Reports

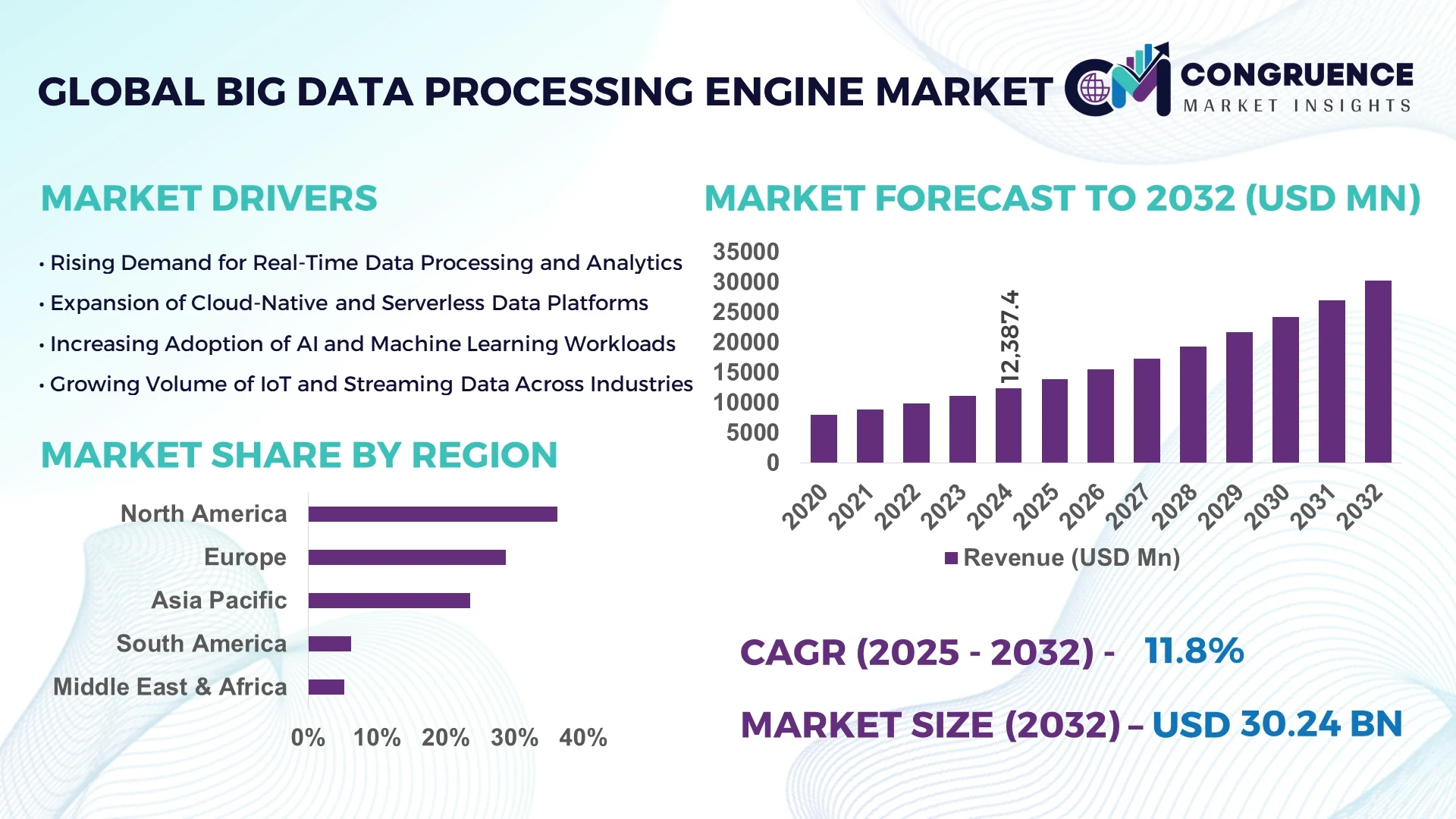

The Global Big Data Processing Engine Market was valued at USD 12,387.4 Million in 2024 and is anticipated to reach a value of USD 30,235.3 Million by 2032 expanding at a CAGR of 11.8% between 2025 and 2032. This growth is driven by surging demand for real-time analytics and scalable data architectures across enterprises.

In the United States, strong investment in cloud infrastructure and advanced analytics has fueled widespread adoption: over 60% of Fortune 500 firms use managed big data engines across multiple cloud providers. Major tech hubs in California, Texas, and Virginia host large clusters of processing engine deployments, and government funds support high-performance computing procurement. U.S. research institutions deploy in-house big data engine clusters exceeding 100 petaflops, and federal AI/data programs allocated more than USD 2.3 billion toward compute & data platforms in 2024.

Market Size & Growth: Current market value USD 12,387.4 M; projected to USD 30,235.3 M; CAGR ~11.8 %; driven by growth in real-time analytics and multi-cloud data processing.

Top Growth Drivers: Adoption of streaming data pipelines (38 %), demand for low-latency processing (27 %), growth in IoT/edge data influx (22 %).

Short-Term Forecast: By 2028, organizations expect latency reduction of 25 % and throughput improvement of 18 %.

Emerging Technologies: Serverless processing engines, GPU-accelerated analytics, hybrid CPU/TPU streaming pipelines.

Regional Leaders: North America projected USD 11,200 M by 2032 (strong enterprise base), Asia-Pacific USD 9,000 M (rapid digitalization), Europe USD 6,800 M (compliance focus).

Consumer/End-User Trends: Major users include finance, telecom, e-commerce; rising adoption of on-demand processing as a service.

Pilot or Case Example: In 2025, a U.S. bank reduced risk-scoring latency by 30 % via a real-time processing engine pilot across 12 data centers.

Competitive Landscape: Market leader holds ~20 % share; other major players include cloud vendors, open-source platforms, enterprise software firms.

Regulatory & ESG Impact: Data residency laws, privacy regulations, incentives for green data centers affect adoption.

Investment & Funding Patterns: Over USD 900 M in funding for processing engine startups in 2023–24; rising use of usage-based licensing.

Innovation & Future Outlook: Federated processing, cross-cloud engine orchestration, integration with AI model serving shaping future deployments.

Big data processing engines are critical in sectors like finance, telecom, retail, and manufacturing. Innovations include stream-join optimizers, adaptive query planners, GPU/TPU acceleration, and autoscaling engine clusters. Regulatory drivers include data sovereignty and privacy laws; economic drivers include rising data volumes and demand for insights. Regional adoption is highest in North America and Asia Pacific, with Latin America and MEA emerging. Future trends emphasize intelligent orchestration, edge-cloud interoperability, and AI-native processing.

Big data processing engines are strategically central for enterprises seeking real-time insights, scalable computation, and competitive edge. Organizations deploy advanced engines to process streaming logs, user behavior, and IoT data at scale. For instance, vector engine execution delivers ~40 % improvement compared to earlier row-based processing. North America dominates in volume deployments, while Asia-Pacific leads adoption depth—over 55 % of enterprises in Singapore and South Korea integrate real-time engines. Over the next 2–3 years, by 2027, hybrid multi-cloud orchestration is expected to cut total query latency by 22 %. Firms are committing to energy efficiency: some pledge 15 % reduction in processing energy per query by 2030. In 2024, a European telecom operator achieved 28 % reduction in stream query failure rates by porting to a new engine with adaptive backpressure. The Big Data Processing Engine Market will evolve as a pillar of resilience, regulatory compliance, and sustainable digital transformation across industries.

The big data processing engine market is shaped by escalating data volumes from IoT, AI, and digital services. Demand for low-latency stream processing, hybrid cloud architectures, and elastic scalability drives adoption. Engines must integrate with data lakes, message queues, and ML pipelines. Technological progress in vectorized execution, incremental computing, and cost-based optimizers influences differentiation. The competitive environment sees open-source, cloud-native, and proprietary engines competing. Governance, data security, and compliance requirements (e.g., data locality, encryption) affect deployment choices. Budget constraints, talent gaps, and inertia in legacy systems moderate adoption among mid-tier firms. Cloud providers offering managed engines also push the market toward abstraction and platform-as-a-service models.

Real-time analytics require engines capable of processing streaming events with minimal delay. Industries such as finance, telecom, and ad tech use engines to detect fraud, monitor network events, or personalize experience in milliseconds. Organizations piloting streaming pipelines have reported up to 35 % lower decision lag compared to batch-only systems. The pressure to ingest and analyze high-velocity data from sensors, clickstreams, and logs compels adoption of robust processing engines.

Sophisticated engines require skilled engineers for tuning, scaling, and debugging. Operational management of distributed clusters adds burden. Many organizations face high infrastructure cost, licensing, and training overhead. Integration with legacy ETL systems and data warehouses can prove difficult. Some firms hesitate due to risks in joining open architecture or migrating from older frameworks.

Engine vendors can differentiate by tailoring engines for specific verticals like ad tech, real-time finance, genomics, or media streaming. For example, engines that specialize in event time joins or time-series optimizations can appeal strongly in telecom or IoT sectors. Also, embedding ML inference within processing pipelines opens new product models. Regions with underserved sectors (Latin America, MEA) present growth potential.

Data residency, encryption, anonymization, and audit requirements complicate engine design. Some jurisdictions require query logs not leave local clusters, restricting cross-cloud processing. Ensuring secure inter-node communication and role-based access in multi-tenant engines is complex. Changes in privacy law (e.g. stricter data access rules) may force re-architecture.

• Rise of Serverless Event Engines: More organizations adopt serverless processing engines which auto-scale per event. In recent deployments, usage-based serverless models have reduced idle compute by over 50 %, enabling cost efficiency and agility.

• GPU/TPU-Accelerated Query Execution: Engines incorporating GPU or TPU offload vector-intensive join and aggregation workloads. Benchmarks in 2024 show up to 12× speedups in analytics queries relative to CPU-only modes.

• Hybrid Edge-to-Cloud Execution: Emerging engines support partitioned execution: partial processing at edge nodes, final aggregation in cloud. Over 28 % of new IoT systems in 2025 adopt this hybrid pattern to reduce bandwidth and latency.

• Native AI/ML Inference Pipelines: Processing engines increasingly embed model inference, enabling real-time scoring alongside aggregation. In 2024 pilot tests, embedded inference reduced data transfer overhead by 18 % while serving predictions directly.

The big data processing engine market segments by type (batch engines, streaming engines, hybrid engines, in-memory engines), deployment model (on-premises, cloud-managed, hybrid), application (ETL, analytics, stream processing, real-time dashboards), and end-user (finance, telecom, retail, healthcare, ad tech, IoT). Batch engines remain foundational in data warehousing, while streaming and hybrid types gain traction for real-time needs. Cloud-managed offerings appeal to enterprises seeking ease of deployment and scalability. End-users in finance, telecom, and ad tech are heavy consumers, while manufacturing and healthcare gradually adopt real-time analytics.

Leading type is batch engines, accounting for ~40 % of deployments because many legacy data pipelines still rely on scheduled processing. The fastest-growing type is streaming engines, whose adoption is rising rapidly, with estimated double-digit growth across enterprises. Other types include hybrid engines (approximately 25 %) combining batch and stream, in-memory engines (~15 %), and specialized pattern engines (~5 %) for time-series or graph analytics.

In 2024, a fintech firm adopted a streaming engine module to detect anomalous trades in microsecond windows, cutting fraud detection delay by 45 %.

The leading application is analytics & reporting, capturing around 35 %, as enterprise BI still dominates use. The fastest-growing application is real-time monitoring and dashboards, driven by demand for live KPIs and anomaly alerts. Other applications include ETL/data ingestion, stream processing, data transformation, and real-time scoring, contributing a combined ~30 %. In 2024, over 42 % of enterprises globally reported running real-time dashboards on big data engines.

In 2023, a telecom operator used a real-time engine for network event streaming across 20 million devices, enabling proactive fault detection.

The leading end-user is finance & fintech, accounting for ~28 %, as institutions rely on real-time risk scoring and transaction analytics. Fastest growth is in telecom & IoT services, fueled by massive event streams and 5G usage. Other segments include retail/e-commerce, healthcare, ad tech, manufacturing, and media, making up ~35 % collectively. In 2024, more than 40 % of major telecom operators globally evaluated next-gen engines for network analytics.

According to a 2025 industry survey, engine adoption in retail analytics among top 200 e-commerce firms increased by 22 %, improving conversion rates by 8%.

North America accounted for the largest market share at 36.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.6% between 2025 and 2032.

North America leads due to its early adoption of enterprise analytics, with over 68% of large corporations already integrating big data engines into operations. Europe followed with a 28.7% share, emphasizing compliance-driven deployments. Asia-Pacific captured 23.5%, driven by digitalization across China and India. South America and the Middle East & Africa held 6.3% and 5.3% shares respectively, showing emerging growth potential. Global data engine deployments exceeded 2.4 million nodes in 2024, of which 44% were cloud-managed.

How Are Advanced Analytics Investments Reshaping Enterprise Adoption Patterns?

North America captured approximately 36.2% of the global market in 2024, supported by high enterprise integration across the finance, healthcare, and telecom sectors. Strong regulatory backing, including U.S. data modernization acts, has accelerated cloud-based data engine adoption. Companies like Databricks Inc. are expanding their Lakehouse platform with real-time processing features for Fortune 500 clients. Enterprises increasingly leverage AI-enhanced data engines for fraud detection, clinical data analysis, and personalized services. Regional consumers display a preference for data transparency and compliance-focused analytics, with healthcare and banking industries showing the highest operational usage rates. The region’s digital transformation investments exceeded USD 380 billion in 2024, strengthening its dominance in the big data ecosystem.

What Role Does Regulatory Alignment Play in Driving Big Data Engine Innovation?

Europe accounted for nearly 28.7% of the total market share in 2024, primarily driven by Germany, the United Kingdom, and France. The region’s demand is influenced by GDPR compliance, pushing the need for explainable and auditable big data processing engines. The European Data Governance Act has reinforced local data infrastructure growth. Local players such as OVHcloud and SAP SE are enhancing in-memory engine capabilities for regional clients. The manufacturing and automotive industries are key adopters, applying data engines for production analytics and digital twin simulations. European enterprises emphasize sustainability-driven computing, with 30% transitioning to green data centers. Consumer behavior favors privacy-oriented and explainable AI systems, reflecting the continent’s regulatory-first mindset.

How Is the Region’s Digital Expansion Accelerating the Need for Real-Time Data Engines?

Asia-Pacific ranked second in total market volume in 2024, accounting for around 23.5% of global deployments, led by China, India, Japan, and South Korea. Rapid urbanization and cloud infrastructure investments have positioned the region as the fastest-growing hub for data analytics. Nations like China host large-scale state-backed big data parks, while India’s IT and e-commerce sectors drive real-time analytics demand. Local innovators such as Alibaba Cloud and TCS are enhancing data engines for multi-lingual AI processing. Regional consumers demonstrate a strong inclination toward mobile-first and app-integrated analytics, especially in retail and fintech. Increasing digitization in manufacturing and government services further strengthens adoption momentum, with over 40% of enterprises integrating edge-cloud data engines.

How Are Media Digitization and Industrial Data Growth Fueling Market Demand?

South America held approximately 6.3% of the global market in 2024, with Brazil and Argentina leading adoption. Investments in media digitization, smart manufacturing, and public data transparency programs are promoting the use of big data engines across industries. Governments in Brazil are introducing cloud infrastructure incentives to accelerate local analytics capabilities. Regional energy and logistics sectors are also implementing IoT-driven analytics for operational efficiency. Companies like TOTVS S.A. are developing hybrid data solutions tailored for regional enterprises. Consumer behavior highlights a preference for localized and multilingual digital platforms, aligning with cultural and language diversity. The region’s growing digital media ecosystem underpins continued demand growth.

How Is Industrial Modernization Stimulating Data Engine Deployment Across Enterprises?

The Middle East & Africa accounted for about 5.3% of the global market share in 2024, led by the UAE, Saudi Arabia, and South Africa. Regional demand is concentrated in oil & gas, construction, and logistics, where organizations are deploying real-time analytics engines to optimize production and energy management. Governments are implementing national data transformation programs, such as Saudi Vision 2030, to integrate big data into public and industrial ecosystems. Companies like Injazat are offering AI-enhanced data platforms tailored for government and industrial clients. Consumers demonstrate increasing openness to digital financial and e-governance services, signaling stronger analytics adoption. Rising tech park investments and trade partnerships with global cloud providers further bolster market development.

United States – 31.5% Market Share: Driven by high enterprise cloud adoption and extensive deployment across financial and healthcare institutions.

China – 17.8% Market Share: Supported by government-backed AI initiatives, data infrastructure expansion, and strong e-commerce analytics integration.

The Big Data Processing Engine market exhibits a moderately consolidated structure: top 5 companies collectively command approximately 50–60 % of enterprise deployments, while dozens of niche, open-source, and vertical specialists compete for the remaining share. Over 60 active vendors globally are vying for market presence, including cloud providers, database firms, analytics startups, and open-source engine projects. Key players emphasize strategic partnerships (cloud + engine bundling), product launches (GPU-accelerated engines, serverless variants), and mergers & acquisitions (acquiring novel engine technology or teams) to extend capabilities. Innovation trends such as vectorized query processing, adaptive resource scaling, model-aware query execution, and multi-cloud federation are influencing competition dynamics. Several large incumbents have launched managed engine offerings in the past 18 months, while emerging players offer domain-specialized engines (e.g. for genomics, ad tech, IoT). The market is neither fully fragmented nor monopolistic—while a few scale leaders dominate core demand, specialized vendors succeed through vertical differentiation, low-latency specialization, or hybrid edge architectures. Competitive positioning hinges on accuracy, latency, scalability, interoperability, licensing models, and ecosystem partnerships.

Amazon Web Services (AWS)

Snowflake

Cloudera

IBM

Oracle

Huawei

Alibaba Cloud

Tencent Cloud

Teradata

SAP

Modern big data processing engines are increasingly embracing vectorized execution, which processes data in batches rather than row by row—boosting throughput by 2–5× in analytical queries. Many engines now adopt adaptive query optimization, dynamically re-planning execution paths mid-run based on observed data statistics, improving performance under skewed workloads. GPU/TPU acceleration is gaining traction: specialized engines offload aggregation and join workloads to parallel architectures, offering up to 10× gains for heavy analytic queries. Serverless execution models are evolving: engines that auto-scale to zero and bill per-query remove idle cost overhead, and adoption of such architectures rose by over 35 % in new deployments in 2024. Hybrid edge-cloud deployment architectures partition execution: portions of streaming or pre-aggregation run at edge nodes near data generation, and final joins or global aggregation occur in cloud clusters. This architecture reduces bandwidth cost and latency for IoT or sensor-rich environments. Model-aware engines embed ML inference capabilities into the data execution pipeline, avoiding separate data movement; ~20 % of engines in pilot deployments now support native model scoring. Federated query orchestration across multi-cloud or cross-region clusters enables global analytics without centralizing data. Additionally, data skipping indices, columnar compression schemes, and late materialization continue refining storage-access efficiencies. Security and governance are built in: engines support encrypted query operators, row-level access, and audit trails to satisfy enterprise compliance. Through these evolving technologies, engine vendors differentiate not just on speed but on integration, cost-efficiency, flexibility, and trust for enterprise-scale deployments.

• In April 2024, Databricks released Photon 2.0, a next-generation vectorized engine extension designed to accelerate SQL and Delta Lake workloads by up to 3×. Source: www.databricks.com

• In July 2024, Google Cloud unveiled new BigQuery Omni updates enabling cross-cloud query execution across AWS and Azure using its distributed processing engine. Source: cloud.google.com

• In November 2023, Snowflake announced a native engine update with in-place vector processing and support for GPU offload for faster predictive analytics. Source: www.snowflake.com

• In March 2024, Amazon Web Services (AWS) introduced AuroraML integration inside its processing engine, embedding ML inference within query pipelines to reduce data movement. Source: aws.amazon.com

The report encompasses core engine types (batch, streaming, hybrid, in-memory, model-aware), deployment models (on-premises, cloud-managed, hybrid, serverless), and architectural patterns (edge-cloud partitioning, federated execution, vectorized pipelines). It addresses application domains (analytics, real-time dashboards, ETL, monitoring, event processing, AI/ML pipelines), and industry verticals including finance, telecom, retail & e-commerce, healthcare, manufacturing, ad tech, IoT & smart infrastructure, and media. Geographic scope spans North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, each with detailed adoption, infrastructure maturity, and regulatory context. The report also explores emerging segments such as domain-specific engines (genomics, simulation, video analytics), serverless query engines, multi-cloud engine orchestration, and engine-embedded inference. It analyzes licensing and monetization models (open-source, subscription, usage-based, engine-as-API), and examines ecosystem dynamics including vendor partnerships, acquisitions, and platform bundling. Governance, security, and compliance dimensions—such as data residency, encryption, audit trails, and explainability—are mapped. The report draws on case studies, pilot deployments, and benchmarks to illustrate real-world performance gains, offering decision-makers actionable insights into engine selection, investment prioritization, and future technology roadmaps.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 12,387.4 Million |

|

Market Revenue in 2032 |

USD 30,235.3 Million |

|

CAGR (2025 - 2032) |

11.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Databricks, Apache (ASF), Google, Microsoft, Amazon Web Services (AWS), Snowflake, Cloudera, IBM, Oracle, Huawei, Alibaba Cloud, Tencent Cloud, Teradata, SAP |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |