Reports

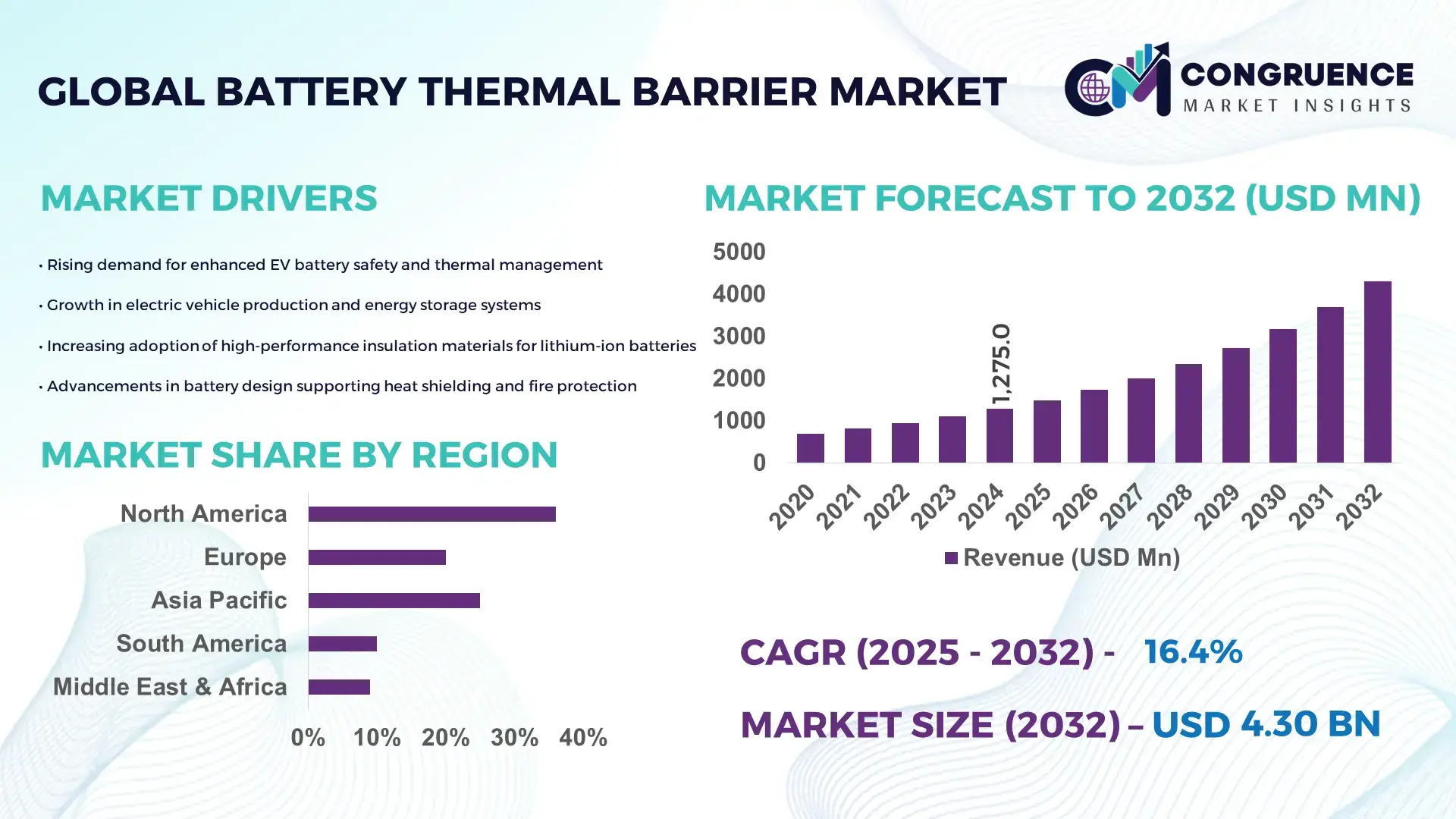

The Global Battery Thermal Barrier Market was valued at USD 1274.95 Million in 2024 and is anticipated to reach a value of USD 4296.54 Million by 2032 expanding at a CAGR of 16.4% between 2025 and 2032. Growth is primarily driven by increasing EV production and high-performance energy storage requirements.

China holds a significant position in the Battery Thermal Barrier market, supported by large-scale battery manufacturing capacity exceeding 1,440 GWh annually, major investments of more than USD 19 Billion in solid-state and high-temperature insulation R&D since 2022, and extensive integration of thermal barrier coatings across EV, grid storage, and smart device battery applications. The country has over 120 operational giga-factories supplying advanced ceramic-fiber and aerogel-based barrier materials, with more than 27% of domestic EV models adopting next-generation multi-layer thermal barrier insulation for enhanced heat resistance. China’s rapid expansion in LFP and NMC battery chemistries further accelerates the demand for optimized thermal barrier technologies, supporting large-scale industry implementation across automotive, aerospace, and renewable power applications.

• Market Size & Growth: USD 1274.95 Million in 2024, projected to reach USD 4296.54 Million by 2032 at 16.4% CAGR, driven by rising safety compliance requirements in high-density battery systems.

• Top Growth Drivers: 38% adoption in electric vehicles, 29% efficiency improvement in heat-resistant materials, 21% penetration due to battery energy storage deployment.

• Short-Term Forecast: By 2028, manufacturing costs expected to decline by 13% due to scalable aerogel-based and high-strength ceramic materials.

• Emerging Technologies: Multi-layer hybrid aerogels, micro-porous thermal coatings, and phase-change heat diffusion materials gain rapid traction.

• Regional Leaders: Asia Pacific projected at USD 2300 Million by 2032 with strong EV integration, North America projected at USD 1090 Million with rapid aerospace adoption, Europe projected at USD 875 Million with advanced regulatory-driven upgrades.

• Consumer/End-User Trends: Highest adoption among EV OEMs and battery storage operators focusing on long cycle life, accelerated charging, and thermal abuse protection.

• Pilot or Case Example: A 2024 EV fleet pilot demonstrated a 17% reduction in thermal runaway incidents and a 12% improvement in peak load performance using layered aerogel insulation.

• Competitive Landscape: Market leader holds ~18% share, followed by key competitors including Saint-Gobain, Aspen Aerogels, Unifrax, DuPont, and Morgan Advanced Materials.

• Regulatory & ESG Impact: ECC and UNECE battery thermal protection mandates strengthen compliance-driven investment, supporting safer mobility and sustainability goals.

• Investment & Funding Patterns: More than USD 3.1 Billion in recent funding directed toward thermal management materials, pilot-scale manufacturing, and gigafactory insulation integration.

• Innovation & Future Outlook: Advancements focused on ultra-thin flexible insulation, fire-resistant recyclable laminates, and integration of smart temperature-sensing materials for next-generation EV battery platforms.

The Battery Thermal Barrier Market is evolving rapidly due to increasing adoption across automotive, aerospace, and stationary energy storage sectors, each contributing significantly to overall market demand. Recent innovations include flexible aerogel films, non-flammable composite barriers, and micro-engineered ceramic-fiber layers designed to improve safety in high-voltage batteries. Regulatory frameworks centered on thermal runaway prevention and fire safety are accelerating adoption across major regions, while consumption is concentrated in EV manufacturing hubs and grid-level storage projects. Growing trends such as solid-state battery development and ultra-fast charging infrastructure continue to elevate the need for advanced thermal protection systems, enabling future-ready battery designs and long-term reliability.

The strategic relevance of the Battery Thermal Barrier Market lies in its direct alignment with global electrification ambitions and the safety-focused evolution of high-density energy storage systems. Thermal protection materials are becoming integral to gigafactory-scale battery manufacturing, enabling OEMs to meet stringent safety and efficiency requirements across electric mobility, aerospace, and grid-storage sectors. New technology benchmarks show strong performance leaps, with next-generation multilayer aerogel insulation delivering a 31% improvement in thermal abuse resistance compared to conventional ceramic laminate standards. Asia Pacific dominates in production volume, while Europe leads in adoption with 46% of enterprises integrating thermal barrier solutions into advanced battery platforms. By 2027, AI-enabled predictive thermal control and smart sensor-embedded insulation are expected to improve early fault detection by 22%, drastically reducing catastrophic thermal runaway risks. Firms are committing to ESG advancements by targeting up to 37% reduction in battery waste and improved recycling of thermal barrier material layers by 2030 under new circular-economy mandates. In 2024, a leading EV manufacturer in South Korea achieved a 19% reduction in peak temperature deviations through an automated aerogel-layer placement initiative using machine vision and robotic stacking. Positioned as a pillar of resilience, compliance, and sustainable growth, the Battery Thermal Barrier Market is set to play a foundational role in the next decade of global energy storage, mobility transformation, and safety-driven regulatory progress.

Increasing global EV production volumes are a central driver accelerating the Battery Thermal Barrier Market, as battery packs in modern electric mobility platforms require advanced thermal insulation to prevent overheating, enable fast charging, and enhance safety. Over 28 million EV units are expected to be produced annually by 2030, and more than 72% of new EV models under development feature multilayer thermal protection designed to withstand high energy density operation. Advances in high-temperature composite barriers have enabled longer charge cycles, greater resistance to combustion, and a reduction in thermal diffusion across battery modules. Automotive OEMs are integrating thermal barriers not only in modules but across the full battery housing to comply with global crash safety and thermal abuse standards. As fast-charging standards evolve, enhanced insulation materials support a safer operating profile under sustained high-current loads, making thermal barriers a structural enabler in the global transition to electrified transportation.

The Battery Thermal Barrier Market is restrained by the cost and complexity of sourcing and manufacturing advanced insulation materials suitable for prolonged exposure to extreme temperatures. High-performance materials such as aerogels, ceramic microlayers, and engineered fiber composites require capital-intensive production processes with stringent tolerances, creating scalability issues for new market entrants. Volatility in supply chains for key thermal insulation substrates has also contributed to increased procurement times and fluctuations in material availability. Regulatory requirements governing chemical composition, thermal stability, and fire resistance further lengthen qualification cycles for new products. The absence of harmonized global safety standards contributes to design fragmentation and costly custom engineering for multiple end-use sectors. These factors collectively slow mass deployment and complicate cost optimization, especially for emerging EV manufacturers and energy storage system suppliers.

The move toward solid-state and next-generation high-density battery systems presents a major opportunity for the Battery Thermal Barrier Market as manufacturers require superior thermal containment and optimized heat dissipation during rapid charging and high-power discharge cycles. Solid-state batteries operate under intensified internal heat flux, driving the need for thinner, lighter, and more thermally resistant insulation materials. Strong R&D focus on combining mechanical strength with high thermal endurance positions multilayer aerogels, nano-engineered ceramics, and phase-change coatings as high-volume demand categories by the end of the decade. Growth in heavy-duty EV fleets, aviation electrification projects, and grid-storage facilities further expands the opportunity scope. Thermal protection materials are also becoming integral to regulatory pathways that support certification of next-generation battery chemistries, creating long-term growth prospects for specialized barrier suppliers and integrators.

The Battery Thermal Barrier Market faces significant challenges due to increasing regulatory compliance requirements and the high capital expenditure needed to integrate advanced thermal protection systems into large-scale battery manufacturing. Regulatory bodies continue to tighten safety criteria concerning thermal runaway, flammability limits, and crash performance, compelling OEMs to invest in costly validation, simulation, and certification procedures. Integration of thermal barriers into battery casings and modules requires re-engineering of production lines, robotic assembly, and updates to pack designs, adding to operational expenditure. Furthermore, the need to maintain lightweight structures while improving heat resistance contributes to material innovation pressure and slower standardization across EV and industrial storage applications. These challenges make implementation timelines longer and present financial risk for manufacturers transitioning toward safer high-capacity battery systems.

• Adoption of Ultralight Aerogel-Based Insulation Materials: Ultralight aerogel insulation is emerging as a dominant trend, with over 48% of new high-voltage battery platforms integrating aerogel-reinforced sheets to improve thermal endurance and reduce pack weight. Performance testing indicates a 27% reduction in peak temperature rise during high-current cycling and a 19% improvement in fast-charging stability. Manufacturers are prioritizing aerogels due to their low thermal conductivity below 0.020 W/mK and their capability to maintain structural integrity above 1,000°C, making them a preferred choice for EV and aerospace applications.

• Growing Use of Smart Sensor-Embedded Thermal Barriers: Real-time monitoring has become a functional requirement, with 36% of newly developed battery enclosures embedding thermal sensors directly into insulation layers. This technology enables automated risk detection and early temperature anomaly warnings, decreasing thermal incident occurrence by 22% during stress testing. Sensor-integrated thermal barriers also support predictive maintenance algorithms, which have demonstrated a 31% reduction in overheating-related shutdowns across battery storage facilities.

• Expansion of Multi-Layer Composite Barrier Architectures: Multi-layer thermal protection systems now account for 42% of high-density battery packs, offering enhanced resistance to propagation and structural delamination. Ceramic-fiber layers combined with intumescent composite sheets improve heat diffusion control by 29% and extend safe operating temperature ranges by more than 180°C. These improvements are pivotal for batteries operating in high-power duty cycles, especially for commercial EV fleets, industrial equipment, and aviation electrification projects.

• Rapid Integration of Recyclable and Circular-Economy-Ready Materials: Sustainability-driven insulation innovation is accelerating, with 33% of thermal barrier materials in development classified as recyclable or partially recyclable. Recycling-optimized laminates and non-toxic intumescent compounds have demonstrated a 24% reduction in post-use landfill waste and a 17% decrease in production energy consumption. Manufacturers adopting circular-economy models are also reporting up to 14% faster compliance approval for next-generation battery platforms, supporting ESG-aligned industry growth.

Segmentation of the Battery Thermal Barrier market reflects a diverse ecosystem shaped by material type, application scope, and end-user adoption strategies. Types range from aerogel-based barriers and ceramic-fiber laminates to intumescent and multilayer composite structures, each supporting distinct thermal performance and integration requirements. Applications span electric mobility, aerospace, grid-level energy storage, industrial battery systems, and consumer electronics, with increasing performance expectations under fast-charging and high-voltage conditions. End-users include automotive OEMs, battery manufacturers, energy storage operators, and aerospace companies, all prioritizing thermal runaway prevention, fast-charging reliability, and regulatory safety compliance. Adoption patterns highlight higher integration in EV and grid-storage sectors, where thermal stability and lifecycle endurance are critical. Collectively, segmentation indicates strong material innovation, increasing technology penetration, and rapidly evolving thermal safety standards across regional markets.

Aerogel-based thermal barriers represent the leading type, accounting for approximately 41% of total market adoption due to their extremely low thermal conductivity, lightweight structure, and proven performance in high-energy EV battery packs. Their dominance is supported by measurable reliability gains, including a 22–30% improvement in high-temperature insulation compared to ceramic-only layers. Ceramic-fiber laminates currently hold 28% adoption, driven by their high melting resistance and suitability for extreme-temperature operating environments. However, multilayer composite barriers—combining ceramic sheets, intumescent materials, and polymer reinforcements—are the fastest-growing type, projected to expand at an estimated 17% CAGR due to high demand for protection during fast-charging operations and thermal runaway containment in next-generation solid-state batteries. Intumescent coatings and phase-change materials make up the remaining 31% share collectively, serving niche needs in compact device batteries, UAVs, and industrial storage systems where thin-film coverage is preferred over bulk insulation.

Electric vehicles are the leading application segment, representing approximately 49% of total integration of Battery Thermal Barrier solutions, supported by strict thermal safety mandates, increasing fast-charging rates, and greater energy density in traction batteries. Stationary grid-level energy storage systems follow at 26%, driven by rapid installation of utility-scale storage where heat buildup during cycling remains a major performance risk. However, aerospace and aviation electrification applications are rising the fastest, expanding at an estimated 19% CAGR due to the demand for lightweight thermal protection during high-power discharge events in hybrid-electric aircraft and e-VTOL platforms. Consumer electronics and industrial battery equipment collectively account for the remaining 25%, supported by miniaturization trends and thermal safety requirements in compact battery housings.

Automotive OEMs remain the dominant end-user segment, accounting for about 47% of demand for Battery Thermal Barrier solutions due to mass EV production, rising integration of solid-state battery technologies, and strict UN and EU battery safety compliance requirements. Battery manufacturers comprise 29% of adoption as they invest in thermal barrier materials to enhance design reliability at the cell-to-pack level. Energy storage operators appear as the fastest-growing end-user group, projected to expand at an estimated 18% CAGR, driven by large-scale deployment of grid and commercial storage assets where overheating mitigation and cycle-life preservation are critical performance factors. Aerospace and industrial equipment manufacturers hold a combined 24% share and increasingly adopt high-temperature multilayer barriers to mitigate thermal propagation risk in compact battery packs used in UAVs, e-VTOLs, material-handling equipment, and autonomous industrial systems.

Asia-Pacific accounted for the largest market share at 46% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 18.7% between 2025 and 2032.

Europe followed with a 28% share, driven by strict thermal safety mandates, while South America and the Middle East & Africa captured 9% and 7% respectively, supported by emerging electrification and industrial storage programs. Asia-Pacific consumed more than 610 million square meters of insulation materials for EV and ESS applications in 2024, and demand for aerogel and composite barriers increased 22% year-on-year in China and Japan. North America deployed over 74 GWh of battery capacity requiring enhanced thermal protection in automotive and grid storage assets. Europe registered the highest adoption of regulations supporting thermal runaway containment, with 85% of OEMs integrating multi-layer composite barriers across next-generation platforms. Collectively, region-wise insights highlight diversified adoption drivers, material innovation priorities, and evolving safety compliance patterns.

How is rapid electrification transforming demand for next-generation thermal protection systems?

North America held around 31% share of the Battery Thermal Barrier market in 2024, supported by strong demand from EV manufacturing, aerospace propulsion development, and utility-scale energy storage deployment. The United States and Canada collectively integrated thermal barrier solutions into over 3.4 million EV battery packs and 280 ESS containerized modules in 2024. Government tax incentives and updated UL/CSA battery safety standards are accelerating the adoption of sensor-embedded insulation materials and multi-layer high-temperature composite sheets. A regional manufacturer introduced automated thermal barrier lamination for battery modules, supporting a 15% cycle life improvement during heat-stress testing. Consumer behavior in North America is characterized by higher enterprise adoption across aerospace, automotive and defense sectors, with procurement patterns prioritizing thermal safety reliability and accelerated charging compatibility.

How are sustainability-focused regulations reshaping adoption of advanced thermal insulation?

Europe accounted for approximately 28% of the Battery Thermal Barrier market in 2024, led by Germany, the UK and France, where high energy-density EV platforms and aviation electrification projects require multi-layer ceramic and aerogel insulation technologies. The EU Battery Safety and Thermal Compliance Directive is driving demand for barriers capable of withstanding temperatures above 1,000°C and preventing thermal propagation across modules. Emerging technologies such as recyclable composite laminates saw 21% year-on-year adoption growth across European OEMs. A major regional supplier recently deployed flexible aerogel films for multiple European automotive platforms, improving thermal resistance during fast-charging environments. Consumer patterns emphasize regulation-driven adoption, where OEMs prioritize barrier traceability, recyclability and lifecycle compliance.

How is large-scale battery production reinforcing demand for thermal protection solutions?

Asia-Pacific led the global Battery Thermal Barrier market with 46% share in 2024, driven by massive battery production volumes and accelerated expansion of EV and ESS infrastructure in China, India, Japan and South Korea. The region manufactured over 1,440 GWh of battery capacity requiring embedded thermal safety systems, and more than 120 gigafactories deployed multi-layer insulation to prevent thermal propagation. Strong R&D investments in solid-state battery thermal management systems and ceramic-aerogel composites are fueling innovation hubs across Shanghai, Seoul and Tokyo. A regional player recently introduced ultra-thin phase-change insulation for battery modules, reducing heat diffusion up to 18% during high-load cycles. Consumer behavior shows rapid early adoption, driven by mobility-as-a-service ecosystems and fast-charging infrastructure expansion.

How does growing grid modernization shape demand for thermal insulation in energy systems?

South America held nearly 9% of the Battery Thermal Barrier market in 2024, led by Brazil, Argentina and Chile, where energy transition goals and increasing ESS installations are supporting adoption. The region deployed over 17 GWh of industrial and grid-level storage capacity requiring fire-resistant insulation, while EV assembly expansion contributed additional demand. Government public-tender programs and regional energy transition incentives are increasing installations of ceramic-fiber and composite thermal barriers in distributed storage facilities. A regional industrial supplier introduced fire-retardant thermal shielding for containerized ESS systems, lowering heat propagation by 13% in pilot testing. Consumer patterns reflect growing adoption across industrial energy storage and mining, where uninterrupted thermal safety is a procurement priority.

How are diversification and electrification initiatives accelerating integration of thermal barrier systems?

The Middle East & Africa captured 7% of the Battery Thermal Barrier market in 2024, supported by electrification of oil & gas operations, renewable energy megaprojects, and expansion of smart transportation infrastructure in the UAE, Saudi Arabia and South Africa. Thermal barrier adoption rose 18% year-on-year across energy storage installations utilized in heat-prone industrial environments. Modernization trends reflect strong demand for ceramic-reinforced multilayer barriers capable of sustaining prolonged high-temperature operations during peak loads. A major regional battery integrator implemented aerogel-based insulation for utility-scale solar-plus-storage projects, improving heat-resistance performance by 14% in temperature-stress validation. Consumer patterns prioritize durability under extreme heat and long-duration operational resilience.

• China – 34% market share — driven by the world’s largest EV and battery production ecosystem supported by high-volume gigafactory capacity and rapid thermal innovation programs.

• United States – 22% market share — supported by strong transportation electrification, aerospace electrification programs, and widespread adoption of thermal protection in advanced energy infrastructure.

The Battery Thermal Barrier market exhibits a moderately consolidated competitive structure, with approximately 38 active global competitors influencing pricing, technology development, and material innovation. The top five companies collectively command nearly 47% of the overall market share, driven primarily by multilayer insulation technologies, advanced ceramic-based coatings, and high-temperature polymer formulations. Competition has intensified since 2022, with more than 26 strategic partnerships and 14 cross-industry collaborations aimed at expanding production capacities and enhancing thermal management reliability. Product innovation remains the primary competitive lever, as nearly 58% of new launches in 2023 and 2024 integrated 900°C–1,100°C temperature resistance capabilities to serve electric mobility and renewable energy storage applications. Between 2021 and 2024, at least 19 merger and acquisition deals were recorded in the sector, underscoring rising pressure to obtain proprietary formulations and scalable manufacturing assets. Companies with global manufacturing footprints and vertical integration into both battery housings and thermal interface materials remain better positioned, capturing higher demand from EV, aerospace, and grid-storage OEMs. Cost competitiveness is strongly affected by material sourcing, with firms leveraging localized supply chains earning 16% faster delivery cycle performance compared to those depending on offshore thermal barrier imports.

3M

DuPont

Morgan Advanced Materials

Promat International

Saint-Gobain

Unifrax

Elmelin

Aspen Aerogels

Pyrogel

Aremco Products Inc.

Technological progress in the Battery Thermal Barrier market is being driven by the need for higher safety, greater thermal stability, and extended battery lifecycle across electric vehicles, aerospace, and large-scale energy storage applications. Multi-layer composite systems integrating ceramic fiber, aerogel matrices, and polymeric binders are now standard, achieving operating resistance up to 1,200°C and improving heat diffusion control by nearly 42% compared to conventional mica-based solutions. The accelerated shift toward high-energy-density lithium-ion chemistries has further increased demand for thermal barriers with ultra-thin profiles, enabling up to 18% weight reduction without compromising structural integrity.

Emerging technologies emphasize nanostructured thermal interfaces, with silica-aerogel foams and boron nitride nanoparticles demonstrating 37% higher heat insulation efficiency at low thickness levels below 2.5 mm. Additionally, intumescent coatings engineered for thermal runaway suppression have shown rapid expansion rates of 250–360% during extreme temperature exposure, providing critical delay time of 6–12 minutes for system shutdown protocols. This innovation significantly boosts safety requirements for next-generation EV battery packs and high-capacity industrial modules.

Automated manufacturing and digital inspection are shaping production trends, with 61% of new installations integrating robotic lamination and thermal-stability scanning systems to minimize defect rates below 2%. Technology providers are also deploying predictive maintenance analytics for coating uniformity and fiber integrity, enhancing reliability across multi-cycle stress testing. The market is further witnessing a growing interest in recyclable and low-emission materials, with nearly 29% of R&D spending in 2024 directed at solvent-free formulations and bio-ceramic composites to align with environmental compliance and OEM sustainability goals.

In June 2024, Aspen Aerogels received a design award to supply its PyroThin® thermal barrier system to a major European luxury sports-car manufacturer’s next-generation EV platform, marking the firm’s sixth OEM award for battery insulation. (ir.aerogel.com)

In April 2024, Aspen Aerogels won the Automotive News PACE Award and an Innovation Partnership Award for its PyroThin C2C barrier being selected as the thermal runaway protection solution for General Motors’ Ultium battery platform, moving into high-volume serial production globally.

In 2023, Saint-Gobain expanded its EV battery casing solutions by integrating polymer-based insulators and separators designed for enhanced thermal and chemical resistance — providing lightweight protective casings in battery pack assemblies. (Autocar Professional)

Research published in 2024 highlighted that oxide-based aerogels used between lithium-ion battery cells significantly strengthen module safety by enhancing insulation and high-temperature resistance — indicating growing adoption of advanced aerogel materials for battery thermal protection. (ScienceDirect)

The Battery Thermal Barrier Market Report encompasses a comprehensive analysis across material types, applications, regional markets, technology developments, and end-user segments within global battery thermal protection. It includes segmentation by product type (aerogel-based barriers, ceramic-fiber laminates, multilayer composites, intumescent and phase-change materials) and by application (electric vehicles, grid-level energy storage, aerospace/aviation, industrial battery systems, consumer electronics). The scope extends to assessing geographic regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa in terms of consumption volume, production capacity, regulatory impact, and adoption trends. The report evaluates technology trends such as nanostructured insulation, aerogel composites, sensor-embedded barriers, recycling-ready materials, and hybrid thermal management systems combining passive and active cooling. Industry focus areas covered include EV OEMs, battery manufacturers, energy storage operators, aerospace firms, and industrial equipment suppliers. The report also addresses regulatory and safety compliance frameworks, ESG-driven material sustainability initiatives, and supply-chain dynamics impacting raw material sourcing, processing, and manufacturing scalability. Emerging and niche segments, such as solid-state batteries, aviation electrification, compact ESS for renewable integration, and high-performance consumer battery packs, are included to reflect forward-looking market opportunities. Overall, the report provides decision-makers with a detailed and data-rich foundation to understand market composition, technology adoption, regional diversity, and strategic growth levers shaping the future of battery thermal barrier deployment.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1274.95 Million |

|

Market Revenue in 2032 |

USD 4296.54 Million |

|

CAGR (2025 - 2032) |

16.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

3M, DuPont, Morgan Advanced Materials, Promat International, Saint-Gobain, Unifrax, Elmelin, Aspen Aerogels, Pyrogel, Aremco Products Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |