Reports

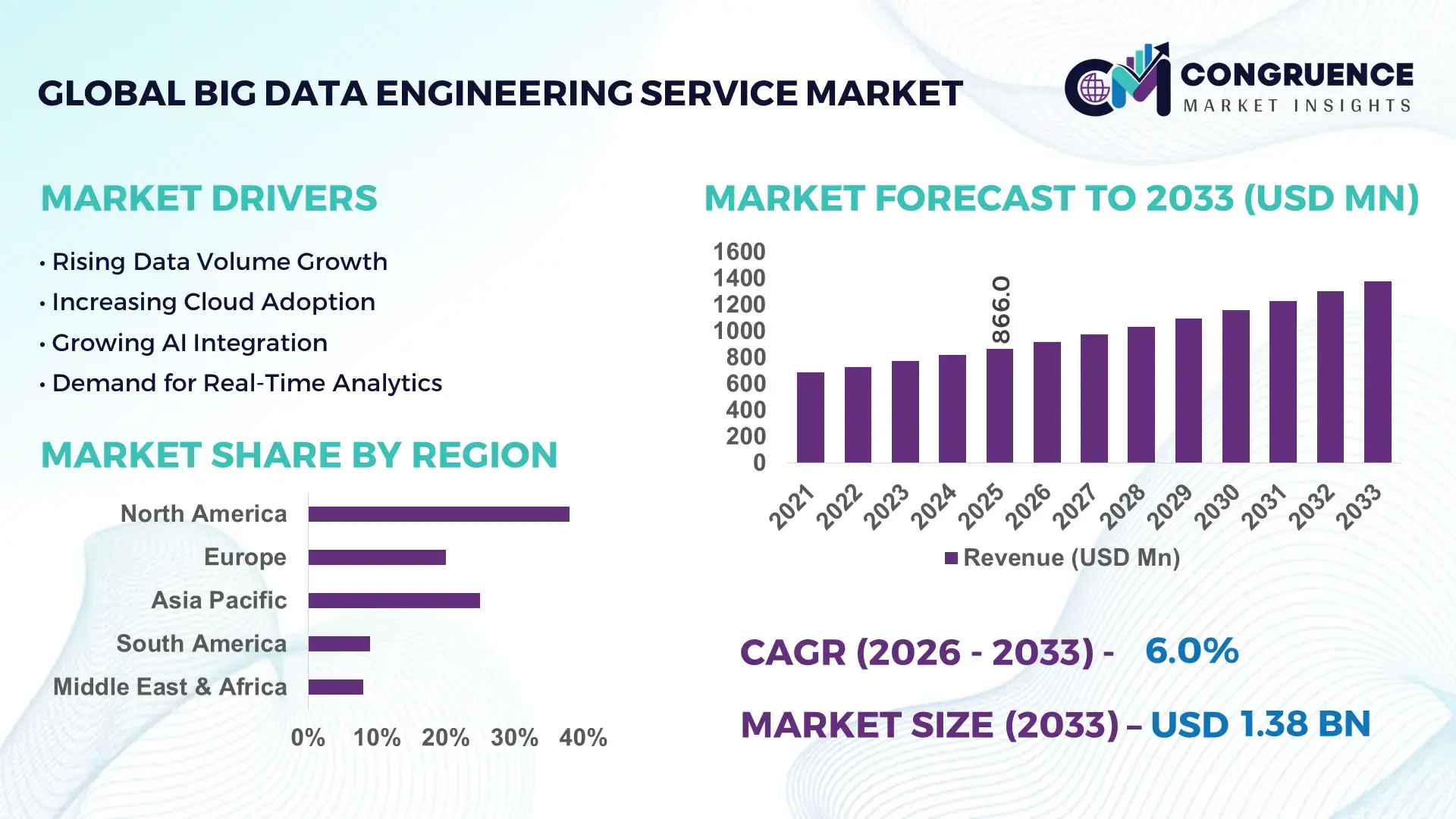

The Global Big Data Engineering Service Market was valued at USD 866 Million in 2025 and is anticipated to reach a value of USD 1380.27 Million by 2033 expanding at a CAGR of 6% between 2026 and 2033. Growth is accelerating through enterprise AI integration, real-time analytics deployment, hybrid cloud modernization, and rising data governance mandates across banking, telecom, manufacturing, and healthcare ecosystems.

The United States accounted for nearly 34% of global advanced big data engineering service deployment in 2026, supported by hyperscale cloud investments exceeding USD 75 billion and strong adoption across financial services, retail analytics, and defense intelligence platforms. India processed over 20% higher enterprise data workloads through offshore engineering hubs compared to 2024, while Germany expanded industrial data orchestration programs across automotive and Industry 4.0 facilities amid tightening EU data sovereignty regulations linked to the European Data Act framework.

Organizations prioritizing scalable data pipeline automation, low-latency analytics infrastructure, and AI-ready engineering architecture are securing faster operational decision cycles and stronger cross-border digital competitiveness.

Market Size & Growth: USD 866 Million in 2025 reaching USD 1380.27 Million by 2033 at 6% CAGR, driven by enterprise AI integration and cloud-native data modernization programs.

Top Growth Drivers: Real-time analytics adoption rose 41%, hybrid cloud migration expanded 38%, and automated data governance deployment increased 33% globally.

Short-Term Forecast: By 2028, enterprises are projected to reduce data processing latency by 29% while improving analytics workflow efficiency by 35%.

Emerging Technologies: AI-driven data orchestration, lakehouse architecture, and edge analytics improved enterprise data utilization rates by over 30% in high-volume environments.

Regional Leaders: North America surpassed USD 390 Million with BFSI-led deployments, Asia-Pacific crossed USD 280 Million through digital infrastructure expansion, and Europe exceeded USD 240 Million supported by regulated cloud adoption.

Consumer/End-User Trends: Nearly 62% of large enterprises shifted toward unified data engineering platforms to support predictive analytics and multi-cloud operations.

Pilot/Case Example: In 2026, a telecom data modernization project reduced network analytics downtime by 44% using automated streaming data engineering infrastructure.

Competitive Landscape: Top providers controlled approximately 46% market share, with leading participation from IBM, Accenture, TCS, Capgemini, and Infosys.

Regulatory & ESG Impact: Advanced governance frameworks lowered enterprise compliance risks by 31% amid stricter cross-border data localization and sustainability reporting mandates.

Investment & Funding: Global enterprise investment exceeded USD 18 billion in scalable data platforms, fueled by cloud partnerships, AI infrastructure expansion, and regional supply-chain digitization.

Innovation & Future Outlook: Autonomous data engineering, synthetic data pipelines, and AI-assisted observability platforms are accelerating strategic transition toward self-optimizing enterprise analytics ecosystems.

Big Data Engineering Service Market demand is expanding across banking fraud analytics, smart manufacturing, telecom network intelligence, and healthcare data interoperability platforms. Over 57% of enterprises now prioritize AI-ready data architecture upgrades to improve operational visibility and automated decision execution. Cloud-native pipeline engineering, real-time streaming frameworks, and low-code observability tools are reshaping deployment models as organizations navigate stricter regional data compliance and distributed digital infrastructure strategies, setting the foundation for broader strategic transformation discussions.

Big data engineering services are becoming strategically critical as enterprises shift from fragmented analytics environments toward AI-ready operational ecosystems capable of supporting real-time automation, predictive intelligence, and cross-platform decision execution. More than 64% of global enterprises accelerated modernization of legacy data architectures in 2026 following stricter data localization frameworks and rising cloud optimization costs. The market is increasingly tied to digital supply-chain restructuring, especially across banking, manufacturing, and telecom sectors where low-latency analytics infrastructure now directly influences operational resilience and customer retention.

Cloud-native data engineering platforms process workloads nearly 42% faster than traditional on-premise batch systems while reducing infrastructure maintenance costs by approximately 28% through containerized orchestration and automated scaling. The United States leads in enterprise-grade AI pipeline deployment, while India expanded managed data engineering operations through offshore delivery hubs supporting over 30% higher enterprise integration volumes. In Germany, industrial firms prioritized sovereign data frameworks for automotive analytics and factory telemetry integration under evolving European compliance standards.

A 2026 telecom deployment integrating streaming analytics with edge data pipelines reduced service disruption detection time by 37%, prompting broader investment in observability platforms and multi-cloud engineering partnerships. Over the next three years, enterprises are expected to prioritize autonomous data operations, sector-specific governance models, and scalable AI integration frameworks to strengthen competitive positioning, accelerate decision velocity, and secure long-term digital infrastructure advantage.

Large enterprises are accelerating investment in advanced data engineering services to support AI-driven operations, predictive analytics, and real-time automation. More than 61% of enterprises migrated critical analytics workloads toward hybrid cloud ecosystems in 2026, while automated data pipeline adoption improved operational efficiency by nearly 34%. In the United States, financial institutions increased spending on scalable data orchestration platforms following tighter cybersecurity and reporting mandates. Manufacturing companies in Japan expanded industrial IoT integration programs to process machine telemetry with lower latency and higher reliability. This structural shift is pushing service providers to expand cloud engineering partnerships, develop industry-specific accelerators, and strengthen managed data governance capabilities. Companies prioritizing unified data infrastructure are achieving faster model deployment cycles and improved enterprise-wide operational visibility.

Complex multi-cloud environments and fragmented enterprise architecture remain major barriers to scalable deployment. Nearly 47% of enterprises report integration delays caused by incompatible legacy systems, while data migration costs increased by approximately 22% due to rising storage optimization and compliance requirements. In Germany, strict enterprise data sovereignty standards continue to complicate cross-border analytics deployment across manufacturing and automotive networks. Many organizations still operate isolated data warehouses that reduce interoperability between operational technology and enterprise applications. These limitations directly impact deployment consistency, processing efficiency, and long-term infrastructure scalability. To reduce operational risks, companies are adopting modular data engineering frameworks, regionalized hosting strategies, and open-source interoperability standards while expanding partnerships with cloud infrastructure providers to stabilize migration and integration performance.

Autonomous data engineering platforms are creating high-value opportunities across healthcare, telecom, and industrial automation environments where enterprises require faster analytics execution with lower operational overhead. More than 53% of large organizations are deploying AI-assisted observability and self-healing data pipeline technologies to improve reliability and reduce manual intervention. India’s digital infrastructure expansion and rapid enterprise cloud adoption are accelerating demand for managed engineering services supporting real-time analytics and AI workloads. Advanced lakehouse architectures improved enterprise data accessibility by nearly 36% compared to traditional siloed systems, enabling stronger cross-functional analytics integration. Companies are increasing investment in low-code engineering tools, edge analytics platforms, and industry-specific data governance ecosystems to capture untapped mid-market demand while strengthening recurring service-based operational models.

Long-term scalability is increasingly constrained by shortages in advanced data engineering talent, evolving cybersecurity threats, and operational complexity linked to distributed analytics infrastructure. Nearly 44% of enterprises report delays in large-scale deployment due to shortages in cloud-native engineering and data governance expertise. In the United Kingdom, financial and healthcare organizations are strengthening compliance oversight following increased scrutiny around AI-driven data processing and cross-platform security exposure. At the same time, multi-cloud environments expanded enterprise attack surfaces by approximately 31%, increasing pressure on infrastructure resilience and monitoring capabilities. Companies must invest in automated governance frameworks, specialized engineering training programs, and secure-by-design architecture strategies to maintain deployment consistency, protect operational continuity, and sustain long-term competitive differentiation in high-volume digital ecosystems.

AI-Native Pipeline Automation Expansion Enterprises are replacing manually managed data workflows with AI-assisted orchestration platforms that reduce processing delays by nearly 39% and lower infrastructure monitoring workloads by 27%. In the United States, telecom and banking firms accelerated autonomous pipeline deployment following rising real-time analytics demand and stricter reporting compliance requirements. Service providers are responding through workflow automation partnerships, observability integration, and low-code engineering frameworks that shorten deployment cycles and improve operational scalability.

Lakehouse Architecture Deployment Surge Enterprise adoption of lakehouse environments increased by approximately 44% during 2026 as organizations consolidated fragmented storage systems into unified analytics ecosystems. Manufacturing companies in Germany improved cross-platform data accessibility by over 31% through centralized industrial telemetry integration. The shift is reducing duplication costs, improving governance consistency, and enabling faster AI model training. Vendors are restructuring service portfolios around cloud-native architecture modernization and scalable metadata management capabilities.

Edge Analytics Integration Acceleration Real-time edge analytics deployment expanded by nearly 36% across logistics, retail, and smart manufacturing operations due to rising latency-sensitive workloads and connected device expansion. Japanese industrial facilities integrated distributed analytics engines to reduce machine response delays by 24% during automated production monitoring. Companies are prioritizing regional processing nodes, lightweight engineering frameworks, and telecom partnerships to stabilize operational continuity while reducing cloud bandwidth dependency and infrastructure congestion risks.

Sovereign Data Infrastructure Prioritization Enterprise demand for sovereign data engineering frameworks increased by nearly 33% following stricter localization policies and evolving cybersecurity regulations across Europe and parts of Asia. Financial institutions and healthcare providers are restructuring multi-cloud deployment strategies to maintain compliance while improving audit transparency and operational resilience. A less visible shift involves companies redesigning vendor contracts around localized hosting and encryption-layer interoperability, creating stronger demand for region-specific engineering expertise and managed governance services.

Cloud Data Services remain the leading segment due to enterprise demand for scalable analytics infrastructure, lower maintenance overhead, and flexible multi-cloud deployment models. More than 58% of large organizations prioritized cloud-native engineering environments in 2026 to improve real-time data accessibility and reduce processing latency. Data Integration continues to hold strong strategic relevance as enterprises consolidate fragmented operational systems across finance, manufacturing, and telecom networks. Companies are expanding managed orchestration capabilities and strengthening partnerships with hyperscale cloud providers to support unified analytics environments and AI-ready infrastructure modernization.

Data Migration is emerging as the fastest-growing type as enterprises replace legacy warehouses with distributed lakehouse architectures and hybrid cloud ecosystems. Migration-driven modernization projects reduced infrastructure redundancy by approximately 26% while improving deployment flexibility across geographically distributed operations. Data Warehousing remains critical for compliance-intensive industries requiring structured governance and historical reporting, while Data Analytics services are gaining traction through predictive intelligence and autonomous workflow optimization. Service providers are increasing investment in automated migration frameworks, metadata intelligence tools, and containerized engineering solutions to strengthen operational efficiency and recurring enterprise contracts.

Business Intelligence remains the leading application segment as enterprises prioritize centralized decision-making, executive reporting, and operational visibility across distributed digital environments. More than 61% of enterprises expanded integrated BI deployments in 2026 to support cross-functional analytics and automated reporting workflows. Real-Time Analytics is the fastest-growing application due to increasing demand for low-latency operational monitoring in telecom, logistics, and digital commerce ecosystems. Companies deploying streaming analytics frameworks improved incident response speed by nearly 34%, strengthening customer experience management and operational continuity.

Predictive Analytics is gaining strategic traction through AI-assisted forecasting and demand-planning integration, particularly across manufacturing and financial services operations. Customer Analytics deployment expanded by approximately 29% as retailers and digital platforms intensified personalization strategies and behavioral segmentation initiatives. Risk Management applications remain essential in BFSI and healthcare environments where compliance monitoring and fraud detection require continuous data orchestration. Service providers are scaling event-driven architecture capabilities, integrating machine learning workflows, and expanding managed analytics partnerships to address rising enterprise demand for continuous intelligence and operational responsiveness.

BFSI remains the dominant end-user segment due to high transaction volumes, strict compliance requirements, and continuous demand for fraud detection and real-time risk monitoring infrastructure. More than 64% of large banking institutions expanded cloud-integrated data engineering environments during 2026 to support AI-driven financial analytics and regulatory reporting automation. IT and Telecom also maintain strong adoption intensity through network intelligence, subscriber analytics, and distributed data processing workloads. Companies are strengthening cybersecurity integration, expanding managed analytics partnerships, and investing in low-latency processing frameworks to improve operational reliability and customer retention.

Healthcare is emerging as the fastest-growing end-user segment as hospitals and healthcare networks modernize patient data interoperability and predictive care analytics infrastructure. Healthcare analytics deployment improved operational workflow efficiency by approximately 32% through integrated clinical data orchestration and AI-assisted diagnostics support. Manufacturing companies are increasing industrial IoT data engineering adoption, while retail enterprises continue scaling customer intelligence and inventory optimization systems. Government Sector demand is also strengthening through digital governance modernization and national cybersecurity programs. Providers are responding through industry-specific engineering platforms, compliance-focused deployment models, and ecosystem-driven service customization strategies.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

AI-Driven Enterprise Data Modernization

North America leads the market through advanced enterprise cloud infrastructure, hyperscale data center concentration, and large-scale analytics deployment across BFSI, healthcare, telecom, and retail industries. The region represented nearly 38% of global enterprise-grade data engineering implementation activity in 2025, supported by rising adoption of AI-ready analytics ecosystems and automated pipeline orchestration platforms. More than 66% of large enterprises accelerated migration toward multi-cloud data environments during 2026 to improve operational agility and reduce analytics latency. Strategic collaboration between cloud infrastructure providers and consulting firms intensified as organizations prioritized governance modernization, cybersecurity resilience, and scalable real-time analytics operations across distributed digital environments.

United States Market Outlook: The United States remains the largest contributor due to strong enterprise AI adoption, concentrated hyperscale cloud infrastructure, and mature digital transformation spending across regulated industries. Banking and telecom enterprises expanded deployment of automated data orchestration systems during 2026 to strengthen predictive intelligence and fraud analytics. Nearly 71% of Fortune 500 organizations increased investment in cloud-native engineering modernization programs, while federal cybersecurity compliance requirements accelerated demand for secure and scalable analytics infrastructure.

Sovereign Cloud and Industrial Analytics Expansion

Europe is strengthening market positioning through sovereign data infrastructure investment, industrial analytics modernization, and stricter enterprise governance frameworks. The region accounted for approximately 27% of advanced analytics deployment activity in 2025, led by manufacturing, automotive, and financial services sectors. Germany, France, and the United Kingdom accelerated deployment of low-latency analytics systems and localized cloud environments to comply with evolving digital compliance requirements. More than 42% of large enterprises expanded encrypted analytics deployment during 2026 to improve operational control and regulatory alignment. Service providers are expanding governance-focused engineering capabilities and regional hosting partnerships to support compliance-intensive enterprise workloads and industrial automation ecosystems.

Germany Market Outlook: Germany remains the region’s most strategically important market due to its strong industrial automation ecosystem and advanced manufacturing analytics adoption. Automotive and industrial engineering firms increased integration of AI-assisted factory telemetry and predictive maintenance systems during 2026 to improve production efficiency and operational reliability. Nearly 48% of large manufacturers expanded investment in sovereign data infrastructure platforms to strengthen regulatory compliance, energy-efficient processing, and industrial response speed within Industry 4.0 environments.

Large-Scale Cloud Infrastructure Acceleration

Asia-Pacific is emerging as the fastest-expanding regional market due to aggressive enterprise cloud migration, digital infrastructure modernization, and large-scale AI deployment across manufacturing, telecom, and e-commerce industries. The region contributed nearly 24% of global advanced data engineering deployment activity in 2025, supported by rapid hyperscale infrastructure expansion and government-backed digital transformation initiatives. More than 58% of enterprises across India, China, and Southeast Asia accelerated migration from legacy analytics systems toward cloud-native orchestration frameworks during 2026. Service providers are scaling delivery centers, expanding managed analytics partnerships, and investing in low-latency processing environments to support high-volume enterprise workloads and real-time operational intelligence.

India Market Outlook: India is rapidly strengthening its strategic position through large-scale offshore engineering capability, rising enterprise cloud adoption, and expanding AI infrastructure modernization. Telecom, banking, and digital commerce enterprises increased deployment of automated analytics pipelines and real-time data processing systems during 2026 to improve operational scalability. Over 63% of large Indian enterprises prioritized modernization of fragmented legacy data environments, while global service providers expanded regional delivery hubs to leverage engineering talent availability and growing domestic digital infrastructure investment.

Telecom and Digital Banking Expansion

South America is experiencing steady market development through rising digital banking adoption, telecom analytics deployment, and enterprise cloud modernization across large urban economies. Brazil and Chile continue driving operational demand as enterprises modernize fragmented analytics environments and improve customer intelligence systems. Approximately 36% of medium and large enterprises increased investment in cloud-integrated data engineering platforms during 2026 to strengthen fraud monitoring and operational visibility. However, uneven infrastructure maturity and inconsistent enterprise digitization continue to affect deployment scalability across several markets. Service providers are responding through localized implementation partnerships, managed analytics services, and cost-efficient cloud deployment frameworks tailored for mid-scale enterprises.

Brazil Market Outlook: Brazil leads the regional market through expanding fintech ecosystems, accelerating telecom modernization, and increasing enterprise cloud integration across retail and banking industries. Financial institutions strengthened investment in AI-driven fraud analytics and customer behavior intelligence during 2026 as digital transaction volumes expanded sharply. Nearly 46% of large enterprises adopted hybrid cloud analytics environments to improve operational scalability and reduce infrastructure dependency. Domestic technology integrators are also increasing collaboration with international cloud providers to strengthen enterprise deployment and governance capabilities.

Smart Infrastructure and Digital Transformation Investments

Middle East & Africa is expanding through sovereign cloud investment, smart city development, and government-led digital transformation programs across energy, transportation, finance, and public administration sectors. Gulf economies accelerated deployment of advanced analytics ecosystems to improve operational intelligence and infrastructure modernization efficiency. Approximately 41% of enterprise modernization initiatives launched during 2026 included AI-ready data engineering integration and cloud-native governance frameworks. Strategic partnerships between telecom operators, hyperscale cloud providers, and public-sector organizations are increasing deployment of localized analytics infrastructure. African markets are also expanding enterprise cloud adoption, although infrastructure fragmentation and workforce limitations continue to affect deployment consistency and operational scale.

United Arab Emirates Market Outlook: The United Arab Emirates remains the region’s leading market due to aggressive smart infrastructure investment, advanced digital governance initiatives, and strong enterprise cloud adoption. Banking, aviation, and public-sector organizations expanded deployment of AI-enabled operational analytics and real-time monitoring systems during 2026 to improve digital service efficiency. More than 52% of large enterprises accelerated migration toward sovereign cloud frameworks to strengthen compliance and data control capabilities, while hyperscale infrastructure partnerships continue positioning the country as a regional analytics and AI operations hub.

The market is dominated by global technology consulting leaders including Accenture, IBM, Capgemini, Infosys, and Tata Consultancy Services, competing directly against regional integrators, cloud-native engineering specialists, and AI-focused analytics firms. The top five players collectively control nearly 46% of enterprise-scale deployment activity, with competition centered on automation capability, deployment speed, multi-cloud integration depth, and industry-specific customization. Large global firms dominate BFSI and telecom contracts through scalable managed analytics ecosystems, while regional players compete through localized compliance expertise and lower deployment costs. AI-assisted orchestration reduced enterprise workflow management overhead by approximately 28%, forcing providers to accelerate observability integration and autonomous pipeline engineering capabilities. Strategic cloud partnerships expanded by over 32% during 2026 as enterprises prioritized scalable real-time analytics infrastructure. Competitive advantage increasingly depends on AI-ready architecture expertise, cybersecurity integration, low-latency deployment capability, and strong enterprise governance execution.

Accenture

IBM

Tata Consultancy Services (TCS)

Infosys

Capgemini

Wipro

Cognizant

HCLTech

Deloitte

Tech Mahindra

NTT DATA

DXC Technology

LTIMindtree

Fujitsu

Cloud-native lakehouse architecture, AI-assisted pipeline orchestration, and containerized analytics environments are reshaping enterprise data engineering operations. More than 62% of large enterprises adopted hybrid cloud data frameworks in 2026 to improve interoperability and analytics scalability. Modern streaming architectures process real-time workloads nearly 41% faster than legacy batch-processing systems while reducing infrastructure maintenance overhead by approximately 26%. Enterprises in banking and telecom sectors are integrating automated observability platforms to minimize downtime and accelerate incident resolution. Global consulting firms and hyperscale cloud providers are expanding co-engineering partnerships to strengthen deployment speed and enterprise-grade governance capabilities.

Emerging technologies including agentic AI workflows, metadata intelligence engines, and edge-native analytics platforms are improving operational responsiveness across distributed enterprise ecosystems. AI-assisted data orchestration reduced manual workflow intervention by nearly 33% during 2026 deployments, while low-code engineering platforms improved developer productivity by approximately 24%. Around 57% of enterprises are prioritizing autonomous data operations to support predictive analytics and cross-platform intelligence. Companies with strong multi-cloud engineering ecosystems are securing competitive advantage through lower latency analytics delivery and faster AI model integration.

Between 2026 and 2028, sovereign cloud frameworks, synthetic data environments, and self-healing data pipelines will accelerate deployment standardization across regulated industries. Enterprises adopting unified AI-ready architectures are expected to improve analytics execution efficiency by over 35%, positioning advanced engineering capabilities as a critical operational differentiator.

May 2025 – Accenture partnered with Dell Technologies and NVIDIA to expand AI Refinery deployment across private enterprise infrastructure environments. The solution enabled one-click deployment and reduced enterprise AI implementation complexity while improving infrastructure scalability for regulated industries. Operational adoption accelerated across high-performance analytics workloads.

April 2025 – Accenture expanded its strategic collaboration with Google Cloud to strengthen agentic AI, networking modernization, and enterprise-scale analytics integration capabilities. The initiative focused on accelerating cloud-native data engineering deployment and improving enterprise operational agility through scalable AI-ready digital core infrastructure.

December 2025 – Accenture and Anthropic launched a multi-year enterprise AI partnership involving training for approximately 30,000 professionals to accelerate Claude-powered analytics and engineering deployment. The collaboration strengthened regulated-industry AI integration and improved enterprise software development productivity through large-scale AI workflow modernization.

April 2026 – Accenture acquired Spain-based Keepler Data Tech, adding more than 240 cloud-native AI and data specialists to strengthen enterprise DataOps and MLOps modernization capabilities. The acquisition expanded advanced analytics engineering expertise and accelerated AI-driven data infrastructure transformation across European enterprise environments. Source: cincodias.elpais.com

The report provides detailed analysis of enterprise data engineering transformation trends across Data Integration, Data Warehousing, Data Analytics, Cloud Data Services, and Data Migration segments. It evaluates operational adoption patterns across Business Intelligence, Predictive Analytics, Customer Analytics, Risk Management, and Real-Time Analytics applications while assessing deployment dynamics across BFSI, Healthcare, Retail, IT and Telecom, Manufacturing, and Government sectors. Nearly 62% of large enterprises are prioritizing AI-ready analytics infrastructure modernization, increasing demand for scalable cloud-native engineering ecosystems and automated data orchestration frameworks.

The study covers strategic regional analysis across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure modernization, enterprise cloud deployment, sovereign data initiatives, and industrial analytics expansion. The report also examines competitive positioning, partnership strategies, observability technologies, edge analytics integration, and AI-assisted pipeline automation trends shaping operational transformation between 2026 and 2033. It supports investment planning, digital expansion strategy, vendor benchmarking, and long-term enterprise modernization decisions through deployment-focused business intelligence and sector-specific technology insights.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 866 Million |

|

Market Revenue in 2033 |

USD 1380.27 Million |

|

CAGR (2026 - 2033) |

6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Accenture, IBM, Tata Consultancy Services (TCS), Infosys, Capgemini, Wipro, Cognizant, HCLTech, Deloitte, Tech Mahindra, NTT DATA, DXC Technology, LTIMindtree, Fujitsu |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |