Reports

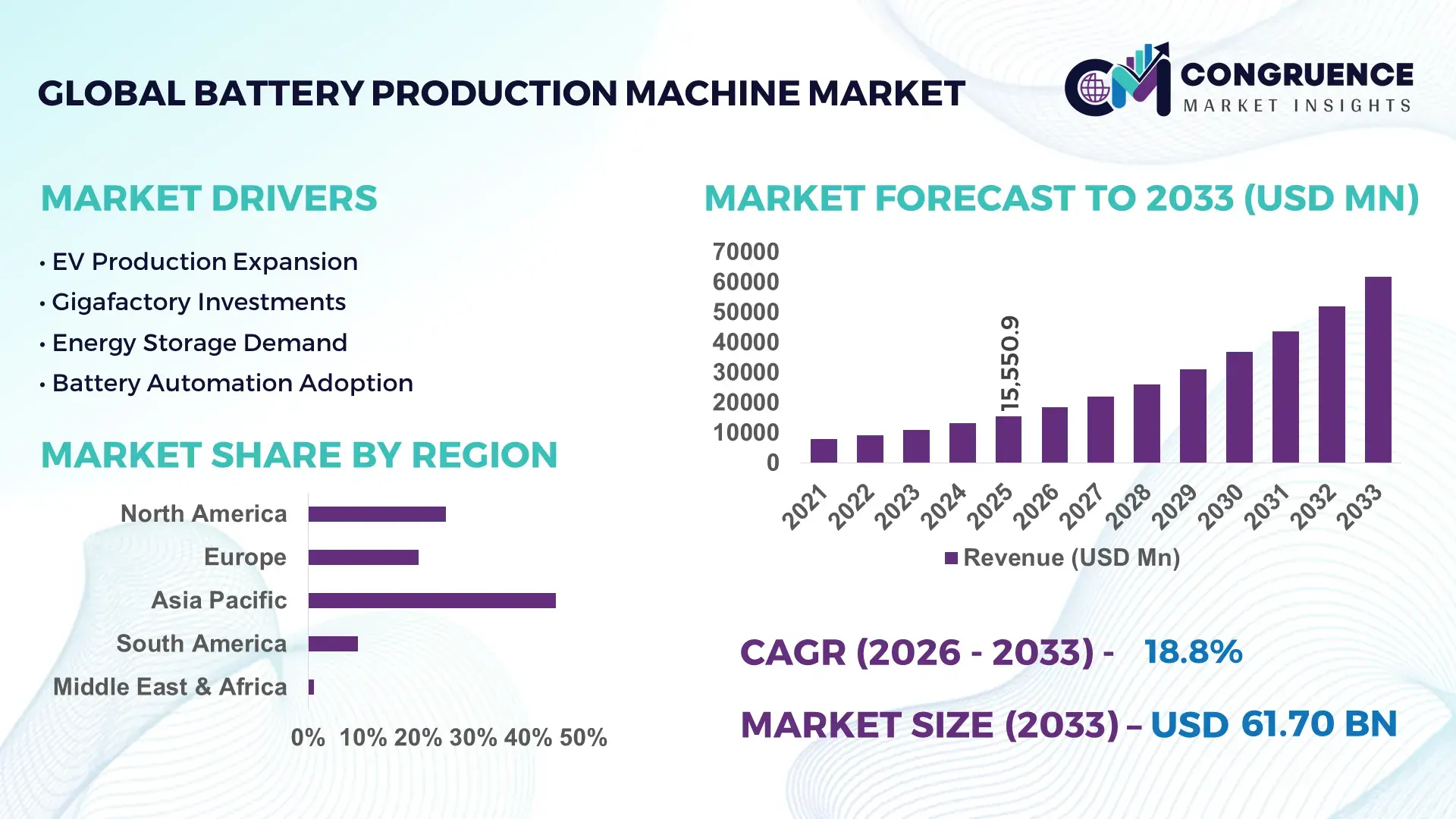

The Global Battery Production Machine Market was valued at USD 15550.92 Million in 2025 and is anticipated to reach a value of USD 61700.34 Million by 2033 expanding at a CAGR of 18.8% between 2026 and 2033. High-volume lithium-ion gigafactory expansion, accelerated EV localization policies, and rising automation adoption in electrode coating and cell assembly lines are driving advanced battery production machine deployment across Asia, Europe, and North America.

China leads the global battery production machine market with over 46% of installed lithium-ion cell manufacturing capacity in 2026, supported by multi-billion-dollar gigafactory investments and vertically integrated EV supply chains. Germany remains Europe’s strongest automation hub, with battery equipment utilization rates exceeding 82% across automotive cell plants, while the U.S. continues expanding domestic battery manufacturing under strategic clean-energy industrial policies and supply-chain localization initiatives linked to post-Inflation Reduction Act production targets.

Manufacturers prioritizing high-speed automation, dry electrode processing, and AI-enabled defect inspection systems are positioned to secure long-term contracts as global battery producers intensify regional manufacturing diversification strategies.

Market Size & Growth: Global market expands from USD 15550.92 Million in 2025 to USD 61700.34 Million by 2033, driven by EV battery gigafactory automation and localized cell manufacturing expansion at 18.8% CAGR.

Top Growth Drivers: EV battery demand contributes 41% growth momentum, factory automation 33%, and energy storage expansion 26% across advanced production equipment demand.

Short-Term Forecast: By 2028, automated electrode manufacturing reduces material wastage by 21% while boosting line productivity by 28% in high-capacity battery plants.

Emerging Technologies: AI-based defect detection, dry electrode coating, and digital twin-enabled process optimization improve production efficiency by over 30% in advanced battery facilities.

Regional Leaders: Asia-Pacific surpasses USD 31 Billion with aggressive gigafactory expansion, Europe exceeds USD 14 Billion through localized EV supply chains, and North America crosses USD 10 Billion via clean-energy manufacturing incentives.

Consumer/End-User Trends: Over 68% of battery manufacturers prioritize fully automated assembly systems to reduce labor dependency and improve yield consistency.

Pilot/Case Example: In 2026, a high-speed cylindrical cell production project improved throughput by 34% and lowered energy consumption by 18% using AI-integrated coating equipment.

Competitive Landscape: Top manufacturers control nearly 44% market share, with leading competition centered around Wuxi Lead, Manz, Hirano Tecseed, Yinghe Technology, and Sovema Group.

Regulatory & ESG Impact: Advanced solvent recovery and low-emission production systems reduce factory carbon output by approximately 27% under tightening global sustainability regulations.

Investment & Funding: Global battery manufacturing investments exceed USD 145 Billion, with strategic partnerships and regional supply-chain diversification accelerating equipment procurement.

Innovation & Future Outlook: Solid-state battery manufacturing systems, modular production lines, and smart factory integration are reshaping next-generation high-throughput battery equipment strategies.

Advanced battery production machines are witnessing strong demand across EV manufacturing, grid-scale energy storage, and consumer electronics sectors as manufacturers accelerate high-throughput cell production upgrades. AI-driven inspection systems and dry electrode technologies improve operational efficiency by nearly 30% while reducing defect rates in large-scale facilities. Supply-chain regionalization across North America and Europe, combined with stricter carbon-reduction targets, is accelerating investment in automated, energy-efficient battery manufacturing infrastructure and strategic production scalability.

Battery production machines have become strategically critical as automotive, energy storage, and electronics manufacturers accelerate localized battery supply-chain development to reduce geopolitical exposure and logistics dependency. Gigafactory deployment across the U.S., Germany, India, and South Korea is reshaping industrial equipment procurement priorities, with automated electrode coating, laser welding, and AI-enabled inspection systems now central to manufacturing competitiveness. More than 64% of newly commissioned battery plants in 2026 are integrating smart manufacturing architectures to improve yield consistency and reduce production downtime under rising EV demand and stricter carbon-efficiency benchmarks.

Advanced dry electrode processing systems deliver nearly 32% lower energy consumption compared with conventional wet coating lines while reducing factory floor requirements by approximately 25%. China maintains the largest scaled deployment advantage through vertically integrated battery ecosystems, whereas Germany focuses on precision automation and low-defect manufacturing standards for premium automotive applications. North American manufacturers are prioritizing modular production lines to shorten installation cycles by almost 20% and accelerate domestic cell production readiness over the next two years.

In 2026, several battery manufacturers expanded partnerships with robotics and industrial automation firms to deploy predictive maintenance platforms capable of reducing unplanned downtime by 18%. Companies are increasingly directing capital toward localized equipment ecosystems, digital production monitoring, and flexible manufacturing architectures to strengthen operational resilience and secure long-term positioning in the global battery manufacturing transition.

Large-scale battery gigafactory construction across China, the U.S., and India is accelerating demand for high-speed battery production machinery capable of supporting continuous manufacturing operations. Automated cell assembly systems improve production throughput by nearly 35%, while AI-integrated defect inspection reduces quality rejection rates by over 22% in high-volume facilities. The rapid expansion of electric mobility programs and domestic battery localization mandates is forcing manufacturers to shorten commissioning timelines and increase process consistency. In response, equipment suppliers are expanding robotics integration, localized engineering support, and turnkey production solutions. Indian industrial corridors and U.S. clean-energy manufacturing clusters are increasingly prioritizing automated battery lines to reduce import dependency and improve supply-chain security, creating a strong operational advantage for companies with scalable, precision-driven manufacturing capabilities.

Battery production machine deployment remains constrained by persistent fluctuations in lithium-processing infrastructure costs, industrial automation component pricing, and semiconductor availability. High-precision coating and calendaring systems experienced equipment procurement cost increases of nearly 18% during recent supply-chain disruptions, while lead times for industrial control modules extended beyond 30 weeks in several manufacturing hubs. European battery equipment manufacturers also face rising compliance costs linked to energy-efficiency and emissions standards. These pressures directly impact project scalability, factory commissioning schedules, and operating margins for mid-sized manufacturers. To reduce exposure, companies are localizing component sourcing, securing long-term supplier agreements, and redesigning production systems with modular architectures that lower maintenance complexity and improve procurement flexibility across geographically diversified operations.

The integration of AI-driven process analytics, digital twins, and predictive maintenance platforms is creating major efficiency opportunities across advanced battery manufacturing facilities. Smart production systems improve equipment utilization rates by approximately 27% while reducing unplanned downtime by nearly 20% in automated lithium-ion cell plants. Japan and South Korea are accelerating adoption of machine-learning-enabled quality monitoring to support next-generation solid-state battery production and precision coating requirements. Simultaneously, sodium-ion and semi-solid battery development programs are opening new demand pathways for flexible production machinery with adaptable tooling systems. Equipment manufacturers are responding through collaborative R&D partnerships, software-integrated production ecosystems, and cloud-connected manufacturing platforms that enable real-time operational optimization. A key strategic advantage is emerging for suppliers capable of combining automation hardware with proprietary manufacturing intelligence software.

Battery production facilities are becoming increasingly difficult to scale due to engineering talent shortages, software interoperability issues, and complex integration requirements across multi-vendor automation systems. More than 41% of battery manufacturers report delays linked to advanced robotics programming and industrial software synchronization during plant commissioning phases. In Germany and the U.S., demand for skilled automation engineers continues exceeding supply as factories transition toward fully digitalized manufacturing environments. Cybersecurity exposure is also intensifying because cloud-connected production systems and AI-driven monitoring platforms increase operational vulnerability across critical infrastructure. Companies must strengthen workforce training programs, standardized industrial communication protocols, and cybersecurity frameworks to maintain deployment consistency. Long-term competitiveness will depend on balancing high-speed automation expansion with resilient digital infrastructure and technically specialized operational ecosystems.

• AI-Driven Quality Inspection Expansion Battery manufacturers are rapidly deploying AI-enabled vision inspection systems capable of reducing defect detection time by 40% and improving production accuracy by nearly 25% across cylindrical and prismatic cell lines. Chinese and South Korean gigafactories are integrating real-time analytics platforms into coating and assembly workflows to reduce scrap losses amid rising raw material costs. Equipment suppliers are responding through software partnerships and cloud-based monitoring integration to secure recurring industrial automation contracts.

• Dry Electrode Processing Adoption Dry electrode manufacturing is gaining traction as battery producers target lower energy consumption and solvent-free production methods under stricter emissions regulations. Advanced dry coating systems reduce factory energy usage by approximately 32% while cutting equipment footprint requirements by nearly 20%. U.S. and German manufacturers are restructuring production layouts around high-throughput continuous processing lines, while machinery vendors accelerate pilot-scale deployments and specialized thermal processing equipment development.

• Localized Equipment Supply Chains Supply-chain disruptions and industrial policy shifts are pushing battery manufacturers to regionalize machinery procurement and component sourcing strategies. More than 48% of new battery equipment contracts in 2026 prioritize local engineering support and spare-part availability to reduce commissioning delays. Indian and North American producers are expanding domestic supplier partnerships, while equipment companies establish localized assembly hubs to shorten installation cycles and improve after-sales service responsiveness.

• Flexible Modular Production Systems Battery manufacturers are increasingly shifting toward modular production architectures capable of supporting lithium-ion, sodium-ion, and semi-solid battery formats on shared manufacturing lines. Flexible assembly platforms improve changeover efficiency by nearly 27% and reduce line reconfiguration downtime by over 18%. Japanese automation firms are scaling modular robotics integration to address evolving battery chemistries, while manufacturers prioritize adaptable production ecosystems to maintain long-term utilization rates amid fast-changing battery technology roadmaps.

Coating Equipment remains the dominant segment in the battery production machine market due to its direct influence on electrode precision, material utilization, and production consistency across lithium-ion cell manufacturing. Advanced coating systems improve electrode uniformity by nearly 24% while reducing slurry waste by approximately 18%, making them operationally critical for large-scale EV battery plants. Chinese and South Korean manufacturers continue expanding high-speed coating line deployments to support increasing gigafactory throughput requirements. Meanwhile, Assembly Equipment is witnessing the fastest adoption growth as manufacturers prioritize robotic welding, stacking, and automated cell integration systems to reduce labor dependency and improve scalability across high-volume battery facilities.

Testing Equipment is becoming increasingly strategic as battery producers tighten quality assurance standards for high-energy-density cells and next-generation chemistries. Cutting Equipment maintains relevance through precision electrode shaping requirements, particularly in cylindrical and pouch cell production, while Packaging Equipment demand is rising steadily with expanding energy storage deployments and transportation safety compliance needs. Equipment manufacturers are responding through integrated production platforms, AI-enabled diagnostics, and modular automation partnerships to strengthen long-term industrial competitiveness and improve production flexibility.

Electric Vehicles represent the leading application segment due to large-scale battery cell manufacturing expansion, aggressive EV localization strategies, and rising deployment of high-capacity gigafactories. EV-focused battery production lines account for more than 62% of advanced machinery installations in 2026, with automated assembly and testing systems improving production throughput by nearly 30%. China, the U.S., and Germany continue accelerating investments in high-speed cylindrical and prismatic battery manufacturing infrastructure to support domestic EV supply-chain resilience. Energy Storage is emerging as the fastest-growing application as utilities and renewable energy operators deploy grid-scale battery systems requiring larger-format cell production and long-duration storage technologies.

Consumer Electronics remains a mature but technologically intensive segment where miniaturized battery formats demand precision coating and high-speed inspection systems. Industrial Batteries are gaining traction in warehouse automation and heavy equipment electrification, while Medical Devices continue driving demand for compact, high-reliability battery manufacturing processes with strict quality validation requirements. Battery equipment manufacturers are adapting through customized automation platforms, flexible production tooling, and strategic integration partnerships targeting diverse battery form factors and end-use specifications.

Automotive companies remain the dominant end-user group due to large-scale EV battery manufacturing expansion, vertically integrated supply-chain strategies, and growing demand for localized cell production capabilities. Automotive battery plants account for nearly 58% of high-throughput machinery deployments, with automated assembly systems reducing production cycle times by approximately 26%. Major vehicle manufacturers in China, Germany, and the U.S. are increasingly investing in dedicated battery manufacturing ecosystems to improve operational control and secure long-term battery availability. Energy & Utilities represents the fastest-growing end-user segment as utility-scale storage projects accelerate deployment of large-format battery systems requiring advanced coating, formation, and testing infrastructure.

Electronics manufacturers continue prioritizing compact, high-speed battery production systems to support smartphones, wearables, and portable computing devices, while Industrial end-users expand demand through warehouse automation and electric industrial equipment adoption. Healthcare applications maintain niche but strategically important demand for precision battery manufacturing with ultra-low defect tolerance. Equipment suppliers are responding through application-specific automation platforms, localized service partnerships, and scalable manufacturing architectures designed to support varying production volumes and chemistry requirements across multiple industrial sectors.

Asia-Pacific accounted for the largest market share at 48.6% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 20.4% between 2026 and 2033.

Localized Gigafactory Expansion Accelerates Automation Deployment

North America is rapidly strengthening its position in advanced battery manufacturing through large-scale gigafactory investments, localized supply-chain strategies, and industrial automation upgrades. The region contributes nearly 24% of global battery production machine deployments, supported by aggressive EV manufacturing expansion and energy storage infrastructure development. Automated electrode coating and robotic assembly systems are increasingly replacing semi-automated production workflows, improving manufacturing throughput by approximately 28% across newly commissioned facilities. Strategic partnerships between battery manufacturers and industrial robotics firms are accelerating deployment timelines, while government-backed clean manufacturing incentives continue driving domestic machinery procurement. U.S.-based battery projects announced during 2025–2026 significantly increased demand for precision testing and AI-enabled quality inspection systems across lithium-ion cell production plants.

United States Market Outlook: The United States remains the region’s operational center for advanced battery production equipment deployment due to large-scale EV manufacturing expansion and domestic battery localization programs. More than 70% of newly planned North American gigafactory projects are concentrated in the U.S., with states including Texas, Michigan, and Tennessee emerging as key industrial hubs. Manufacturers are prioritizing high-speed automated production lines, predictive maintenance systems, and localized engineering partnerships to shorten commissioning cycles and strengthen supply-chain resilience for automotive and grid-scale storage applications.

Sustainability-Led Manufacturing Modernization Reshapes Production Infrastructure

Europe continues advancing battery production machine adoption through strict emissions regulations, industrial decarbonization targets, and premium EV manufacturing requirements. The region accounts for nearly 21% of advanced battery machinery installations, with Germany, Sweden, and France leading automated cell manufacturing expansion. European battery facilities are prioritizing solvent recovery systems, dry electrode technologies, and energy-efficient production architectures capable of lowering factory energy consumption by approximately 26%. Cross-border industrial partnerships and localized raw material processing initiatives are accelerating integrated battery manufacturing ecosystems. Battery equipment suppliers are also increasing investment in modular automation systems to support evolving solid-state battery production requirements and flexible cell configurations across automotive and energy storage sectors.

Germany Market Outlook: Germany remains Europe’s strongest battery production machine market due to its precision engineering ecosystem, advanced automotive manufacturing base, and industrial automation leadership. German battery facilities are increasingly integrating AI-driven inspection systems and high-speed robotic assembly platforms capable of improving production consistency by nearly 23%. Domestic manufacturers continue expanding strategic collaborations with EV producers and industrial robotics firms, while government-backed industrial modernization programs strengthen localized battery manufacturing infrastructure and next-generation cell production capabilities.

High-Volume Manufacturing Scale Strengthens Global Leadership

Asia-Pacific dominates the battery production machine market through unmatched battery manufacturing scale, vertically integrated supply chains, and concentrated gigafactory deployment activity. The region contributes over 60% of global lithium-ion cell production capacity, with China, South Korea, and Japan leading high-throughput equipment adoption across EV and consumer electronics manufacturing. Automated coating and assembly systems are achieving utilization rates exceeding 85% in major Chinese battery plants, while regional manufacturers continue scaling export-oriented machinery production. Strategic investment in sodium-ion and semi-solid battery technologies is also driving demand for adaptable modular production equipment. Industrial automation suppliers across the region are expanding software-integrated manufacturing ecosystems to improve operational precision and long-term production flexibility.

China Market Outlook: China remains the global center for battery production machine manufacturing and deployment due to its vertically integrated battery ecosystem, industrial scale, and aggressive EV supply-chain expansion. The country controls more than 45% of global lithium-ion production infrastructure and continues investing heavily in AI-enabled manufacturing systems, laser welding technologies, and high-speed coating equipment. Domestic equipment suppliers are strengthening export competitiveness through localized component sourcing, faster installation cycles, and integrated smart-factory solutions supporting both domestic and international battery manufacturers.

Resource-Driven Industrialization Supports Emerging Deployment Activity

South America is gradually expanding its battery production machine market through lithium resource development, renewable energy projects, and early-stage battery manufacturing initiatives. The region currently represents a smaller share of global equipment deployment, yet industrial activity is increasing around localized battery processing and energy storage infrastructure modernization. Brazil and Chile are strengthening partnerships with Asian and European battery technology firms to improve domestic battery value-chain participation. Production equipment demand is rising for pilot-scale coating, testing, and packaging systems supporting regional EV and industrial battery projects. Infrastructure limitations and limited large-scale automation capacity remain operational constraints, but targeted industrial investments and resource-driven manufacturing strategies are improving long-term deployment potential.

Brazil Market Outlook: Brazil leads South America’s battery production machine activity through expanding industrial electrification projects, renewable energy investments, and automotive manufacturing modernization efforts. The country is increasing deployment of automated battery assembly and testing systems for industrial mobility and grid-support applications. Brazilian manufacturers are also pursuing strategic partnerships with international battery equipment providers to strengthen local engineering capabilities and reduce reliance on imported production infrastructure amid rising regional battery demand.

Industrial Diversification Initiatives Drive Infrastructure Investment

The Middle East & Africa battery production machine market is developing through industrial diversification programs, renewable energy expansion, and localized manufacturing ambitions. The region is witnessing increasing investment in battery assembly infrastructure linked to energy storage, electric mobility, and mining sector electrification projects. Gulf countries are prioritizing smart industrial zones and advanced manufacturing ecosystems capable of supporting automated battery production facilities. Several infrastructure modernization initiatives launched during 2025–2026 accelerated deployment of robotic assembly systems and industrial quality-control platforms. While large-scale battery cell manufacturing remains limited, strategic partnerships with Asian technology providers are improving technical expertise and equipment deployment readiness across emerging industrial clusters.

Saudi Arabia Market Outlook: Saudi Arabia is becoming the region’s leading battery production machine market through industrial diversification initiatives and large-scale clean energy investments. The country is expanding localized battery manufacturing capabilities to support EV adoption and renewable energy storage projects under long-term industrial transformation programs. Industrial zones focused on advanced manufacturing are attracting automation suppliers and battery technology partnerships, while government-backed infrastructure programs continue strengthening domestic production capacity for energy storage and mobility-related battery systems.

The battery production machine market is dominated by global automation leaders competing against specialized regional equipment manufacturers and vertically integrated battery technology suppliers. Wuxi Lead, Yinghe Technology, Manz, Hirano Tecseed, and Sovema Group collectively control nearly 43% of advanced production equipment deployments, competing through manufacturing speed, precision automation, digital integration, and turnkey gigafactory solutions. Chinese manufacturers are aggressively competing on cost efficiency and installation speed, reducing commissioning timelines by approximately 20%, while German and Japanese firms focus on ultra-precision coating, defect reduction, and AI-enabled process optimization capable of improving yield consistency by over 25%. Companies are strengthening market position through robotics partnerships, localized engineering hubs, and integrated software ecosystems supporting predictive maintenance and real-time quality control. Competition is increasingly shifting toward modular production systems compatible with sodium-ion and solid-state batteries. High capital intensity, process engineering expertise, and long validation cycles remain major entry barriers. Market leadership now depends on scalable automation, localization capability, and integrated smart manufacturing execution.

Wuxi Lead Intelligent Equipment

Yinghe Technology

Manz AG

Hirano Tecseed

Sovema Group

Hitachi High-Tech Corporation

Fuji Corporation

CKD Corporation

PNT Co., Ltd.

Shenzhen Geesun Intelligent Technology

CIS Co., Ltd.

Rosendahl Nextrom

Toray Engineering

Dürr AG

Battery production machines are rapidly transitioning toward AI-enabled automation, high-speed robotics, and inline digital inspection systems to support large-scale lithium-ion manufacturing efficiency. Smart coating and assembly platforms improve production throughput by nearly 28% while reducing defect rates by approximately 22% compared with conventional semi-automated systems. More than 64% of newly commissioned gigafactories in 2026 are integrating predictive maintenance and machine-learning-driven quality control to stabilize multi-shift operations. Manufacturers deploying connected production ecosystems gain stronger yield consistency, lower scrap generation, and faster commissioning cycles across EV and energy storage battery plants.

Emerging technologies such as dry electrode coating, digital twins, and modular production architectures are reshaping battery factory design between 2026 and 2028. Dry coating systems reduce factory energy consumption by nearly 32% and lower floor-space requirements by approximately 20% compared with wet processing lines. Japanese and German equipment manufacturers are scaling flexible modular systems capable of supporting lithium-ion, sodium-ion, and semi-solid battery chemistries on shared manufacturing infrastructure, improving long-term equipment utilization and reducing line conversion downtime.

Disruptive solid-state battery manufacturing technologies are creating a new competitive divide between integrated automation leaders and conventional machinery suppliers. Companies adopting AI-driven adaptive process control and dry electrode manufacturing platforms are achieving nearly 25% faster production optimization during pilot-scale deployments. Chinese and South Korean equipment providers benefit most from this transition due to vertically integrated supply chains, advanced robotics capabilities, and accelerated industrial-scale deployment readiness.

March 2025 – Dürr AG and GROB-WERKE expanded their strategic partnership for battery cell production technology after Manz exited the alliance, strengthening integrated factory equipment capabilities across Europe and North America. The collaboration now covers nearly the entire battery manufacturing value chain, improving large-scale deployment flexibility and industrial competitiveness.

June 2025 – Dürr and GROB introduced a lithium-ion battery concept factory featuring dry electrode coating and advanced Z-folding assembly technology. The system reduces factory energy and space requirements by nearly 50%, enabling lower operating costs and higher production efficiency for next-generation battery manufacturing facilities.

April 2025 – Manz AG completed asset sales involving Tesla Automation, Greatech, and its Asia subgroup management team following insolvency proceedings. The restructuring accelerated consolidation within the battery production equipment sector and strengthened Tesla Automation’s strategic position in advanced lithium-ion manufacturing system integration.

February 2026 – Wuxi Lead Intelligent Equipment advanced its international expansion strategy through a Hong Kong listing initiative targeting approximately HK$4.29 billion to strengthen global R&D and service infrastructure. The move reinforces China’s leadership in intelligent battery production systems supporting EV and energy storage manufacturing scalability.

The Battery Production Machine Market report delivers detailed analysis across coating equipment, assembly equipment, testing equipment, cutting equipment, and packaging equipment, with strategic evaluation of operational adoption patterns and manufacturing integration trends. The study covers applications including electric vehicles, consumer electronics, energy storage, industrial batteries, and medical devices while assessing purchasing behavior across automotive, electronics, energy & utilities, industrial, and healthcare end-users. Asia-Pacific accounts for the highest deployment concentration, while North America demonstrates accelerating automation adoption and localized gigafactory expansion between 2026 and 2033.

The report evaluates advanced technologies including AI-enabled inspection systems, dry electrode processing, predictive maintenance platforms, and modular manufacturing architectures shaping next-generation battery production ecosystems. More than 60% of emerging battery facilities are transitioning toward fully automated production environments, increasing demand for high-speed precision equipment and digital manufacturing integration. Strategic insights support expansion planning, competitive benchmarking, investment prioritization, supply-chain optimization, partnership development, and long-term positioning across lithium-ion, sodium-ion, and solid-state battery manufacturing segments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 15550.92 Million |

|

Market Revenue in 2033 |

USD 61700.34 Million |

|

CAGR (2026 - 2033) |

18.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Wuxi Lead Intelligent Equipment, Yinghe Technology, Manz AG, Hirano Tecseed, Sovema Group, Hitachi High-Tech Corporation, Fuji Corporation, CKD Corporation, PNT Co., Ltd., Shenzhen Geesun Intelligent Technology, CIS Co., Ltd., Rosendahl Nextrom, Toray Engineering, Dürr AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |