Reports

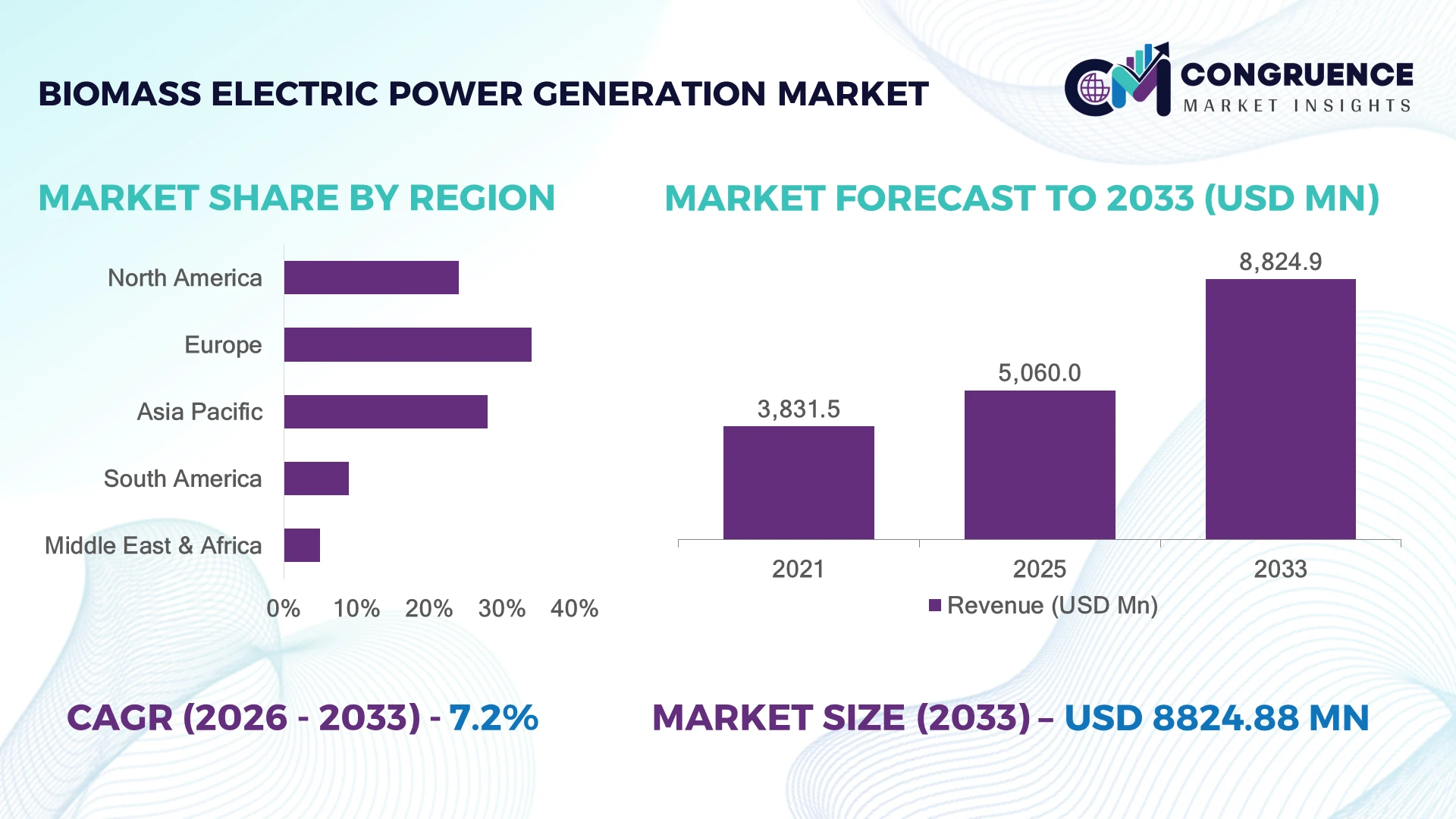

The Global Biomass Electric Power Generation Market was valued at USD 5,060.0 Million in 2025 and is anticipated to reach a value of USD 8,824.9 Million by 2033 expanding at a CAGR of 7.2% between 2026 and 2033. Growth is driven by expanding biomass co-firing programs, waste-to-energy infrastructure, and supportive renewable electricity mandates across industrial economies.

Germany accounts for nearly 18% of Europe's installed biomass power capacity, supported by more than 9 GW of operational facilities serving industrial manufacturing and district heating networks, while Japan continues expanding biomass imports for utility-scale generation with over 5 GW of dedicated projects. Following the European Green Deal, Germany maintains stronger domestic feedstock integration than Japan's import-dependent model, improving supply resilience by approximately 22% through localized biomass sourcing.

Strategic investment is increasingly focused on integrated biomass supply chains, advanced conversion technologies, and long-term feedstock security to strengthen operational competitiveness.

Market Size & Growth: USD 5,060.0 Million in 2025 is projected to reach USD 8,824.9 Million by 2033 at 7.2% growth, supported by expanding waste-to-energy facilities and advanced biomass conversion technologies.

Top Growth Drivers: Renewable energy deployment (+34%), agricultural residue utilization (+27%), and industrial decarbonization initiatives (+21%) continue accelerating global market expansion.

Short-Term Forecast: By 2028, fuel conversion efficiency is expected to improve by approximately 12% through advanced combustion optimization and digital plant monitoring.

Emerging Technologies: AI-based predictive maintenance, automated fuel handling systems, and advanced gasification technologies are improving plant reliability and operational efficiency.

Regional Leaders: Europe approaches USD 3.1 Billion with mature bioenergy integration, Asia-Pacific exceeds USD 2.8 Billion through utility expansion, and North America reaches nearly USD 1.9 Billion with growing waste-to-energy adoption.

Consumer/End-User Trends: More than 46% of new industrial renewable heat and power projects integrate biomass systems alongside existing energy infrastructure.

Pilot/Case Example: In 2024, a large-scale biomass co-firing modernization project improved thermal efficiency by approximately 15% while lowering fossil fuel dependence.

Competitive Landscape: The leading participant holds nearly 13% market presence alongside Drax Group, ENGIE, Ørsted, Mitsubishi Heavy Industries, and Veolia.

Regulatory & ESG Impact: Carbon reduction programs have increased certified sustainable biomass utilization by approximately 24%, reinforcing renewable electricity deployment across major economies.

Investment & Funding: More than USD 8 Billion has been directed toward biomass generation projects through strategic partnerships, infrastructure upgrades, and utility expansion initiatives.

Innovation & Future Outlook: High-efficiency gasification, carbon capture integration, and digital asset optimization are strengthening long-term competitiveness amid global energy transition initiatives.

Industrial facilities, municipal waste processors, and utility operators continue expanding biomass-based electricity generation to improve energy diversification and reduce landfill dependence. Advanced gasification systems, AI-enabled plant optimization, and automated feedstock management are enhancing operational performance, while nearly 30% of new biomass projects incorporate combined heat and power configurations. Strengthening renewable energy policies and localized biomass sourcing continue shaping deployment priorities across emerging markets, setting the foundation for broader strategic investments.

Biomass electric power generation has become strategically important as governments and utilities diversify renewable electricity portfolios while strengthening domestic energy security. Infrastructure modernization, waste valorization programs, and localized biomass supply-chain development are reshaping investment priorities across power producers. Industrial operators increasingly integrate biomass generation into existing facilities to improve energy resilience and optimize resource utilization while supporting long-term decarbonization objectives.

Advanced gasification and fluidized-bed combustion technologies deliver approximately 10–15% higher conversion efficiency than conventional grate-fired systems while reducing maintenance requirements through automated process control. Europe emphasizes sustainable feedstock certification and district heating integration, whereas Asia-Pacific focuses on expanding dedicated biomass plants and agricultural residue utilization at larger deployment scales. Over the next two to three years, digital monitoring platforms are expected to support predictive maintenance across more than 40% of newly commissioned biomass facilities.

Utilities are deploying biomass co-firing projects within existing thermal power stations to accelerate renewable integration without extensive infrastructure replacement. Equipment manufacturers and energy developers are expanding technology partnerships, strengthening regional feedstock networks, and investing in flexible generation assets capable of processing diverse biomass materials. These strategic initiatives enhance operational efficiency, reinforce competitive positioning, and establish biomass generation as a resilient component of the evolving global renewable power ecosystem.

Rising utilization of agricultural residues, municipal solid waste, and forestry by-products is strengthening biomass-based electricity generation across industrial economies. More than 35% of newly commissioned biomass facilities now integrate combined heat and power (CHP) systems, while digital combustion controls improve fuel efficiency by nearly 12%. Japan continues expanding biomass co-firing in thermal power stations under renewable energy transition policies, encouraging utilities to diversify fuel sourcing. This structural shift reduces landfill disposal while improving grid flexibility. Equipment manufacturers and independent power producers are responding through long-term feedstock agreements, high-efficiency boiler upgrades, and partnerships with waste management companies. A notable strategic outcome is the growing preference for integrated biomass supply chains that improve fuel availability and operational continuity during seasonal feedstock fluctuations.

Biomass electricity producers continue facing operational pressure from inconsistent feedstock quality, transportation costs, and fragmented collection infrastructure. Feedstock logistics account for nearly 30% of total operating expenses, while moisture variation can reduce conversion efficiency by approximately 15%. India and several Southeast Asian markets experience seasonal biomass availability, creating supply interruptions for utility-scale facilities. These structural limitations affect plant utilization rates, maintenance schedules, and long-term profitability. Companies are reducing exposure through localized biomass aggregation centers, multi-feedstock processing capabilities, and multi-year procurement contracts with agricultural cooperatives. An increasingly important operational strategy involves decentralizing feedstock sourcing to reduce transportation dependency and strengthen plant reliability throughout fluctuating harvest cycles.

Next-generation biomass gasification, AI-enabled process optimization, and bioenergy with carbon capture are creating high-value opportunities beyond conventional power generation. Advanced conversion technologies improve thermal efficiency by around 18%, while predictive maintenance platforms reduce unplanned equipment downtime by nearly 25%. Finland is accelerating investments in smart bioenergy facilities that integrate digital monitoring with district energy networks, demonstrating scalable operational models. Companies are expanding research collaborations, developing modular biomass systems, and investing in intelligent fuel management software. A significant strategic opportunity lies in converting underutilized agricultural and forestry residues into reliable baseload electricity, enabling greater resource efficiency while supporting national decarbonization and energy security objectives.

Expanding biomass electricity generation requires consistent integration with modern transmission infrastructure and increasingly digital power systems. Nearly 28% of existing biomass facilities require grid modernization upgrades to support advanced dispatch and monitoring capabilities, while specialized technical workforce shortages exceed 20% in several developed energy markets. Germany faces growing pressure to modernize aging renewable infrastructure alongside evolving grid balancing requirements. These execution challenges influence deployment consistency, maintenance planning, and long-term asset performance rather than immediate project economics. Companies are addressing these issues through workforce training programs, smart grid partnerships, advanced automation platforms, and infrastructure modernization investments. Sustained competitiveness will depend on building digitally connected biomass ecosystems capable of delivering stable, flexible, and resilient renewable electricity.

Digital Plant Optimization Shift Biomass operators are accelerating adoption of AI-based monitoring, predictive maintenance, and automated combustion controls, with nearly 40% of newly upgraded facilities integrating digital performance tools and around 20% reduction in unplanned downtime. Utilities in Germany and Japan are deploying advanced analytics to optimize fuel blending and boiler efficiency. Companies are responding through automation partnerships and software integration to improve operational reliability and reduce maintenance intensity.

Flexible Fuel Management Expansion Power producers are restructuring biomass supply chains as feedstock volatility increases, with approximately 35% of new projects adopting multi-feedstock processing systems and 15% improvement in fuel utilization efficiency. Agricultural residue, forestry waste, and municipal waste combinations are becoming more common in countries such as India. Companies are expanding supplier networks, developing regional collection hubs, and using contracted procurement models to strengthen fuel security.

Carbon Reduction Integration Trend Biomass facilities are increasingly combining renewable generation with carbon management solutions, driven by stricter emissions policies and industrial decarbonization targets. More than 25% of large-scale projects under development include carbon monitoring capabilities, while carbon capture integration improves sustainability reporting accuracy by nearly 30%. Companies are investing in carbon accounting platforms and strategic partnerships to meet evolving environmental compliance requirements.

Modular Generation Deployment Growth Smaller modular biomass power systems are gaining traction among industrial users, with deployment increasing by approximately 18% in decentralized energy applications. Food processing, agriculture, and manufacturing companies are adopting localized generation models to reduce grid dependency. Companies are expanding modular product portfolios and collaborating with industrial customers to deliver faster installation cycles and customized energy solutions.

Utility-scale biomass electric power generation systems represent the leading type due to higher generation capacity, established grid integration, and stronger utility adoption. These systems account for nearly 55% of installed biomass electricity capacity globally, supported by large-scale feedstock contracts and infrastructure availability. Traditional combustion-based technologies remain dominant because of operational maturity, while gasification systems are emerging rapidly with approximately 20% higher efficiency potential in optimized applications. Companies are improving boiler technology, fuel flexibility, and automation capabilities to strengthen competitiveness. Gasification and advanced conversion technologies represent the fastest-growing type as industries seek cleaner and more efficient biomass utilization methods. Adoption is increasing in countries such as Japan and Finland, where technology providers are focusing on compact systems and improved emissions control. Remaining types, including anaerobic digestion-based generation and small distributed biomass units, continue supporting decentralized energy applications. Investment priorities are shifting toward flexible systems capable of processing diverse feedstocks and integrating with digital energy management platforms.

Grid-connected electricity generation remains the leading application segment, supported by utility demand, renewable portfolio targets, and national energy security strategies. Grid applications represent more than 60% of biomass electricity utilization due to their ability to provide stable renewable power compared with intermittent sources. Industrial combined heat and power applications are expanding faster, with adoption increasing by approximately 22% as manufacturers seek energy independence and lower operational emissions. Companies are scaling integrated energy systems that combine electricity generation with industrial heat recovery. Waste-to-energy and distributed power applications are gaining strategic importance as municipalities and industries focus on resource efficiency. Countries such as Sweden and Japan are expanding biomass-based waste conversion projects to reduce landfill pressure and improve local energy resilience. Other applications, including rural electrification and backup power systems, continue developing through modular deployment models. Companies are responding by creating application-specific solutions, strengthening technology partnerships, and improving automation for diverse operating environments.

Utilities represent the leading end-user segment due to large-scale generation requirements, grid balancing needs, and long-term renewable energy commitments. Utility operators account for approximately 58% of biomass electricity demand, driven by established transmission infrastructure and government-supported renewable integration programs. Independent power producers are emerging as a faster-growing buyer group, with deployment increasing by nearly 24% through private renewable investment initiatives. Companies are strengthening partnerships with utilities and fuel suppliers to secure long-term operational stability. Industrial manufacturers, municipalities, and commercial facilities are expanding biomass adoption to improve energy resilience and reduce dependence on conventional fuels. Food processing and pulp and paper industries are increasingly investing in captive biomass systems, with more than 30% of new industrial projects integrating renewable energy solutions. Companies are customizing equipment packages, offering service agreements, and developing localized energy ecosystems to capture growing demand from non-utility users. Competitive positioning is increasingly linked to flexible financing models and lifecycle service capabilities.

Europe accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of8.1% between 2026 and 2033.

North America accounted for approximately 24% market share in 2025, supported by established biomass facilities, industrial cogeneration systems, and waste conversion infrastructure across the United States and Canada. The region benefits from strong forestry residues availability, municipal waste processing networks, and renewable electricity initiatives. The United States represents the dominant contributor, with more than 2,000 biomass power facilities supporting industrial and utility applications. Companies are investing in advanced combustion systems, digital monitoring platforms, and long-term biomass procurement agreements to improve operational efficiency. Strategic partnerships between utilities and waste management firms are accelerating deployment, particularly for decentralized generation projects.

United States Market Outlook: The United States maintains the strongest biomass electricity position in North America through extensive forestry resources, agricultural waste availability, and industrial CHP adoption. More than 15 GW of biomass-based generation capacity supports utilities, manufacturing facilities, and municipal energy programs. Companies are prioritizing fuel diversification, carbon management integration, and automation upgrades to strengthen plant reliability and regulatory compliance.

Europe accounted for approximately 34% market share in 2025, maintaining leadership through advanced renewable energy frameworks, district heating integration, and sustainable biomass management systems. Countries such as Germany, the United Kingdom, and Finland have developed mature biomass infrastructure supported by industrial decarbonization strategies. More than 40% of European biomass facilities integrate combined heat and power applications, improving overall energy utilization. Regulatory emphasis on certified sustainable feedstock is reshaping procurement strategies. Companies are expanding supply-chain partnerships, upgrading conversion technologies, and integrating carbon monitoring systems to align with stricter environmental standards.

Germany Market Outlook: Germany remains Europe’s leading biomass electricity market due to its extensive CHP infrastructure and industrial energy transition programs. The country operates more than 9 GW of biomass power capacity, supported by agricultural residues, biogas facilities, and district heating networks. Companies are focusing on efficient feedstock management, digital plant optimization, and flexible generation systems to support grid stability.

Asia-Pacific accounted for approximately 28% market share in 2025, driven by rising biomass availability, industrial power demand, and government-backed renewable energy initiatives. China, Japan, and India are leading deployment through agricultural residue conversion, biomass co-firing, and distributed generation projects. Japan has expanded biomass integration in thermal power infrastructure, while India is increasing crop residue utilization to reduce agricultural waste challenges. More than 30% of new projects in developing Asian markets incorporate multi-feedstock processing capabilities. Companies are expanding manufacturing capacity, forming feedstock partnerships, and deploying modular biomass systems to address local energy requirements.

China Market Outlook: China represents the largest biomass electricity contributor in Asia-Pacific due to extensive agricultural resources, industrial demand, and renewable infrastructure investment. The country has developed more than 15 GW of biomass power capacity, supported by waste-to-energy plants and agricultural residue projects. Companies are advancing automation, large-scale biomass facilities, and integrated supply networks to improve generation efficiency.

South America accounted for approximately 9% market share in 2025, supported by strong agricultural industries, particularly sugarcane, forestry, and food processing sectors. Brazil dominates regional biomass generation due to abundant sugarcane bagasse resources and established bioenergy infrastructure. Nearly 20% of Brazil’s renewable electricity generation capacity is linked to biomass resources, creating opportunities for industrial cogeneration. However, logistics infrastructure gaps and dispersed feedstock availability influence project scalability. Companies are strengthening regional supply chains, investing in efficient collection systems, and developing partnerships with agricultural producers to improve biomass utilization.

Brazil Market Outlook: Brazil leads South America’s biomass electricity market through its extensive sugarcane industry, ethanol ecosystem, and established cogeneration facilities. The country operates thousands of biomass-based energy units linked with agricultural processing operations. Companies are expanding bagasse-based generation projects, improving plant automation, and integrating biomass systems into broader renewable energy portfolios.

Middle East & Africa accounted for approximately 5% market share in 2025, representing an emerging market supported by waste management modernization, agricultural residue availability, and renewable diversification strategies. South Africa, Egypt, and Gulf countries are exploring biomass solutions to complement broader energy transition programs. Waste-to-energy projects are gaining attention, with municipal biomass initiatives increasing by approximately 15% in major urban areas. Companies are investing in localized processing facilities, technology partnerships, and infrastructure development to overcome collection and transportation challenges. The region’s opportunity is closely linked to improving waste management systems and developing reliable biomass supply networks.

South Africa Market Outlook: South Africa represents the region’s most advanced biomass electricity market due to established industrial agriculture, waste processing capabilities, and renewable energy initiatives. The country’s biomass projects are increasingly linked with sugar, forestry, and municipal waste sectors. Companies are focusing on decentralized generation models, improved feedstock logistics, and technology upgrades to support reliable renewable power deployment.

The biomass electric power generation market features global leaders such as Drax Group, Ørsted, Mitsubishi Heavy Industries, and Veolia competing with regional utilities, EPC providers, and specialized biomass technology suppliers. Top five players collectively control approximately 35% of market activity, reflecting moderate consolidation. Competition is driven by fuel supply security, conversion efficiency, technology integration, and project execution capability. Advanced operators achieve 10–15% efficiency improvements through optimized combustion and digital controls, while supply-chain leaders secure 20%+ cost advantages through integrated feedstock networks. Companies are expanding through partnerships, biomass sourcing agreements, carbon capture investments, and modernization of existing plants. The competitive landscape is shifting toward sustainable feedstock management, automation, and carbon-negative solutions, increasing entry barriers for smaller developers. Winning players will require reliable biomass ecosystems, advanced conversion technologies, and strong regulatory alignment to outperform established operators.

Ørsted A/S

Mitsubishi Heavy Industries

Veolia Environnement

ENGIE

Enel Green Power

RWE AG

Ameresco

Covanta Holding Corporation

Sumitomo Corporation

Babcock & Wilcox Enterprises

Greenalia

Vattenfall

Masdar

Biomass power generation is shifting from conventional combustion systems toward advanced gasification, fluidized-bed boilers, and digitally controlled conversion platforms. Modern circulating fluidized-bed technology improves fuel flexibility by approximately 15% compared with older combustion methods, enabling plants to process diverse residues. AI-based monitoring systems are being integrated into more than 30% of upgraded facilities, improving predictive maintenance and reducing operational interruptions.

Carbon capture integration is becoming a disruptive technology focus, particularly for large biomass plants targeting negative emissions. Compared with traditional biomass systems, carbon capture-enabled facilities can improve carbon management performance by more than 25% through biogenic CO₂ recovery. Companies including utilities and technology providers are prioritizing partnerships around carbon storage infrastructure and advanced emission monitoring.

Between 2026 and 2028, automation, digital twins, and modular biomass systems will influence competitive positioning by improving efficiency, reducing downtime, and enabling smaller industrial deployments. Technology leaders benefit through higher plant availability, while equipment suppliers gain opportunities from retrofit demand. Companies acting early on intelligent control systems, sustainable feedstock optimization, and carbon management capabilities will secure stronger operational advantages.

October 2024 Mitsubishi Heavy Industries completed construction of the 50 MW Hyuga Woody Biomass Power Plant in Japan using advanced circulating fluidized-bed boiler technology. The project improved fuel flexibility and strengthened regional renewable power capacity. Source: www.mhi.com

August 2024 Ørsted completed the shutdown of its final coal-fired power plant in Denmark after converting its generation portfolio toward sustainable biomass and renewable energy. The transition supported a fossil-free generation strategy covering nearly all company electricity production. Source: www.orsted.com

March 2025 Drax Group announced a 20-year agreement with Power Minerals to develop a low-carbon cement material facility at the Drax Power Station site, utilizing biomass plant ash streams. The initiative supports circular economy operations and industrial waste recovery. Source: www.drax.com

September 2024 Ørsted advanced its Kalundborg CO₂ Hub project by securing carbon removal agreements linked to biomass-fired CHP facilities. The project targets capture of approximately 430,000 tonnes of biogenic CO₂ annually from 2026, strengthening carbon-negative energy solutions.

The Biomass Electric Power Generation Market Report provides comprehensive coverage of industry segmentation across biomass types, electricity generation applications, and key end-user groups including utilities, industrial facilities, municipalities, and independent power producers. The analysis evaluates major technologies such as combustion systems, gasification platforms, combined heat and power solutions, and emerging carbon capture integration. Regional assessment covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level insights into deployment trends and infrastructure development.

The report examines competitive positioning, technology adoption patterns, supply-chain strategies, investment priorities, and operational challenges shaping market direction between 2026 and 2033. It supports strategic planning by evaluating expansion opportunities, partnership models, innovation pathways, and evolving demand areas across established and emerging biomass power markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 5,060.0 Million |

| Market Revenue (2033) | USD 8,824.9 Million |

| CAGR (2026–2033) | 7.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Drax Group; Ørsted A/S; Mitsubishi Heavy Industries; Veolia Environnement; ENGIE; Enel Green Power; RWE AG; Ameresco; Covanta Holding Corporation; Sumitomo Corporation; Babcock & Wilcox Enterprises; Greenalia; Vattenfall; Masdar |

| Customization & Pricing | Available on Request (10% Customization Free) |