Reports

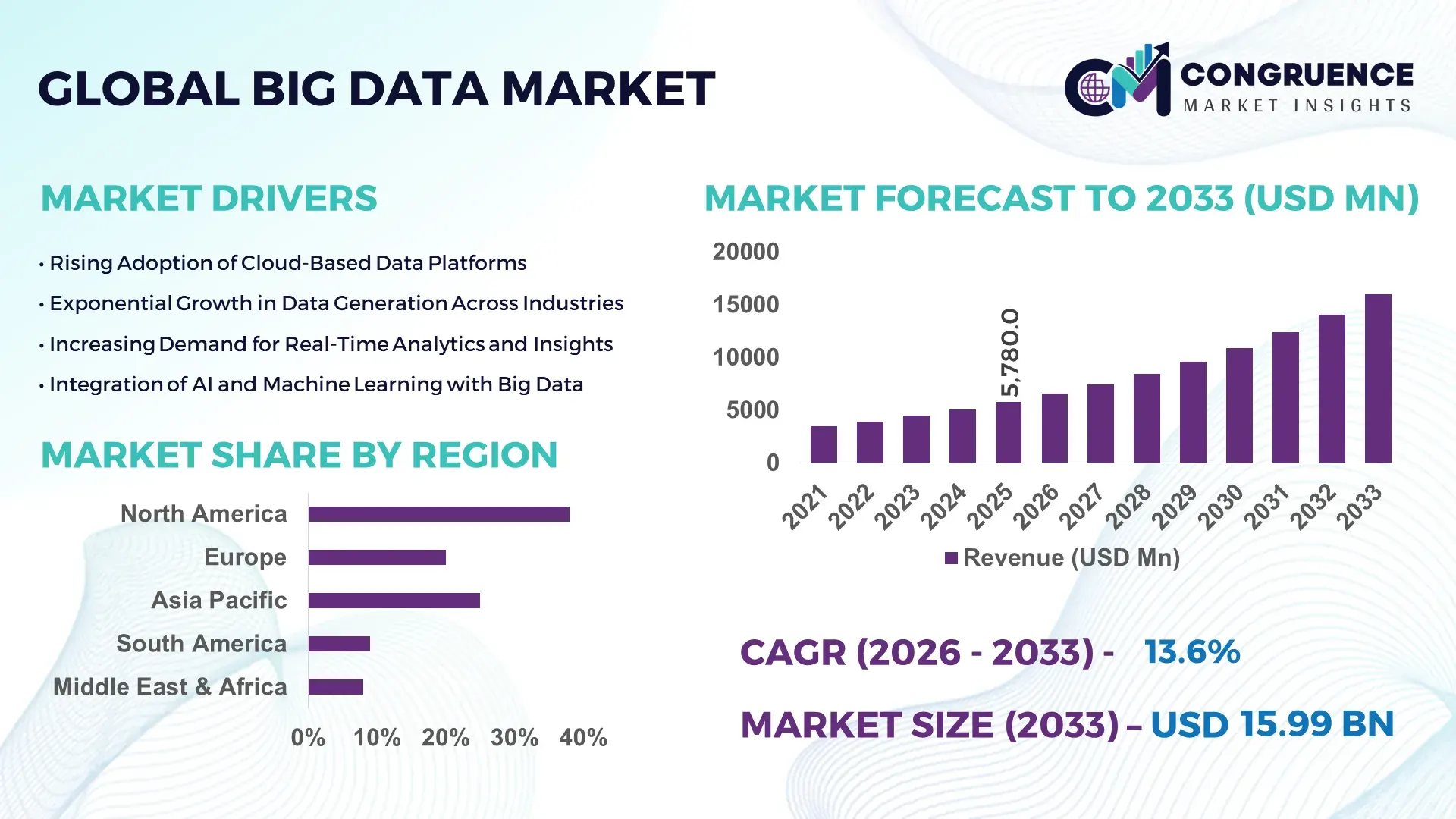

The Global Big Data Market was valued at USD 5780 Million in 2025 and is anticipated to reach a value of USD 15985.67 Million by 2033 expanding at a CAGR of 13.56% between 2026 and 2033. This growth is driven by the accelerating volume of structured and unstructured data generated across enterprises, fueled by digital transformation, cloud adoption, and advanced analytics integration.

The United States continues to maintain a strong position in the Big Data market, supported by extensive hyperscale data center infrastructure and advanced analytics deployment. The country hosts over 2,700 data centers and accounts for more than 40% of global cloud storage capacity. Approximately 65% of large enterprises in the U.S. utilize big data analytics for applications such as fraud detection, customer behavior analysis, and supply chain optimization. The BFSI sector alone processes more than 10 petabytes of data daily, while healthcare analytics adoption has exceeded 58% across major institutions. Additionally, annual investments in AI and data analytics infrastructure surpassed USD 70 billion in 2024, accelerating innovation in real-time analytics, predictive modeling, and machine learning applications.

Market Size & Growth: USD 5780 Million in 2025, projected to reach USD 15985.67 Million by 2033 at a CAGR of 13.56%, driven by exponential enterprise data generation and analytics adoption.

Top Growth Drivers: Cloud adoption 68%, AI integration 55%, real-time analytics demand 47%.

Short-Term Forecast: By 2028, automated data processing is expected to reduce operational costs by 32% and improve decision-making speed by 45%.

Emerging Technologies: AI-powered analytics, edge computing frameworks, and data fabric architecture reshaping enterprise data ecosystems.

Regional Leaders: North America projected at USD 6200 Million by 2033 with strong enterprise analytics adoption; Asia-Pacific at USD 4800 Million with rapid digitalization; Europe at USD 3500 Million driven by regulatory compliance analytics.

Consumer/End-User Trends: BFSI, healthcare, and retail sectors contribute over 60% of total analytics usage, emphasizing predictive and real-time insights.

Pilot or Case Example: In 2024, a global retail enterprise improved inventory efficiency by 28% through AI-driven big data analytics implementation.

Competitive Landscape: Leading player holds approximately 22% market presence, followed by IBM, Microsoft, Oracle, SAP, and Google as key competitors.

Regulatory & ESG Impact: Data governance regulations and green data center initiatives targeting 30% energy efficiency improvement by 2030.

Investment & Funding Patterns: Over USD 50 billion invested globally in big data infrastructure and analytics innovation in 2024.

Innovation & Future Outlook: Integration of generative AI, real-time analytics engines, and decentralized data architectures driving long-term market evolution.

The Big Data market continues to expand across key industries, with BFSI contributing approximately 25% of total analytics usage, followed by healthcare at 18% and retail at 15%. Technological advancements such as AI-driven data lakes, real-time streaming platforms, and automated governance tools have improved data accuracy and processing efficiency by over 35%. Regulatory frameworks including GDPR and data localization mandates are influencing enterprise data strategies, while sustainability initiatives are promoting energy-efficient data centers. Asia-Pacific demonstrates strong consumption growth driven by digital transactions, whereas Europe emphasizes compliance-based analytics adoption. Emerging trends such as data mesh architecture, edge analytics, and generative AI integration are expected to shape the future landscape of the Big Data market.

The Big Data market has become a critical strategic asset for organizations seeking to enhance decision-making, operational efficiency, and competitive advantage. Advanced analytics platforms integrated with artificial intelligence enable enterprises to process massive datasets with high accuracy and speed. AI-driven analytics delivers up to 40% faster insights compared to traditional batch processing systems, significantly improving responsiveness. Cloud-native big data solutions also reduce infrastructure costs by nearly 35% compared to legacy systems, making them increasingly attractive for enterprises.

From a regional perspective, North America dominates in data volume due to established infrastructure, while Asia-Pacific leads in adoption with over 60% of enterprises actively implementing big data analytics in digital transformation initiatives. By 2028, edge computing-enabled real-time analytics is expected to improve operational efficiency by 38% across sectors such as manufacturing and logistics. Organizations are also aligning with ESG goals, targeting a 30% reduction in data center energy consumption by 2030 through green IT initiatives.

A practical example from 2024 highlights a logistics company in Germany achieving a 27% reduction in delivery delays through predictive analytics and real-time data integration. As investments in data governance, cybersecurity, and AI continue to rise, the Big Data market is evolving into a foundational pillar for business resilience, regulatory compliance, and sustainable growth.

The rapid increase in enterprise data generation is significantly driving the Big Data market, with organizations producing over 2.5 quintillion bytes of data daily. Digital transformation initiatives across industries such as banking, healthcare, and retail are generating vast datasets from customer interactions, transactions, and connected devices. More than 70% of enterprises rely on analytics for decision-making, leading to increased demand for advanced data processing platforms. The number of IoT devices is expected to exceed 30 billion globally, further accelerating data generation. Real-time analytics has improved operational efficiency by up to 40% in industries such as manufacturing and logistics, reinforcing the importance of scalable big data solutions.

Data privacy and security concerns continue to restrain the Big Data market as organizations face increasing risks related to cyber threats and regulatory compliance. Billions of records are exposed annually due to data breaches, with the average cost exceeding USD 4 million per incident. Compliance with strict data protection regulations requires significant investment in security infrastructure and governance systems. Around 60% of enterprises report difficulties in managing data privacy across multiple jurisdictions. The complexity of securing distributed data environments increases vulnerability, limiting adoption, particularly among smaller organizations with limited resources.

AI-driven analytics offers significant opportunities for the Big Data market by enabling enhanced data processing, automation, and predictive capabilities. Machine learning algorithms improve data analysis accuracy by up to 50% compared to traditional methods. Industries such as healthcare use AI-powered analytics to improve diagnostic accuracy by over 30%, while retail companies leverage predictive insights to enhance customer personalization. The integration of edge computing allows real-time data processing, creating new opportunities in manufacturing and autonomous systems. As organizations continue to invest in AI capabilities, demand for integrated big data platforms is expected to grow substantially.

Infrastructure complexity and high costs present major challenges for the Big Data market, particularly for organizations transitioning from legacy systems. Implementation costs can exceed budgets by 20–30%, requiring significant investment in hardware, software, and skilled personnel. Managing hybrid and multi-cloud environments adds operational complexity, while the shortage of skilled data professionals remains a critical issue, with demand exceeding supply by over 35%. Integration of diverse data sources and maintaining data quality further complicate deployment, slowing adoption among small and medium enterprises seeking scalable and cost-effective solutions.

Real-Time Analytics Adoption Surges by 48% Across Enterprises: The demand for real-time data processing has increased significantly, with over 48% of enterprises deploying streaming analytics platforms to enable instant decision-making. Organizations using real-time analytics report up to 45% faster response times in operations and customer engagement. Industries such as finance and e-commerce are processing over 70% of their transactional data in real time, reducing fraud incidents by nearly 30% and improving customer retention by 25%. This shift is driving investments in low-latency architectures and event-driven data pipelines.

AI Integration in Data Platforms Improves Accuracy by 52%: Artificial intelligence integration into big data platforms has enhanced data processing accuracy by approximately 52%, enabling predictive analytics and automated insights. Around 60% of enterprises now use AI-driven data tools to optimize operations, with machine learning models reducing forecasting errors by up to 35%. In sectors such as healthcare, AI-enabled analytics systems have improved diagnostic accuracy by 28%, while manufacturing firms report a 32% reduction in equipment downtime through predictive maintenance solutions.

Edge Computing Deployment Expands by 41% for Low-Latency Processing: Edge computing adoption has grown by 41% as organizations seek to process data closer to its source, reducing latency by up to 50%. Over 55% of IoT-enabled enterprises now deploy edge analytics to handle real-time data streams from connected devices. This trend is particularly prominent in industries such as logistics and smart manufacturing, where real-time decision-making improves operational efficiency by 38% and reduces network bandwidth usage by nearly 27%.

Data Governance and Compliance Investments Increase by 37%: With stricter data privacy regulations, enterprises have increased investments in data governance frameworks by 37% to ensure compliance and data security. Approximately 68% of organizations have implemented advanced data governance tools, improving data quality by 33% and reducing compliance risks by 29%. Companies adopting automated governance systems have reported a 40% reduction in data-related errors, while regulatory compliance initiatives are accelerating the adoption of secure and transparent data management practices across global markets.

The Big Data market is segmented based on type, application, and end-user industries, reflecting diverse adoption patterns across sectors. By type, software solutions dominate due to increasing demand for analytics platforms, data integration tools, and AI-enabled systems, while services such as consulting and managed analytics are gaining traction. In terms of application, customer analytics and operational analytics account for a significant share, driven by enterprise demand for actionable insights and process optimization. End-user segmentation highlights strong adoption across BFSI, healthcare, retail, and manufacturing sectors, collectively contributing over 70% of total market utilization. Emerging adoption in government and telecom sectors is also notable, supported by smart infrastructure and digital transformation initiatives. The segmentation landscape underscores the increasing importance of scalable, flexible, and industry-specific big data solutions.

The Big Data market by type is primarily segmented into software and services, with software solutions leading the segment due to their extensive deployment across analytics, data management, and visualization platforms. Software accounts for approximately 62% of total adoption, driven by the growing need for scalable analytics tools and AI-powered data processing systems. In comparison, services hold around 38%, including consulting, integration, and managed services that support implementation and optimization. While software dominates, services represent the fastest-growing segment, expanding at an estimated CAGR of 15.8%, as organizations increasingly seek external expertise to manage complex data environments. The demand for managed analytics services has increased by over 40% in the past two years, particularly among small and medium enterprises lacking in-house capabilities. Within software, segments such as data analytics platforms and data integration tools collectively contribute over 70% of software adoption, while niche areas like data visualization and governance tools account for the remaining share.

The Big Data market by application includes customer analytics, operational analytics, fraud detection, risk management, and supply chain optimization. Customer analytics leads the segment, accounting for approximately 34% of total application usage, as enterprises prioritize personalized experiences and targeted marketing strategies. Operational analytics follows with around 26%, focusing on improving efficiency and reducing costs through data-driven insights. Fraud detection and risk management are among the fastest-growing applications, with an estimated CAGR of 16.2%, driven by increasing cybersecurity threats and regulatory requirements. Financial institutions have reported a 30% reduction in fraudulent transactions through advanced analytics systems. Supply chain analytics is also gaining traction, contributing nearly 18% of application usage, as companies seek to enhance logistics efficiency and inventory management.

The Big Data market by end-user is dominated by the BFSI sector, which accounts for approximately 28% of total market adoption due to its heavy reliance on data for risk assessment, fraud detection, and customer analytics. Healthcare follows with around 20%, leveraging big data for clinical decision support, patient monitoring, and research. Retail contributes approximately 16%, driven by demand for customer behavior analysis and inventory optimization. Healthcare represents the fastest-growing end-user segment, with an estimated CAGR of 17.5%, fueled by the increasing use of predictive analytics, electronic health records, and AI-driven diagnostics. The manufacturing and telecom sectors collectively account for around 22% of the market, benefiting from real-time data processing and IoT integration to improve operational efficiency.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.2% between 2026 and 2033.

North America’s dominance is supported by over 2,700 hyperscale data centers and more than 65% enterprise adoption of advanced analytics platforms. Europe holds approximately 26% share, driven by regulatory compliance and data governance initiatives, while Asia-Pacific contributes nearly 24%, fueled by rapid digitalization and increasing internet penetration exceeding 64%. South America and the Middle East & Africa collectively account for around 12%, with growing investments in telecom, smart infrastructure, and cloud adoption. Over 70% of global enterprises across these regions are investing in big data solutions to enhance operational efficiency, while more than 55% are prioritizing real-time analytics capabilities. Regional variations in cloud infrastructure, regulatory frameworks, and digital maturity levels continue to shape adoption patterns and long-term growth trajectories.

How are enterprise analytics and cloud ecosystems accelerating large-scale data adoption?

North America holds approximately 38% of the global Big Data market share, driven by advanced digital infrastructure and strong enterprise adoption across industries such as BFSI, healthcare, and retail. Over 65% of enterprises in this region actively deploy big data analytics solutions, with financial institutions processing more than 10 petabytes of data daily. Government initiatives supporting AI and data innovation, along with strict data security regulations, are shaping the market landscape. Technological advancements such as AI-powered analytics, cloud-native platforms, and edge computing are widely adopted, improving operational efficiency by up to 40%. A notable example includes a leading technology provider implementing AI-driven analytics platforms to enhance real-time decision-making for over 5,000 enterprise clients. Consumer behavior reflects high reliance on data-driven insights, particularly in healthcare and financial services, where predictive analytics adoption exceeds 60%.

Why is regulatory-driven analytics shaping enterprise data strategies and adoption trends?

Europe accounts for approximately 26% of the global Big Data market, with key countries such as Germany, the United Kingdom, and France leading adoption. Regulatory frameworks such as GDPR have influenced over 70% of enterprises to implement advanced data governance and compliance solutions. Sustainability initiatives and green data center projects are also prominent, with companies targeting up to 30% reductions in energy consumption. The adoption of emerging technologies, including AI and data fabric architectures, has increased by over 45% across enterprises. A regional example includes a major European cloud provider deploying secure analytics platforms to support over 2,000 organizations in achieving compliance and operational efficiency. Consumer behavior in this region emphasizes transparency and data privacy, driving demand for explainable analytics solutions and secure data processing systems.

What factors are driving rapid digital transformation and analytics adoption across emerging economies?

Asia-Pacific represents nearly 24% of the global Big Data market and ranks as the fastest-growing region in terms of adoption. Countries such as China, India, and Japan are leading consumption, with digital transaction volumes increasing by over 50% annually. Infrastructure expansion, including the development of over 1,200 new data centers, supports large-scale data processing needs. The region is also home to major technology hubs driving innovation in AI, machine learning, and edge computing. A notable example includes a leading Asian technology firm deploying big data platforms to support over 10 million small businesses in optimizing operations. Consumer behavior in this region is heavily influenced by e-commerce and mobile applications, with over 70% of users engaging in digital platforms, driving demand for real-time analytics and personalized services.

How are digital media growth and telecom expansion influencing data analytics demand?

South America accounts for approximately 7% of the global Big Data market, with Brazil and Argentina as key contributors. The region is witnessing increased adoption of big data solutions in telecom, media, and energy sectors, where data-driven decision-making improves operational efficiency by up to 28%. Government initiatives promoting digital transformation and data infrastructure investments are supporting market growth. For instance, national digital strategies have increased cloud adoption rates by over 35% among enterprises. A regional example includes a telecom operator leveraging big data analytics to improve network performance and reduce downtime by 25%. Consumer behavior in this region is driven by digital media consumption and localized content, with over 60% of users engaging in streaming and online platforms, boosting demand for analytics solutions.

What role do smart infrastructure and energy sector analytics play in digital transformation?

The Middle East & Africa region holds approximately 5% of the global Big Data market, with strong demand from oil & gas, construction, and government sectors. Countries such as the UAE and South Africa are leading adoption, supported by smart city initiatives and digital transformation programs. Investments in cloud infrastructure and data centers have increased by over 40%, enabling scalable analytics solutions. Technological modernization, including AI-driven analytics and IoT integration, is improving operational efficiency by up to 30% in key industries. A notable example includes a regional energy company deploying predictive analytics to optimize resource management and reduce operational costs by 20%. Consumer behavior reflects growing adoption of digital services, with increased reliance on mobile platforms and smart applications driving demand for real-time data insights.

United States – 38% market share: Big Data market leadership driven by advanced cloud infrastructure, high enterprise analytics adoption, and strong AI investment ecosystem.

China – 18% market share: Big Data market growth supported by massive digital user base, rapid industrial digitization, and government-backed data innovation initiatives.

The Big Data market is moderately consolidated, with the top five companies accounting for approximately 48% of the total market share, while over 150 active players operate globally across software, services, and analytics segments. Leading companies are focusing on strategic partnerships, product innovation, and acquisitions to strengthen their market positions. More than 60% of major players have invested in AI integration and cloud-based analytics platforms to enhance scalability and performance. The market has witnessed over 120 strategic collaborations and mergers between 2023 and 2025, aimed at expanding technological capabilities and geographic presence. Innovation remains a key competitive factor, with companies introducing advanced data fabric architectures, real-time analytics engines, and automated governance tools that improve data processing efficiency by over 35%. Additionally, approximately 55% of vendors are prioritizing industry-specific solutions tailored for sectors such as healthcare, BFSI, and retail. Competitive differentiation is increasingly driven by the ability to deliver secure, scalable, and AI-powered analytics solutions that align with regulatory requirements and enterprise needs.

IBM

Microsoft

Oracle

SAP

Amazon Web Services (AWS)

Teradata

Cloudera

Snowflake

Splunk

SAS Institute

Dell Technologies

Hewlett Packard Enterprise (HPE)

Palantir Technologies

Databricks

The Big Data market is being transformed by rapid advancements in cloud computing, artificial intelligence, and distributed data architectures. Cloud-native platforms now support over 65% of enterprise big data workloads, enabling scalable storage and processing capabilities across hybrid and multi-cloud environments. Technologies such as data lakes and lakehouse architectures are gaining prominence, allowing organizations to manage both structured and unstructured data in unified environments, improving data accessibility by nearly 40%. Additionally, real-time data streaming technologies are processing over 70% of enterprise data flows, significantly enhancing decision-making speed and operational responsiveness.

Artificial intelligence and machine learning integration into big data platforms has increased analytics accuracy by up to 50%, enabling predictive and prescriptive analytics across industries. Automated data pipelines and AI-driven data governance tools are reducing manual data preparation efforts by approximately 35%, improving efficiency and data quality. Edge computing is also playing a critical role, with over 55% of IoT-enabled enterprises deploying edge analytics solutions to reduce latency by up to 50% and optimize bandwidth utilization.

Furthermore, data fabric and data mesh architectures are emerging as key innovations, enabling decentralized data management and improving data integration across distributed systems by 30%. Advanced security technologies, including encryption, zero-trust architectures, and AI-based threat detection, are reducing data breach risks by nearly 25%. As organizations continue to prioritize scalability, security, and real-time insights, these technological advancements are reshaping the Big Data market and driving enterprise-wide digital transformation.

In March 2025, Microsoft announced the expansion of its Fabric data platform with integrated AI-powered analytics capabilities, enabling enterprises to unify data engineering, real-time analytics, and business intelligence workflows. The update improved data processing efficiency by up to 35% and enhanced cross-platform data integration. Source: www.microsoft.com

In November 2024, Amazon Web Services (AWS) introduced enhancements to Amazon Redshift, including automated scaling and AI-driven query optimization, enabling enterprises to reduce query execution time by up to 40% while improving cost efficiency across large-scale data warehousing operations.

In April 2025, Google launched advanced BigQuery AI features, integrating generative AI capabilities directly into its analytics platform, allowing users to generate insights using natural language queries and improving data analysis productivity by approximately 30%.

In September 2024, IBM expanded its watsonx.data platform with enhanced data lakehouse capabilities, enabling organizations to manage large-scale structured and unstructured data more efficiently, reducing data integration complexity by 30% and improving analytics performance across hybrid cloud environments. Source: www.ibm.com

The Big Data Market Report provides a comprehensive evaluation of the global landscape, covering key segments, technologies, applications, and regional insights that define the industry. The report analyzes multiple data types, including structured, semi-structured, and unstructured data, which collectively account for over 80% of enterprise data generation. It also examines deployment models such as cloud-based, on-premise, and hybrid solutions, with cloud deployments representing more than 60% of current enterprise implementations.

From an application perspective, the report focuses on critical use cases including customer analytics, operational intelligence, fraud detection, and supply chain optimization, which together contribute to over 65% of total analytics adoption across industries. Industry verticals covered include BFSI, healthcare, retail, manufacturing, telecom, and government sectors, all of which demonstrate varying levels of adoption and technological maturity. BFSI and healthcare alone account for nearly 45% of total big data utilization due to their reliance on data-driven decision-making.

Geographically, the report provides detailed insights into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional variations in infrastructure, regulatory frameworks, and digital transformation initiatives. It also explores emerging areas such as edge analytics, data mesh architectures, and AI-driven analytics platforms, which are expected to significantly influence future market dynamics. The report further highlights niche segments such as real-time streaming analytics and automated data governance, offering a holistic view of the evolving Big Data ecosystem for strategic decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

13.56% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM, Microsoft, Oracle, SAP, Google, Amazon Web Services (AWS), Teradata, Cloudera, Snowflake, Splunk, SAS Institute, Dell Technologies, Hewlett Packard Enterprise (HPE), Palantir Technologies, Databricks |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |