Reports

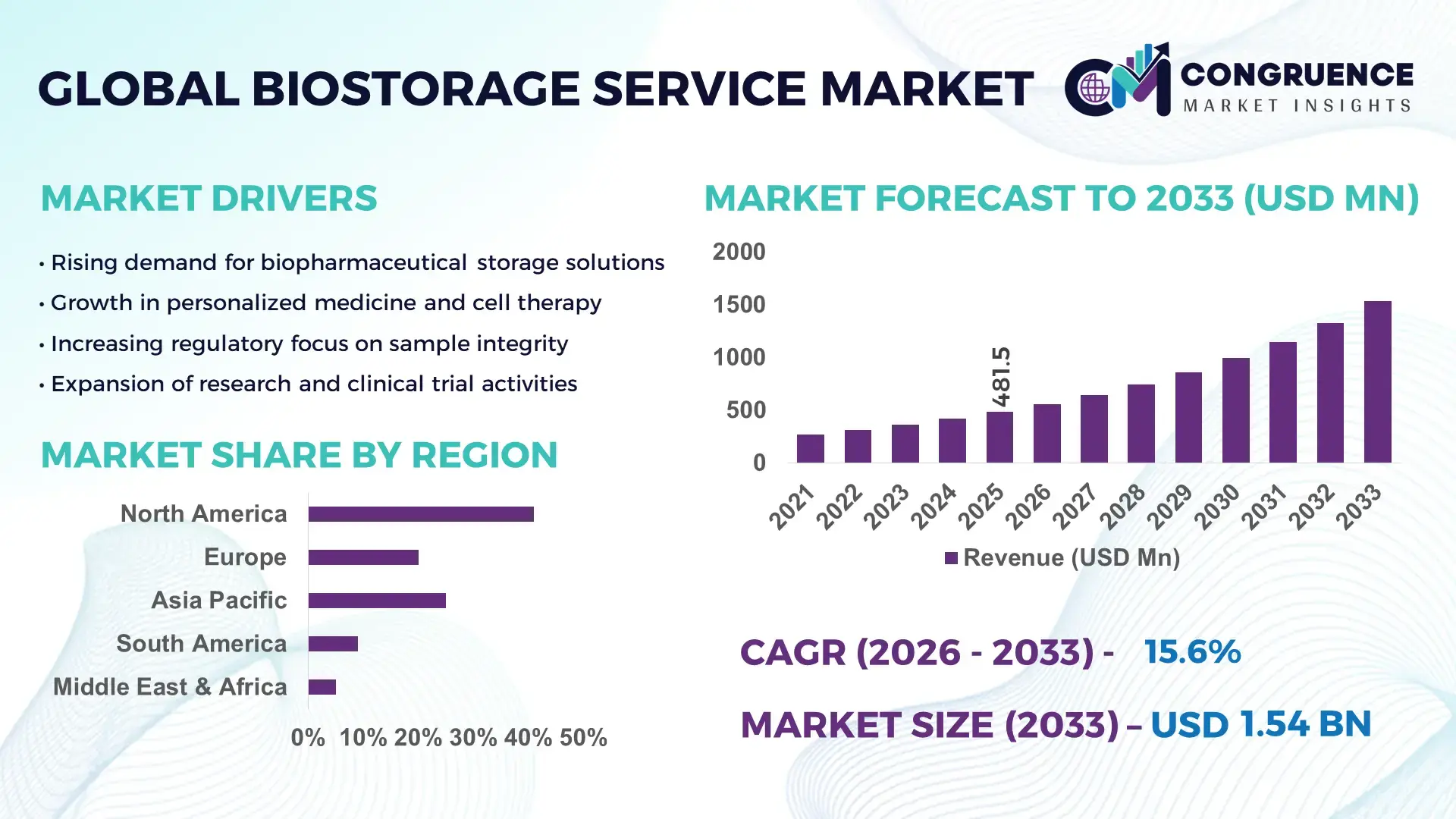

The Global Biostorage Service Market was valued at USD 481.48 Million in 2025 and is anticipated to reach a value of USD 1535.47 Million by 2033 expanding at a CAGR of 15.6% between 2026 and 2033. This growth is primarily driven by the accelerating demand for secure long-term storage of biological samples in pharmaceutical research, regenerative medicine, and precision diagnostics.

The United States remains the dominant country in the biostorage service market, supported by extensive biopharmaceutical manufacturing capacity and advanced cold-chain infrastructure. The country hosts over 6,000 clinical trials annually requiring controlled-temperature biorepositories. More than 45% of global cell and gene therapy trials are conducted in the U.S., increasing demand for ultra-low temperature storage at -80°C and vapor-phase liquid nitrogen facilities. Investments exceeding USD 2 billion in biomanufacturing expansion between 2023 and 2025 have strengthened cryogenic storage capacity. Additionally, leading academic research centers and contract research organizations collectively manage millions of biospecimens, integrating automated inventory systems, IoT-enabled temperature monitoring, and validated regulatory compliance frameworks to ensure sample integrity and traceability.

Market Size & Growth: Valued at USD 481.48 Million in 2025 and projected to reach USD 1535.47 Million by 2033 at a CAGR of 15.6%, fueled by rising biologics production and advanced therapy pipelines.

Top Growth Drivers: Biologics pipeline expansion (38%), clinical trial growth (42%), adoption of cell and gene therapies (35%).

Short-Term Forecast: By 2028, automated cryogenic storage systems are expected to reduce sample handling errors by 30% and operational costs by 18%.

Emerging Technologies: AI-based inventory tracking, IoT-enabled temperature surveillance, robotic cryostorage systems, blockchain-backed chain-of-custody tracking.

Regional Leaders: North America projected to reach USD 620 Million by 2033 with strong biopharma outsourcing trends; Europe expected at USD 410 Million driven by regenerative medicine initiatives; Asia-Pacific estimated at USD 355 Million supported by expanding biotech hubs.

Consumer/End-User Trends: Biopharmaceutical companies account for over 48% of demand, followed by research institutes and CROs, with increasing outsourcing of long-term biospecimen management.

Pilot or Case Example: In 2024, a large-scale automated cryogenic facility deployment improved retrieval efficiency by 27% and reduced temperature excursion incidents by 22%.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including major global biorepository service providers and integrated cold-chain specialists.

Regulatory & ESG Impact: Stringent GMP, GxP, and ISO 20387 standards, alongside carbon-neutral cold storage initiatives, are influencing infrastructure upgrades.

Investment & Funding Patterns: Over USD 1.1 Billion invested globally between 2023 and 2025 in cryogenic infrastructure expansion and digital biostorage platforms.

Innovation & Future Outlook: Expansion of modular cryostorage units, integration of predictive maintenance analytics, and decentralized biobanking models are reshaping long-term biostorage service delivery.

The biostorage service market serves pharmaceutical manufacturers, biotechnology innovators, academic research laboratories, hospitals, and contract development organizations. Biopharmaceutical companies contribute nearly half of total demand due to biologics, monoclonal antibody, and vaccine development programs. Advanced cryopreservation technologies, validated cold-chain logistics, and digitally integrated monitoring systems are redefining operational standards. Regulatory frameworks emphasizing sample traceability, data integrity, and environmental compliance are accelerating facility modernization. Europe and Asia-Pacific are witnessing increasing biospecimen outsourcing, while emerging markets are investing in GMP-compliant repositories. The future outlook highlights decentralized storage networks, energy-efficient ultra-low freezers, and precision inventory management systems that enhance reliability, scalability, and long-term biological asset protection.

The Biostorage Service Market holds strategic relevance within the global life sciences ecosystem by ensuring the integrity, traceability, and long-term preservation of high-value biological materials. As cell and gene therapies, monoclonal antibodies, and mRNA-based products expand across more than 3,000 active development programs worldwide, the requirement for validated ultra-low temperature and cryogenic storage infrastructure has intensified. Advanced robotic cryogenic storage delivers 35% faster sample retrieval and 28% lower manual handling risk compared to conventional manual freezer systems. North America dominates in storage volume due to large-scale clinical research activity, while Europe leads in digital adoption with over 60% of biobanks implementing automated inventory and compliance platforms.

By 2028, AI-driven predictive temperature monitoring is expected to reduce temperature excursion incidents by 32% and improve inventory accuracy by 25%. Firms are committing to ESG improvements such as a 20% reduction in energy consumption by 2030 through energy-efficient ultra-low freezers and liquid nitrogen optimization systems. In 2024, a leading U.S.-based biorepository achieved a 30% reduction in retrieval turnaround time through deployment of automated cryogenic robotics and real-time tracking dashboards. The Biostorage Service Market is therefore evolving beyond conventional storage into a digitally integrated, compliance-driven infrastructure layer that underpins resilience, regulatory assurance, and sustainable growth across global biopharmaceutical value chains.

The surge in advanced therapy medicinal products is a primary growth catalyst for the Biostorage Service Market. Over 2,000 cell and gene therapy trials are currently active worldwide, each requiring strict cryogenic storage and validated chain-of-custody protocols. Autologous therapies often require storage at temperatures below -150°C, necessitating specialized vapor-phase liquid nitrogen systems. Biopharmaceutical companies report up to 45% growth in biologics-related storage volumes over the past three years. Furthermore, the global shift toward personalized medicine increases the need for decentralized storage nodes close to treatment centers, boosting demand for scalable, compliant biostorage infrastructure. These requirements are prompting service providers to expand automated facilities, enhance monitoring redundancy, and strengthen digital traceability capabilities.

Energy-intensive cryogenic storage systems represent a significant operational burden. Ultra-low temperature freezers consume up to 20 kWh per day per unit, and large-scale facilities operate hundreds of such systems simultaneously. Rising electricity prices and liquid nitrogen supply fluctuations have increased operational expenses by approximately 15–20% in certain regions. Additionally, regulatory compliance costs associated with validated monitoring systems, calibration audits, and facility certifications add further financial pressure. Smaller biotechnology firms may hesitate to outsource long-term storage due to contract commitments and premium service pricing. These cost structures can limit expansion in emerging economies where infrastructure and energy reliability remain inconsistent.

Decentralized and hybrid clinical trial models are generating new demand for distributed cryogenic storage networks. More than 35% of global trials now incorporate remote patient sampling, requiring localized storage before centralized processing. This trend creates opportunities for modular biostorage units and regional micro-repositories equipped with automated inventory systems. Emerging biotech hubs in Asia-Pacific and Latin America are expanding biomanufacturing facilities, increasing the need for GMP-compliant biostorage services. Integration of blockchain-based chain-of-custody tracking and AI-enabled compliance analytics further enhances service differentiation. Providers investing in scalable, digitally connected storage ecosystems can capture long-term contracts from research institutions and pharmaceutical sponsors seeking secure, transparent sample management solutions.

The Biostorage Service Market operates under rigorous regulatory frameworks that demand continuous validation, documentation, and audit readiness. Facilities must maintain 24/7 temperature monitoring, backup power redundancy, and disaster recovery protocols. Any temperature excursion can compromise high-value biological assets, leading to substantial financial and reputational risks. Compliance with international standards requires periodic system validation, staff training, and data integrity assessments, increasing administrative complexity. Furthermore, cross-border biospecimen transfer involves strict customs, biohazard classification, and data protection regulations. Managing these multilayered requirements while maintaining operational efficiency remains a persistent challenge for service providers striving to balance reliability, scalability, and cost-effectiveness.

• Rapid Adoption of Automated Cryogenic Storage Systems: Automation is transforming operational efficiency across the Biostorage Service market. More than 62% of newly commissioned biorepositories in 2024 integrated robotic sample handling systems, reducing manual intervention by 40%. Automated cryogenic platforms have demonstrated a 30% improvement in retrieval turnaround time and a 25% reduction in temperature excursion incidents. Large-scale facilities managing over 5 million biospecimens are increasingly deploying AI-enabled robotics to enhance inventory accuracy, which has improved traceability compliance scores by nearly 22% compared to conventional manual systems.

• Expansion of Decentralized and Regional Biostorage Networks: The shift toward decentralized clinical trials has accelerated the deployment of regional storage hubs. Approximately 37% of global clinical studies now incorporate remote or hybrid sampling models, driving a 28% increase in localized storage capacity. Asia-Pacific has recorded a 33% rise in newly established GMP-compliant micro-repositories between 2023 and 2025. Distributed storage nodes reduce transport times by up to 35%, lowering sample degradation risks and enhancing supply chain resilience across multi-country research programs.

• Integration of AI-Based Predictive Monitoring and IoT Sensors: Smart monitoring systems are becoming standard in advanced biostorage facilities. Over 70% of large-scale service providers have implemented IoT-enabled temperature tracking with real-time alerts. AI-driven predictive maintenance has reduced freezer failure incidents by 26% and improved preventive maintenance scheduling accuracy by 31%. These digital upgrades support continuous compliance with regulatory standards while minimizing operational downtime in high-density storage environments.

• Strong Focus on Energy Efficiency and Sustainable Cryogenic Infrastructure: Sustainability is emerging as a measurable priority in the Biostorage Service market. Facilities adopting next-generation ultra-low temperature freezers report 18% lower energy consumption compared to legacy units. Approximately 45% of newly built storage centers in North America and Europe now incorporate energy recovery systems and low-global-warming-potential refrigerants. Liquid nitrogen optimization programs have reduced consumption levels by 15%, while carbon reduction commitments target 20% lower facility emissions by 2030, aligning biostorage operations with broader ESG performance benchmarks.

The Biostorage Service market is segmented by type, application, and end-user, reflecting the increasing complexity of biological sample management across global life sciences ecosystems. By type, the market spans ultra-low temperature storage, vapor-phase liquid nitrogen storage, and ambient controlled storage solutions. Application segmentation highlights pharmaceutical and biotechnology research as the dominant demand center, followed by clinical diagnostics, regenerative medicine, and academic research. End-user insights indicate strong reliance on outsourced storage by biopharmaceutical companies, contract research organizations, and hospitals managing long-term biospecimen inventories. More than 48% of pharmaceutical manufacturers now outsource specialized cryogenic storage to ensure compliance and reduce in-house infrastructure costs. Increasing automation, regulatory oversight, and digital inventory integration are reshaping adoption patterns across all segments, with measurable gains in operational efficiency and traceability compliance.

The Biostorage Service market by type is primarily categorized into ultra-low temperature (ULT) storage (-80°C), vapor-phase liquid nitrogen (below -150°C) cryogenic storage, and controlled ambient storage solutions. Ultra-low temperature storage currently accounts for approximately 46% of total service adoption due to its extensive use in vaccine development, monoclonal antibody programs, and routine biologics research. Vapor-phase liquid nitrogen systems hold nearly 38% share, driven by advanced cell and gene therapy requirements where temperatures below -150°C are mandatory to preserve cell viability. However, cryogenic vapor-phase systems are the fastest-growing segment, expanding at an estimated 17.8% CAGR, supported by a 40% increase in global advanced therapy trials over the past three years. Controlled ambient and refrigerated storage solutions collectively contribute around 16% of total demand, serving clinical diagnostics and short-term specimen preservation needs.

By application, pharmaceutical and biotechnology research represents the leading segment, accounting for approximately 52% of total biostorage service utilization. This dominance is linked to expanding biologics pipelines, with more than 8,000 biologic products currently under development globally. Clinical trial sample storage and long-term stability testing drive consistent demand for validated storage environments. Regenerative medicine and cell therapy applications represent nearly 24% of usage, while clinical diagnostics contribute around 15%. Academic and government research institutions collectively account for the remaining 9%. Regenerative medicine applications are the fastest-growing segment, projected to expand at 18.5% CAGR due to increased approvals of autologous and allogeneic therapies requiring ultra-low and cryogenic preservation.

Biopharmaceutical companies represent the largest end-user segment, accounting for nearly 48% of total demand in the Biostorage Service market. These organizations increasingly outsource storage operations to specialized providers to ensure compliance with GMP and GxP standards while reducing capital expenditure on in-house infrastructure. Contract research organizations (CROs) hold approximately 27% share, supported by the growing trend of outsourced clinical trial management. Hospitals and diagnostic laboratories contribute around 15%, particularly for long-term patient sample preservation and transplant-related storage. Academic and government research institutions collectively account for the remaining 10%. CROs are the fastest-growing end-user segment, expanding at an estimated 16.9% CAGR, fueled by a 35% increase in outsourced clinical trial activities over the past five years.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.2% between 2026 and 2033.

North America’s leadership is supported by more than 6,000 active clinical trials annually and over 45% of global cell and gene therapy programs requiring validated cryogenic storage. Europe held approximately 28% share in 2025, driven by over 500 accredited biobanks and strong regulatory compliance frameworks. Asia-Pacific accounted for nearly 22% of global demand, supported by a 33% increase in biomanufacturing facilities between 2022 and 2025. South America contributed about 5%, led by Brazil and Argentina’s expanding vaccine research initiatives. The Middle East & Africa represented close to 4%, with increasing public health investments and genomic research programs. Regional demand patterns are closely linked to biologics production volumes, decentralized clinical trials, and digital cold-chain infrastructure modernization across advanced and emerging economies.

How Is Advanced Biopharmaceutical Expansion Strengthening Regional Cryogenic Infrastructure?

North America accounts for approximately 41% of the global Biostorage Service market volume, supported by extensive biopharmaceutical research and contract manufacturing activities. The region hosts more than 50% of global biologics development programs, with over 2,500 ongoing advanced therapy trials requiring validated vapor-phase liquid nitrogen storage. Regulatory frameworks such as GMP, GxP, and updated data integrity guidelines have increased compliance-driven outsourcing by 38% among mid-sized biotech firms. Digital transformation is prominent, with nearly 70% of large storage providers deploying IoT-enabled temperature monitoring and AI-based predictive maintenance systems. A leading U.S.-based biorepository operator expanded automated cryogenic capacity by 25% in 2024 to support cell therapy sponsors. Regional consumer behavior shows higher enterprise adoption within healthcare and life sciences, where organizations prioritize validated, audit-ready, and energy-efficient long-term biospecimen management solutions.

How Are Regulatory Standards and Sustainability Goals Accelerating Secure Sample Preservation?

Europe holds around 28% of the global Biostorage Service market share, with Germany, the United Kingdom, and France serving as key demand centers. The region operates more than 500 certified biobanking facilities aligned with ISO 20387 standards. Regulatory pressure emphasizing traceability and cross-border biospecimen transfer compliance has increased outsourcing rates by 30% among pharmaceutical developers. Sustainability initiatives targeting 20% energy reduction by 2030 are driving adoption of low-global-warming-potential refrigeration systems and optimized liquid nitrogen usage. Over 60% of European storage facilities have implemented digital inventory platforms to enhance audit transparency. A prominent life sciences logistics provider in Germany expanded GMP-compliant cold storage capacity by 18% in 2024 to serve advanced therapy developers. Regional consumer behavior reflects strong demand for explainable compliance systems and environmentally responsible cryogenic operations.

How Is Rapid Biomanufacturing Growth Transforming Cryogenic Storage Demand?

Asia-Pacific represents nearly 22% of global Biostorage Service market volume and ranks as the fastest-growing regional contributor. China, India, and Japan collectively account for over 65% of regional demand, supported by a 33% rise in biologics manufacturing facilities between 2022 and 2025. More than 1,200 clinical trials across the region require validated temperature-controlled storage. Infrastructure modernization, including automated inventory systems and smart monitoring platforms, has improved compliance accuracy by 24% in newly established repositories. A major Japanese life sciences service provider expanded cryogenic storage units by 20% in 2024 to meet regenerative medicine demand. Regional consumer behavior indicates rapid adoption among biotechnology startups and government-backed research institutes seeking scalable, cost-efficient, and digitally integrated biostorage solutions.

How Are Expanding Vaccine Programs and Research Initiatives Driving Controlled Storage Demand?

South America accounts for approximately 5% of the global Biostorage Service market, led by Brazil and Argentina. Brazil manages more than 300 active biomedical research projects annually requiring ultra-low temperature preservation. Government health initiatives and vaccine development programs have increased demand for GMP-compliant storage facilities by 22% over the past three years. Infrastructure improvements in cold-chain logistics have enhanced sample transport reliability by 18%. A regional life sciences logistics company expanded refrigerated and cryogenic storage capacity by 15% in 2024 to support immunization research. Consumer behavior across the region reflects growing institutional reliance on outsourced storage services, particularly among public research centers and hospital networks seeking standardized compliance frameworks.

How Are Healthcare Modernization Efforts Supporting Advanced Sample Preservation Systems?

The Middle East & Africa region represents close to 4% of the global Biostorage Service market, with the United Arab Emirates and South Africa emerging as major contributors. Government-led genomic and precision medicine programs have increased demand for cryogenic infrastructure by 19% since 2023. More than 120 large-scale hospital laboratories in the region require validated long-term biospecimen storage. Technological modernization efforts include smart temperature monitoring systems and automated sample tracking platforms, now implemented in over 45% of newly developed facilities. A UAE-based healthcare logistics operator expanded ultra-low temperature storage capacity by 17% in 2024 to support regional research partnerships. Consumer behavior trends indicate increasing institutional preference for internationally compliant and digitally monitored storage environments.

United States – 38% market share: The Biostorage Service market in the United States leads globally due to high biologics production capacity, over 2,000 active advanced therapy trials, and extensive GMP-compliant cryogenic infrastructure.

Germany – 12% market share: The Biostorage Service market in Germany is driven by strong pharmaceutical manufacturing, more than 100 certified biobanks, and rigorous regulatory compliance standards supporting long-term biospecimen preservation.

The Biostorage Service market is moderately fragmented, with more than 120 active global and regional service providers competing across cryogenic storage, ultra-low temperature warehousing, and integrated cold-chain logistics. The top five companies collectively account for approximately 44% of total market share, reflecting a semi-consolidated competitive structure where scale, regulatory compliance, and technological sophistication determine market positioning. Leading providers differentiate through automated cryogenic facilities, AI-enabled monitoring platforms, and multi-continent storage networks supporting over 10 million biospecimens annually.

Strategic initiatives between 2023 and 2025 include more than 15 announced facility expansions globally, increasing combined storage capacity by over 30%. Partnerships between biostorage operators and contract research organizations have risen by 26%, strengthening integrated clinical trial sample management solutions. Mergers and acquisitions activity has accelerated, with at least 8 mid-sized storage providers acquired in the past two years to expand geographic reach and GMP-certified infrastructure. Innovation trends focus on robotic sample retrieval systems capable of reducing manual handling by 40%, predictive temperature analytics lowering freezer failure risk by 25%, and sustainability initiatives targeting 20% lower facility energy consumption. Competitive intensity is further shaped by stringent regulatory compliance, validated disaster recovery systems, and multi-layered digital traceability platforms that enhance long-term client retention and global contract scalability.

Azenta Life Sciences

Thermo Fisher Scientific

Labcorp Drug Development

Cryoport Systems

BioLife Solutions

Charles River Laboratories

Precision for Medicine

Marken

QPS Holdings

WuXi AppTec

The Biostorage Service market is being reshaped by a wave of digital and automation technologies that enhance operational reliability, compliance, and sample integrity. Ultra-low temperature (ULT) storage systems capable of maintaining -80°C are widely deployed across more than 65% of biorepositories, but emerging vapor-phase liquid nitrogen (VPLN) cryogenic systems maintaining temperatures below -150°C are now implemented in over 47% of facilities managing advanced therapy and cellular material. These advanced cryogenic platforms incorporate automated sample retrieval robotics that reduce manual handling by up to 42%, significantly improving throughput and reducing error risks in high-volume facilities housing millions of biospecimens.

IoT-enabled temperature and humidity sensors are now integrated across nearly 72% of contemporary storage facilities, providing real-time alerts and remote monitoring dashboards that enhance compliance tracking and reduce critical excursion incidences by 29%. Predictive analytics systems, powered by machine learning, are increasingly employed to forecast equipment failures, cutting unplanned downtime by approximately 25% and extending freezer lifecycle performance. Inventory management platforms leveraging barcode and RFID tracking have improved audit traceability and audit-readiness metrics by more than 33%, enabling seamless integration with enterprise quality management systems.

Emerging technologies such as blockchain-based chain-of-custody records are gaining traction in roughly 18% of large-scale biostorage networks, supporting immutable tracking of sample handling across multi-site operations. Additionally, digital twin simulations are used in facility planning to optimize storage density and energy utilization, improving spatial efficiency by up to 22%. Sustainability-oriented innovations include energy recovery systems in ultra-low freezers, reducing power usage by approximately 18% and supporting organizational ESG commitments for lower carbon footprints. The convergence of these technologies is driving greater transparency, scalability, and risk mitigation across the Biostorage Service market, making technology strategy a central pillar for competitive differentiation and long-term client retention.

• In March 2024, Azenta Life Sciences expanded its automated cryogenic storage facility in the United States, increasing capacity by over 1 million additional biospecimen slots and integrating advanced robotic retrieval systems to enhance sample accuracy and reduce manual handling risks. Source: www.azenta.com

• In September 2024, Cryoport Systems announced the expansion of its global supply chain network with upgraded cryogenic storage and logistics capabilities in Europe, strengthening support for cell and gene therapy clients and enhancing temperature-controlled storage compliance infrastructure. Source: www.cryoport.com

• In February 2025, BioLife Solutions reported the launch of its next-generation freezer management platform integrating real-time monitoring analytics, designed to reduce temperature excursions and improve preventive maintenance performance across regulated biostorage facilities. Source: www.biolifesolutions.com

• In April 2025, Thermo Fisher Scientific expanded its bioprocessing and cold storage infrastructure in North America, adding new GMP-compliant storage capacity to support increasing biologics and advanced therapy manufacturing demand. Source: www.thermofisher.com

The Biostorage Service Market Report provides comprehensive coverage of service types including ultra-low temperature (-80°C) storage, vapor-phase liquid nitrogen cryogenic systems below -150°C, and controlled ambient storage environments. The report evaluates storage capacities ranging from small-scale modular units managing fewer than 100,000 samples to large automated repositories exceeding 5 million biospecimens. It analyzes application segments spanning pharmaceutical research, biotechnology development, regenerative medicine, vaccine storage, clinical diagnostics, and academic biobanking initiatives.

Geographically, the report assesses market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional infrastructure density, regulatory alignment, and digital transformation adoption rates. More than 120 active service providers are examined, including global multi-site operators and regional specialized cryogenic storage firms. The report further outlines technology integration trends such as IoT-based temperature monitoring deployed in over 70% of modern facilities, robotic retrieval systems reducing manual handling by up to 40%, and energy-efficient ultra-low freezers lowering power consumption by approximately 18%.

In addition to core segments, the scope includes emerging niches such as decentralized clinical trial storage hubs, blockchain-enabled chain-of-custody systems, and ESG-focused sustainable cryogenic operations targeting 20% lower carbon emissions by 2030. The report offers structured insights into compliance frameworks, operational risk management models, infrastructure scalability strategies, and digital inventory platforms shaping next-generation biostorage service ecosystems for pharmaceutical sponsors, research institutions, and contract development organizations.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

15.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Azenta Life Sciences, Thermo Fisher Scientific, Labcorp Drug Development, Cryoport Systems, BioLife Solutions, Charles River Laboratories, Precision for Medicine, Marken, QPS Holdings, WuXi AppTec |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |