Reports

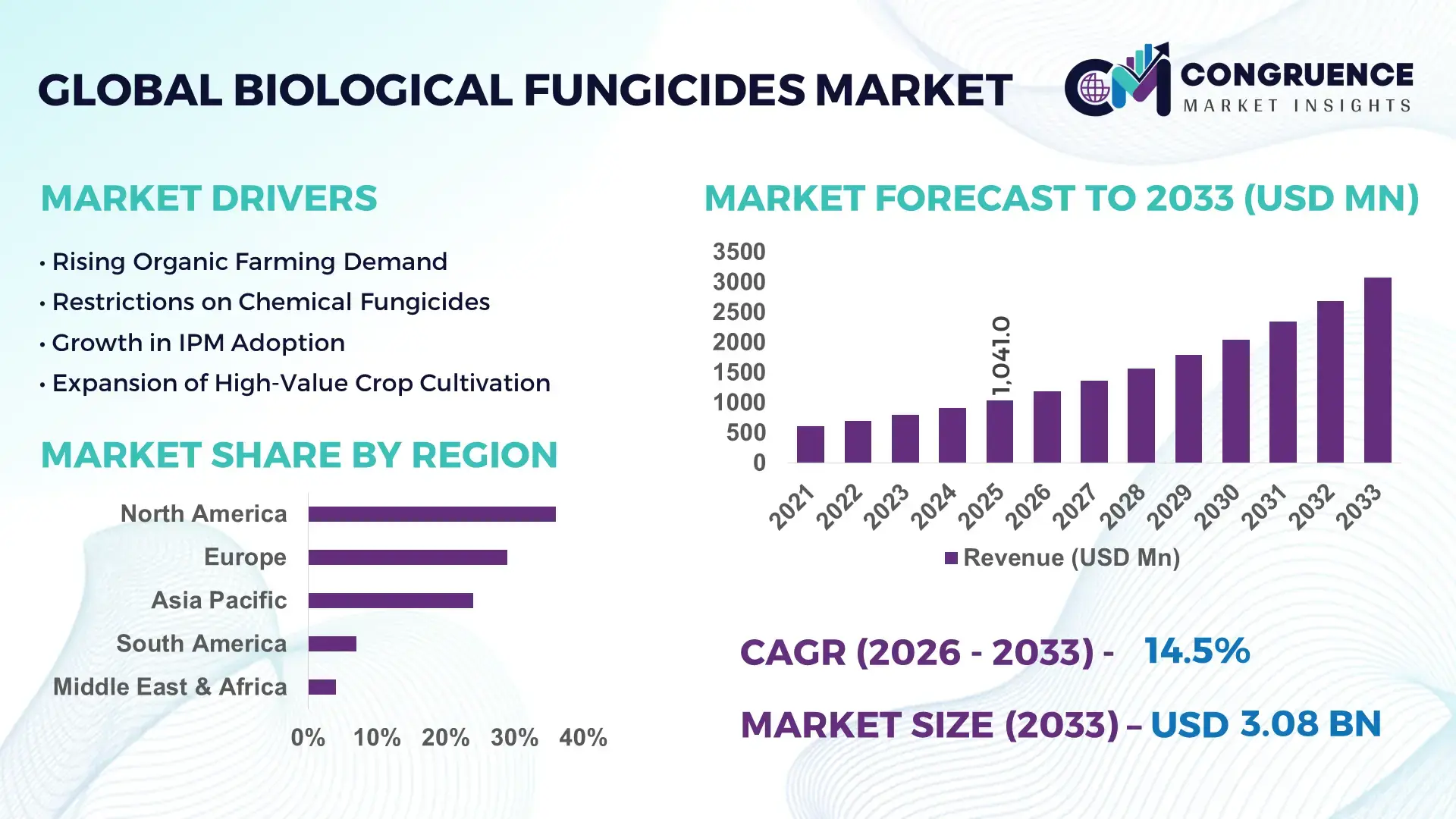

The Global Biological Fungicides Market was valued at USD 1,041.0 Million in 2025 and is anticipated to reach a value of USD 3,075.4 Million by 2033 expanding at a CAGR of 14.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by accelerating adoption of sustainable crop protection solutions and regulatory restrictions on synthetic chemical fungicides across major agricultural economies.

The United States dominates the Biological Fungicides Market in terms of production infrastructure and technology deployment. The country accounts for over 35% of global biological crop protection product registrations and hosts more than 120 commercial-scale biopesticide manufacturing facilities. The U.S. Environmental Protection Agency (EPA) has approved over 430 active biopesticide ingredients, with microbial fungicides forming a significant portion. Biological solutions are used across more than 28% of high-value fruit and vegetable acreage, particularly in California and Florida. Investments exceeding USD 600 million between 2022 and 2025 have been directed toward microbial fermentation capacity expansion, precision formulation technologies, and bio-based seed treatment platforms, strengthening large-scale domestic production and export capabilities.

Market Size & Growth: Valued at USD 1,041.0 Million in 2025, projected to reach USD 3,075.4 Million by 2033 at a CAGR of 14.5%, driven by a 40% rise in organic farming acreage globally.

Top Growth Drivers: 38% increase in organic crop cultivation, 42% reduction in chemical residue tolerance levels, 30% higher export compliance requirements for residue-free produce.

Short-Term Forecast: By 2028, biological fungicide adoption is expected to improve crop disease control efficiency by 25% while reducing chemical fungicide dependence by 20%.

Emerging Technologies: AI-driven microbial strain selection, CRISPR-enhanced bio-agents, nano-encapsulation improving field stability by 35%.

Regional Leaders: North America projected to reach USD 1,050 Million by 2033 with advanced greenhouse usage; Europe nearing USD 890 Million supported by strict residue norms; Asia-Pacific expected at USD 760 Million due to expanding horticulture acreage.

Consumer/End-User Trends: Over 45% of fruit & vegetable growers are integrating biological fungicides into integrated pest management (IPM) programs.

Pilot or Case Example: In 2024, a California vineyard pilot reduced fungal infection incidence by 32% using Bacillus-based biofungicides combined with drone-based spraying.

Competitive Landscape: Market leader holds approximately 18% share, followed by 4–5 global agro-biological innovators with diversified microbial portfolios.

Regulatory & ESG Impact: More than 60 countries have tightened maximum residue limits (MRLs), accelerating transition to low-toxicity crop protection solutions.

Investment & Funding Patterns: Over USD 1.2 Billion invested globally in agricultural biologicals between 2021–2025, with strong venture funding in microbial R&D.

Innovation & Future Outlook: Integration with digital agronomy platforms and precision spraying technologies is expected to enhance application accuracy by 30% over the next decade.

Cereals contribute nearly 32% of biological fungicide usage, followed by fruits and vegetables at 41%, and oilseeds at 18%. Recent innovations include spore-stable Bacillus formulations and dual-action Trichoderma strains enhancing root resistance by 27%. Regulatory push for chemical residue reduction and carbon-neutral farming practices are accelerating adoption in Europe and North America. Asia-Pacific is witnessing 20% growth in protected cultivation, supporting sustained long-term demand.

The Biological Fungicides Market holds strategic importance in advancing sustainable agriculture, strengthening food security, and ensuring regulatory compliance in global trade. With over 190 million hectares under organic cultivation worldwide, growers increasingly rely on microbial fungicides to protect high-value crops while maintaining export standards. Strategy is shifting toward integrating biological fungicides within comprehensive Integrated Pest Management (IPM) frameworks, improving disease suppression rates by up to 35% compared to standalone chemical programs.

CRISPR-enhanced microbial strains deliver 28% higher pathogen inhibition efficiency compared to conventional wild-type bio-agents, positioning advanced biotechnology as a competitive differentiator. North America dominates in production volume, while Europe leads in adoption with over 52% of greenhouse enterprises integrating biological crop protection into routine disease management programs.

By 2028, AI-enabled disease prediction platforms are expected to reduce fungicide over-application by 22%, directly improving input efficiency and lowering environmental runoff. Firms are committing to ESG targets, including 30% reduction in synthetic pesticide intensity by 2030 and measurable soil biodiversity improvements.

In 2025, a U.S.-based agri-biotech firm achieved a 34% improvement in shelf-life stability through microencapsulation technology, reducing storage losses and enhancing field persistence. Looking ahead, the Biological Fungicides Market is positioned as a pillar of agricultural resilience, regulatory alignment, and sustainable yield enhancement in a climate-sensitive global food system.

The Biological Fungicides Market is evolving in response to structural shifts in global agriculture, sustainability mandates, and technological progress in microbial science. Increasing restrictions on chemical fungicides across more than 60 countries are accelerating substitution trends. Expansion of greenhouse cultivation—now exceeding 5 million hectares globally—has intensified demand for residue-free disease control solutions. Advancements in fermentation technology have improved microbial production efficiency by nearly 30% over the past decade, reducing batch variability and enhancing scalability. Simultaneously, rising incidences of fungicide-resistant pathogens are pushing growers toward biological rotation strategies. Digital agriculture tools, including remote disease diagnostics and drone-assisted application systems, are further optimizing deployment precision and improving overall field performance metrics.

Global organic food sales surpassed USD 130 billion, supported by over 190 million hectares of certified organic farmland. More than 45% of consumers in developed economies prefer residue-free produce, increasing pressure on growers to reduce chemical inputs. Export-driven agricultural economies must comply with strict maximum residue limits, affecting over 70% of fruit and vegetable shipments. Biological fungicides offer targeted disease suppression without harmful residues, enabling growers to maintain compliance while preserving soil microbiota. Additionally, large retail chains now mandate sustainable sourcing certifications, influencing procurement policies across 35% of commercial farms supplying international markets.

Biological fungicides often exhibit shorter shelf stability—averaging 12–24 months compared to over 36 months for synthetic products. Field efficacy can decline by 15–20% under extreme temperature or UV exposure. Storage and transport require controlled conditions, increasing logistical complexity for distributors. In regions with high humidity variability, microbial viability losses can exceed 18% during peak summer months. Farmers in emerging markets may lack adequate cold-chain infrastructure, limiting adoption. Additionally, slower initial pathogen suppression compared to chemical fungicides can influence grower perception, especially in high-risk disease outbreaks.

Precision agriculture adoption has expanded across more than 30% of large-scale farms globally. Drone-assisted spraying improves application uniformity by 26% and reduces input waste by 18%. Integration of IoT soil sensors enables real-time pathogen monitoring, enhancing timing accuracy of biological fungicide application. Greenhouse horticulture—growing at over 20% annually in parts of Asia—provides controlled environments ideal for microbial stability. Seed treatment applications represent another growth avenue, with bio-based treatments improving seedling survival rates by up to 24% in field trials.

Developing a new microbial fungicide can require 6–8 years of validation, including efficacy trials across multiple climatic zones. Registration processes in regulated markets demand toxicology and environmental safety data, increasing compliance costs by 20–25%. Scaling fermentation capacity requires capital-intensive bioreactors, often exceeding USD 10 million per facility. Additionally, maintaining consistent microbial strain performance across geographies presents formulation complexities. Resistance management protocols also require ongoing field monitoring programs, adding operational expenditures for manufacturers and distributors.

Expansion of Microbial Fermentation Capacity: Global fermentation capacity for agricultural biologicals has increased by 32% since 2022, with average batch yields improving by 27% through automated bioreactor systems. Over 150 new pilot-scale fermentation units have been commissioned globally, enhancing supply reliability and reducing microbial production cycle time by 18%.

Integration with Digital Disease Forecasting Platforms: Approximately 36% of large-scale farms now use AI-based crop disease prediction tools. These platforms reduce unnecessary fungicide applications by 22% and improve targeted intervention timing accuracy by 31%, directly enhancing biological product efficiency under field conditions.

Growth in Protected Cultivation and High-Value Crops: Greenhouse cultivation area has expanded by 20% in Asia-Pacific and 14% in Europe. Biological fungicides are used in nearly 48% of greenhouse vegetable operations, improving disease management consistency by 29% compared to open-field application variability.

Increased Adoption in Seed Treatment Programs: Bio-based seed treatments now account for 26% of new seed protection registrations. Field trials demonstrate 24% higher seedling survival rates and 19% improvement in early-stage root vigor, supporting broader integration of microbial fungicides in pre-plant disease prevention strategies.

The Biological Fungicides Market is segmented by type, application, and end-user, reflecting the diversification of microbial technologies and crop protection strategies across agricultural systems. Product-level segmentation highlights the dominance of microbial-based formulations, particularly Bacillus and Trichoderma strains, which are widely used in integrated pest management programs. Application-based segmentation reveals strong adoption in fruits and vegetables, driven by strict residue limits and export compliance standards. Cereals and oilseeds also contribute significantly due to large cultivation acreage exceeding 700 million hectares globally.

From an end-user perspective, large commercial farms account for the majority of usage due to structured crop protection programs and access to advanced agronomic advisory systems. However, small and medium-scale growers are rapidly integrating biological fungicides, particularly in emerging markets where sustainable farming incentives and input cost optimization are priorities. Segmentation trends indicate a shift toward seed treatment and greenhouse-based applications, where microbial stability and targeted delivery systems offer measurable performance advantages over conventional foliar chemical sprays.

Microbial fungicides represent the leading type, accounting for approximately 68% of total product adoption. Bacillus-based biofungicides alone contribute nearly 38%, while Trichoderma strains hold around 21%. These products are preferred due to their multi-mode pathogen suppression and compatibility with integrated pest management systems. Botanical fungicides account for 17%, valued for plant-derived active compounds, while biochemical fungicides hold 9%. However, adoption in RNA-based biological fungicides is rising fastest, expanding at an estimated CAGR of 16.8%, supported by advances in gene-silencing technologies and improved formulation stability. Microbial formulations remain dominant due to proven field efficacy, with disease incidence reductions averaging 28–35% in high-value horticulture crops. Botanical and biochemical segments collectively represent 26% of the market, serving niche organic and specialty crop segments. RNA-interference solutions, though currently under 6%, are projected to gain traction due to precision-targeting capabilities and lower non-target organism impact.

In 2024, the United States Environmental Protection Agency approved multiple new Bacillus-based active ingredients for crop disease management, expanding registered microbial fungicide solutions across specialty crop categories.

Fruits and vegetables constitute the leading application segment, accounting for approximately 41% of biological fungicide usage due to stringent export residue requirements and high disease susceptibility in perishable crops. Cereals represent 29%, while oilseeds and pulses account for 16%. However, greenhouse horticulture is the fastest-growing application segment, expanding at a CAGR of 15.9%, driven by controlled-environment farming practices and year-round cultivation cycles. While open-field horticulture dominates volume, greenhouse operations demonstrate higher per-acre biological fungicide usage intensity, often 22% greater than conventional farms. Seed treatment applications are also gaining momentum, with adoption exceeding 26% in newly registered biological crop protection products. In 2025, over 44% of large horticulture enterprises globally reported integrating biological fungicides into structured IPM frameworks. Additionally, approximately 37% of greenhouse vegetable producers in Europe utilize microbial fungicides as primary disease management tools.

In 2024, the European Food Safety Authority expanded approvals for microbial fungicide applications in greenhouse tomato and cucumber production, enabling wider adoption across protected cultivation systems.

Large commercial farms represent the leading end-user segment, accounting for nearly 54% of biological fungicide consumption due to structured crop management systems and compliance-driven export operations. Agribusiness cooperatives hold 18%, while small and medium-scale farms contribute 21%. However, greenhouse and vertical farming enterprises are the fastest-growing end-user group, expanding at a CAGR of 17.3%, supported by rising investment in protected agriculture and high-value crop cultivation. While large-scale farms dominate total application volume, adoption intensity in greenhouse enterprises is significantly higher, with usage rates exceeding 48% across protected vegetable production units. In 2025, more than 39% of agribusiness enterprises globally reported piloting biological fungicides in at least one major crop category. Additionally, approximately 34% of small-scale organic farmers in North America now rely primarily on microbial fungicides for fungal disease control.

In 2024, the United States Department of Agriculture reported increased participation in organic certification programs, with over 28,000 certified organic operations utilizing biological crop protection inputs across multiple crop categories.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2026 and 2033.

North America’s leadership is supported by over 28% organic farmland penetration in specialty crops and more than 430 registered biopesticide active ingredients. Europe follows with 29% share, driven by strict maximum residue limits and Farm-to-Fork sustainability targets aiming to reduce chemical pesticide use by 50% by 2030. Asia-Pacific holds approximately 24% share, supported by over 220 million hectares of cultivated land and rapid greenhouse expansion exceeding 20% in select economies. South America represents 7%, led by Brazil’s large soybean and fruit export base spanning more than 80 million hectares. The Middle East & Africa collectively account for 4%, with protected agriculture projects expanding by 18% in water-scarce nations. Regional consumption intensity varies, with greenhouse operations in Europe and North America using up to 22% higher biological input per hectare compared to open-field farms.

North America represents 36% of the global Biological Fungicides Market share, supported by strong regulatory frameworks and high organic acreage across the United States and Canada. Over 35% of fruit and vegetable farms integrate biological fungicides within structured IPM programs. Key demand drivers include specialty crops, greenhouse vegetables, vineyards, and almond orchards. Regulatory support through streamlined biopesticide approvals has reduced product registration timelines by nearly 25% over the past decade. Technological advancements such as drone-based spraying, AI-driven disease forecasting, and precision irrigation integration have improved application efficiency by 30%. Digital farm management systems are used by approximately 48% of large commercial farms. A leading regional player, Corteva Agriscience, has expanded microbial fermentation capacity and launched multi-strain biofungicide solutions targeting soil-borne pathogens. Regional consumer behavior reflects higher adoption among export-focused growers prioritizing residue-free certification and sustainability compliance.

Europe holds approximately 29% share of the Biological Fungicides Market, led by Germany, France, Italy, and Spain. The European Union’s Farm-to-Fork strategy targets a 50% reduction in chemical pesticide usage by 2030, accelerating biological product adoption. Over 52% of greenhouse enterprises in Western Europe report routine use of microbial fungicides. Adoption of emerging technologies such as automated greenhouse climate control and sensor-based pathogen detection has improved disease management accuracy by 27%. Digital agronomy platforms are deployed across nearly 40% of high-value horticulture farms. A prominent European player, Koppert Biological Systems, continues expanding beneficial microbe portfolios and integrated biological crop protection programs. Regional consumer behavior shows strong alignment with sustainability labeling, with over 45% of consumers preferring produce certified under eco-friendly farming standards, reinforcing demand for biological fungicides.

Asia-Pacific accounts for nearly 24% of global Biological Fungicides Market volume and ranks as the fastest-growing regional market. China, India, and Japan represent the largest consuming countries, supported by combined cultivated land exceeding 300 million hectares. Greenhouse cultivation in China alone spans over 3 million hectares, encouraging higher-intensity biological fungicide usage. Manufacturing infrastructure is expanding, with more than 90 microbial formulation units established across India and Southeast Asia. Innovation hubs in Japan are focusing on RNA-based biofungicides and advanced fermentation efficiency improvements of up to 25%. UPL Limited has expanded biological product lines targeting rice and vegetable crops. Regional consumer behavior indicates rising adoption among smallholder farmers, with government-backed subsidy programs covering up to 40% of biological input costs in select countries.

South America represents 7% of the Biological Fungicides Market, led by Brazil and Argentina. Brazil alone cultivates more than 80 million hectares of soybeans and specialty crops, supporting biological fungicide integration across large commercial farms. Export compliance standards for fruit and coffee crops have increased biological input usage by approximately 18% over five years. Infrastructure modernization in precision agriculture has expanded across 32% of large farms. Government-backed low-carbon agriculture programs provide incentives covering up to 25% of sustainable input investments. A regional player, Biotrop (Brazil), has scaled microbial production facilities to enhance domestic supply capacity. Consumer behavior reflects strong alignment with export-driven compliance, where residue-free certification is mandatory for over 70% of high-value shipments.

The Middle East & Africa account for approximately 4% of the Biological Fungicides Market, with demand concentrated in the UAE, Saudi Arabia, South Africa, and Kenya. Protected agriculture projects have expanded by 18% in arid Gulf countries, promoting high-intensity biological fungicide usage per hectare. Technological modernization, including hydroponic and vertical farming systems, has increased by 22% across urban food security initiatives. Trade partnerships with European agri-biotech suppliers facilitate product imports and local formulation partnerships. In South Africa, domestic biopesticide manufacturers are expanding production capacity to meet rising horticulture demand. Consumer behavior reflects strong preference for residue-free produce in premium retail chains, with biological crop protection integrated into nearly 35% of commercial greenhouse operations.

United States – 32% Market Share: Strong production capacity, over 430 registered biopesticide active ingredients, and widespread adoption in high-value specialty crops drive leadership in the Biological Fungicides Market.

Germany – 11% Market Share: Stringent pesticide reduction mandates and advanced greenhouse horticulture infrastructure position Germany as a key contributor to the Biological Fungicides Market in Europe.

The Biological Fungicides Market is moderately fragmented, with more than 120 active global and regional competitors engaged in microbial strain development, formulation technologies, and integrated crop protection solutions. The top five companies collectively account for approximately 46% of the total market share, reflecting a competitive yet innovation-driven environment. Large multinational agrochemical corporations are increasingly expanding biological portfolios to complement synthetic product lines, while specialized agri-biotech firms focus exclusively on microbial and bio-based innovations.

Strategic initiatives between 2023 and 2025 include over 35 product launches targeting soil-borne and foliar fungal pathogens, 18 cross-border distribution partnerships, and at least 12 mergers or technology acquisitions aimed at strengthening fermentation capacity and strain libraries. Investment in advanced fermentation infrastructure has increased by nearly 30%, with automated bioreactors improving production yields by up to 27%. Competitive differentiation increasingly centers on multi-strain formulations, extended shelf-life stability (up to 24 months), and digital agronomy integration improving application precision by 25%. Companies are also investing in RNA-based and CRISPR-enhanced biologicals to enhance pathogen specificity and field persistence. Intellectual property filings related to microbial consortia have risen by 22% over the last three years, highlighting innovation intensity across the competitive landscape.

Corteva Agriscience

UPL Limited

Koppert Biological Systems

Valent BioSciences LLC

Certis Biologicals

Isagro S.p.A.

Biotrop Participações S.A.

Andermatt Group AG

Marrone Bio Innovations (now part of Bioceres Crop Solutions, listed independently for historical relevance)

Novozymes A/S

Sumitomo Chemical Co., Ltd.

Technological advancements are reshaping the Biological Fungicides Market by enhancing efficacy, shelf stability, and scalability. Microbial fermentation technologies have improved yield efficiency by approximately 25–30% through automated bioreactor systems and optimized nutrient substrates. Modern fermentation units now support batch cycles reduced by 18%, enabling faster commercialization of new microbial strains.

Nano-encapsulation and microencapsulation technologies are increasing field persistence of biofungicides by up to 35%, protecting active microorganisms from UV degradation and temperature fluctuations. RNA interference (RNAi)-based biological fungicides are emerging as precision-targeting tools capable of silencing specific fungal genes, improving pathogen suppression rates by 28% compared to conventional microbial strains.

CRISPR-based genome editing has accelerated microbial strain enhancement, enabling improved spore stability and root colonization efficiency by 22%. Additionally, integration with AI-driven disease forecasting platforms has reduced over-application by 20%, supporting optimized dosage control. Drone-assisted spraying systems have improved coverage uniformity by 26%, particularly in vineyards and greenhouse crops.

Digital traceability platforms are also gaining traction, enabling farmers to monitor biological application rates and soil microbiome health. More than 40% of large commercial farms now use sensor-based monitoring tools to align fungicide application with real-time humidity and pathogen risk indicators. Collectively, these technologies are positioning biological fungicides as precision-oriented, scalable alternatives within modern crop protection systems.

• In February 2025, Syngenta Crop Protection AG strengthened its global leadership in agricultural biologicals by acquiring natural products and genetic strain assets from Novartis and inaugurating a new purpose-built biologicals production facility in Orangeburg, South Carolina, USA, enhancing capacity for nature-inspired crop protection solutions and accelerating rollout of its expanded biologicals portfolio. Source: www.syngenta.com

• In March 2025, Syngenta announced a strategic partnership with Ceres Biotics to bring the innovative biological product VIXERAN® to growers worldwide, enabling enhanced nitrogen optimization and sustainable farm practices globally. Source: www.syngenta.com

• In January–April 2024, UPL Corporation Ltd. completed the acquisition of Corteva Agriscience’s solo mancozeb global fungicide business outside major markets, securing ownership of the iconic Dithane® brand and Rainshield™ technology for enhanced disease protection in wet conditions and broad crop use. Source: www.upl-ltd.com

• In March 2025, Syngenta and PepsiCo expanded its regenerative farming program, rewarding growers adopting sustainable practices that support traceable agriculture and drive biological solution usage on commercial farms. Source: www.syngenta.com

The Biological Fungicides Market Report provides a comprehensive evaluation of microbial and bio-based crop protection technologies across major agricultural economies. The scope covers product segmentation including microbial (Bacillus, Trichoderma, Pseudomonas), botanical extracts, biochemical agents, and emerging RNA-based biological fungicides. Application coverage spans fruits and vegetables, cereals, oilseeds, pulses, greenhouse horticulture, seed treatment, and specialty crops cultivated across more than 700 million hectares globally.

Geographically, the report analyzes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting region-specific adoption intensity, regulatory frameworks, greenhouse expansion trends, and organic farming penetration exceeding 190 million hectares worldwide. The study also assesses production infrastructure, including over 120 commercial fermentation facilities and advancements in automated bioreactor systems.

Technological focus areas include nano-encapsulation, CRISPR-enhanced microbial strains, RNA interference platforms, AI-driven disease prediction systems, and drone-based precision application tools improving coverage efficiency by over 25%. The report further examines end-user adoption across large commercial farms, agribusiness cooperatives, greenhouse enterprises, and smallholder farmers. Emerging niche segments such as vertical farming and hydroponic cultivation are evaluated for biological input intensity and sustainability alignment. Overall, the scope delivers strategic insights into innovation, regulatory compliance, competitive positioning, and sustainable agriculture transformation within the Biological Fungicides Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,041.0 Million |

| Market Revenue (2033) | USD 3,075.4 Million |

| CAGR (2026–2033) | 14.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Bayer AG; Syngenta Group; BASF SE; Corteva Agriscience; UPL Limited; Koppert Biological Systems; Valent BioSciences LLC; Certis Biologicals; Isagro S.p.A.; Biotrop Participações S.A.; Andermatt Group AG; Novozymes A/S; Marrone Bio Innovations; Sumitomo Chemical Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |