Reports

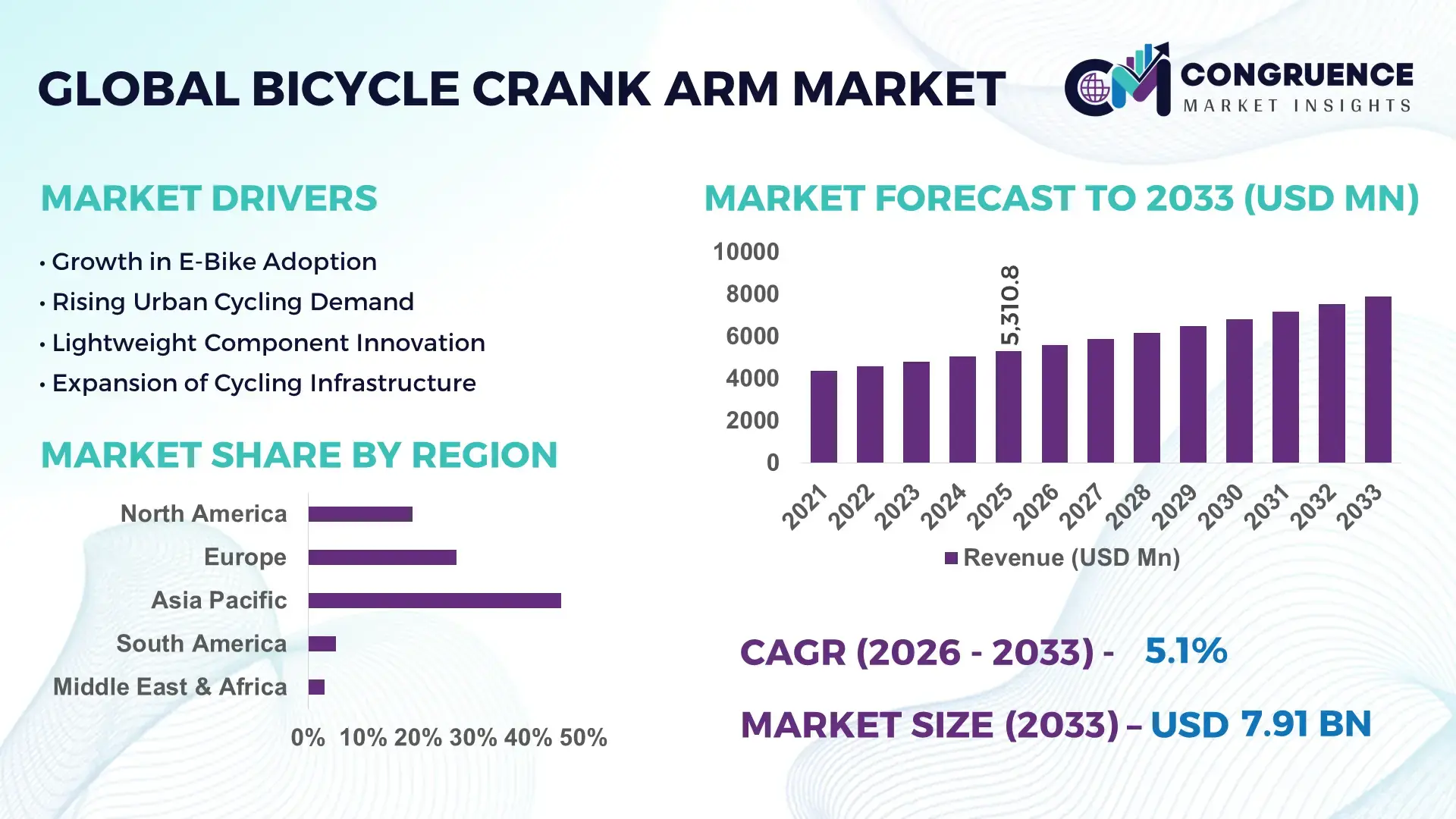

The Global Bicycle Crank Arm Market was valued at USD 5,310.8 Million in 2025 and is anticipated to reach a value of USD 7,906.5 Million by 2033 expanding at a CAGR of 5.10% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is supported by rising global bicycle production volumes, increasing penetration of performance-oriented drivetrain components, and steady replacement demand across commuter, mountain, and electric bicycles.

China dominates the Bicycle Crank Arm Market in terms of industrial scale and manufacturing depth. The country hosts more than 60% of global bicycle component manufacturing facilities, with annual bicycle production exceeding 80 million units, creating strong downstream demand for crank arms. Over 70% of aluminum crank arms used globally are produced in China, supported by vertically integrated forging, CNC machining, and surface treatment ecosystems. Investments exceeding USD 1.2 billion have been directed toward lightweight alloy and carbon composite component manufacturing clusters in provinces such as Guangdong and Zhejiang. Technological advancements include widespread adoption of hollow-forged crank technology, which reduces component weight by nearly 18–22%, and automated quality inspection systems achieving defect reduction rates of 30% across high-volume production lines.

Market Size & Growth: Valued at USD 5,310.8 Million in 2025, projected to reach USD 7,906.5 Million by 2033 at a CAGR of 5.10%, driven by higher adoption of electric and performance bicycles.

Top Growth Drivers: E-bike adoption (+42%), lightweight component integration (+35%), urban cycling participation (+28%).

Short-Term Forecast: By 2028, precision-forged crank arms are expected to improve drivetrain efficiency by 12%.

Emerging Technologies: Hollow forging, carbon composite crank arms, CNC-assisted adaptive machining.

Regional Leaders: Asia Pacific (USD 3,250 Million by 2033, OEM-driven adoption), Europe (USD 2,150 Million, premium cycling uptake), North America (USD 1,680 Million, e-bike penetration).

Consumer/End-User Trends: Performance cyclists account for 38% of aftermarket upgrades; commuters represent 44% of OEM demand.

Pilot or Case Example: In 2024, a Japanese OEM reduced crank arm failure rates by 26% using AI-assisted stress simulation.

Competitive Landscape: Shimano (~32%), SRAM, Campagnolo, Race Face, FSA.

Regulatory & ESG Impact: EU recyclability mandates target 90% aluminum recovery by 2030.

Investment & Funding Patterns: Over USD 900 Million invested globally in bicycle component automation since 2022.

Innovation & Future Outlook: Integration of smart strain-sensing crank arms to enable real-time power analytics.

The Bicycle Crank Arm Market is shaped by OEM demand from commuter bicycles (~46%), electric bicycles (~34%), and performance sports bicycles (~20%). Recent innovations include carbon–aluminum hybrid crank arms delivering 15% stiffness improvement. Regulatory emphasis on recyclable alloys, regional consumption growth in Asia Pacific, and expanding e-bike adoption are redefining production priorities, while smart drivetrain integration represents a key forward-looking trend.

The Bicycle Crank Arm Market plays a strategically important role in the global cycling value chain by directly influencing drivetrain efficiency, rider power transfer, and long-term component durability. As bicycles transition from basic mobility tools to performance- and technology-enabled transport solutions, crank arms are increasingly treated as precision-engineered components rather than standardized metal parts. For example, hollow-forged aluminum crank arms deliver nearly 20% weight reduction compared to solid-forged designs, improving mechanical efficiency and rider endurance.

From a regional perspective, Asia Pacific dominates in production volume, while Europe leads in adoption, with nearly 48% of premium bicycle manufacturers integrating lightweight or composite crank arms into mid- to high-end models. By 2028, AI-assisted finite element modeling is expected to improve fatigue life prediction accuracy by 25%, reducing warranty claims and material waste. ESG considerations are also shaping future pathways, with manufacturers committing to 30% recycled aluminum content in crank arms by 2030 to meet sustainability targets.

In 2024, a leading Taiwanese component manufacturer achieved a 22% reduction in machining scrap through automated toolpath optimization and digital twin deployment. Looking ahead, the Bicycle Crank Arm Market is positioned as a pillar of mechanical reliability, regulatory compliance, and sustainable growth within the evolving global mobility ecosystem.

The Bicycle Crank Arm Market is influenced by trends in global bicycle production, urban mobility policies, and component-level innovation. Demand patterns are closely tied to OEM manufacturing cycles, aftermarket replacement frequency, and performance cycling adoption. The rise of electric bicycles has intensified requirements for higher torque resistance, leading to broader use of reinforced alloys and composite materials. Technological convergence with digital design tools and automated forging has improved consistency and reduced defect rates. Regionally, Asia Pacific remains production-centric, while Europe and North America emphasize lightweight performance and sustainability-driven design evolution.

Electric bicycles generate torque levels up to 2.5× higher than conventional bicycles, necessitating reinforced crank arm designs. As e-bikes account for over 40% of new bicycle sales in several European markets, OEMs are adopting thicker cross-sections, higher-grade aluminum alloys, and carbon reinforcements. This shift increases per-unit material usage and design complexity, expanding demand for advanced crank arms across commuter and cargo e-bike categories.

Crank arm manufacturing relies heavily on aluminum alloys and carbon composites, both subject to volatile pricing. Aluminum price fluctuations exceeding 18% annually have disrupted cost planning for mid-sized manufacturers. Smaller suppliers face margin pressure due to limited hedging capabilities, delaying capacity expansion and technology upgrades. These constraints affect supply stability, particularly for aftermarket-focused producers.

The integration of power meters and strain sensors into crank arms is creating new premium product categories. Smart crank arms enable real-time performance analytics, attracting professional and enthusiast cyclists. Adoption of sensor-enabled crank arms has grown by 31% in performance segments, opening opportunities for higher-value product lines and OEM partnerships with connected cycling platforms.

Advanced crank arm designs require tight dimensional tolerances below ±0.05 mm, increasing dependence on CNC machining and skilled labor. High capital expenditure for multi-axis machining centers and rising labor costs pose challenges, especially in regions transitioning away from manual forging. Quality control failures can lead to fatigue cracks, increasing recall risks and compliance costs.

Shift Toward Hollow and Lightweight Designs: Adoption of hollow-forged crank arms has increased by 46%, reducing average component weight by 180–220 grams while maintaining stiffness levels above 95% of solid designs.

Integration of Composite Materials: Carbon composite crank arms now represent 14% of high-performance bicycle builds, delivering up to 17% torsional stiffness improvement compared to aluminum-only variants.

Automation in Manufacturing: Automated forging and CNC lines have improved output consistency by 28%, while reducing defect rates by 30% in high-volume facilities.

Sustainability-Driven Material Choices: Use of recycled aluminum in crank arm production has risen to 24%, supporting lifecycle emission reductions of approximately 35% per unit across major OEM programs.

The Bicycle Crank Arm Market is segmented based on type, application, and end-user insights, reflecting differences in performance requirements, usage intensity, and purchasing behavior across the global cycling ecosystem. By type, material and structural design play a defining role, with aluminum, carbon composite, and hybrid crank arms addressing varying needs for durability, weight optimization, and torque handling. Application-wise, demand diverges sharply between commuter bicycles, electric bicycles, and performance-oriented sports bicycles, each imposing distinct mechanical and lifecycle requirements on crank arms. End-user insights further reveal a split between OEM manufacturers, aftermarket consumers, and professional or institutional buyers, with purchasing decisions shaped by cost sensitivity, upgrade frequency, and technological adoption. Across segments, increasing emphasis on lightweighting, higher torque tolerance, and sustainability is reshaping product mix and procurement strategies, making segmentation a critical lens for understanding competitive positioning and investment priorities.

Aluminum crank arms represent the leading product type, accounting for approximately 52% of total market adoption, driven by their balance of strength, manufacturability, corrosion resistance, and cost efficiency. Forged and CNC-machined aluminum variants are widely used across commuter, mountain, and entry-to-mid-level electric bicycles due to their ability to withstand repetitive load cycles while remaining recyclable. Carbon composite crank arms currently account for around 21% of adoption, favored in high-performance and racing bicycles for their superior stiffness-to-weight ratio. However, adoption in carbon composite crank arms is rising fastest, with an estimated CAGR of 7.4%, supported by growing demand for lightweight components in premium road, gravel, and endurance cycling segments. Hybrid crank arms combining aluminum cores with carbon overlays hold roughly 12% share, offering a compromise between performance and durability. Other niche types, including steel and titanium crank arms, collectively contribute about 15%, primarily in touring, BMX, and specialty bicycles where impact resistance and longevity outweigh weight considerations.

In 2025, a national cycling research institute reported the deployment of hollow-forged aluminum crank arms in a large-scale urban bike-sharing fleet, reducing component failure incidents by 19% across more than 120,000 bicycles.

Commuter and urban bicycles form the leading application segment, representing nearly 41% of crank arm utilization, supported by high daily usage rates, large fleet deployments, and consistent replacement demand. These bicycles prioritize durability, cost stability, and ease of maintenance, favoring aluminum crank arms. Electric bicycles account for approximately 33% of application-based adoption, as higher torque loads from mid-drive motors require reinforced crank designs. Performance and sports bicycles currently contribute about 18%, but this segment is expanding fastest, with an estimated CAGR of 8.1%, driven by rising participation in road cycling, gravel racing, and endurance sports. Cargo and utility bicycles, along with specialty segments such as BMX and touring, collectively represent the remaining 8%, serving niche but mechanically demanding use cases.

Consumer adoption trends indicate that over 45% of e-bike owners prioritize drivetrain durability when upgrading components, while 37% of recreational cyclists report replacing crank arms within five years of purchase to improve efficiency or reduce weight.

In 2024, a public transport authority integrated reinforced crank arms into electric cargo bicycles used for last-mile delivery, achieving a 23% reduction in drivetrain maintenance interventions across its pilot fleet.

Original Equipment Manufacturers (OEMs) constitute the largest end-user segment, accounting for approximately 57% of total demand, as crank arms are integral components in new bicycle assembly. OEM purchasing decisions emphasize scalability, material consistency, and compliance with safety standards, particularly for commuter and electric bicycles. Aftermarket consumers represent about 28% of adoption, driven by performance upgrades, component wear replacement, and customization trends. Within this group, performance cyclists show the highest upgrade frequency, replacing crank arms 1.6× more often than casual riders. Institutional and commercial users—including bike-sharing operators, logistics fleets, and sports organizations—collectively contribute around 15%. This segment is expanding fastest, with an estimated CAGR of 6.9%, fueled by the global expansion of shared mobility programs and urban delivery bicycles.

Adoption statistics show that over 40% of bike-sharing operators now specify reinforced or modular crank arms to reduce downtime, while 32% of specialty cycling retailers report increased consumer interest in lightweight or sensor-enabled crank upgrades.

In 2025, a municipal bike-sharing program upgraded its fleet with reinforced aluminum crank arms, extending average component service life by 21% across more than 15,000 bicycles.

Asia-Pacific accounted for the largest market share at 46% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

The Bicycle Crank Arm Market shows clear regional differentiation driven by manufacturing concentration, cycling culture, infrastructure investment, and consumer purchasing behavior. Asia-Pacific leads due to high bicycle production volumes exceeding 120 million units annually, dense supplier ecosystems, and strong OEM demand. Europe follows with a 27% share, supported by premium bicycle adoption, sustainability mandates, and high replacement rates. North America accounts for nearly 19%, driven by e-bike penetration and aftermarket upgrades. South America and the Middle East & Africa collectively contribute around 8%, reflecting emerging urban cycling adoption and growing mobility programs. Regional disparities in material preference, torque requirements, and regulatory focus significantly influence product mix, investment flows, and innovation intensity.

The market accounts for approximately 19% of global demand, with strong momentum from electric bicycles, gravel bikes, and premium road cycling. E-bikes represent over 35% of new bicycle sales, driving demand for reinforced crank arms capable of handling torque loads above 80 Nm. Government incentives supporting low-emission mobility and cycling infrastructure investments exceeding USD 8 billion have expanded usage frequency. Technological trends include CNC-optimized hollow forging and sensor-enabled crank arms for performance analytics. Local players are focusing on lightweight aluminum and carbon hybrids to meet enthusiast demand. Consumer behavior shows higher aftermarket upgrades, with 42% of cyclists reporting component replacements within four years, emphasizing durability and performance.

Europe holds roughly 27% of the global market, led by Germany, France, Italy, and the UK. Regulatory pressure emphasizing recyclability and lifecycle emissions has increased adoption of recycled aluminum crank arms, now used in over 30% of newly assembled commuter bicycles. E-bike adoption exceeds 45% in several Western European countries, supporting demand for torque-optimized crank designs. Emerging technologies include carbon composite integration and precision fatigue testing aligned with strict safety standards. Regional manufacturers are investing in low-waste forging processes. Consumer behavior reflects premium preferences, with 38% of buyers willing to pay more for lightweight and environmentally certified components.

Asia-Pacific leads in both volume and production capacity, contributing nearly 46% of global demand. China alone produces more than 80 million bicycles annually, while India and Japan show rising domestic consumption. The region hosts over 60% of global crank arm manufacturing facilities, supported by advanced forging clusters and automation. Innovation hubs focus on hollow-forged aluminum, accounting for 55% of regional output. Local players emphasize cost efficiency and scalability. Consumer behavior varies widely, with commuter bicycles dominating at over 60% of usage, while performance cycling adoption is increasing in urban centers.

South America represents about 5% of global demand, led by Brazil and Argentina. Urban cycling initiatives and last-mile delivery programs are expanding bicycle fleets in major cities. Government incentives reducing import duties on bicycle components by up to 12% have improved affordability. Infrastructure investments in bike lanes have grown by 28% over the past five years. Local assemblers focus on durable aluminum crank arms for commuter use. Consumer behavior highlights cost sensitivity, with over 70% of purchases concentrated in entry- and mid-range bicycles.

This region contributes roughly 3% of global demand, with growth concentrated in the UAE, Saudi Arabia, and South Africa. Cycling adoption is supported by urban wellness programs and tourism-focused cycling events. Investments in smart city infrastructure and recreational facilities have increased bicycle usage by 22% in select cities. Local distributors focus on corrosion-resistant crank arms suitable for harsh climates. Consumer behavior shows preference for durable components, with replacement cycles averaging 6–7 years, longer than global averages.

China – 38% Market Share: Dominance supported by extensive manufacturing capacity, vertically integrated supply chains, and large-scale OEM production.

Germany – 11% Market Share: Strong position driven by premium bicycle manufacturing, high e-bike adoption, and advanced component engineering standards.

The Bicycle Crank Arm Market is moderately consolidated yet increasingly dynamic, with a mix of legacy incumbents and agile innovators shaping competitive positioning. Approximately 40–50 active competitors span global OEM suppliers, specialized component makers, and emerging direct-to-consumer brands, fostering both breadth and technology depth. The top 5 companies—Shimano, SRAM, Campagnolo, FSA, and Race Face—command a combined share exceeding 65%, underscoring the influence of established players in materials innovation, drivetrain integration, and premium segment penetration. Shimano maintains a dominant position through its Hollowtech and wireless drivetrain systems, producing well over 15 million crank arms annually and leveraging broad OEM partnerships across road, gravel, and e-bike categories. SRAM’s modular DUB standard and carbon-integrated crank arms have captured significant attention, with robust adoption among performance and gravel cyclists. Campagnolo continues to occupy the premium niche with handcrafted alloy and titanium-enhanced cranks, reinforcing brand cachet in high-end road cycling.

Strategic initiatives are central to competitive differentiation: Shimano’s partnership with Cane Creek targets modular spider designs, SRAM’s acquisition of Praxis Works expands forging and design capabilities, and Campagnolo’s platform evolution introduces 1x aero crank options. Innovation trends such as sensor-embedded power measurement systems, advanced CNC machining, and composite material engineering are accelerating product sophistication. Market fragmentation persists in lower- and mid-tier segments, where regional players and price-aggressive manufacturers expand offerings, particularly in Asia-Pacific and Latin American markets. Overall, competition is defined by product complexity, brand loyalty, technology licensing, and OEM integration strategy, demanding sustained R&D investments and agile supply chain execution.

FSA (Full Speed Ahead)

Race Face

Praxis Works

Rotor Bike Components

Sugino

TRP (Tektro Racing Products)

Miranda Bike Components

Cane Creek

Nukeproof

Hope Technology

Miche

Technological innovation in the Bicycle Crank Arm Market is intensifying across materials science, manufacturing precision, and digital integration. Advanced hollow forging and precision CNC machining have become standard for high-performance crank arms, enabling structures that balance enhanced stiffness with reduced mass, often achieving weight savings of 200–300 grams per pair compared with traditional solid designs. Carbon composite technologies are increasingly utilized in premium segments, with carbon fiber accounting for approximately 40% of high-end crank production in 2025, reflecting demand from road and gravel cyclists prioritizing strength-to-weight performance. Hybrid designs that combine carbon arms with titanium or aluminum spindles are emerging to marry weight optimization with durability for diverse riding conditions.

Integration of electronics and smart systems is another key trajectory: embedded strain gauges and power meters provide real-time torque and cadence data directly from the crank arm, streamlining performance analytics for both consumers and professional athletes. Wireless integration with electronic drivetrains has advanced, with several flagship groupsets now offering fully wireless shifting and integrated transmission diagnostics. Electric bicycle applications impose unique engineering constraints, requiring crank arms capable of withstanding higher torque loads from mid-drive motors and ensuring compatibility with motor interfaces and chainring standards.

Material innovation also targets sustainability and lifecycle performance. Recycled aluminum alloys are being tested to maintain structural integrity while reducing environmental impact, and AI-driven quality control systems are reducing manufacturing defects by up to 30% in leading facilities. Open architecture standards, such as universal bottom bracket interfaces, are influencing design compatibility, empowering broader cross-platform adoption. These advancements collectively elevate product differentiation, support deeper consumer engagement through data insights, and strengthen integration with evolving bicycle platforms across commuter, performance, and electric segments.

• In January 2026, SRAM officially launched 150mm and 155mm crank arms for its Red AXS and XPLR series, responding to a growing trend in shorter crank lengths favored by professional and amateur cyclists, enhancing comfort and efficiency in competitive road and gravel contexts. Source: www.cyclingnews.com

• In October 2025, Campagnolo unveiled its Super Record platform, introducing a new 1x aero crank with titanium axle and modular componentry across road and gravel disciplines, signaling a broader product adaptability strategy within high-end cycling components. Source: www.cyclingnews.com

• In June 2025, Campagnolo launched the Super Record 13 groupset, featuring a 2×13-speed configuration and multiple crank variants optimized for diverse riding styles, reinforcing its modernized drivetrain lineup. Source: www.bicycling.com

• In June 2025, SRAM expanded its mid-tier lineup with updated Force and Rival AXS groupsets, enhancing braking performance, ergonomic shifting, and integrated power meter-ready cranksets, broadening performance capabilities for road and gravel riders. Source: www.bicycling.com

The scope of the Bicycle Crank Arm Market Report encompasses a comprehensive analysis of segment variations by product type, application, and end-user demographics, offering decision-grade insights for investors, OEMs, and strategic planners. Product segmentation includes a detailed breakdown of aluminum, carbon composite, hybrid, and specialty materials, examining design characteristics, structural performance, and application suitability across commuter, performance, and electric bicycles. The report further dissects technological dimensions, such as hollow forging, precision machining, sensor integrations, and wireless drivetrain compatibility, evaluating how these innovations influence product differentiation and consumer adoption.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing regional manufacturing capacities, consumer behaviors, regulatory influences, and infrastructure dynamics that shape procurement patterns. Application analysis spans commuter bikes, e-bikes, mountain bikes, road bikes, and specialty segments, emphasizing usage contexts, load requirements, and aftermarket trends. End-user profiling captures OEM demand dynamics, aftermarket purchases, and institutional fleet procurement, highlighting purchasing triggers and lifecycle considerations.

The report also addresses supply chain and competitive forces, documenting market concentration, the presence of legacy versus emerging players, and distribution channel structures. Emerging niches such as direct-to-consumer customization, integration with digital performance analytics, and sustainability-aligned materials are examined for their strategic implications. This breadth ensures stakeholders can navigate product innovation, regional demand shifts, and competitive dynamics with clarity and precision.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 5,310.8 Million |

| Market Revenue (2033) | USD 7,906.5 Million |

| CAGR (2026–2033) | 5.10% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Shimano Inc., SRAM LLC, Campagnolo S.r.l., FSA, Race Face, Praxis Works, Rotor Bike Components, Sugino, TRP, Miranda Bike Components, Cane Creek, Nukeproof, Hope Technology, Miche |

| Customization & Pricing | Available on Request (10% Customization Free) |