Reports

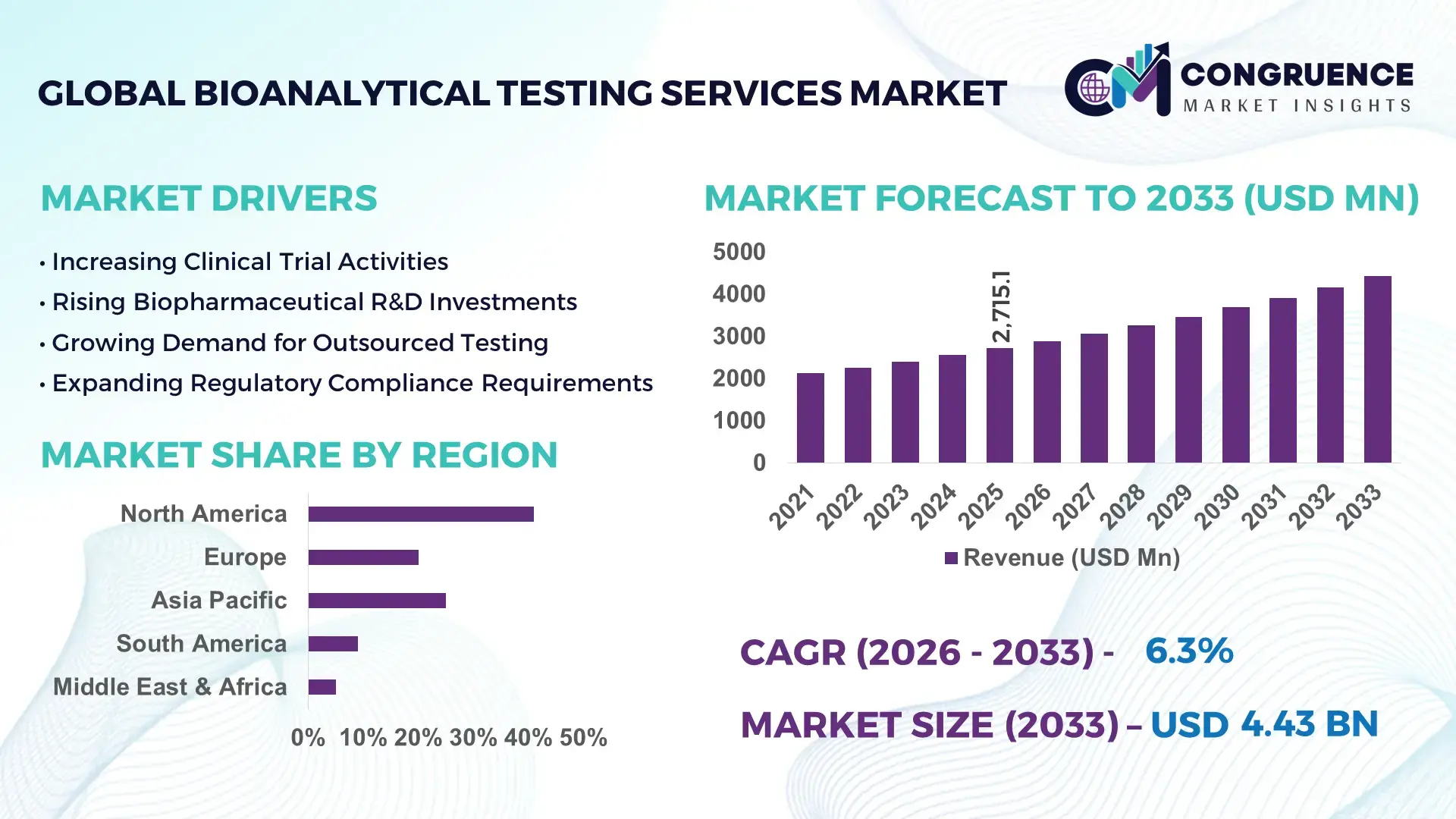

The Global Bioanalytical Testing Services Market was valued at USD 2715.08 Million in 2025 and is anticipated to reach a value of USD 4426.39 Million by 2033 expanding at a CAGR of 6.3% between 2026 and 2033. Increasing outsourcing of complex drug development analytics and growing biologics pipelines are accelerating demand for specialized bioanalytical testing services across regulated research environments.

The United States continues to represent the most advanced country in the Bioanalytical Testing Services landscape with extensive laboratory networks and large-scale drug development programs. The country operates more than 3,000 analytical and contract research laboratories engaged in pharmacokinetics, biomarker discovery, immunogenicity testing, and bioequivalence studies. Pharmaceutical research investment exceeds USD 200 billion annually, with a significant share directed toward clinical-stage bioanalysis and assay validation. More than 45% of active biologic drug trials are conducted in the United States, driving adoption of high-throughput LC-MS/MS systems, automated sample analysis platforms, and advanced biomarker testing technologies across oncology, metabolic disorders, and precision medicine research.

Market Size & Growth: Valued at USD 2715.08 Million in 2025 and projected to reach USD 4426.39 Million by 2033, expanding at a CAGR of 6.3% as pharmaceutical companies increasingly outsource regulated bioanalytical testing and biomarker validation to specialized laboratories.

Top Growth Drivers: Contract research outsourcing increased by 38%, biologics and biosimilar pipeline expansion reached 41%, and analytical platform productivity improved by 29% across clinical testing facilities.

Short-Term Forecast: By 2028, automated bioanalytical workflows are expected to reduce laboratory processing costs by 18% while improving sample throughput efficiency by approximately 24%.

Emerging Technologies: High-resolution mass spectrometry platforms, AI-assisted biomarker analytics, and automated robotic sample preparation technologies are transforming modern bioanalytical testing capabilities.

Regional Leaders: North America projected to approach USD 1.9 Billion by 2033 with strong clinical trial density; Europe expected to exceed USD 1.3 Billion driven by regulated bioequivalence studies; Asia-Pacific forecast near USD 0.9 Billion supported by expanding CRO infrastructure.

Consumer/End-User Trends: Pharmaceutical companies contribute around 52% of demand, biotechnology firms approximately 34%, while academic and clinical research organizations account for nearly 14% of service utilization globally.

Pilot or Case Example: In 2024, an automated clinical bioanalysis deployment improved analytical throughput by 31% and reduced laboratory turnaround delays by about 22% in large-scale pharmacokinetic testing programs.

Competitive Landscape: Leading provider holds nearly 14% of the market, followed by several global contract research organizations and specialized bioanalytical service providers competing through advanced assay development and global laboratory expansion.

Regulatory & ESG Impact: Updated bioanalytical method validation guidelines, strengthened regulatory oversight for clinical bioanalysis, and sustainability initiatives in laboratory operations are shaping procurement and compliance strategies.

Investment & Funding Patterns: More than USD 1.2 Billion has recently been invested in analytical infrastructure, advanced instrumentation, and expansion of global bioanalytical laboratory networks.

Innovation & Future Outlook: Integration of digital laboratory ecosystems, multiplex biomarker assays, and decentralized clinical trial testing models is expected to accelerate drug development and enhance data reliability.

The Bioanalytical Testing Services market is influenced by strong demand from pharmaceutical development, biosimilar manufacturing, biologics testing, and emerging cell and gene therapy programs. Pharmaceutical companies contribute roughly half of global testing demand, while biotechnology innovators account for more than one-third of analytical service utilization. Advancements in ultra-sensitive ligand binding assays, automated bioanalysis systems, and integrated data analytics platforms are improving testing accuracy and regulatory compliance. Increasing clinical trial volumes, evolving regulatory standards, and expanding precision medicine programs are driving regional adoption, particularly across North America, Europe, and rapidly developing Asia-Pacific research hubs. Emerging trends include decentralized clinical testing, biomarker-driven research models, and next-generation analytical platforms designed for complex therapeutic molecules.

The Bioanalytical Testing Services Market holds strategic importance in modern pharmaceutical and biotechnology development because it enables accurate measurement of drug concentration, biomarker validation, and regulatory compliance throughout clinical research. Global drug development pipelines currently include more than 20,000 active clinical trials involving biologics, biosimilars, and advanced therapies, all of which require validated bioanalytical testing frameworks. Contract research organizations are expanding high-capacity laboratories capable of processing more than 1.5 million biological samples annually, strengthening scalability for large multi-site trials and complex pharmacokinetic studies.

Technological modernization is redefining laboratory productivity and precision across bioanalysis platforms. High-resolution mass spectrometry delivers 35% improvement in analytical sensitivity compared to traditional immunoassay-based quantification standards. North America dominates in volume due to its dense clinical research ecosystem, while Asia-Pacific leads in adoption with nearly 42% of emerging biotechnology enterprises integrating outsourced bioanalytical services into early-stage drug development workflows. These patterns are reshaping competitive strategies, encouraging global CRO expansion and cross-border laboratory collaborations.

Digital transformation is accelerating operational efficiency and regulatory readiness. By 2028, AI-driven laboratory informatics and automated sample tracking systems are expected to improve data processing accuracy by 28% and reduce analytical turnaround time significantly in large-scale clinical programs. Sustainability initiatives are also influencing laboratory operations, with firms committing to ESG targets such as 30% reduction in laboratory solvent waste and 20% energy efficiency improvements by 2030 through green chemistry and automated instrumentation.

The rapid expansion of biologics, biosimilars, and advanced therapeutic molecules is significantly increasing demand for sophisticated bioanalytical testing services. Biologic drugs now represent over 40% of clinical development pipelines globally, requiring complex ligand binding assays, immunogenicity testing, and pharmacokinetic analysis. More than 5,000 biologic drug candidates are currently under development, each requiring validated analytical studies throughout clinical phases. Biosimilar development programs have also increased, particularly in Europe and Asia, where regulatory frameworks support comparative bioanalytical testing. Large pharmaceutical companies are outsourcing approximately 60% of early-phase bioanalysis to specialized laboratories to improve efficiency and maintain compliance with evolving validation standards. These trends are expanding the need for high-throughput analytical platforms and expert contract research capabilities.

Strict global regulatory expectations for bioanalytical method validation, data integrity, and clinical documentation create operational complexity for laboratories and service providers. Regulatory frameworks require extensive assay validation procedures, stability testing, and reproducibility verification before results can be accepted in regulatory submissions. Many bioanalytical laboratories must upgrade instrumentation and quality systems to meet compliance guidelines, increasing operational burden. In addition, maintaining Good Laboratory Practice (GLP) and clinical data management standards requires continuous training and infrastructure investment. Smaller laboratories often face difficulties scaling operations while meeting these requirements, which can delay project timelines. Regulatory audits and documentation processes also extend the duration of testing programs, limiting rapid deployment of new analytical technologies within regulated clinical environments.

Precision medicine initiatives and biomarker-driven clinical studies are creating substantial opportunities for specialized bioanalytical testing services. More than 70% of oncology trials now incorporate biomarker analysis to guide patient selection and treatment evaluation. This trend is increasing demand for advanced biomarker assays, genomic testing integration, and multi-analyte bioanalysis platforms. The expansion of cell and gene therapy programs is also generating new testing requirements for viral vectors, gene expression markers, and immune response monitoring. Pharmaceutical developers are investing heavily in personalized medicine trials that require high-sensitivity assays capable of detecting extremely low biomolecule concentrations. Additionally, emerging biotechnology companies are partnering with contract laboratories that provide integrated pharmacokinetic and biomarker testing capabilities, opening new avenues for specialized service expansion.

Bioanalytical laboratories require highly specialized instruments such as liquid chromatography-mass spectrometry systems, automated sample handling robotics, and advanced biomarker detection platforms, which involve significant acquisition and maintenance costs. High-precision analytical equipment can require regular calibration, compliance monitoring, and skilled personnel training to ensure accurate results. Laboratory infrastructure must also support secure data management systems and temperature-controlled sample storage facilities capable of handling thousands of biological samples simultaneously. Additionally, increasing clinical trial complexity requires multi-site coordination and standardized testing protocols, which can raise operational overhead. The shortage of experienced bioanalytical scientists and regulatory specialists further intensifies the challenge of maintaining quality standards while expanding laboratory capacity.

• Expansion of Automated High-Throughput Bioanalysis Platforms: Laboratories adopting robotic sample preparation and automated analytical systems have improved testing throughput by nearly 32% while reducing manual processing errors by approximately 18%. Over 60% of large contract research laboratories have integrated automation technologies to handle rising clinical trial sample volumes efficiently.

• Increasing Adoption of Biomarker-Driven Clinical Trials: Biomarker-based testing has grown rapidly, with nearly 68% of oncology trials incorporating biomarker analysis. Advanced ligand binding assays and multiplex biomarker platforms are improving detection sensitivity by around 27%, enabling more precise evaluation of targeted therapies and personalized treatment strategies.

• Growth of Outsourced Bioanalytical Services by Biotechnology Firms: Biotechnology startups now account for nearly 34% of outsourced bioanalytical testing demand, reflecting increasing reliance on external laboratories for pharmacokinetic analysis, immunogenicity testing, and assay validation. Outsourcing has improved project completion efficiency by roughly 25% in early-phase drug development programs.

• Digital Laboratory Integration and Data Management Transformation: More than 50% of bioanalytical laboratories have implemented digital laboratory information management systems, improving data traceability and compliance monitoring by about 30%. Integration of AI-based analytics and cloud-enabled platforms is strengthening clinical research coordination and accelerating regulatory documentation workflows.

The Bioanalytical Testing Services Market is segmented based on service types, application areas, and end-user categories, reflecting the diverse analytical requirements across pharmaceutical research, biotechnology development, and clinical trial ecosystems. In terms of service types, pharmacokinetic and bioequivalence testing, biomarker analysis, and immunogenicity assessments form the core analytical segments supporting drug development and regulatory approval processes. Application-wise segmentation highlights extensive use in clinical trials, biologics development programs, and therapeutic drug monitoring, where accurate bioanalysis is essential for evaluating safety and efficacy. From an end-user perspective, pharmaceutical companies and biotechnology firms represent the primary demand centers, supported by increasing outsourcing of specialized laboratory services. More than 60% of late-stage clinical trials now involve complex biomarker or pharmacokinetic evaluations, demonstrating how segmentation is directly aligned with evolving drug discovery pipelines, regulatory expectations, and precision medicine initiatives across global research hubs.

Bioanalytical testing services are categorized into pharmacokinetic testing, bioavailability and bioequivalence studies, biomarker testing, immunogenicity testing, and other specialized analytical services such as cell and gene therapy bioanalysis. Pharmacokinetic testing currently accounts for approximately 38% of adoption due to its critical role in measuring drug absorption, metabolism, distribution, and elimination during clinical development. Bioavailability and bioequivalence testing holds nearly 27%, reflecting growing demand for generic drug approvals and comparative studies required by regulatory authorities. However, biomarker testing is rising fastest, expanding at an estimated CAGR of about 8.1% as precision medicine programs and targeted therapies increasingly rely on biomarker-driven data for clinical validation. Immunogenicity testing and specialized therapeutic analysis collectively represent around 35% of the remaining service demand, supporting biologics safety monitoring and advanced therapy assessments.

Clinical trials remain the leading application area within the Bioanalytical Testing Services Market, accounting for roughly 46% of total adoption because every investigational drug must undergo detailed pharmacokinetic and safety analysis across multiple trial phases. Drug discovery and early-stage research activities represent approximately 29% of the application share, reflecting increasing collaboration between biotechnology firms and contract research laboratories. However, biologics and biosimilar development is the fastest-growing application segment, expanding at an estimated CAGR of about 8.5% due to the rapid expansion of monoclonal antibodies, gene therapies, and advanced biologic formulations entering regulatory pathways. Other applications, including therapeutic drug monitoring, toxicology research, and biomarker-guided diagnostics, collectively contribute around 25% of market utilization, particularly in specialized therapeutic areas such as oncology, autoimmune diseases, and rare genetic disorders.

Pharmaceutical companies represent the largest end-user segment in the Bioanalytical Testing Services Market, accounting for approximately 52% of total adoption because of their extensive involvement in drug discovery, clinical trials, and regulatory submissions requiring validated analytical testing. Biotechnology firms follow with nearly 31% of utilization, reflecting their increasing reliance on contract laboratories for specialized assays and biomarker analysis. However, adoption among emerging biotech startups and advanced therapy developers is growing fastest, expanding at an estimated CAGR of around 9.2% as innovation in gene therapy, RNA-based therapeutics, and personalized medicine continues to accelerate. Other end-users, including academic research institutes, government laboratories, and clinical research organizations, collectively contribute roughly 17% of demand, often focusing on translational research and collaborative clinical programs.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2026 and 2033.

The Bioanalytical Testing Services Market shows clear regional concentration supported by clinical research density and biotechnology investments. North America processes nearly 50% of global clinical trial samples through more than 3,500 advanced bioanalytical laboratories. Europe contributes about 27% of testing demand, supported by over 1,500 regulated analytical facilities focusing on biosimilar and pharmacokinetic studies. Asia-Pacific represents close to 22% of the global market with more than 6,000 active clinical trials across China, India, and Japan. South America and the Middle East & Africa together account for nearly 10%, driven by expanding biomedical infrastructure and multinational drug development programs.

How Is Advanced Clinical Research Infrastructure Increasing Demand for Analytical Testing Services?

North America holds approximately 41% of the Bioanalytical Testing Services Market volume, supported by large pharmaceutical pipelines and extensive clinical trial activity. More than 55% of global late-stage clinical studies are conducted in this region, increasing demand for pharmacokinetic and biomarker testing. Over 3,500 laboratories operate across the United States and Canada with high-throughput LC-MS/MS systems capable of processing thousands of samples weekly. Regulatory requirements for validated bioanalytical methods are strengthening testing demand. Digital laboratory management platforms are implemented in nearly 60% of contract research facilities, improving compliance and data accuracy. A regional contract research organization recently expanded capacity to handle over 200,000 additional clinical samples annually. Consumer behavior shows strong adoption among pharmaceutical enterprises and biotechnology innovators outsourcing analytical workflows.

What Regulatory and Innovation Factors Are Strengthening Demand for Advanced Bioanalytical Testing?

Europe accounts for nearly 27% of the Bioanalytical Testing Services Market, with Germany, the United Kingdom, and France leading regional clinical research activity. The region hosts more than 1,500 bioanalytical laboratories supporting pharmacokinetic studies, biomarker analysis, and bioequivalence testing. Strict drug evaluation frameworks encourage pharmaceutical companies to rely on validated analytical testing services. Sustainability initiatives have helped reduce laboratory solvent consumption by about 22% in multiple research facilities adopting green analytical techniques. Automation technologies have increased sample processing efficiency by nearly 25% across several contract laboratories. A European research organization recently expanded biologics testing programs covering over 90 multinational clinical development projects. Consumer behavior indicates strong preference for highly regulated, traceable testing frameworks among pharmaceutical and biosimilar developers.

Why Are Expanding Clinical Trials and Biotechnology Investments Accelerating Analytical Testing Demand?

Asia-Pacific represents about 22% of the Bioanalytical Testing Services Market and ranks among the fastest-expanding regions in testing activity. China, India, and Japan together contribute more than 70% of regional bioanalytical testing demand. Over 6,000 clinical trials are actively conducted in the region, especially in oncology and rare disease research. Governments are investing in biomedical parks and laboratories capable of processing more than 500,000 biological samples annually. Advanced analytical technologies such as AI-supported laboratory systems are improving testing accuracy by nearly 20%. A regional research institute recently launched a bioanalytical center equipped with high-resolution mass spectrometry systems to support multinational drug trials. Consumer behavior shows strong growth among biotechnology startups and contract research organizations seeking scalable analytical services.

How Are Expanding Pharmaceutical Research Programs Supporting Regional Analytical Testing Demand?

South America accounts for roughly 6% of the Bioanalytical Testing Services Market, with Brazil and Argentina representing the main clinical research hubs. More than 350 active clinical research sites operate across Brazil, requiring pharmacokinetic and bioequivalence testing for generic and biosimilar drug approvals. Investments in biomedical laboratories and healthcare innovation programs are strengthening regional analytical capacity. Automated laboratory systems have improved sample analysis efficiency by around 18% across several research institutions. Pharmaceutical companies are increasingly outsourcing bioanalytical services to specialized facilities to meet regulatory requirements. A regional research institute recently expanded clinical testing infrastructure to support multicenter drug development studies. Consumer behavior indicates growing demand from pharmaceutical manufacturers focusing on compliance and clinical trial efficiency.

What Role Do Emerging Biomedical Hubs Play in Expanding Analytical Testing Capabilities?

The Middle East & Africa region contributes nearly 4% of the Bioanalytical Testing Services Market and is expanding gradually through healthcare infrastructure development. Countries such as the United Arab Emirates and South Africa are strengthening biomedical research capabilities with more than 120 modern laboratories supporting clinical testing programs. Government initiatives promoting biotechnology development and international research partnerships are encouraging adoption of advanced bioanalytical technologies. Digital laboratory systems and automated sample analysis platforms are improving testing efficiency across hospitals and research institutions. A biomedical research center recently launched a specialized facility designed to process thousands of oncology trial samples annually. Consumer demand in the region is growing among hospitals, research institutes, and pharmaceutical distributors seeking reliable bioanalytical validation.

United States – Holds approximately 38% share in the Bioanalytical Testing Services Market due to strong pharmaceutical R&D infrastructure and large-scale clinical trial activity.

China – Accounts for nearly 14% share in the Bioanalytical Testing Services Market supported by expanding biotechnology research programs and increasing clinical development projects.

The Bioanalytical Testing Services market is moderately fragmented, with more than 120 active global and regional service providers operating specialized laboratories for pharmacokinetic testing, biomarker analysis, immunogenicity studies, and bioequivalence research. The top five companies collectively account for nearly 36% of the overall market presence, reflecting a competitive environment where both global contract research organizations and niche analytical specialists compete through technology, capacity expansion, and integrated clinical research solutions. Leading firms are investing heavily in high-throughput LC-MS/MS platforms, automated bioanalytical workflows, and AI-enabled laboratory data management systems capable of improving sample processing efficiency by 25% to 30%. Over the past three years, more than 40 strategic collaborations and laboratory expansion projects have been announced to strengthen global testing capacity. Mergers and acquisitions are also shaping the competitive landscape, with several contract research organizations acquiring smaller bioanalytical labs to expand regional coverage. Additionally, many companies are establishing multi-site laboratory networks capable of processing more than 1 million biological samples annually to support global clinical trials and complex biologics development programs.

Laboratory Corporation of America Holdings

Eurofins Scientific

SGS SA

Charles River Laboratories

Intertek Group plc

Syneos Health

Pace Analytical Services

WuXi AppTec

Frontage Laboratories

Medpace Holdings Inc.

Toxikon Corporation

BioAgilytix Labs

Technological transformation is significantly reshaping laboratory efficiency, analytical precision, and regulatory compliance in the Bioanalytical Testing Services Market. Advanced liquid chromatography–mass spectrometry (LC-MS/MS) platforms are widely deployed across more than 70% of large bioanalytical laboratories due to their ability to detect compounds at picogram-level sensitivity and process thousands of biological samples weekly. High-resolution mass spectrometry systems now enable multi-analyte detection in a single run, improving analytical throughput by nearly 30% compared with earlier-generation instruments. Automated sample preparation robotics are also expanding rapidly, reducing manual processing errors by about 20% while increasing laboratory productivity in large-scale clinical programs.

Artificial intelligence and machine learning technologies are becoming integral components of digital bioanalysis workflows. AI-enabled data analytics tools are capable of reviewing large pharmacokinetic datasets containing millions of analytical data points, accelerating validation and quality control processes. More than 50% of global contract research laboratories have adopted laboratory information management systems integrated with AI-based anomaly detection, which enhances regulatory compliance and reduces data review time by roughly 25%. Cloud-based laboratory infrastructure is further supporting secure cross-border collaboration among clinical research organizations, pharmaceutical companies, and biotechnology developers.

Emerging technologies such as multiplex biomarker assays, microfluidic testing platforms, and next-generation ligand-binding assays are expanding testing capabilities for complex biologics and gene therapies. Multiplex immunoassay platforms can measure over 40 biomarkers simultaneously from a single sample, improving efficiency in precision medicine research. Additionally, automated bioanalytical laboratories are implementing digital twin simulations to optimize testing workflows and predict instrument performance, enabling operational efficiency improvements exceeding 15% across high-volume clinical testing facilities.

• In March 2025, Eurofins Scientific expanded its global bioanalytical laboratory network by adding advanced LC-MS/MS platforms and increasing biologics testing capacity across multiple facilities. The expansion improved high-throughput pharmacokinetic testing capabilities and strengthened support for complex biologic and biosimilar clinical studies. Source: www.eurofins.com

• In September 2024, Charles River Laboratories announced the expansion of its biologics testing services and advanced analytical capabilities for cell and gene therapy development. The initiative enhanced specialized biomarker and immunogenicity testing workflows, supporting growing demand from biotechnology companies conducting complex therapeutic research. Source: www.criver.com

• In May 2024, WuXi AppTec strengthened its bioanalytical testing infrastructure by launching new laboratory capabilities focused on large-molecule analysis and advanced biomarker assays. The expansion improved integrated clinical research services and increased capacity to process thousands of biological samples for multinational trials. Source: www.wuxiapptec.com

• In February 2025, SGS expanded its life sciences laboratory services with upgraded bioanalytical testing technologies designed for pharmacokinetic and bioequivalence studies. The upgrade enhanced analytical accuracy and increased testing throughput for pharmaceutical and biotechnology clients conducting regulated clinical development programs. Source: www.sgs.com

The Bioanalytical Testing Services Market Report provides a comprehensive examination of global laboratory testing services supporting pharmaceutical, biotechnology, and clinical research industries. The report covers detailed segmentation across service types such as pharmacokinetic testing, biomarker analysis, bioavailability and bioequivalence studies, immunogenicity testing, and specialized bioanalysis for biologics, gene therapies, and advanced therapeutics. These segments collectively support thousands of ongoing clinical development programs worldwide, including more than 20,000 active clinical trials involving novel drug candidates and targeted therapies.

Geographically, the report evaluates market activity across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with analysis of regional laboratory capacity, clinical trial distribution, and research infrastructure. More than 5,000 specialized laboratories globally contribute to bioanalytical research supporting multinational drug development programs. The report also highlights application-specific insights covering clinical trial support, early-stage drug discovery, therapeutic drug monitoring, toxicology analysis, and biomarker-based research initiatives.

Technological coverage within the report includes advanced analytical platforms such as LC-MS/MS systems, automated sample preparation robotics, AI-enabled laboratory informatics, multiplex biomarker testing technologies, and digital data management frameworks used in regulated clinical environments. Additionally, the report assesses end-user demand across pharmaceutical companies, biotechnology firms, contract research organizations, and academic research institutes that collectively drive global testing volumes. Emerging niche segments such as precision medicine bioanalysis, cell and gene therapy testing, and integrated biomarker validation are also examined to provide a forward-looking perspective for decision-makers and industry stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Laboratory Corporation of America Holdings, Eurofins Scientific, SGS SA, Charles River Laboratories, Intertek Group plc, Syneos Health, Pace Analytical Services, WuXi AppTec, Frontage Laboratories, Medpace Holdings Inc., Toxikon Corporation, BioAgilytix Labs |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |