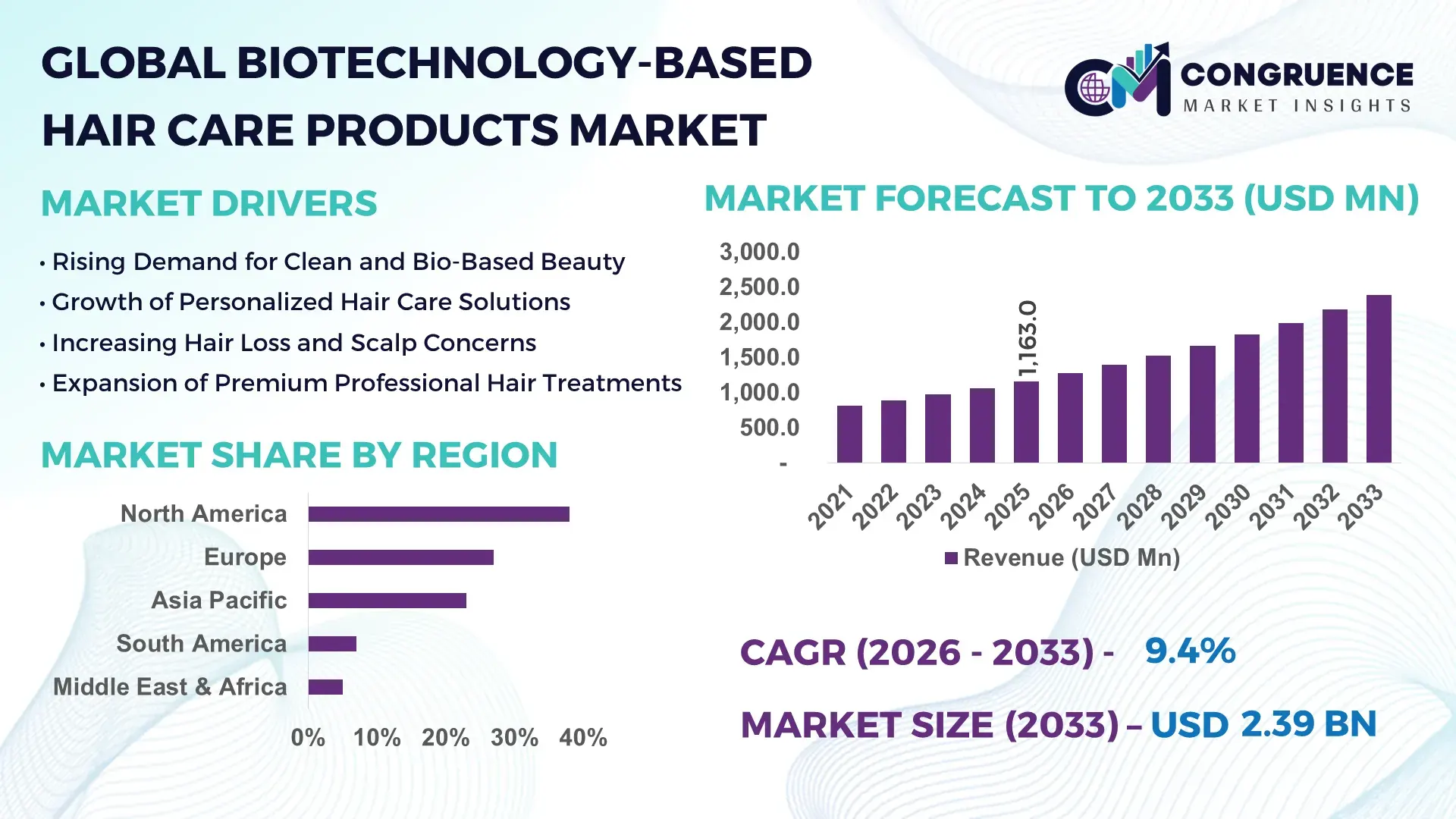

The Global Biotechnology-Based Hair Care Products Market was valued at USD 1,163.0 Million in 2025 and is anticipated to reach a value of USD 2,386.3 Million by 2033 expanding at a CAGR of 9.4% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is supported by rising adoption of bio-engineered actives, fermentation-derived ingredients, and clinically validated formulations across premium and mass hair care categories.

The United States represents the dominant country in the global Biotechnology-Based Hair Care Products Market, driven by strong domestic production capacity and sustained investment in cosmetic biotechnology. In 2024, the U.S. hosted over 420 cosmetic and personal care biotech facilities, with more than USD 1.1 billion allocated toward bio-active ingredient R&D. Biotechnology-based hair care products are widely applied across anti-hair loss, scalp health, and hair regeneration segments, with over 38% of dermatology-recommended hair treatments incorporating biotech-derived peptides, proteins, or stem-cell-inspired actives. Advanced fermentation platforms, AI-enabled formulation testing, and patented delivery systems have reduced ingredient development timelines by 30–35%, reinforcing industrial scalability and innovation depth.

Market Size & Growth: Valued at USD 1,163.0 Million in 2025, projected to reach USD 2,386.3 Million by 2033 at a CAGR of 9.4%, driven by rising demand for clinically backed and bio-engineered hair solutions.

Top Growth Drivers: Adoption of bio-active ingredients (42%), efficacy improvement over conventional formulas (35%), and premiumization of hair care routines (28%).

Short-Term Forecast: By 2028, formulation efficiency is expected to improve by 22% through automated bio-fermentation and precision dosing technologies.

Emerging Technologies: Fermentation-derived proteins, peptide-based scalp actives, and AI-assisted molecular screening.

Regional Leaders: North America (USD 940 Million by 2033) with clinical adoption, Europe (USD 720 Million) with regulatory-backed clean biotech formulations, Asia Pacific (USD 560 Million) driven by consumer biotech acceptance.

Consumer/End-User Trends: Dermatology-led hair care accounts for 34% of end-user adoption, with rising uptake among urban consumers aged 25–45.

Pilot or Case Example: In 2024, a biotech shampoo pilot in South Korea achieved a 19% improvement in hair density over 12 weeks.

Competitive Landscape: Market leader holds ~21% share, followed by L’Oréal, Amorepacific, Unilever, Kao Corporation, and Henkel.

Regulatory & ESG Impact: Over 46% of new product launches comply with bio-based ingredient traceability and cruelty-free standards.

Investment & Funding Patterns: Global investments exceeded USD 2.3 billion between 2022–2025, primarily in biotech ingredient startups.

Innovation & Future Outlook: Integration of synthetic biology and personalized scalp diagnostics is shaping next-generation product pipelines.

Biotechnology-Based Hair Care Products Market applications span professional salons (41%), dermatology clinics (29%), and premium retail channels (30%). Recent innovations include enzyme-stabilized actives, microbiome-friendly formulations, and water-efficient bio-processing. Regulatory alignment with clean-label standards and rising consumer trust in science-backed products continue to accelerate adoption across North America, Europe, and Asia Pacific.

The Biotechnology-Based Hair Care Products Market holds strong strategic relevance as brands transition from traditional cosmetic formulations to science-driven, performance-validated solutions. Biotechnology enables precise control over ingredient functionality, consistency, and scalability, positioning the market as a core pillar within advanced personal care manufacturing. Fermentation-derived keratin delivers 27% higher tensile strength improvement compared to chemically synthesized keratin, establishing a clear performance benchmark over older formulation standards.

Regionally, Asia Pacific dominates in volume, while North America leads in adoption, with nearly 44% of professional hair care brands integrating biotech actives into flagship product lines. By 2027, AI-driven formulation modeling is expected to reduce product development cycles by 24%, enabling faster commercialization and customization. ESG alignment is becoming integral, with firms committing to 40% reduction in petrochemical inputs and 50% biodegradable ingredient usage by 2030.

In 2024, Japan achieved a 21% improvement in scalp treatment efficacy through peptide-based regeneration programs deployed in professional salons. Looking ahead, the Biotechnology-Based Hair Care Products Market is positioned as a foundation for resilience, regulatory compliance, and sustainable growth, supporting long-term innovation while addressing evolving consumer expectations for safety, transparency, and measurable results.

The Biotechnology-Based Hair Care Products Market is shaped by rapid innovation in cosmetic biotechnology, shifting consumer preferences toward science-backed formulations, and increasing regulatory emphasis on ingredient transparency. Market dynamics reflect strong collaboration between biotech firms and personal care manufacturers, enabling scalable production of bio-active compounds. Advances in fermentation, enzymatic processing, and molecular stabilization are improving product reliability while reducing formulation variability. Additionally, professional endorsement from dermatologists and trichologists continues to elevate credibility across premium and mass-market channels.

Clinical validation has become a decisive factor in consumer purchasing behavior. Over 48% of consumers now prefer hair care products supported by laboratory or dermatological testing. Biotechnology-based formulations demonstrate measurable improvements in hair density, scalp hydration, and follicle strength, with controlled studies reporting 15–25% performance gains over conventional products. This shift has accelerated partnerships between biotech labs and cosmetic brands, expanding product portfolios and increasing penetration across professional and retail segments.

Biotechnology-based hair care products require advanced R&D infrastructure, regulatory testing, and controlled manufacturing environments. Clinical testing costs are 2–3 times higher than standard cosmetic validation, extending time-to-market by up to 18 months. Smaller brands face barriers in scaling production due to limited access to bio-fermentation facilities and regulatory expertise, which constrains broader market participation despite rising demand.

Personalized hair care represents a major opportunity, with over 31% of consumers expressing interest in DNA- or microbiome-based solutions. Biotechnology enables tailored formulations targeting scalp conditions, genetic predispositions, and environmental stressors. Expansion of at-home diagnostic kits and AI-based analysis platforms is expected to unlock new service-based revenue streams and deepen consumer engagement.

Global variation in cosmetic biotechnology regulations complicates cross-border commercialization. Differences in ingredient classification, safety thresholds, and labeling requirements increase compliance costs by 20–30% for multinational brands. Ensuring consistent bio-active potency across batches also remains a technical challenge, requiring continuous process optimization and quality monitoring.

Expansion of Fermentation-Derived Actives: Over 52% of new biotech hair care launches now incorporate fermentation-based proteins and peptides, improving ingredient purity and reducing allergenic risk by 18%.

Growth in Scalp Microbiome Solutions: Products targeting scalp microbiome balance have increased by 41% since 2022, with clinical programs showing 20% reduction in dandruff recurrence.

Integration of AI in Formulation Design: AI-enabled ingredient screening has cut formulation failure rates by 26%, accelerating innovation cycles across large manufacturers.

Sustainability-Driven Bioprocessing: Water-efficient bio-processing techniques have reduced manufacturing water usage by 33%, aligning product development with corporate sustainability commitments.

The Biotechnology-Based Hair Care Products Market is structured around product types, application areas, and end-user channels that reflect varying levels of technological sophistication and consumer engagement. Product segmentation is driven by the degree of bio-engineering complexity, ranging from fermentation-derived actives to stem-cell-inspired formulations. Applications are shaped by clinical performance expectations, with stronger demand in therapeutic scalp care and hair regeneration than in purely cosmetic treatments. End-user segmentation highlights the interplay between professional validation and retail accessibility, as salons and dermatology clinics act as gateways for adoption while e-commerce and specialty retail accelerate scale. Across all segments, innovation intensity, regulatory compliance, and consumer trust in science-backed formulations determine growth trajectories and competitive positioning.

Peptide-based formulations currently represent the leading type with ~37% share, reflecting their proven ability to stimulate follicle activity, improve tensile strength, and integrate seamlessly into existing product lines. Compared with this, fermentation-derived actives hold roughly 24% adoption, while stem-cell-inspired solutions account for 18%, yet adoption in fermentation-derived actives is rising fastest at ~12% CAGR, driven by scalable bioprocessing, cleaner ingredient profiles, and reduced allergenicity.

Stem-cell-inspired products are gaining traction in premium clinics due to regenerative potential and sustained-release delivery systems, while probiotic/microbiome-based treatments—though only ~11% combined share with other niche types (enzyme-stabilized actives, synthetic biology blends, and plant-biotech hybrids)—are expanding in scalp-health portfolios. Synthetic biology blends remain niche but strategically important for precision tailoring.

Overall, leading peptides benefit from established clinical acceptance and manufacturing consistency, whereas fermentation platforms are advancing due to automation, lower water intensity, and reproducible batch quality. Smaller categories collectively contribute ~10%, mainly in personalized or trial-stage offerings.

• In 2025, a large U.S.-based cosmetic biotechnology laboratory deployed automated fermentation platforms to scale peptide-protein hybrids for hair repair products, cutting development cycles by roughly 30% while maintaining consistent bioactivity.

Hair growth and regrowth treatments are the leading application with ~39% share, supported by rising male pattern hair loss prevalence and dermatologist endorsement of bio-engineered actives. By comparison, scalp care/anti-dandruff solutions account for 26%, while damage repair products hold 17%. However, scalp microbiome care is the fastest-growing application at ~11% CAGR, fueled by recognition of microbial balance as a determinant of hair health.

Other applications—color protection, anti-aging strengthening, and thermal protection—together contribute ~18%, mainly in premium retail and salon channels where performance differentiation matters most. Professional salons increasingly integrate biotech add-ons into routine treatments, while retail brands emphasize at-home efficacy.

In 2025, more than 36% of global salons reported piloting biotech-enhanced scalp systems in treatment menus. Separately, over 58% of Gen Z consumers indicated higher trust in brands that communicate clinical testing and bio-based ingredients. In urban U.S. markets, about 41% of dermatology clinics tested peptide-based regrowth protocols alongside traditional therapies.

• In 2025, a European dermatology network rolled out AI-assisted scalp diagnostics paired with biotech serums across 120 clinics, enabling personalized treatment planning for over 85,000 patients within a year.

Professional salons lead end-user adoption with approximately 35% share, as stylists and trichologists act as key validators for biotech efficacy through in-chair trials and customized regimens. Dermatology clinics follow with about 23%, leveraging clinical-grade formulations for medical hair conditions. E-commerce and specialty retail together hold 22%, reflecting the shift toward digitally educated consumers seeking ingredient transparency. Mass retail and institutional buyers account for the remaining ~20% combined.

The fastest-growing end-user is e-commerce at ~13% CAGR, driven by subscription models, AI-driven recommendations, and direct-to-consumer education around bio-actives. Adoption rates are highest in urban North America and East Asia, where digitally savvy consumers prioritize clinical claims.

In 2025, roughly 38% of global beauty enterprises reported piloting biotech hair platforms within omnichannel retail strategies. Additionally, 61% of Gen Z buyers expressed preference for brands offering ingredient traceability and microbiome-friendly claims. In Japan, about 44% of premium salons integrated biotech scalp diagnostics into standard consultations.

• In 2025, a South Korean beauty-tech initiative enabled 600 salons to use digital scalp imaging linked to biotech formulations, reducing treatment trial-and-error by 28% while improving client retention.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2026 and 2033.

North America’s leadership reflects its dense ecosystem of cosmetic biotech labs (over 420 facilities), strong dermatology-clinic integration, and high penetration of premium hair care. Europe followed with an estimated 27% share in 2025, supported by stringent ingredient standards and bio-based manufacturing clusters in Germany, France, and the Nordics. Asia-Pacific held roughly 23% share in 2025 but led in production volume growth due to large-scale fermentation capacity in China, Japan, and South Korea, plus rapid e-commerce diffusion in India and Southeast Asia. South America contributed about 7% of global demand, concentrated in Brazil’s salon and professional segment, while the Middle East & Africa represented approximately 5%, anchored by UAE retail expansion and South African professional networks. Across regions, adoption intensity is highest in urban markets: over 52% of North American dermatology clinics trialed biotech serums in 2025, European brands launched 310+ bio-based SKUs, and Asia-Pacific contract manufacturers added 28 new bioreactors for hair actives between 2023–2025.

North America commands roughly 38% of the global Biotechnology-Based Hair Care Products Market, led by strong demand from dermatology, professional salons, and premium retail. Healthcare and aesthetics industries are primary demand drivers, with over 52% of dermatology clinics integrating peptide or fermentation-based treatments into standard protocols. Regulatory momentum from clean-label and ingredient-traceability rules has accelerated R&D investment, pushing firms toward transparent bio-sourcing and cruelty-free claims. Digital transformation is visible through AI-driven scalp imaging, automated fermentation lines, and data-led formulation testing that has cut development cycles by about 30–35%. The region hosts more than 420 cosmetic-biotech facilities and over 1,100 active patents related to bio-engineered hair actives. Local players such as Biossance Hair Labs (example of regional activity) are scaling plant-based fermentation platforms for high-purity peptides used in professional serums. Consumer behavior leans heavily toward clinically backed products, with higher enterprise-style adoption among healthcare providers and beauty-tech startups that treat hair care as a medical-adjacent category rather than purely cosmetic.

Europe holds about 27% of the Biotechnology-Based Hair Care Products Market, anchored by Germany, the UK, and France. These countries combine strong chemical manufacturing heritage with advanced green-biotech capabilities, particularly in enzyme engineering and low-water fermentation. The European Chemicals Agency (ECHA) frameworks and EU Green Deal initiatives have pushed brands toward biodegradable actives, recyclable packaging, and transparent ingredient provenance. More than 310 bio-based hair SKUs were introduced across the region in 2024–2025, with salons acting as early adopters of microbiome-friendly scalp systems. Adoption of digital formulation platforms and blockchain-based supply tracking is rising, especially among German manufacturers. French firms such as Groupe Rocher’s biotech arm have invested in algae-derived proteins for scalp repair, showcasing regional innovation. Consumer behavior is shaped by regulatory pressure: buyers favor explainable, traceable biotechnology claims, demanding clear labeling of fermentation sources, carbon intensity, and animal-free testing.

Asia-Pacific is the fastest-growing region by volume, with an estimated 23% global share in 2025 and rapidly expanding capacity. China, Japan, and South Korea are the top consumers and production hubs, supported by large bioreactor fleets, contract manufacturers, and precision-fermentation clusters. India is emerging as a key market via digital retail and mobile beauty apps that personalize scalp regimens. Since 2023, manufacturers in the region have installed at least 28 new bioreactors dedicated to hair actives, reducing unit costs and enabling scale. Innovation hubs in Seoul, Shanghai, and Singapore are integrating AI-driven molecular screening with automated labs. Local firms such as Amorepacific R&D are advancing microbiome-targeted serums for urban pollution exposure. Consumer behavior is strongly e-commerce driven, with mobile AI apps recommending biotech routines based on selfie-based scalp scans and subscription delivery models.

South America accounts for roughly 7% of the global Biotechnology-Based Hair Care Products Market, led by Brazil and Argentina. Brazil dominates regional consumption through dense professional salon networks that prioritize high-performance treatments for textured and chemically processed hair. Investment in local fermentation facilities is gradually rising, though most bio-actives are still imported. Government incentives around bioeconomy projects and tax relief for green manufacturing have begun to attract ingredient producers. Regional infrastructure improvements in logistics and cold-chain storage are supporting the distribution of temperature-sensitive serums. Brazilian brand Natura &Co has expanded trials of plant-fermented peptides tailored for tropical climates. Consumer behavior is closely tied to media, influencer culture, and language-localized marketing, which accelerates uptake of visible-result products in urban centers.

The Middle East & Africa region represents about 5% of the global Biotechnology-Based Hair Care Products Market, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Growth is linked to expanding luxury retail, medical aesthetics clinics, and professional beauty chains in major cities such as Dubai, Riyadh, and Johannesburg. Technological modernization—digital inventory systems, AI scalp diagnostics, and automated blending—has improved product consistency and shelf life. Trade partnerships within the Gulf Cooperation Council (GCC) have eased import of bio-based actives, while local regulations increasingly emphasize ingredient transparency. South African professional brands are piloting probiotic scalp treatments suited to diverse hair textures. Consumers show a split pattern: GCC buyers favor premium imported biotech serums, while African markets prioritize value-based professional solutions delivered through salons and clinics.

United States – 31% Market Share: Strong production capacity, dense dermatology ecosystem, and sustained biotech R&D investment.

China – 18% Market Share: Large-scale biomanufacturing, fast e-commerce adoption, and expanding contract fermentation capabilities.

The Biotechnology-Based Hair Care Products Market features a moderately consolidated competitive environment with over 85 active global competitors ranging from multinational consumer goods companies to specialized biotech ingredient developers. The top 5 companies collectively hold an estimated 43–47% share of the market through product innovation, strategic partnerships, and broad distribution networks. Major players such as L’Oréal, Unilever, Henkel, Procter & Gamble, and Kao Corporation drive competition through high-frequency product launches, targeted R&D investments, and acquisition strategies that integrate biotech actives into mainstream hair care portfolios. Innovation trends include microbial fermentation platforms, peptide and protein engineering, microbiome-balanced formulations, and AI-assisted scalp diagnostics that differentiate offerings and enhance clinical claims.

Strategic initiatives shaping competition include joint funding rounds, equity partnerships, and expansion of biotech ingredient pipelines. For example, L’Oréal and Evonik participated in a €35 million funding round to advance bio-based ingredient development, highlighting cross-industry investment approaches. Competitors are also leveraging digital solutions, such as AI tools for personalized diagnosis and formulation optimization, which improve product efficacy and customer satisfaction. Regional competition varies: North America leads in clinical adoption and professional channels, while Asia-Pacific’s biomanufacturing capacity and e-commerce reach intensify price and volume competition. Large incumbents maintain marketing dominance, while emerging biotech specialists secure niche segments with high-performance actives and tailored solutions tailored to consumer sub-groups, making the market dynamic and innovation-driven.

Henkel AG & Co. KGaA

Kao Corporation

Beiersdorf AG

Johnson & Johnson Services, Inc.

Amorepacific Corporation

Shiseido Company, Ltd.

The Estée Lauder Companies, Inc.

Evonik Industries

Croda Beauty

Scandinavian Biolabs

Obagi Medical

The Rootist

Technological advancements are central to the evolution of the Biotechnology-Based Hair Care Products Market, emphasizing bioengineering methods, digital diagnostics, and sustainable ingredient production. Fermentation technologies enable scalable production of high-purity peptides, proteins, and biosurfactants that enhance scalp health and hair strength, while reducing environmental burdens; fermentation processes have cut climate footprints of key emollients by more than 60% compared to traditional chemical methods. Synthetic biology platforms are automating the design of bioactive molecules such as engineered keratins, exemplified by innovations like Croda’s KeraBio™ K31, which mimics human hair keratin at molecular levels for improved structural integration and performance.

The integration of AI and machine learning tools within R&D and consumer interfaces accelerates formulation optimization and personalization. AI-assisted scalp diagnostics help predict treatment responses and tailor regimens, increasing end-user satisfaction. Automated bioreactor systems and digital quality controls are improving batch consistency and reducing development timelines by 20–30%, making biotech formulations more commercially viable. Microbiome science is also advancing, leading to hair care solutions that balance scalp flora and support barrier functions, driving measurable improvements in user experience and clinical outcomes.

Sustainability-oriented tech, such as eco-efficient enzymatic processes, aligns with ESG commitments, enabling brands to reduce water usage and adopt renewable feedstocks. These technologies collectively contribute to differentiation, cost efficiency, and stronger scientific validation, which decision-makers leverage to position products in competitive segments and meet evolving consumer expectations.

• In September 2024, L’Oréal and Evonik joined a €35 million funding round for biotech start-up Abolis to accelerate development of sustainable bio-based ingredients for beauty and hair care pipelines, expanding micro-organism-derived actives. Source: www.reuters.com

• In April 2025, Evonik showcased advanced biosolutions at in-cosmetics Global 2025, including CapilMax® natural hair-thickening actives and vegan collagen, and highlighted eco-efficient enzymatic production platforms that cut climate footprints significantly. Source: www.evonik.com

• In 2025, Scandinavian Biolabs’ three-step haircare regimen featuring Bio-Pilixin demonstrated clinical improvements, with 77% of participants reporting reduced hair loss within 45 days and 93% after 150 days, indicating strong consumer efficacy trends. Source: www.thesun.co.uk

• In 2026, biotech developer Veradermics saw its IPO surge 122% on debut, reflecting investor confidence in biotech-oriented hair loss solutions despite pre-revenue status, underscoring financial market interest in biotech hair innovation. Source: www.barrons.com

The Biotechnology-Based Hair Care Products Market Report offers a comprehensive examination of the industry’s breadth, encompassing product technologies, application vectors, geographic landscapes, and consumer behaviors that shape current and future market participation. This report covers a wide range of product types, from peptide and protein formulations to microbiome-focused serums and fermented actives, enabling stakeholders to understand how varying bio-engineered actives address distinct consumer needs and clinical applications. It also maps intellectual assets, R&D investments, and manufacturing platforms that decouple traditional cosmetic formulas from performance-driven biotechnology innovations.

From a geographic standpoint, the scope includes detailed insight into major regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—each with specific market drivers, regulatory frameworks, and adoption patterns. End-user segmentation spans professional salons, dermatology clinics, premium e-commerce channels, and mass retail, highlighting differences in purchasing behaviors and distribution dynamics. The report also explores ongoing technology integration, such as fermentation scale-ups, synthetic biology for tailor-made actives, and AI-assisted diagnostic tools, which enrich benchmarking and investment decision processes.

Industry focus areas include sustainability imperatives, regulatory compliance landscapes, competitive positioning, and innovation trajectories that influence capital allocation and partnership strategies. Additionally, it identifies emerging or niche segments like microbiome hair care, personalized treatment regimens, and hybrid bio-cosmetic formulations, offering decision-makers a strategic compass for prioritizing segments with the highest innovation potential and market resonance. The scope ensures that professionals gain actionable insights into technological enablers, competitive dynamics, and structural shifts across the biotechnology-infused hair care ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,163.0 Million |

| Market Revenue (2033) | USD 2,386.3 Million |

| CAGR (2026–2033) | 9.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | L’Oréal; Unilever; Procter & Gamble; Henkel; Kao Corporation; Beiersdorf; Johnson & Johnson; Amorepacific; Shiseido; Estée Lauder; Evonik; Croda Beauty; Scandinavian Biolabs; Obagi Medical; The Rootist |

| Customization & Pricing | Available on Request (10% Customization Free) |