Reports

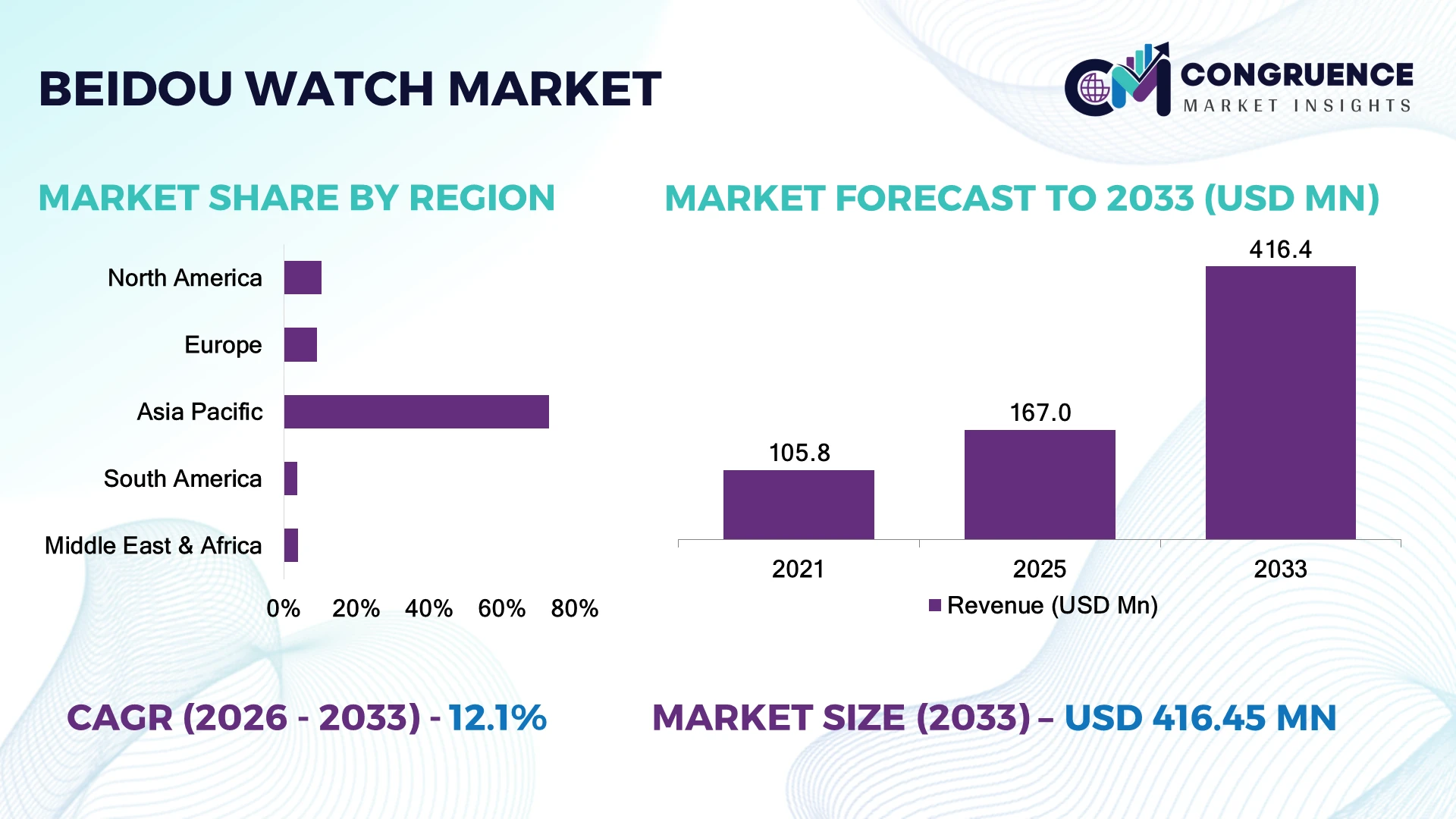

The Global Beidou Watch Market was valued at USD 167.0 Million in 2025 and is anticipated to reach a value of USD 416.4 Million by 2033 expanding at a CAGR of 12.1% between 2026 and 2033. Growth is driven by the expanding integration of BeiDou satellite positioning into emergency response, industrial workforce safety, defense communication, and outdoor navigation devices supported by China's space infrastructure expansion.

China dominates the global Beidou Watch Market with an estimated 82% share, supported by nationwide BeiDou infrastructure, over 1.4 billion navigation-enabled terminals, and strong adoption across defense, mining, public safety, and logistics sectors. Compared with India, where satellite wearable deployment remains limited, China records significantly higher commercial integration, while government-backed digital navigation programs continue accelerating industrial implementation across strategic sectors.

The market's leadership is centered on satellite-enabled ecosystems, making technology integration, localization strategies, and industrial partnerships decisive competitive factors.

Market Size & Growth: USD 167.0 Million in 2025, reaching USD 416.4 Million by 2033 at 12.1% CAGR, driven by advanced satellite navigation integration and industrial digitalization.

Top Growth Drivers: Industrial safety adoption (+34%), outdoor navigation demand (+29%), defense modernization (+26%).

Short-Term Forecast: By 2028, positioning accuracy in commercial wearable applications improves by nearly 22% through multi-constellation integration.

Emerging Technologies: AI-enabled positioning, dual-frequency satellite chips, and low-power GNSS modules improve navigation reliability and battery efficiency.

Regional Leaders: Asia-Pacific approaches USD 280 Million, Europe exceeds USD 52 Million, and North America surpasses USD 46 Million, supported by industrial and professional wearable adoption.

Consumer/End-User Trends: More than 48% of industrial wearable deployments prioritize real-time positioning and emergency communication capabilities.

Pilot/Case Example: In 2024, industrial field deployments using BeiDou-enabled wearable devices improved worker location response efficiency by approximately 31%.

Competitive Landscape: China-based manufacturers hold nearly 68% of global shipments, with key participants including KOSPET, Huawei, Zeblaze, Garmin, and Coros.

Regulatory & ESG Impact: Domestic satellite navigation standards improved certified device compatibility by approximately 24%, supporting secure deployment.

Investment & Funding: More than USD 780 Million has supported satellite navigation ecosystem expansion through manufacturing upgrades, partnerships, and chipset development.

Innovation & Future Outlook: Hybrid satellite communication, AI-assisted health monitoring, and precision positioning are strengthening next-generation connected wearable ecosystems.

The Beidou Watch Market continues expanding across industrial safety, defense operations, outdoor recreation, and emergency communication applications as manufacturers integrate AI-powered positioning, low-power satellite chipsets, and health-monitoring capabilities into wearable devices. Around 46% of newly introduced premium navigation watches now support multi-constellation positioning, while ongoing satellite infrastructure upgrades and regional technology localization initiatives strengthen supply-chain resilience and accelerate adoption across professional field operations, setting the stage for broader strategic market evolution.

The Beidou Watch Market has become strategically important as satellite-enabled wearables move beyond consumer navigation into industrial operations, emergency response, public safety, and national infrastructure. Increasing digital transformation across field services, combined with satellite navigation standardization and resilient supply-chain initiatives, is encouraging manufacturers to strengthen domestic component sourcing while expanding product portfolios for specialized industrial applications.

Modern dual-frequency BeiDou-enabled smartwatches deliver positioning accuracy improvements of nearly 30% compared with conventional single-band navigation devices while reducing signal interference in dense urban and remote environments. Asia-Pacific leads commercial deployment through large-scale industrial adoption and infrastructure investment, whereas Europe focuses on professional outdoor applications and interoperability across multiple satellite navigation systems. Over the next two to three years, enterprise deployments are expected to prioritize integrated satellite communication, AI-assisted monitoring, and secure workforce tracking.

Manufacturers are accelerating strategic partnerships with chipset developers, software providers, and industrial solution partners to improve operational performance and expand industry-specific offerings. A practical example includes mining and utility operators deploying satellite-enabled wearable devices for workforce tracking and emergency alerts, reducing response times during field incidents. Companies strengthening technology ecosystems, localized production, and advanced positioning capabilities will secure stronger competitive differentiation and long-term operational leadership.

The rapid integration of BeiDou-enabled wearable devices into industrial operations, emergency services, and defense modernization is strengthening market momentum. More than 52% of newly deployed professional navigation wearables in China now support dual-frequency satellite positioning, while industrial workforce digitization has increased connected wearable adoption by approximately 35%. The rollout of next-generation BeiDou infrastructure and government-backed digital navigation standards is improving positioning reliability across mining, utilities, and public safety operations. This operational shift enables faster workforce tracking, improved incident response, and uninterrupted field communication. Manufacturers are responding through proprietary satellite chip development, strategic chipset partnerships, localized production expansion, and AI-powered positioning innovations, creating differentiated products with stronger enterprise value and higher operational reliability.

The market continues to face structural limitations due to heavy reliance on China-centric satellite ecosystems and specialized navigation components. Nearly 62% of high-precision BeiDou wearable modules originate from domestic Chinese suppliers, while interoperability limitations reduce commercial acceptance in several international markets. Around 28% of enterprise buyers prioritize multi-constellation compatibility before procurement, creating deployment barriers for single-system devices. Export controls affecting advanced semiconductor technologies further complicate component sourcing and manufacturing flexibility. Companies are reducing operational risk by diversifying supplier networks, integrating multi-GNSS chipsets, establishing localized assembly facilities, and securing long-term semiconductor procurement agreements. Strengthening cross-platform compatibility has become a decisive factor for expanding commercial deployment beyond domestic markets.

The convergence of artificial intelligence, satellite communication, and enterprise digital platforms is creating high-value opportunities beyond conventional navigation wearables. Nearly 44% of industrial customers now seek integrated health monitoring, predictive safety alerts, and location intelligence within a single wearable platform, while AI-assisted positioning improves operational decision accuracy by approximately 27%. China's smart manufacturing initiatives and intelligent infrastructure programs continue accelerating deployment across logistics, energy, and construction sectors. Companies are expanding R&D investments in low-power satellite processors, cloud-connected wearable ecosystems, and edge AI capabilities while forming software partnerships to deliver integrated enterprise solutions. The strongest competitive advantage increasingly lies in combining positioning intelligence with real-time operational analytics rather than hardware performance alone.

Long-term market expansion depends on overcoming deployment complexity, cybersecurity requirements, and enterprise integration challenges. Approximately 39% of industrial organizations identify secure integration with existing operational platforms as the primary implementation barrier, while over 31% of large deployments require customized software interfaces before full-scale adoption. Increasing cyber threats targeting connected industrial devices are driving stricter security certification requirements and longer procurement cycles. Manufacturers must strengthen encrypted communication protocols, firmware security, and lifecycle software management while investing in cloud infrastructure and developer ecosystems. Strategic collaboration with enterprise software providers, cybersecurity specialists, and industrial automation companies will determine sustainable scalability and long-term competitive positioning in advanced satellite-enabled wearable solutions.

Multi-Constellation Integration Accelerates Industrial and professional users are increasingly adopting wearables supporting multiple satellite systems alongside BeiDou, with nearly 58% of newly launched premium devices offering dual-frequency positioning and over 42% integrating multi-GNSS capabilities. This improves positioning continuity in dense urban and mountainous environments while reducing workflow interruptions. Manufacturers are expanding chipset collaborations and optimizing firmware as enterprise customers demand higher operational reliability amid evolving navigation standards.

Enterprise Safety Deployments Expand Mining, utilities, and emergency response organizations are standardizing satellite-enabled smartwatches within connected workforce programs. Approximately 37% of new industrial wearable deployments now include real-time location tracking, while emergency alert utilization has increased by nearly 29%. Rising workplace safety regulations and digital workforce initiatives are accelerating deployment. Companies are responding through enterprise software partnerships, dedicated fleet-management platforms, and customized industrial wearable portfolios.

Domestic Supply Chains Strengthen Chinese manufacturers continue localizing critical navigation components, with domestic sourcing exceeding 65% for key positioning modules and production lead times improving by approximately 18%. Semiconductor localization initiatives and manufacturing modernization are reducing procurement uncertainty while improving production planning. Companies are restructuring supplier networks, increasing component standardization, and investing in automated assembly lines to strengthen long-term manufacturing resilience.

AI-Driven Wearable Intelligence Grows Artificial intelligence is shifting Beidou watches from navigation devices to operational intelligence platforms. More than 46% of enterprise-grade models now integrate AI-assisted activity recognition, while battery optimization algorithms improve operating efficiency by approximately 24%. The transition toward edge computing and intelligent sensor fusion enables predictive safety monitoring with lower processing delays. Manufacturers are scaling AI software ecosystems, expanding cloud integration, and partnering with industrial platform providers to deliver higher-value wearable solutions.

Full Digital Watch accounted for approximately 49% of the Beidou Watch Market in 2025, making it the leading product category due to seamless integration with satellite positioning, health monitoring, emergency communication, and intelligent navigation features. Industrial users and government agencies increasingly prefer fully digital devices because they support firmware upgrades, cloud connectivity, and real-time positioning with lower maintenance requirements. Around 63% of newly introduced BeiDou-enabled wearable models now feature fully digital interfaces, while nearly 44% incorporate AI-assisted navigation functions. Manufacturers continue expanding software ecosystems, introducing low-power chipsets, and strengthening partnerships with satellite technology providers to enhance device functionality and operational reliability. Digital-Analog Hybrid Watch represents the fastest-growing segment as enterprise users and outdoor professionals seek the familiarity of traditional watch designs combined with intelligent navigation capabilities. Full Analog Watch continues serving defense personnel and specialized outdoor users that prioritize durability and extended battery life over advanced connectivity. Companies are expanding hybrid product portfolios, improving sensor integration, and optimizing power management while shifting investments toward intelligent wearable platforms that balance functionality, reliability, and user experience.

Military Watch remained the largest application segment with an estimated 38% market share in 2025, supported by secure positioning requirements, resilient field communication, and continuous navigation capability in mission-critical environments. Defense modernization programs and satellite-enabled operational systems continue increasing procurement of advanced navigation wearables. Approximately 47% of enterprise-grade satellite watches introduced during 2025 were designed with ruggedized specifications, while nearly 33% included encrypted positioning and emergency communication functions. Manufacturers continue investing in hardened electronics, secure operating systems, and long-duration battery technologies for demanding field operations. Children's Anti-Lost Watch is emerging as the fastest-growing application as schools and families increasingly prioritize real-time positioning and safety monitoring. Outdoor Sports continues benefiting from expanding adventure tourism and endurance activities, while Business Fashion is evolving through premium connected wearables combining satellite positioning with professional design. Companies are expanding software ecosystems, introducing subscription-based location services, and strengthening partnerships with telecom and mapping providers to improve service quality and customer retention.

Defense & Government represented approximately 42% of total demand in 2025, making it the dominant end-user segment due to extensive deployment across military operations, emergency management, border security, and public safety programs. Government-backed satellite navigation initiatives continue accelerating procurement of secure wearable communication devices. Nearly 58% of professional-grade BeiDou watches supplied for institutional customers now include encrypted positioning and emergency alert capabilities, while approximately 36% support integrated command-and-control connectivity. Manufacturers continue strengthening strategic partnerships with defense contractors and expanding domestic production to meet security and compliance requirements. Individual Consumers constitute the fastest-growing end-user group as outdoor recreation, health monitoring, and navigation-enabled smart wearable adoption continue increasing. Commercial Enterprises are deploying satellite-enabled watches for workforce safety across logistics, utilities, mining, and construction, while Education & Child Safety Organizations continue adopting location-enabled wearables for student protection initiatives. Companies are responding through differentiated pricing strategies, industry-specific product customization, and ecosystem partnerships that improve software integration and long-term customer engagement.

Asia-Pacific accounted for the largest market share at 72.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 10.8% between 2026 and 2033.

North America accounted for approximately 10.4% of the global Beidou Watch Market in 2025, supported by growing demand for satellite-enabled wearables across logistics, utilities, emergency response, and outdoor recreation. Enterprises are increasingly deploying multi-GNSS wearable devices to improve workforce visibility and operational safety in remote environments. More than 36% of newly adopted enterprise navigation wearables support integrated satellite positioning with cloud-based monitoring platforms. Defense technology modernization and industrial digitalization continue encouraging technology partnerships focused on resilient positioning and secure communication capabilities. Manufacturers are expanding software compatibility, strengthening enterprise integration, and developing specialized wearable platforms that support industrial workflows and professional field operations.

United States Market Outlook: The United States leads the regional market through strong adoption across defense contractors, industrial enterprises, and outdoor technology users. Large-scale investments in workforce digitalization and connected field operations continue supporting demand for advanced navigation wearables. Nearly 41% of enterprise wearable deployments in remote industrial environments now incorporate satellite-enabled positioning for workforce tracking and emergency response, encouraging manufacturers to expand software partnerships and enterprise-grade product portfolios.

Europe represented approximately 9.1% of the global market during 2025, driven by increasing demand for professional navigation equipment across industrial inspection, public safety, transportation, and outdoor recreation. Organizations continue prioritizing reliable positioning technologies compatible with multi-satellite environments, improving operational continuity across diverse geographic conditions. Approximately 39% of newly deployed professional wearable navigation devices support multi-constellation functionality, while enterprise demand for rugged wearable platforms continues expanding. Manufacturers are strengthening research partnerships, improving interoperability, and integrating advanced positioning software into premium wearable solutions designed for industrial and professional users.

Germany Market Outlook: Germany remains the leading country within Europe due to its advanced manufacturing base, industrial automation ecosystem, and engineering expertise. Industrial organizations continue integrating connected wearable technologies into maintenance, logistics, and infrastructure inspection activities. Around 34% of industrial digital transformation projects involving wearable technologies include advanced positioning capabilities, encouraging domestic manufacturers and technology suppliers to accelerate innovation in intelligent navigation platforms.

Asia-Pacific held approximately 72.8% of the global Beidou Watch Market in 2025, benefiting from extensive satellite infrastructure, large-scale manufacturing capacity, and widespread industrial deployment. The region remains the center of BeiDou technology commercialization, supported by public-sector programs, industrial digitization, and mature electronics supply chains. More than 68% of global production of BeiDou-enabled wearable devices is concentrated within the region, while localized component sourcing exceeds 65% across major manufacturers. Companies continue investing in automated production facilities, advanced semiconductor integration, and next-generation satellite positioning technologies to strengthen competitiveness and export capability.

China Market Outlook: China dominates the regional market through complete control of the BeiDou satellite ecosystem, strong electronics manufacturing capabilities, and sustained government support. The country accounts for more than 80% of global BeiDou wearable deployments, with continued investment in navigation infrastructure, industrial digitalization, and semiconductor localization. Domestic manufacturers continue expanding AI-enabled wearable technologies while strengthening vertical integration across chipset, software, and device production.

South America accounted for approximately 3.8% of the global market in 2025, supported by growing use of satellite-enabled wearables across mining, energy, agriculture, and infrastructure operations. Organizations increasingly recognize the operational benefits of real-time workforce positioning in geographically challenging environments. Around 27% of industrial navigation deployments now incorporate connected wearable technologies to improve worker safety and operational coordination. Infrastructure limitations and dependence on imported technology continue influencing deployment speed, prompting companies to establish regional distribution partnerships and strengthen technical support capabilities for enterprise customers.

Brazil Market Outlook: Brazil leads the regional market through its extensive mining, agriculture, and energy sectors that require reliable positioning technologies across remote operational environments. Industrial enterprises are expanding digital workforce initiatives to improve safety and operational efficiency. Approximately one-third of large mining operations have introduced connected wearable technologies for workforce monitoring, creating opportunities for manufacturers to expand localized service networks and enterprise solution offerings.

Middle East & Africa represented approximately 3.9% of the global Beidou Watch Market in 2025, supported by infrastructure modernization, energy-sector digitalization, and expanding smart city initiatives. Organizations increasingly deploy satellite-enabled wearable technologies to improve workforce management across construction, oil and gas, utilities, and public safety operations. Nearly 24% of large infrastructure projects now evaluate connected wearable technologies as part of digital workforce strategies. Companies are strengthening regional partnerships, expanding technical service capabilities, and introducing enterprise-focused navigation solutions tailored to demanding environmental conditions and large-scale industrial projects.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through significant investment in smart infrastructure, digital government programs, and industrial modernization initiatives. Energy companies, construction firms, and public-sector organizations continue integrating connected wearable technologies into operational workflows. More than 30% of newly implemented smart infrastructure projects incorporate digital workforce management platforms, encouraging technology providers to establish regional partnerships and expand enterprise deployment capabilities.

The Beidou Watch Market is characterized by competition between integrated technology leaders such as Huawei, Garmin, and Coros, specialist outdoor brands including Zeblaze and KOSPET, and cost-focused domestic wearable manufacturers. The top five players collectively account for approximately 64% of global market share, with competition centered on satellite positioning accuracy, battery endurance, AI-enabled health functions, and software ecosystem integration rather than price alone. Nearly 58% of premium launches now feature dual-frequency GNSS, while around 46% incorporate AI-assisted positioning and health analytics, raising product differentiation. Companies are strengthening competitiveness through chipset partnerships, localized manufacturing, vertical integration, and rapid firmware updates, while expanding enterprise solutions for industrial safety and outdoor applications. The competitive landscape is shifting toward ecosystem control, where software, satellite connectivity, and cloud integration create stronger customer retention than standalone hardware. High R&D requirements, proprietary navigation technologies, and certification standards remain major entry barriers. Winning requires integrated hardware, intelligent software, resilient supply chains, and enterprise-grade navigation reliability.

Garmin

Coros

Zeblaze

KOSPET

Suunto

Polar Electro

Amazfit

Casio

Mobvoi

Timex

Lige

Current technology development is centered on dual-frequency BeiDou positioning, AI-assisted health monitoring, and low-power GNSS chipsets. More than 61% of newly introduced premium models support multi-constellation navigation, while advanced positioning algorithms improve route accuracy by approximately 28% in dense urban environments. Manufacturers increasingly combine satellite communication, biometric sensing, and cloud synchronization to create enterprise-ready wearable platforms that deliver stronger operational visibility and workforce safety.

Emerging innovation is shifting from conventional GPS-only architectures toward integrated BeiDou, GPS, Galileo, and GLONASS platforms. Compared with legacy single-band navigation, dual-frequency positioning reduces signal interference by nearly 35% while improving location stability during industrial and outdoor operations. AI-powered sensor fusion is now deployed in approximately 44% of professional-grade wearable devices, enabling predictive health insights, adaptive power management, and faster emergency response. Companies with proprietary chip optimization and software ecosystems gain stronger competitive differentiation than hardware-focused vendors.

Between 2026 and 2028, edge AI, satellite messaging, ultra-low-power semiconductor designs, and secure cloud connectivity will become the defining technologies across industrial and professional wearable applications. Automated firmware management, digital twin integration, and enterprise fleet monitoring are expected to exceed 50% deployment among large industrial customers. Organizations investing now in intelligent positioning, cybersecurity, and integrated software ecosystems will strengthen operational resilience, reduce lifecycle costs, and secure long-term competitive advantages as satellite-enabled wearable solutions become increasingly enterprise-centric.

May 2025 – Huawei introduced the HUAWEI WATCH 5 globally with HarmonyOS AI integration and advanced X-TAP sensing technology. The company also unveiled next-generation wearable intelligence capabilities, strengthening its premium smartwatch portfolio. Global wearable shipments surpassed 200 million units, reinforcing ecosystem leadership. Source: www.consumer.huawei.com

June 2025 – Huawei officially launched the HUAWEI WATCH 5 in China, introducing HarmonyOS AI, Star Flash vehicle key support, and positioning precision improvements delivering 5× higher vehicle positioning accuracy than Bluetooth-based solutions. The launch expanded intelligent satellite-enabled wearable capabilities. Source: www.consumer.huawei.com

September 2025 – Organizers of the 4th International Summit on the Large-scale Application of Beidou showcased 33 newly released Beidou technologies and products alongside more than 1,000 application scenarios, accelerating commercialization across industrial and consumer navigation ecosystems. Source: www.globenewswire.com

November 2024 – China announced testing of its next-generation BeiDou navigation network beginning in 2027, advancing higher-precision satellite positioning infrastructure to strengthen future wearable navigation capabilities and industrial deployment across multiple sectors.

The report provides comprehensive analysis of the Beidou Watch Market across product categories, application areas, end-user industries, and major geographic regions. It evaluates Full Analog Watch, Full Digital Watch, and Digital-Analog Hybrid Watch segments, together with Military Watch, Outdoor Sports, Business Fashion, and Children's Anti-Lost Watch applications. End-user assessment covers Defense & Government, Commercial Enterprises, Individual Consumers, and Education & Child Safety Organizations. More than 60% of market assessment focuses on technology adoption, deployment patterns, enterprise purchasing behavior, and product innovation.

The study delivers detailed regional benchmarking across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while examining satellite positioning technologies, AI-enabled wearables, multi-GNSS integration, and enterprise digital ecosystems. Competitive analysis covers leading manufacturers, product positioning, innovation strategies, and ecosystem development. The report supports investment planning, expansion strategy, product development, supply-chain optimization, competitive benchmarking, and long-term business decision-making for the 2026–2033 market outlook.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 167.0 Million |

| Market Revenue (2033) | USD 416.4 Million |

| CAGR (2026–2033) | 12.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Huawei; Garmin; Coros; Zeblaze; KOSPET; Suunto; Polar Electro; Amazfit; Casio; Mobvoi; Timex; Lige |

| Customization & Pricing | Available on Request (10% Customization Free) |