Reports

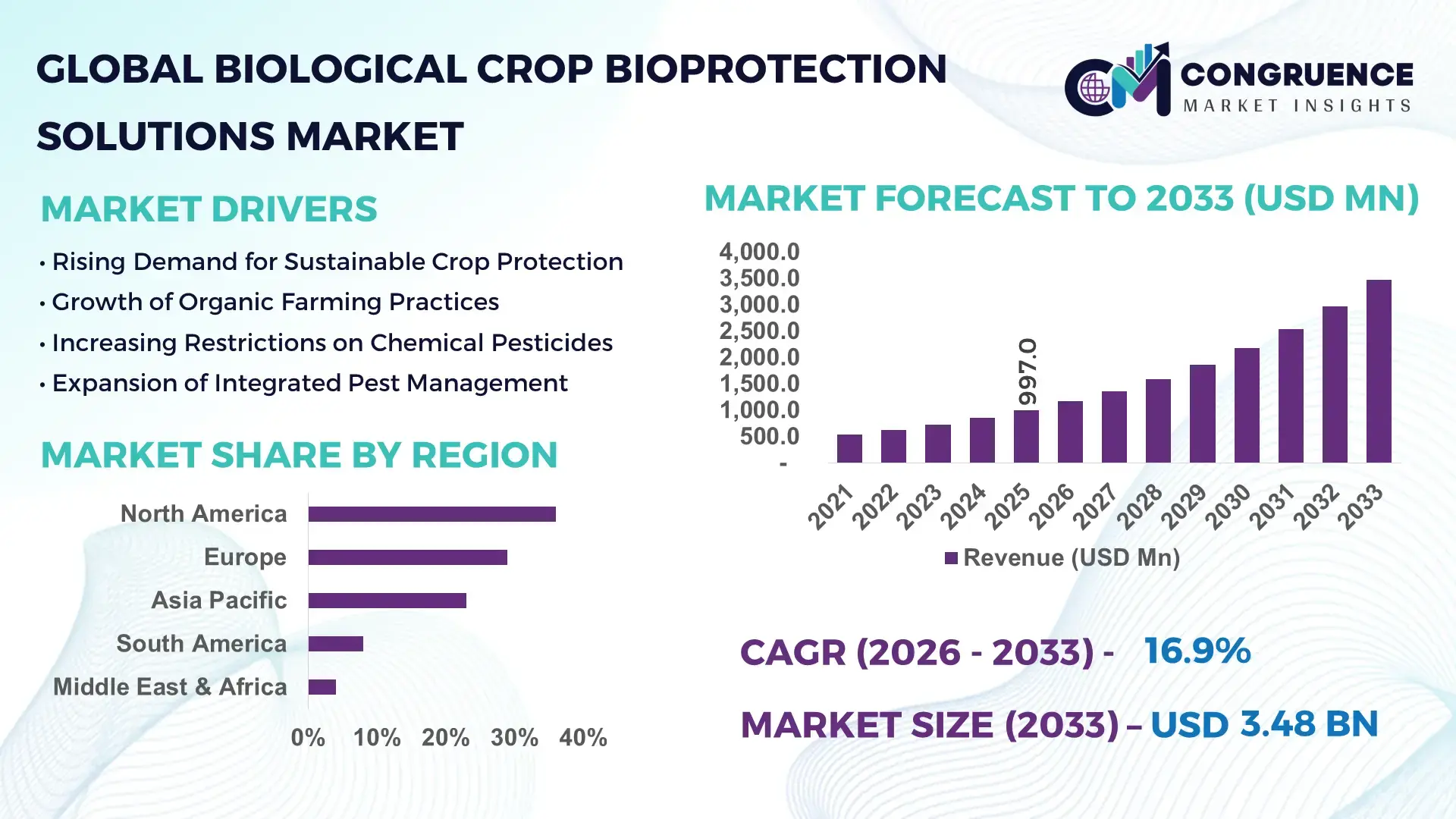

The Global Biological Crop Bioprotection Solutions Market was valued at USD 997.0 Million in 2025 and is anticipated to reach a value of USD 3,477.1 Million by 2033 expanding at a CAGR of 16.9% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by the rising adoption of sustainable farming practices and increasing regulatory restrictions on chemical pesticides worldwide.

The United States remains a major production and innovation hub in the Biological Crop Bioprotection Solutions Market, supported by advanced agricultural biotechnology infrastructure and strong investment in sustainable crop inputs. The country hosts more than 220 registered biological crop protection manufacturers and technology developers, supplying microbial pesticides, biofungicides, and plant-based bioinsecticides. Biological products account for nearly 28% of new crop protection product registrations in the U.S. agricultural sector, reflecting a significant shift toward eco-friendly solutions. The U.S. also invests heavily in agricultural biotechnology, with over USD 3 billion annually allocated to agricultural R&D programs, supporting microbial formulation research and fermentation-based production technologies. Adoption of biological crop protection solutions is particularly high in high-value crops such as fruits, vegetables, and specialty crops, where over 35% of growers report integrating biological pest control agents into integrated pest management (IPM) programs. Additionally, U.S. agricultural exports rely increasingly on residue-free production standards, accelerating the deployment of biological crop protection technologies across large-scale commercial farms.

Market Size & Growth: The market stood at USD 997.0 Million in 2025 and is projected to reach USD 3,477.1 Million by 2033, expanding at 16.9% CAGR, driven by growing regulatory pressure on chemical pesticides and increasing demand for residue-free agricultural products.

Top Growth Drivers: Organic farming adoption rising 22% globally, integrated pest management adoption improving farm productivity by 30%, and microbial pesticide efficiency increasing pest control success rates by 25%.

Short-Term Forecast: By 2028, biological crop protection adoption is projected to improve farm input efficiency by 18% while reducing chemical pesticide usage by nearly 20% in intensive agriculture regions.

Emerging Technologies: AI-driven crop monitoring, microbial fermentation optimization, and nano-encapsulation delivery systems are improving biological product stability and field efficacy.

Regional Leaders: North America projected to reach USD 1.2 Billion by 2033 driven by sustainable farming mandates; Europe expected to exceed USD 980 Million due to pesticide reduction targets; Asia Pacific forecast near USD 840 Million as organic farming acreage expands rapidly.

Consumer/End-User Trends: Commercial farmers and greenhouse operators represent nearly 60% of product usage, while adoption among organic growers has crossed 45% penetration in high-value crop cultivation.

Pilot or Case Example: In 2024, a large-scale microbial pesticide pilot program in Latin America improved pest suppression efficiency by 27% while lowering synthetic pesticide dependency by 21%.

Competitive Landscape: Bayer AG holds approximately 16% share, followed by Syngenta, BASF SE, Corteva Agriscience, and UPL Ltd., with strong investment in microbial and plant-derived formulations.

Regulatory & ESG Impact: Over 70 countries have introduced sustainable agriculture frameworks encouraging biological pesticides, while the EU aims to reduce chemical pesticide usage by 50% by 2030.

Investment & Funding Patterns: More than USD 1.8 Billion has been invested globally in biological crop protection startups and fermentation facilities over the past five years.

Innovation & Future Outlook: Synthetic biology, precision agriculture integration, and advanced microbial strain engineering are expected to significantly improve crop protection efficiency and sustainability outcomes.

Biological crop bioprotection solutions are gaining momentum across horticulture, cereals, and specialty crops, where sustainable pest management solutions are increasingly prioritized. Microbial-based biofungicides and bioinsecticides collectively contribute nearly 58% of total product adoption, while plant-extract-based solutions are emerging rapidly due to their compatibility with organic farming practices. Regulatory support for residue-free food production, expansion of organic farmland, and rising consumer demand for sustainable agriculture are accelerating innovation and commercialization across the sector.

The Biological Crop Bioprotection Solutions Market is becoming strategically significant as global agriculture transitions toward environmentally sustainable and regulatory-compliant crop protection methods. Governments and agricultural institutions worldwide are encouraging biological alternatives to conventional chemical pesticides in order to mitigate soil degradation, biodiversity loss, and chemical residue contamination in food supply chains. Biological crop protection solutions—particularly microbial bioinsecticides and plant-based biofungicides—are increasingly integrated into Integrated Pest Management (IPM) programs, which are currently used by more than 40% of commercial farming operations globally.

Technological innovation is further strengthening the strategic relevance of the market. Microbial fermentation technology delivers nearly 35% higher formulation stability compared to conventional microbial extraction methods, enabling longer shelf life and improved pest control efficacy. Additionally, nano-encapsulation delivery systems deliver 28% improvement in controlled release performance compared to traditional spray formulations, improving field effectiveness and reducing input waste.

Regional market development also highlights distinct adoption patterns. North America dominates in production volume, supported by extensive biotechnology infrastructure and large-scale fermentation facilities, while Europe leads in adoption with nearly 48% of agricultural enterprises integrating biological crop protection tools due to stringent pesticide reduction policies and sustainability mandates.

Short-term technology deployment is expected to accelerate operational efficiency. By 2028, AI-enabled precision agriculture platforms are expected to reduce pesticide application volumes by nearly 20%, enabling farmers to deploy biological crop protection agents more precisely based on pest detection analytics and satellite monitoring.

Environmental compliance and ESG commitments are also influencing industry adoption. Many agribusiness firms have pledged to achieve 30% reductions in synthetic pesticide usage by 2030, aligning with sustainability frameworks and responsible agriculture standards.

A measurable example of innovation occurred in 2024 when an agricultural biotechnology firm in the United States implemented AI-guided microbial formulation optimization, achieving a 22% improvement in pest control performance and a 17% reduction in field application frequency.

As sustainability regulations tighten and global food demand continues to rise, the Biological Crop Bioprotection Solutions Market is positioned to become a foundational pillar of resilient agricultural supply chains, enabling regulatory compliance, environmental stewardship, and long-term sustainable growth.

The Biological Crop Bioprotection Solutions Market is shaped by increasing pressure on the agricultural sector to reduce chemical pesticide usage while maintaining crop productivity and food security. Governments and environmental organizations worldwide are implementing stricter pesticide regulations to reduce soil and water contamination, which is accelerating the adoption of biological alternatives such as microbial pesticides, plant-derived compounds, and beneficial organisms. Farmers are also adopting integrated pest management practices that combine biological solutions with precision agriculture technologies to optimize pest control while minimizing ecological impact. Additionally, rising global demand for organic and residue-free food products is encouraging food producers and agribusiness companies to invest in biological crop protection technologies. Advances in microbial fermentation, biotechnology, and formulation science are improving the stability, shelf life, and field performance of biological crop protection products, making them increasingly viable alternatives to traditional pesticides. At the same time, expansion of organic farmland, increasing sustainability commitments by global food companies, and improvements in digital crop monitoring tools are collectively transforming the adoption landscape of biological crop bioprotection solutions across developed and emerging agricultural economies.

The rapid expansion of organic agriculture worldwide is significantly driving demand for biological crop bioprotection solutions. Organic farming standards prohibit the use of most synthetic pesticides, creating strong demand for biological pest management tools such as microbial biofungicides, bioinsecticides, and plant-derived crop protection agents. Globally, organic farmland has expanded to more than 75 million hectares, reflecting growing consumer demand for pesticide-free and environmentally sustainable food products. Biological crop protection products play a critical role in maintaining crop productivity in organic farming systems while preserving soil health and biodiversity. In high-value crops such as fruits, vegetables, and nuts, biological crop protection adoption has reached nearly 40% of pest management programs due to stricter export standards for pesticide residues. Furthermore, increasing awareness among farmers about long-term soil fertility and ecosystem preservation has strengthened the adoption of biological crop protection products in integrated pest management programs, especially in regions where chemical pesticide resistance has become a significant agricultural challenge.

Despite their environmental advantages, biological crop bioprotection solutions face technical limitations that restrict broader adoption. Many biological formulations rely on living microorganisms or natural compounds that can be sensitive to temperature fluctuations, ultraviolet exposure, and storage conditions. These factors can reduce product stability and effectiveness during transportation and field application. Compared with conventional chemical pesticides, biological formulations often require controlled storage temperatures between 4°C and 25°C, increasing logistics complexity and distribution costs. In addition, microbial products may demonstrate slower pest-control activity compared to chemical alternatives, which can discourage adoption among farmers managing severe pest outbreaks. Shelf life limitations also create supply chain challenges for agricultural distributors and retailers, particularly in developing markets with limited cold-chain infrastructure. Furthermore, inconsistent performance under varying environmental conditions such as humidity, soil composition, and crop varieties can influence farmer confidence in biological solutions, slowing large-scale adoption across some agricultural regions.

Precision agriculture technologies are creating substantial opportunities for the Biological Crop Bioprotection Solutions Market by enabling targeted and efficient pest management strategies. Technologies such as satellite imaging, drone-based crop monitoring, and AI-driven pest detection systems allow farmers to identify pest outbreaks early and deploy biological control agents precisely where needed. This targeted approach improves the effectiveness of biological crop protection products while reducing overall pesticide application volumes. In many advanced agricultural markets, over 30% of commercial farms now use precision agriculture tools, which increases compatibility with biological pest management strategies. Additionally, integration of digital crop monitoring with automated spraying equipment allows farmers to apply microbial pesticides with greater accuracy, improving pest suppression rates and minimizing product waste. Emerging technologies such as predictive pest modeling and climate-driven disease forecasting systems are also enabling agricultural producers to adopt proactive pest management approaches, which align well with biological crop protection solutions designed for preventive pest control.

Regulatory approval processes for biological crop protection products present a significant challenge for manufacturers and innovators in the industry. Although biological pesticides are generally considered safer than synthetic chemicals, they must still undergo extensive testing to demonstrate environmental safety, product efficacy, and non-toxicity to beneficial organisms such as pollinators. The approval process for new biological crop protection products can take three to five years in many jurisdictions, requiring detailed environmental risk assessments and field trials. Regulatory requirements vary significantly between regions, creating compliance complexity for companies seeking to commercialize products globally. For example, product registration standards in North America, Europe, and Asia often require separate testing procedures and documentation, increasing product development timelines and costs. Smaller biotechnology firms and startups often face financial and administrative barriers when navigating these regulatory frameworks, which can slow innovation and limit the introduction of new biological crop protection technologies into the market.

Rapid Expansion of Microbial Biofungicide Adoption: Microbial biofungicides are increasingly adopted as farmers seek alternatives to chemical fungicides in high-value crops. More than 46% of biological crop protection products introduced globally in recent years are microbial-based formulations. Agricultural trials demonstrate that microbial biofungicides can reduce fungal disease incidence by 30–40% in greenhouse vegetable cultivation. Adoption is particularly strong in Europe and North America where environmental regulations limit synthetic fungicide use. Additionally, advanced fermentation technology has improved microbial production yields by nearly 35%, enabling larger-scale commercial manufacturing and broader global distribution.

Growth of AI-Driven Precision Pest Monitoring: Digital agriculture technologies are transforming pest monitoring and crop protection strategies. AI-powered pest detection systems now analyze field images and satellite data to identify early pest infestations with over 90% detection accuracy. More than 32% of large commercial farms in technologically advanced agricultural regions have implemented digital pest monitoring tools integrated with biological crop protection deployment systems. These tools reduce pesticide application frequency by approximately 18% while improving targeted pest control outcomes across large agricultural fields.

Increasing Adoption in High-Value Specialty Crops: Biological crop bioprotection solutions are increasingly utilized in fruits, vegetables, and specialty crops where pesticide residue limits are strict. Nearly 52% of specialty crop growers have integrated at least one biological pest management product into their production systems. In greenhouse horticulture operations, biological pest control agents such as beneficial microbes and bioinsecticides have improved pest suppression rates by 25–30% while maintaining soil microbial diversity. These benefits are driving higher adoption in export-oriented agriculture sectors.

Expansion of Fermentation-Based Manufacturing Infrastructure: Industrial fermentation facilities dedicated to microbial pesticide production are expanding rapidly. Global agricultural biotechnology companies have increased microbial production capacity by over 40% in the past five years, enabling higher-volume production of bioinsecticides and biofungicides. New fermentation technologies improve microbial yield efficiency by around 33%, reducing manufacturing costs and improving product scalability. This expansion is enabling faster commercialization of new biological crop protection solutions across emerging agricultural markets.

The Biological Crop Bioprotection Solutions Market is segmented based on product type, application, and end-user groups, reflecting the diverse technological approaches and agricultural use cases across global farming systems. Biological crop protection solutions include microbial-based products, plant-derived compounds, and biochemical pest control agents that support environmentally sustainable crop protection strategies. Adoption varies across crop types and farming systems, with organic agriculture, greenhouse farming, and high-value crop cultivation driving the highest demand. Different biological product categories target specific pests, plant diseases, and nematodes, making segmentation essential for understanding market development patterns. Applications range from seed treatment and foliar spraying to soil treatment methods designed to improve crop resilience against pests and pathogens. End-user demand is influenced by farm size, crop specialization, and regulatory compliance requirements, particularly in regions where pesticide residue limits and sustainable agriculture policies are strongly enforced.

The Biological Crop Bioprotection Solutions Market includes bioinsecticides, biofungicides, bionematicides, and bioherbicides, each serving different pest management functions within agricultural systems. Biofungicides represent the leading segment with nearly 38% adoption, primarily because fungal diseases significantly impact crop yields in cereals, fruits, and vegetables. These products utilize beneficial microorganisms such as Bacillus and Trichoderma species to suppress fungal pathogens while maintaining soil microbiome balance. Bioinsecticides account for around 32% adoption, widely used to control insect pests such as aphids, caterpillars, and beetles. These products are particularly popular in organic agriculture where chemical insecticides are restricted. Bionematicides are the fastest-growing segment with an estimated 17.5% growth rate, driven by increasing nematode infestations in intensive farming systems and the need for environmentally safe soil treatment methods. Bioherbicides and other specialized biological pest control products collectively contribute around 30% of the remaining product adoption, targeting weed management and niche agricultural applications.

Biological crop bioprotection solutions are applied through foliar spray, seed treatment, and soil treatment methods, each suited for different pest management strategies. Foliar spray applications account for approximately 44% of product usage, as they provide direct protection against insect pests and fungal diseases affecting leaves, stems, and fruit surfaces. Seed treatment represents about 28% adoption, particularly in cereals and oilseed crops where biological seed coatings enhance early plant immunity and improve root health. Soil treatment is the fastest-growing application with an estimated 18.9% growth rate, driven by increasing awareness of soil-borne pathogens and nematode infestations that reduce crop productivity. These treatments utilize beneficial microorganisms to enhance soil microbial balance and plant resistance. Other applications, including post-harvest biological protection and greenhouse pest management, collectively account for around 28% of total application use cases. In 2025, over 36% of commercial farms globally reported experimenting with biological seed treatment products to reduce dependency on synthetic fungicides during early crop development.

End-users of biological crop bioprotection solutions include commercial agriculture farms, greenhouse operators, organic farms, and agricultural cooperatives. Large commercial farms represent the leading end-user group with approximately 48% adoption, as these operations increasingly integrate biological pest management solutions into integrated pest management programs to meet sustainability targets and export standards. Organic farms account for about 27% of product usage, driven by strict regulations prohibiting synthetic pesticides and increasing consumer demand for organic food products. Greenhouse and controlled-environment agriculture operators represent the fastest-growing end-user segment with an estimated 19.6% growth rate, supported by the need for residue-free pest control solutions in high-value horticulture crops such as tomatoes, cucumbers, and leafy vegetables. Agricultural cooperatives and regional farming organizations collectively contribute around 25% of remaining demand, often facilitating bulk procurement and shared adoption of biological crop protection technologies among smallholder farmers. In 2025, more than 41% of commercial greenhouse producers globally reported integrating biological pest management solutions into their crop protection programs to maintain pesticide-free cultivation environments.

North America accounted for the largest market share at 36% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.2% between 2026 and 2033.

The regional distribution of the Biological Crop Bioprotection Solutions Market reflects variations in agricultural practices, regulatory frameworks, and technology adoption levels. North America leads with approximately 36% share, supported by large-scale commercial farming and strong biotechnology infrastructure. Europe follows with nearly 29% market share, driven by strict pesticide reduction policies and increasing organic farmland exceeding 17 million hectares. Asia-Pacific represents around 23% of global demand, fueled by the region’s vast agricultural base exceeding 600 million hectares of cultivated land, particularly in China and India. South America contributes roughly 8% of total market share, with Brazil accounting for over 45% of the region’s biological crop protection consumption due to large soybean and corn cultivation areas exceeding 70 million hectares. The Middle East & Africa collectively account for about 4% market share, supported by expanding greenhouse farming and food security initiatives. Across all regions, biological crop protection adoption has grown significantly, with more than 42% of commercial farms globally incorporating at least one biological pest management tool into integrated pest management systems.

North America holds approximately 36% of the global Biological Crop Bioprotection Solutions Market, making it the largest regional contributor in terms of adoption and technological innovation. The United States and Canada are key drivers due to extensive commercial agriculture operations and strong agricultural biotechnology research ecosystems. The region cultivates more than 190 million hectares of farmland, with biological crop protection solutions increasingly integrated into integrated pest management programs. Key industries driving demand include grain production, specialty crops, horticulture, and greenhouse agriculture, particularly in fruits and vegetables where residue-free standards are critical. Regulatory support from agencies encouraging reduced pesticide dependency has accelerated the registration of microbial pesticides and plant-based pest control products. Technological advancements such as AI-based crop monitoring, drone-assisted biological spraying systems, and fermentation-based microbial production are widely implemented across large farms. A notable example is Corteva Agriscience, which continues to expand microbial crop protection product lines and digital crop monitoring tools to support sustainable agriculture initiatives. Consumer behavior trends indicate that growers increasingly prioritize sustainable farming certifications, with nearly 40% of commercial farms in the region integrating biological solutions into crop protection programs.

Europe accounts for approximately 29% of the global Biological Crop Bioprotection Solutions Market, driven by strong regulatory frameworks and environmental sustainability mandates. Major markets such as Germany, France, Italy, Spain, and the United Kingdom play a critical role in expanding biological crop protection adoption across large-scale farming operations and greenhouse horticulture sectors. The European Union’s agricultural sustainability initiatives, including pesticide reduction targets of 50% by 2030, are encouraging farmers to adopt biological alternatives such as microbial pesticides and plant-based biocontrol agents. The region cultivates more than 160 million hectares of farmland, with nearly 17 million hectares certified as organic agriculture, which significantly increases demand for biological crop protection products. European regulatory authorities emphasize sustainable pest management, accelerating the development and commercialization of biological solutions. Emerging technologies such as precision agriculture analytics, automated greenhouse pest monitoring systems, and advanced microbial fermentation platforms are improving pest control efficiency and product scalability. Local companies such as Koppert Biological Systems have expanded beneficial microorganism-based crop protection solutions, supporting greenhouse and specialty crop farming. Consumer behavior trends show strong preference for pesticide-free agricultural products, influencing farmers to integrate biological crop protection into nearly 45% of high-value crop cultivation systems.

Asia-Pacific ranks among the fastest-growing regions in the Biological Crop Bioprotection Solutions Market and represents approximately 23% of global demand. Major agricultural economies such as China, India, Japan, South Korea, and Australia are expanding biological crop protection adoption due to rising food demand and increasing environmental regulations. The region has more than 600 million hectares of agricultural land, accounting for nearly 40% of the world’s cultivated farmland, which creates substantial demand for sustainable pest control solutions. China and India together produce over 50% of the region’s fruits and vegetables, sectors where biological pest control adoption is growing rapidly. Agricultural modernization initiatives and government-backed sustainable farming programs are supporting the expansion of biological crop protection technologies. Manufacturing infrastructure for microbial pesticides is also increasing, with fermentation-based production capacity rising by more than 30% in the past five years. Companies such as UPL Ltd. are investing in biological product development and microbial fermentation facilities to support regional agricultural markets. Consumer behavior in this region is influenced by increasing demand for pesticide-free food and mobile-based digital agriculture tools, with over 35% of large farms now experimenting with precision agriculture technologies integrated with biological pest management solutions.

South America represents roughly 8% of the global Biological Crop Bioprotection Solutions Market, driven primarily by large-scale agricultural production in countries such as Brazil, Argentina, and Chile. Brazil is the dominant market in the region, contributing more than 45% of regional biological crop protection demand, supported by its extensive cultivation of soybeans, corn, sugarcane, and coffee. The region collectively manages over 200 million hectares of agricultural land, making pest management efficiency a critical priority for farmers. Biological crop protection solutions are increasingly used in soybean and maize production where pest resistance to chemical pesticides has become a major concern. Governments across the region are introducing agricultural sustainability programs and regulatory incentives that support the adoption of microbial pesticides and environmentally friendly pest control solutions. Infrastructure improvements in agricultural supply chains and biotechnology research facilities are also supporting product development. Regional companies such as Biotrop are expanding microbial-based biological crop protection products tailored for tropical agriculture. Consumer behavior trends show increasing demand for export-quality agricultural products with minimal pesticide residues, encouraging farmers to integrate biological crop protection into nearly 30% of commercial crop production programs.

The Middle East & Africa region accounts for approximately 4% of the global Biological Crop Bioprotection Solutions Market, but adoption is increasing due to food security initiatives and modernization of agricultural systems. Countries such as United Arab Emirates, Saudi Arabia, South Africa, and Kenya are investing in advanced agricultural technologies to improve crop productivity under challenging climate conditions. The region manages more than 120 million hectares of agricultural land, with increasing investment in greenhouse agriculture and controlled-environment farming systems. Biological crop protection solutions are gaining popularity in horticulture and greenhouse crop production where chemical pesticide use is restricted. Technological modernization initiatives such as precision irrigation systems, digital crop monitoring platforms, and climate-controlled greenhouse farming are improving compatibility with biological pest management strategies. Regional agritech startups and biotechnology firms are expanding local production of microbial pesticides and plant-based crop protection products. Consumer behavior trends show increasing demand for locally produced food and sustainable agriculture practices, particularly in urban farming projects where nearly 25% of greenhouse farms have started experimenting with biological pest control solutions.

United States – 31% Market Share: Dominance driven by advanced agricultural biotechnology infrastructure, large-scale commercial farming operations, and extensive adoption of integrated pest management practices utilizing biological crop protection solutions.

Germany – 12% Market Share: Leadership supported by strong regulatory push for pesticide reduction, large organic farming acreage, and high adoption of microbial biofungicides and biological pest control technologies.

The Biological Crop Bioprotection Solutions Market features a moderately fragmented competitive landscape, with more than 120 active global and regional companies engaged in microbial pesticide production, plant-based biopesticide development, and biological crop protection technologies. The top five companies collectively account for approximately 42% of the total market share, reflecting strong competition between multinational agrochemical companies and specialized biotechnology firms focused on sustainable agriculture solutions.

Major players are investing heavily in research and development, microbial fermentation facilities, and advanced formulation technologies to enhance the effectiveness and scalability of biological crop protection products. Strategic partnerships between biotechnology startups and established agricultural input companies have increased significantly, enabling faster commercialization of innovative biological pest control solutions. Over the past five years, more than 35 strategic collaborations and acquisitions have been recorded in the sector, primarily focused on microbial strain development, digital agriculture integration, and biological seed treatment technologies.

Product innovation is another key competitive factor. Companies are developing multi-strain microbial formulations capable of targeting multiple pest types simultaneously, improving field performance and reducing application frequency. Additionally, integration with AI-based crop monitoring and precision agriculture platforms is enabling companies to provide comprehensive pest management solutions rather than standalone crop protection products.

Regional competition dynamics also vary. North America and Europe host many large multinational players with strong biotechnology capabilities, while Asia-Pacific is witnessing rapid expansion of local manufacturers focusing on cost-effective microbial pesticide production. Increasing venture capital investments and government-backed agricultural sustainability initiatives are further encouraging innovation and market entry for emerging biological crop protection companies.

Syngenta AG

BASF SE

Corteva Agriscience

UPL Ltd.

Koppert Biological Systems

Valent BioSciences LLC

Marrone Bio Innovations

Certis Biologicals

Novozymes A/S

FMC Corporation

Isagro S.p.A.

Biotrop

Lallemand Plant Care

Technological advancements are significantly reshaping the Biological Crop Bioprotection Solutions Market, improving the effectiveness, scalability, and commercial viability of biological crop protection products. One of the most impactful technologies is microbial fermentation-based manufacturing, which enables large-scale production of beneficial microorganisms used in biofungicides, bioinsecticides, and bionematicides. Modern fermentation facilities are capable of producing microbial strains with up to 40% higher yield efficiency compared to earlier batch fermentation systems, allowing companies to scale production to meet growing agricultural demand.

Another critical innovation involves genomic sequencing and microbial strain engineering, enabling researchers to identify highly effective microorganisms capable of suppressing plant pathogens and pests. Advanced bioinformatics tools are helping scientists analyze microbial genomes and develop targeted biological pest control solutions optimized for specific crops and climatic conditions.

Nano-encapsulation technology is also gaining traction within the market. By encapsulating biological active ingredients in protective nano-carriers, manufacturers can improve product stability and extend shelf life under varying environmental conditions. Field trials indicate that nano-encapsulation techniques can enhance biological pesticide delivery efficiency by up to 28%, improving pest suppression rates and reducing application frequency.

Digital agriculture technologies are further enhancing biological crop protection strategies. AI-based pest monitoring systems, drone-assisted spraying equipment, and satellite-based crop analytics enable farmers to detect pest outbreaks early and apply biological control agents with greater precision. These technologies can reduce unnecessary pesticide applications by nearly 20%, improving both environmental sustainability and farm profitability.

Emerging innovations such as synthetic biology and microbial consortia formulations are also gaining attention. Instead of relying on a single microorganism, new biological crop protection products combine multiple beneficial microbial strains to provide broader pest suppression capabilities and improve crop resilience against diseases and environmental stress.

• In June 2025, Syngenta announced a major expansion of its global biologicals strategy and opened a 22,000 m² biologicals production facility in Orangeburg, South Carolina, capable of producing 16,000 tons of biostimulants annually, strengthening its manufacturing network for biological crop protection solutions worldwide. Source: www.syngenta.com

• In February 2025, Syngenta Crop Protection partnered with Ceres Biotics to globally expand access to VIXERAN®, a biological solution based on Azotobacter salinestris bacteria that helps crops utilize nitrogen more efficiently and supports sustainable farming practices.

• In July 2024, Syngenta Crop Protection collaborated with Ginkgo Bioworks to accelerate development of a new biological crop protection product by engineering microbial strains capable of producing targeted metabolites, using machine learning and advanced strain engineering to scale biological production.

• In February 2024, Syngenta and Lavie Bio announced a strategic partnership to develop novel bio-insecticides using microbiome-based discovery platforms and computational biology technologies aimed at improving pest control and combating insect resistance in crops.

The Biological Crop Bioprotection Solutions Market Report provides a comprehensive analysis of industry trends, technological developments, and strategic opportunities shaping the future of sustainable crop protection technologies. The report examines multiple product categories including biofungicides, bioinsecticides, bionematicides, and bioherbicides, which collectively support environmentally responsible pest management across global agricultural systems. These solutions are increasingly adopted across more than 75 million hectares of organic farmland and a growing portion of conventional commercial agriculture operations.

The study covers extensive segmentation across product types, applications, and end-user groups, providing detailed insights into how different biological crop protection technologies are utilized in modern farming practices. Applications evaluated include foliar spraying, seed treatment, and soil treatment, which are widely used in grain production, horticulture, greenhouse farming, and specialty crop cultivation.

Geographically, the report analyzes regional market developments across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 30 major agricultural economies. Each regional assessment evaluates factors such as agricultural production scale, regulatory frameworks, technological adoption levels, and sustainability initiatives influencing biological crop protection demand.

The report also evaluates the role of emerging technologies such as AI-driven precision agriculture, microbial fermentation, synthetic biology, and nano-encapsulation formulations, which are transforming biological crop protection product development and application strategies. Additionally, the study assesses evolving agricultural practices including integrated pest management programs, organic farming expansion, and sustainable agriculture policies implemented by governments and agribusiness organizations.

Overall, the report provides decision-makers with a detailed overview of industry developments, competitive dynamics, technological innovation trends, and strategic investment opportunities influencing the long-term evolution of the Biological Crop Bioprotection Solutions Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 997.0 Million |

| Market Revenue (2033) | USD 3,477.1 Million |

| CAGR (2026–2033) | 16.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Bayer AG; Syngenta AG; BASF SE; Corteva Agriscience; UPL Ltd.; Koppert Biological Systems; Valent BioSciences LLC; Marrone Bio Innovations; Certis Biologicals; Novozymes A/S; FMC Corporation; Isagro S.p.A.; Biotrop; Lallemand Plant Care |

| Customization & Pricing | Available on Request (10% Customization Free) |