Reports

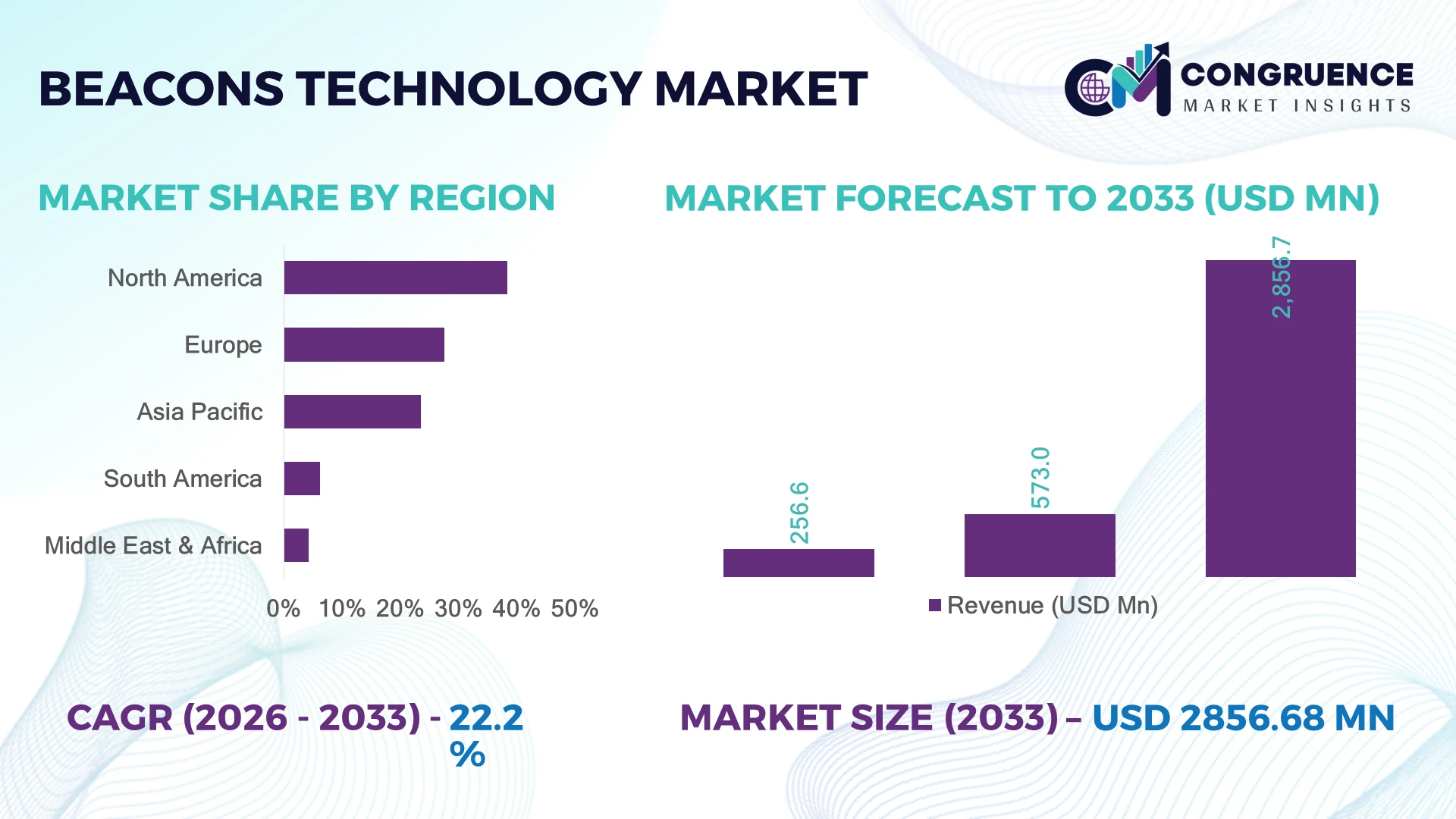

The Global Beacons Technology Market was valued at USD 573.0 Million in 2025 and is anticipated to reach a value of USD 2,856.7 Million by 2033 expanding at a CAGR of 22.24% between 2026 and 2033. Growth is driven by expanding indoor location services, smart retail engagement platforms, industrial asset tracking, and rising deployment of Bluetooth Low Energy (BLE) infrastructure across healthcare, transportation, and logistics environments.

The United States dominates the global market with approximately 34% share, supported by widespread deployment across retail, airports, hospitals, and smart buildings, alongside more than 7,000 large retail locations using proximity marketing solutions. Strong investments in digital infrastructure and Industry 4.0 initiatives accelerate enterprise adoption, while Germany leads European industrial deployment through manufacturing digitization, creating a clear technology adoption advantage over several emerging economies. Ongoing smart infrastructure investments and digital transformation policies continue strengthening large-scale beacon implementation.

For market participants, prioritizing scalable BLE ecosystems, software integration capabilities, and industry-specific location intelligence solutions will be critical for sustaining long-term competitive differentiation.

Market Size & Growth: USD 573.0 Million (2025) to USD 2,856.7 Million (2033) at 22.24% CAGR, driven by accelerated BLE deployment and enterprise digital transformation.

Top Growth Drivers: Retail proximity engagement (+38%), indoor navigation adoption (+31%), industrial asset tracking (+29%).

Short-Term Forecast: By 2028, enterprise location accuracy improves over 40% while asset search time declines nearly 35% through AI-enabled beacon management.

Emerging Technologies: AI analytics, Bluetooth 5.x, ultra-low-power chipsets, and cloud-based location intelligence enhance real-time operational visibility.

Regional Leaders: North America (~USD 1.02 Billion), Europe (~USD 760 Million), Asia-Pacific (~USD 690 Million), supported by smart infrastructure and regional digital expansion.

Consumer/End-User Trends: More than 62% of organized retailers are expanding personalized in-store engagement using proximity-based mobile experiences.

Pilot/Case Example: In 2024, a smart airport deployment reduced passenger navigation time by 28% through integrated beacon navigation systems.

Competitive Landscape: Top vendors collectively control about 48% of the market, led by Kontakt.io, HID Global, Estimote, Gimbal, and BlueCats.

Regulatory & ESG Impact: Smart building initiatives lowered facility energy consumption by nearly 15% while supporting digital infrastructure modernization.

Investment & Funding: More than USD 900 Million has been directed toward IoT infrastructure, enterprise partnerships, and intelligent location platform expansion amid global supply-chain digitization.

Innovation & Future Outlook: AI-powered edge analytics, digital twins, and interoperable IoT ecosystems are strengthening enterprise location intelligence and operational automation.

The Beacons Technology Market is expanding across retail, healthcare, manufacturing, airports, logistics, and smart buildings where precise indoor positioning and contextual engagement improve operational efficiency. AI-enabled location analytics, Bluetooth 5.x innovation, and edge computing continue enhancing deployment performance, while nearly 45% of new enterprise IoT projects now incorporate indoor location capabilities. Ongoing smart infrastructure modernization and enterprise digitalization are reinforcing demand, setting the stage for broader strategic adoption.

Beacons technology has become a strategic enabler for enterprises seeking precise indoor visibility, automated customer engagement, and intelligent asset management. Organizations are integrating beacon infrastructure into broader IoT and digital workplace strategies to improve operational responsiveness and decision-making. Continued smart infrastructure modernization, warehouse automation, and digital public infrastructure programs are accelerating deployment across transportation hubs, healthcare facilities, and commercial real estate.

Modern Bluetooth Low Energy beacon platforms deliver nearly 45% lower power consumption than many legacy wireless location systems while reducing deployment complexity and maintenance requirements. North America continues leading large-scale enterprise implementations across retail and healthcare, whereas Asia-Pacific is rapidly expanding installations through smart city projects, manufacturing modernization, and logistics digitization. Over the next two to three years, enterprise deployments are expected to increasingly integrate AI-driven location analytics and cloud-based management platforms to improve workforce productivity and operational visibility.

Large retailers and airport operators are combining beacon networks with mobile applications, digital signage, and analytics platforms to deliver personalized navigation and real-time operational intelligence. Technology providers are strengthening software partnerships, expanding managed service offerings, and investing in interoperable IoT ecosystems. Organizations that establish scalable, secure, and data-driven beacon infrastructure today will strengthen competitive positioning while enabling long-term operational efficiency and intelligent digital transformation.

Enterprise demand for precise indoor positioning and real-time asset visibility is driving rapid deployment of beacon ecosystems across retail, healthcare, manufacturing, and transportation. More than 65% of large retailers are expanding location-based engagement initiatives, while warehouse operators report inventory search time reductions exceeding 30% through BLE-enabled tracking. In the United States, smart logistics investments and digital warehouse modernization are accelerating beacon integration with AI-powered analytics and IoT platforms. This operational shift improves workforce productivity, customer engagement, and inventory accuracy. Technology providers are responding through cloud-native beacon management platforms, strategic partnerships with enterprise software vendors, and expanded interoperability with edge computing infrastructure, enabling scalable deployments that deliver measurable operational intelligence rather than isolated proximity services.

Fragmented wireless standards, legacy enterprise infrastructure, and integration complexity continue limiting large-scale beacon deployments. Nearly 42% of enterprise buyers identify interoperability with existing IoT ecosystems as a primary deployment barrier, while implementation and system integration account for approximately 35% of total project expenditure. Germany's industrial facilities frequently require upgrades to legacy automation networks before supporting advanced location services, extending deployment timelines. These structural constraints reduce implementation speed, increase project costs, and complicate cross-site scalability. Companies are mitigating risks through standardized Bluetooth 5.x architectures, multi-vendor compatibility programs, localized implementation partnerships, and long-term service agreements that simplify migration while improving operational consistency across distributed enterprise environments.

The convergence of AI, digital twins, and intelligent infrastructure is creating high-value opportunities beyond conventional proximity marketing. More than 55% of smart building projects now incorporate indoor positioning capabilities, while predictive asset management can improve equipment utilization by nearly 25% through continuous location intelligence. Japan's smart manufacturing initiatives are accelerating adoption of beacon-enabled production monitoring integrated with edge AI and industrial IoT platforms. Companies are expanding R&D investments, forming ecosystem partnerships with cloud providers, and developing software-defined location intelligence platforms capable of supporting autonomous facilities. A significant strategic opportunity lies in combining beacon-generated spatial data with enterprise analytics to optimize workflows, compliance monitoring, and real-time operational decision-making across complex industrial environments.

As beacon deployments expand across multiple facilities and industries, maintaining secure, unified, and scalable location intelligence presents a significant execution challenge. Approximately 48% of enterprises identify cybersecurity and device authentication as key concerns, while managing thousands of distributed beacon endpoints can increase administrative workloads by over 30% without centralized orchestration. In the United States, stricter enterprise cybersecurity frameworks require stronger encryption, identity management, and continuous device monitoring for connected infrastructure. These requirements increase implementation complexity and long-term operational costs. Technology providers must strengthen centralized management software, zero-trust security architectures, automated device lifecycle management, and cross-platform interoperability to ensure resilient deployments that remain competitive as enterprise IoT ecosystems continue expanding.

AI-Powered Indoor Intelligence Enterprise deployments are increasingly combining beacons with AI-driven analytics to enhance indoor positioning, customer engagement, and workforce visibility. More than 58% of new enterprise location projects now integrate AI-based analytics, while location accuracy has improved by nearly 35% through Bluetooth 5.x enhancements. Large retailers in the United States are expanding cloud-managed beacon networks, enabling faster campaign execution, automated asset monitoring, and more efficient customer flow management across multi-site operations.

Industrial Asset Tracking Expansion Manufacturing and logistics operators are shifting from manual inventory monitoring to real-time beacon-enabled asset visibility. Smart warehouse deployments have reduced equipment search time by over 32%, while inventory accuracy has improved by approximately 27%. Labor shortages and warehouse automation initiatives are accelerating adoption, prompting technology providers to expand industrial partnerships and integrate beacon platforms with warehouse management and enterprise resource planning systems.

Smart Infrastructure Integration Airports, hospitals, and commercial buildings are embedding beacon infrastructure into broader smart facility modernization programs. More than 45% of newly digitized facilities now include indoor navigation or occupancy monitoring capabilities, while facility response times have improved by nearly 24% through automated location intelligence. Enterprises are standardizing interoperable Bluetooth ecosystems to simplify maintenance and strengthen operational resilience across distributed infrastructure.

Privacy-Centric Platform Evolution As enterprise digital governance becomes stricter, beacon solution providers are redesigning platforms with stronger encryption, consent management, and secure edge processing. Nearly 52% of enterprise buyers now prioritize privacy-by-design capabilities during procurement, while centralized device management reduces maintenance workloads by approximately 30%. Companies are responding through software upgrades, cybersecurity partnerships, and unified management platforms that support scalable deployment across multiple operational environments.

Hardware remains the leading segment as beacon devices form the core infrastructure supporting indoor positioning, proximity marketing, navigation, and industrial asset tracking. The segment accounts for nearly 48% of total deployments due to declining Bluetooth Low Energy component costs, longer battery life, and improved deployment flexibility. Enterprise customers continue expanding beacon networks across retail stores, airports, hospitals, and manufacturing facilities, while vendors focus on compact designs, extended battery performance, and simplified installation. Services maintain strategic importance by supporting deployment planning, maintenance, analytics integration, and lifecycle management for enterprise customers with complex infrastructure. Software represents the fastest-growing segment as organizations increasingly seek cloud-based analytics, centralized device management, AI-enabled location intelligence, and workflow automation. Nearly 44% of newly deployed enterprise beacon projects now prioritize software integration over standalone hardware purchases. Technology providers are investing heavily in SaaS platforms, API ecosystems, and enterprise partnerships, shifting competitive differentiation from hardware specifications toward intelligent software capabilities and recurring service models.

Retail remains the dominant application as businesses continue investing in personalized customer engagement, indoor navigation, digital promotions, and shopper analytics. Approximately 39% of beacon deployments are concentrated in organized retail environments where proximity-based engagement improves customer interaction and store performance. Healthcare continues expanding adoption for patient navigation, medical equipment tracking, and workflow optimization, while hospitality leverages beacon technology for contactless guest services and location-aware experiences that improve operational efficiency. Transportation & Logistics is emerging as the fastest-growing application as warehouses, distribution centers, and airports prioritize real-time asset visibility and workforce coordination. Asset search time has declined by nearly 30% following beacon integration into warehouse operations, while manufacturing facilities increasingly deploy beacon networks to optimize production workflows and monitor mobile equipment. Vendors are expanding industry-specific software capabilities, automation partnerships, and AI-powered analytics to strengthen operational performance across diverse enterprise environments.

Retail remains the largest end-user segment due to extensive deployment across supermarkets, shopping malls, department stores, and omnichannel retail networks. Nearly 36% of enterprise beacon installations serve retail operations, where customer engagement, store analytics, and proximity marketing remain key operational priorities. Healthcare organizations continue strengthening demand through patient flow optimization and asset management, while transportation operators utilize beacon infrastructure to improve passenger navigation and fleet coordination across complex facilities. Manufacturing represents the fastest-growing end-user segment as factories accelerate smart production, connected worker programs, and digital plant modernization. More than 41% of newly digitized manufacturing facilities now evaluate indoor positioning technologies as part of broader Industry 4.0 investments. BFSI institutions are adopting beacon-enabled branch experiences and location-based security applications, while vendors increasingly develop customized enterprise platforms, vertical-specific software, strategic implementation partnerships, and subscription-based deployment models that improve scalability and customer retention across multiple industries.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 24.8% between 2026 and 2033.

North America maintains its leadership through extensive deployment of beacon technology across organized retail, healthcare networks, airports, logistics centers, and smart commercial buildings. The region contributes approximately 38.4% of global demand, supported by mature Bluetooth Low Energy infrastructure, cloud computing adoption, and enterprise IoT investments. More than 65% of Fortune 500 retailers have incorporated indoor location technologies into customer engagement and inventory optimization strategies. Continuous investment in AI-enabled asset tracking, workplace automation, and digital infrastructure modernization is accelerating enterprise-scale deployments. Technology vendors continue expanding strategic software partnerships and managed service capabilities, strengthening interoperability across large multi-site operations while improving deployment efficiency and long-term lifecycle management.

United States Market Outlook: The United States represents the region's largest market due to its highly developed retail ecosystem, advanced healthcare infrastructure, and strong enterprise technology spending. Major retailers, airport authorities, logistics providers, and healthcare organizations continue integrating beacon platforms with AI analytics and cloud management systems. More than 7,000 large-format retail outlets have implemented proximity-based customer engagement technologies, while smart warehouse modernization continues expanding demand for real-time asset visibility. Continuous investment in enterprise software ecosystems and digital infrastructure reinforces the country's leadership in commercial beacon deployments.

Europe is expanding beacon technology deployment through industrial digitalization, smart manufacturing, healthcare modernization, and intelligent building initiatives. The region accounts for approximately 27.6% of global market activity, supported by advanced industrial automation and strong enterprise adoption of connected infrastructure. Manufacturing facilities increasingly integrate beacon-enabled workforce monitoring and equipment tracking into Industry 4.0 strategies, while hospitals deploy indoor navigation to improve operational workflows. Nearly 48% of newly modernized industrial facilities now evaluate indoor positioning technologies as part of broader digital transformation projects. Vendors continue strengthening interoperability, cybersecurity capabilities, and localized implementation services to support enterprise-scale deployments across highly regulated operating environments.

Germany Market Outlook: Germany remains Europe's strategic leader through its advanced manufacturing base, industrial automation expertise, and strong Industry 4.0 implementation. Automotive producers, logistics operators, and industrial enterprises increasingly deploy beacon infrastructure for equipment monitoring, production visibility, and workforce optimization. Approximately 45% of large manufacturing organizations are actively expanding connected factory initiatives incorporating indoor positioning technologies. Continued investment in industrial IoT platforms and enterprise automation supports sustained deployment across manufacturing and supply-chain operations.

Asia-Pacific is emerging as the fastest-expanding regional market as governments and enterprises accelerate smart city development, digital manufacturing, intelligent transportation, and connected commercial infrastructure. The region represents nearly 23.5% of global deployment activity, with enterprise investments strengthening across retail, logistics, airports, and manufacturing. More than 50% of newly constructed smart commercial facilities in leading economies now incorporate digital location technologies to enhance operational efficiency. Growing Bluetooth ecosystem manufacturing, expanding cloud adoption, and large-scale digital transformation initiatives continue improving deployment affordability. Technology companies are increasing regional partnerships, software localization, and enterprise integration capabilities to support rapidly expanding customer demand.

China Market Outlook: China leads regional deployment through extensive smart city investments, large-scale manufacturing modernization, and rapidly expanding digital retail infrastructure. Industrial enterprises are integrating beacon technology with AI, robotics, and warehouse automation to improve production visibility and asset utilization. More than 40% of new intelligent logistics facilities incorporate indoor positioning technologies to support automated inventory management and workforce coordination. Continued government-backed digital infrastructure initiatives reinforce China's position as the region's primary enterprise deployment market.

South America is witnessing steady adoption of beacon technology as retailers, logistics operators, healthcare providers, and commercial facilities invest in digital customer engagement and operational modernization. The region contributes approximately 6.2% of global market activity, supported by expanding mobile commerce and enterprise digital transformation initiatives. Retail organizations report customer engagement improvements exceeding 20% following location-aware marketing deployments. Infrastructure limitations and uneven digital maturity remain operational constraints, encouraging phased implementation strategies. Solution providers are responding through cloud-based deployment models, regional implementation partnerships, and scalable software platforms that reduce infrastructure complexity while improving accessibility for medium-sized enterprises.

Brazil Market Outlook: Brazil represents the largest market in South America owing to its extensive retail sector, expanding logistics infrastructure, and accelerating enterprise digitalization. Shopping centers, hospitals, airports, and logistics providers continue deploying beacon-enabled navigation and customer engagement platforms. More than 35% of large retail chains are actively investing in connected in-store technologies to strengthen omnichannel experiences. Growing investment in smart commercial infrastructure and enterprise mobility solutions continues supporting broader adoption across multiple industries.

The Middle East & Africa market is advancing through government-led smart city initiatives, airport modernization, digital healthcare programs, and commercial infrastructure expansion. The region accounts for approximately 4.3% of global deployment activity, with intelligent building projects driving increasing demand for indoor positioning solutions. More than 30% of newly developed smart commercial complexes in leading Gulf economies incorporate connected location technologies for facility management and visitor navigation. Technology providers continue expanding regional partnerships, cloud infrastructure investments, and enterprise integration services to support growing digital transformation requirements across public and private sectors.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through ambitious smart city programs, world-class airport infrastructure, and advanced commercial real estate developments. Beacon technology is increasingly deployed across airports, retail destinations, hospitality facilities, and government buildings to enhance navigation, customer experiences, and operational efficiency. Approximately 40% of newly commissioned premium commercial developments integrate intelligent location services as part of broader digital infrastructure strategies. Continued investment in smart infrastructure and enterprise technology ecosystems strengthens the country's role as the regional innovation hub for beacon deployment.

The market is led by Kontakt.io, HID Global, Estimote, BlueCats, and Radius Networks, competing against regional IoT platform providers and low-cost BLE hardware manufacturers. Global technology leaders focus on enterprise software integration, while regional vendors compete primarily on deployment cost and customization. The top five companies collectively account for approximately 48% of the market. Competition increasingly centers on platform intelligence, battery life, cybersecurity, and interoperability rather than hardware pricing alone. Enterprise customers report that software-driven location analytics improve operational efficiency by nearly 35%, while cloud-based device management reduces maintenance effort by around 30%. Vendors are expanding through healthcare partnerships, smart building deployments, AI-enabled RTLS innovation, and integrated IoT ecosystems. Market competition is shifting toward end-to-end location intelligence platforms, encouraging acquisitions and software-led differentiation. High enterprise integration requirements and security compliance create significant entry barriers for new participants. Winning depends on scalable software ecosystems, seamless interoperability, proven enterprise deployments, and continuous innovation that delivers measurable operational value.

HID Global

Estimote

BlueCats

Radius Networks

Gimbal Inc.

MOKO Smart

Accent Systems

Minew Technologies

Sensoro

BlueUp

KKM Company Limited

Beacon technology is rapidly evolving from simple Bluetooth transmitters into intelligent indoor location platforms combining Bluetooth Low Energy (BLE), AI analytics, cloud computing, and edge processing. More than 60% of new enterprise deployments now integrate cloud-based device management, while Bluetooth 5.x improves communication range by nearly 40% compared with earlier BLE generations. AI-powered location analytics enables automated workflow optimization, predictive asset tracking, and intelligent occupancy monitoring, creating stronger operational visibility across healthcare, retail, manufacturing, and logistics environments.

Modern BLE platforms outperform legacy beacon infrastructure by reducing battery consumption by approximately 35% while improving indoor positioning accuracy by nearly 30% through adaptive signal calibration and edge intelligence. Around 55% of enterprise buyers now prioritize API-driven software ecosystems over standalone beacon hardware. Organizations adopting integrated RTLS, digital twin platforms, and AI-based analytics gain faster deployment, lower maintenance costs, and stronger operational decision-making, creating clear competitive advantages over hardware-focused implementations.

Between 2026 and 2028, ultra-wideband integration, AI-powered digital twins, and autonomous asset orchestration will reshape enterprise indoor intelligence. Healthcare providers, logistics operators, and smart manufacturing facilities will benefit most as software-defined location services become standard infrastructure. Companies investing early in interoperable IoT ecosystems, cybersecurity, and predictive analytics will strengthen enterprise competitiveness while improving scalability, automation, and long-term operational resilience.

January 2025 – Kontakt.io appointed a new Chief Technology Officer, Chief Financial Officer, and Vice President of Marketing to accelerate AI-powered RTLS innovation and U.S. healthcare expansion. The leadership investment strengthens product development and enterprise execution across hospital operations.

July 2025 – Kontakt.io expanded its Staff Safe RTLS platform to cover outdoor hospital campuses and parking facilities, addressing workplace violence concerns. The unified platform supports 100% campus coverage through integrated indoor and outdoor safety monitoring, improving enterprise healthcare protection.

June 2025 – Kontakt.io released major cloud platform and device management updates, enhancing enterprise fleet administration, firmware management, and operational visibility for large-scale beacon deployments. The enhancements improve lifecycle management efficiency across thousands of connected devices.

March 2026 – Kontakt.io introduced its AI-powered "Curiosity Engine" for healthcare operations, enabling hospital teams to transform operational data into actionable decisions within minutes through advanced RTLS analytics. The launch strengthens enterprise automation and workflow optimization. Source: www.kontakt.io

This report delivers comprehensive analysis of the global Beacons Technology Market across hardware, software, and services, covering deployment trends in retail, healthcare, transportation & logistics, hospitality, manufacturing, and other emerging applications. It evaluates demand across major end-user industries including retail, manufacturing, healthcare, BFSI, and logistics while assessing deployment patterns across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 45% of enterprise deployments are analyzed through operational adoption, technology integration, and infrastructure modernization perspectives.

The report also examines Bluetooth Low Energy, AI-powered location analytics, cloud-based device management, edge computing, RTLS platforms, and interoperability developments shaping enterprise adoption. Competitive benchmarking covers leading global technology providers alongside emerging innovators, supporting investment planning, product positioning, partnership evaluation, and expansion strategies. Strategic insights into enterprise digitization, smart infrastructure, industrial automation, and intelligent location services provide decision-makers with actionable guidance for market opportunities and competitive positioning throughout the 2026–2033 assessment period.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 573.0 Million |

| Market Revenue (2033) | USD 2,856.7 Million |

| CAGR (2026–2033) | 22.24% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Kontakt.io; HID Global; Estimote; BlueCats; Radius Networks; Gimbal Inc.; MOKO Smart; Accent Systems; Minew Technologies; Sensoro; BlueUp; KKM Company Limited |

| Customization & Pricing | Available on Request (10% Customization Free) |