Reports

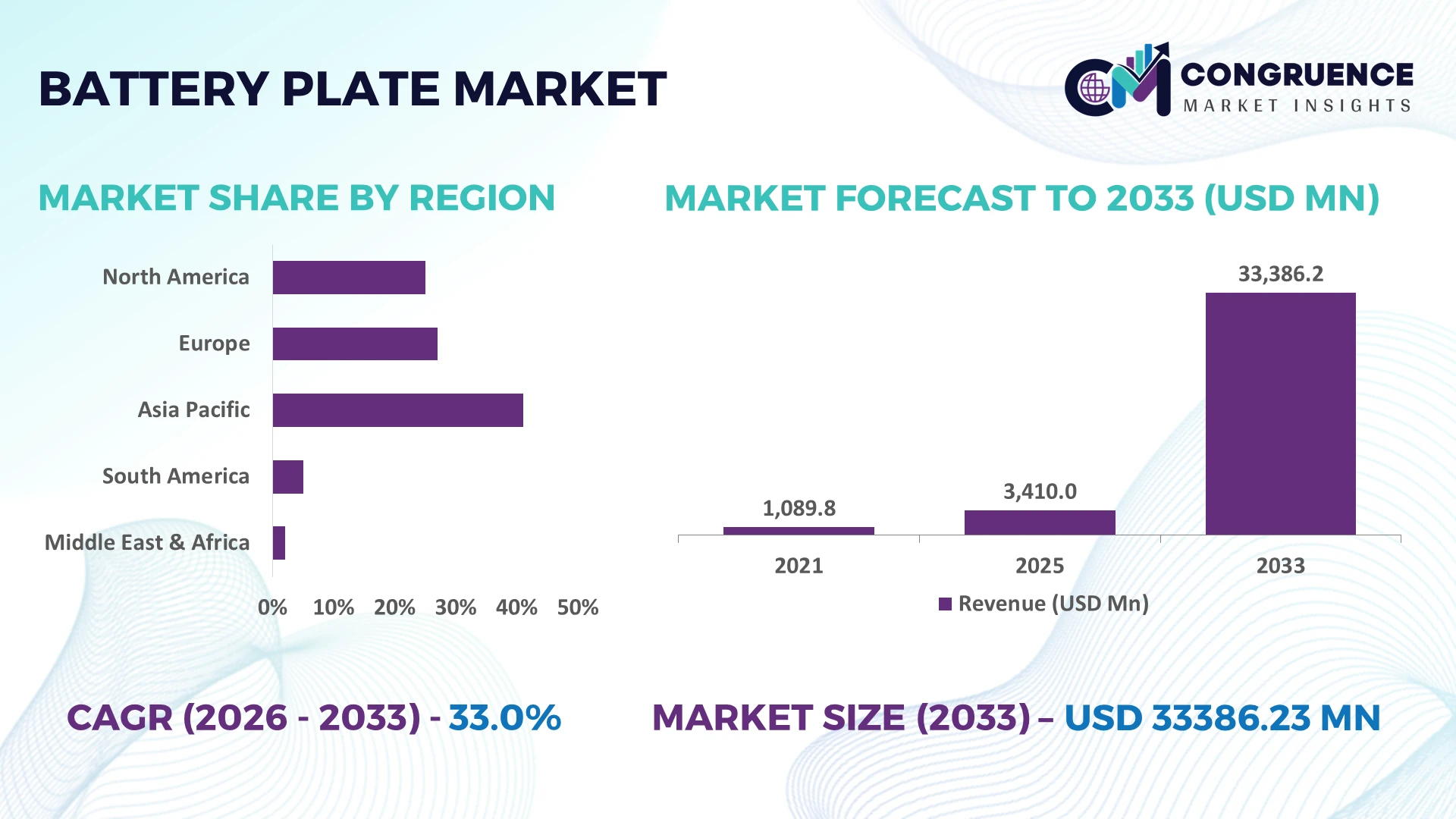

The Global Battery Plate Market was valued at USD 3410 Million in 2025 and is anticipated to reach a value of USD 33386.23 Million by 2033 expanding at a CAGR of 33% between 2026 and 2033. Growth is driven by rapid expansion of electric vehicle battery manufacturing, advanced lead-acid battery modernization, and automated plate production supported by localized critical mineral processing.

China remains the dominant battery plate manufacturing hub, accounting for approximately 52% of global production capacity, supported by large-scale EV supply chains, energy storage investments, and automated battery manufacturing. India is emerging as a strategic alternative with battery manufacturing investments exceeding 120 GWh of planned capacity, while Europe accelerates localization under the Critical Raw Materials Act, reducing import dependence and strengthening regional supply resilience.

Manufacturers prioritizing regionalized production, advanced plate technologies, and resilient raw material sourcing are positioned to secure long-term competitive advantages across high-growth battery applications.

Market Size & Growth: USD 3410 million (2025) to USD 33386.23 million (2033) at 33% CAGR, driven by EV battery expansion and localized manufacturing.

Top Growth Drivers: EV production +28%, grid-scale energy storage +31%, battery recycling capacity +22% globally.

Short-Term Forecast: By 2028, automated production reduces manufacturing defects by 18% while improving throughput by 25%.

Emerging Technologies: AI quality inspection, robotic plate assembly, and advanced lead-alloy engineering improve production efficiency by over 20%.

Regional Leaders: Asia-Pacific exceeds USD 18 billion, Europe approaches USD 7 billion, North America surpasses USD 5 billion, supported by domestic battery investments.

Consumer & End-User Trends: More than 60% of new battery manufacturing projects target EV and stationary energy storage applications.

Pilot/Case Example: A 2026 smart manufacturing deployment increased battery plate production efficiency by 19% while lowering material waste by 14%.

Competitive Landscape: Top manufacturers collectively control nearly 45% of global supply alongside established battery component producers.

Regulatory & ESG Impact: Recycling initiatives recover over 85% of lead materials, supporting circular manufacturing and supply security.

Investment & Funding: More than USD 20 billion supports battery manufacturing expansion, joint ventures, and regional supply-chain localization.

Innovation & Future Outlook: High-performance plate coatings, digital production monitoring, and next-generation manufacturing strengthen long-term competitiveness amid global supply-chain diversification.

Battery plate manufacturers are expanding solutions for electric mobility, industrial backup power, renewable energy storage, and telecom infrastructure where durability and charging performance remain critical purchasing factors. Advanced alloy formulations and automated precision manufacturing have improved plate consistency by nearly 20%, while regional supply-chain localization and stricter recycling requirements continue reshaping procurement strategies, setting the stage for broader strategic market evaluation.

Battery plate manufacturing has become a strategic priority as battery supply chains shift toward localized production, advanced automation, and secure raw material sourcing. Competition increasingly depends on production efficiency, material recovery, and quality consistency rather than manufacturing scale alone. Government-backed battery ecosystem programs in China, India, and the United States are accelerating industrial capacity while stricter recycling frameworks encourage greater integration of secondary lead into commercial production.

Advanced robotic casting and AI-enabled inspection systems deliver approximately 18% higher production efficiency and reduce defect rates by nearly 22% compared with conventional manual manufacturing lines. China continues to lead large-scale deployment through vertically integrated battery clusters, while Germany emphasizes precision manufacturing, digital quality management, and high-value industrial batteries. Over the next two to three years, automated production lines are expected to account for more than 55% of newly commissioned battery plate facilities, improving throughput and reducing production variability. Several manufacturers are expanding closed-loop recycling partnerships to secure raw material availability while lowering operational dependence on imported feedstock.

Battery producers are also integrating digital manufacturing platforms with predictive maintenance to improve equipment utilization and reduce unplanned downtime by around 15%. Companies investing in localized supply partnerships, automation, and advanced alloy technologies are strengthening competitive positioning through lower operating costs, improved product consistency, and greater resilience against evolving industrial and regulatory requirements.

Rapid electrification and industrial energy storage deployment continue to reshape battery plate production priorities. Global EV production increased by more than 25% during the past year, while stationary battery installations expanded by approximately 30%, creating sustained demand for high-performance battery components. India's battery manufacturing ecosystem is expanding through large-scale cell production projects, while China's integrated supply chain supports high-volume plate manufacturing with advanced automation. In response, manufacturers are investing in robotic casting, precision alloy engineering, and recycling integration to improve material utilization by nearly 15% and shorten production cycles. Strategic partnerships with battery manufacturers are also strengthening long-term supply agreements and improving operational flexibility across industrial and mobility applications.

Battery plate manufacturers continue to face pressure from fluctuating lead prices, uneven secondary material availability, and concentrated raw material sourcing. Recycled lead supplies account for nearly 60% of production feedstock in several industrial markets, yet collection and processing infrastructure remains inconsistent across developing economies. Periodic logistics disruptions and tightening environmental compliance requirements increase procurement costs and production planning complexity. Companies are reducing exposure through long-term procurement contracts, localized recycling facilities, and diversified supplier networks. Investment in advanced material recovery technologies is also improving feedstock stability while reducing operational dependence on imported raw materials, strengthening manufacturing resilience despite ongoing supply-chain uncertainty.

The next wave of competitive advantage is emerging from intelligent manufacturing and next-generation battery plate materials. AI-driven production monitoring improves process consistency by approximately 20%, while automated inspection systems reduce quality defects by nearly 18%. Japan and South Korea continue investing in precision manufacturing technologies that enable thinner, higher-performance battery plates with longer operational life. Companies are expanding research partnerships focused on corrosion-resistant alloys, digital manufacturing platforms, and closed-loop recycling systems. A growing opportunity also exists in industrial backup power, telecom infrastructure, and renewable energy storage, where longer service life and lower maintenance requirements provide measurable lifecycle cost advantages beyond conventional automotive demand.

Maintaining consistent product quality while rapidly expanding manufacturing capacity remains a major execution challenge. Automated production requires highly skilled technical personnel, yet workforce shortages exceed 20% in several advanced manufacturing locations. Equipment standardization across multi-country production networks also remains limited, creating variability in product performance and quality assurance. Increasing digitalization further requires secure production data management and integrated factory systems to maintain operational continuity. Companies are addressing these issues through workforce training, digital quality control platforms, standardized production protocols, and cross-border technology partnerships. Organizations capable of scaling automation while preserving manufacturing precision will secure stronger long-term competitiveness in increasingly demanding battery supply chains.

AI-Driven Manufacturing Expansion AI-enabled visual inspection and robotic plate handling are reducing production defects by nearly 22% while increasing manufacturing throughput by around 18%. Battery producers in China and South Korea are integrating digital factory platforms to counter skilled labor shortages and improve production consistency. Companies are expanding automation partnerships to shorten delivery cycles and stabilize quality across high-volume battery manufacturing.

Localized Supply Chain Integration Supply-chain restructuring is accelerating as manufacturers shift sourcing closer to battery production facilities. More than 45% of new capacity announcements emphasize regional raw material procurement and recycled lead utilization, while transport distances have fallen by approximately 15% in selected manufacturing clusters. Companies are restructuring supplier networks and investing in localized recycling operations to improve inventory resilience and reduce logistics disruptions.

Advanced Plate Material Optimization High-performance alloy formulations and precision grid engineering are extending battery cycle life by roughly 20% while lowering internal resistance by nearly 12%. Industrial buyers increasingly prioritize durability over initial component cost, particularly in backup power applications. Manufacturers are expanding material research collaborations and upgrading production lines to deliver higher-performance battery plates for demanding operational environments.

Circular Manufacturing Adoption Environmental compliance and resource efficiency are driving broader deployment of closed-loop production systems. Modern recovery technologies now reclaim more than 90% of lead from end-of-life batteries, reducing virgin material dependence and improving supply continuity. Companies are scaling recycling partnerships, integrating traceability platforms, and redesigning manufacturing workflows to strengthen regulatory compliance while improving long-term operational efficiency.

Tubular Plates represent the leading segment because of their superior durability, deep-cycle capability, and strong suitability for industrial batteries, renewable energy storage, and backup power applications. Their operational lifespan is typically 30–40% longer than conventional flat designs, making them the preferred choice for high-duty installations. Flat Plates continue serving cost-sensitive automotive applications where high-volume manufacturing and established production infrastructure maintain stable demand. Positive Plates and Negative Plates remain fundamental components across battery assembly, with continuous improvements in alloy composition enhancing conductivity and manufacturing precision.

AGM Plates are emerging as the fastest-growing type as maintenance-free battery designs gain wider acceptance across automotive start-stop systems, UPS equipment, and premium energy storage applications. Production efficiency has improved by approximately 18% through automated plate fabrication and precision coating technologies, while manufacturers are expanding specialized product portfolios and strategic partnerships to support advanced battery platforms. Investment priorities increasingly favor high-performance plate technologies capable of delivering longer operational life, greater reliability, and improved manufacturing consistency across evolving battery applications.

Automotive Batteries remain the dominant application due to large-scale vehicle production, replacement demand, and expanding electrification programs. More than 55% of battery plate consumption continues to originate from automotive manufacturing, supported by continuous improvements in production automation and quality control. Industrial Batteries maintain a stable position across manufacturing, mining, and material-handling operations where dependable power delivery remains operationally critical. UPS Systems and Telecom Backup continue generating consistent demand as digital infrastructure expands and uninterrupted power availability becomes increasingly important.

Energy Storage is the fastest-growing application as renewable integration and grid modernization accelerate deployment of stationary battery systems. Utility-scale installations have expanded by approximately 30%, increasing demand for high-cycle battery plates optimized for longer service life. Manufacturers are responding through dedicated production capacity, automation investments, and collaborative product development for large-scale storage projects. Companies are also strengthening customized solutions across automotive and industrial applications, enabling greater operational flexibility while addressing diverse battery performance requirements across evolving infrastructure sectors.

The Automotive sector remains the largest end-user because of continuous vehicle production, replacement battery demand, and expanding manufacturing ecosystems. Approximately 58% of battery plate procurement is linked to automotive production, where manufacturers prioritize consistent quality, high-volume supply, and production efficiency. Industrial customers remain significant buyers for forklifts, backup systems, and heavy equipment requiring dependable battery performance. Telecommunications also sustain steady procurement as network expansion and uninterrupted power infrastructure remain operational priorities.

Data Centers represent the fastest-growing end-user segment as digital infrastructure expansion increases demand for reliable backup power systems. Backup battery installations supporting mission-critical facilities have expanded by nearly 25%, while Energy & Utilities continue increasing battery deployment for grid resilience and renewable integration. Manufacturers are responding with customized plate designs, long-term supply partnerships, and application-specific engineering to improve lifecycle performance. Competitive positioning increasingly depends on delivering specialized battery solutions tailored to operational intensity, maintenance requirements, and infrastructure reliability across diverse industrial sectors.

Asia-Pacific accounted for the largest market share at 54% in 2025 however, North America is expected to register the fastest growth, expanding at a 35% CAGR between 2026 and 2033.

Advanced Manufacturing and Domestic Supply Chain Expansion

North America is strengthening its position through battery manufacturing localization, automation, and integrated recycling infrastructure. The region contributes approximately 22% of global battery plate demand, supported by expanding EV production, utility-scale energy storage deployment, and resilient backup power investments. Manufacturers are increasing robotic production capacity while integrating recycled lead into commercial manufacturing to improve supply security. More than 70% of newly announced battery manufacturing projects incorporate automated quality inspection and digital production management. Strategic partnerships between battery manufacturers, material suppliers, and recycling companies are shortening procurement cycles while improving production consistency. Infrastructure investments and supportive industrial policies continue encouraging domestic manufacturing, reducing import dependency, and strengthening long-term operational resilience across mobility and industrial power applications.

United States Market Outlook: The United States remains the regional leader due to its integrated battery manufacturing ecosystem, expanding energy storage infrastructure, and advanced industrial automation. More than 160 GWh of announced battery manufacturing capacity supports increasing demand for high-performance battery components. Companies continue investing in recycling facilities, intelligent manufacturing systems, and long-term raw material agreements to strengthen domestic production while improving supply-chain resilience for automotive, industrial, and utility-scale battery applications.

Circular Manufacturing Drives Competitive Advantage

Europe continues strengthening battery plate manufacturing through sustainability-focused industrial policies, advanced production technologies, and circular economy initiatives. The region represents approximately 18% of global market activity, with manufacturers prioritizing recycled materials, precision engineering, and localized battery supply chains. More than 65% of new industrial battery projects integrate recycled lead into production to improve material efficiency and regulatory compliance. Growing deployment of renewable energy storage and industrial electrification is encouraging manufacturers to modernize production facilities while expanding strategic partnerships across battery value chains. Digital quality management and energy-efficient manufacturing processes are improving operational consistency and supporting premium battery applications throughout the region.

Germany Market Outlook: Germany leads European battery plate manufacturing through advanced engineering capabilities, automotive leadership, and industrial automation. Battery manufacturers continue investing in precision production technologies and high-quality battery materials for mobility and industrial energy storage. Automated manufacturing systems now support approximately 80% of large-scale battery production facilities, enabling higher production efficiency and consistent quality while reinforcing Germany's position within Europe's battery supply network.

Manufacturing Scale Sustains Global Leadership

Asia-Pacific remains the world's largest battery plate manufacturing center due to its extensive battery production ecosystem, integrated raw material processing, and export-oriented industrial capacity. The region accounts for approximately 54% of global demand, supported by large-scale electric vehicle manufacturing and expanding renewable energy infrastructure. Battery manufacturers continue increasing automated production, while several industrial clusters have improved production efficiency by nearly 20% through intelligent manufacturing technologies. Strong domestic demand, extensive supplier networks, and continuous factory expansion enable shorter production cycles and competitive manufacturing costs. Companies are further strengthening regional leadership through capacity expansion, localized recycling, and strategic investments across the battery value chain.

China Market Outlook: China dominates global battery plate manufacturing through unmatched production capacity, vertically integrated supply chains, and advanced battery technology development. The country contributes more than half of global battery manufacturing capacity while continuously expanding intelligent production facilities. Companies are investing in automated manufacturing, recycling integration, and high-performance battery technologies, reinforcing export competitiveness and maintaining leadership across automotive, industrial, and stationary energy storage applications.

Industrial Modernization Expands Battery Demand

South America is witnessing gradual expansion driven by industrial modernization, mining operations, telecom infrastructure, and renewable energy integration. The region contributes approximately 4% of global battery plate demand while increasing investments in localized battery assembly and recycling capabilities. Utility modernization and backup power requirements continue supporting stable procurement of industrial batteries. Manufacturers are improving logistics networks and establishing regional partnerships to reduce import dependence and improve product availability. Infrastructure limitations and uneven manufacturing capabilities remain operational constraints, yet growing industrial electrification continues strengthening long-term market fundamentals across several national economies.

Brazil Market Outlook: Brazil represents the largest battery plate market in South America through its automotive manufacturing base, mining sector, and expanding industrial infrastructure. Domestic battery manufacturers continue increasing production efficiency while strengthening recycling capabilities to improve raw material availability. More than 40% of regional automotive battery production is concentrated in Brazil, supporting continued investment in manufacturing modernization and industrial supply-chain development.

Infrastructure Investment Supports Market Transformation

The Middle East & Africa market is expanding through infrastructure modernization, industrial diversification, and increasing deployment of backup power systems. The region accounts for approximately 2% of global battery plate demand, supported by utility upgrades, telecommunications expansion, and commercial infrastructure projects. Large-scale energy developments continue increasing demand for reliable battery systems capable of operating in demanding environments. Manufacturers are establishing regional distribution partnerships and localized service capabilities to improve delivery efficiency and customer support. Modernization initiatives, together with expanding industrial investment, are strengthening long-term market competitiveness despite varying manufacturing capabilities across national markets.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through industrial diversification initiatives, expanding renewable energy investments, and large-scale infrastructure projects. Battery demand continues rising across utility, telecom, and industrial applications as new facilities require dependable backup power systems. National industrial programs and manufacturing investments are encouraging greater localization of battery supply chains while improving procurement efficiency and supporting long-term operational reliability.

The Battery Plate Market is led by companies including Clarios, Exide Industries, EnerSys, GS Yuasa, and East Penn Manufacturing, competing directly with regional manufacturers across India, China, and Southeast Asia. Global leaders emphasize technology integration, vertically integrated recycling, and long-term OEM contracts, while regional producers compete through lower production costs, flexible customization, and faster delivery. The top five participants collectively account for approximately 48% of global market activity, reflecting moderate market concentration. Competition increasingly depends on manufacturing efficiency, where automated production reduces defect rates by nearly 22% and advanced alloy engineering extends plate durability by around 18%. Companies are expanding recycling capacity, forming battery manufacturing partnerships, and localizing supply chains to reduce procurement risks and improve production continuity. Industry consolidation is strengthening control over raw materials and processing capabilities, raising entry barriers for new manufacturers lacking integrated sourcing and precision manufacturing. Sustained success depends on automation, secure material access, product reliability, and application-specific innovation rather than competing on price alone.

Clarios

Exide Industries Limited

EnerSys

GS Yuasa Corporation

East Penn Manufacturing

Amara Raja Energy & Mobility

Leoch International Technology Limited

Camel Group Co., Ltd.

Chaowei Power Holdings Limited

Tianneng Holding Group

Hoppecke Batteries GmbH & Co. KG

Crown Battery Manufacturing Company

Advanced battery plate manufacturing is transitioning from conventional casting to AI-enabled production, robotic handling, and precision alloy engineering. Automated inspection systems improve defect detection by approximately 22%, while robotic plate assembly increases production throughput by nearly 18% compared with traditional manual manufacturing. More than 55% of newly commissioned high-volume production facilities are integrating intelligent process monitoring to improve consistency, reduce scrap generation, and optimize material utilization. Manufacturers adopting these technologies achieve stronger quality assurance and greater operational flexibility across automotive and industrial battery production.

Emerging technologies focus on corrosion-resistant lead alloys, laser-assisted grid formation, and digital twin manufacturing platforms. Compared with conventional production methods, advanced alloy technologies extend operational life by nearly 20% while reducing internal resistance by approximately 12%. Predictive maintenance platforms decrease unexpected equipment downtime by around 15%, enabling more stable production scheduling. Large integrated manufacturers benefit most because digital manufacturing strengthens process repeatability while supporting rapid product customization for specialized industrial, telecom, and energy storage applications.

Between 2026 and 2028, intelligent manufacturing ecosystems, closed-loop recycling integration, and AI-driven production optimization will become key competitive differentiators. Smart factories integrating real-time production analytics are expected to exceed 65% deployment among newly expanded battery manufacturing facilities. Companies investing early in automation, advanced materials, and digital quality management will achieve faster production scaling, improved supply resilience, lower operating costs, and stronger competitive positioning as customers increasingly prioritize performance consistency and manufacturing reliability.

June 2024 Exide Industries expanded its lead-acid battery recycling capacity in India to strengthen raw material recovery and improve circular manufacturing. The expansion increased recycled lead availability for battery production, enhancing supply-chain resilience and manufacturing efficiency.

January 2025 Clarios secured a second supply agreement with a major U.S. automaker for its advanced hAGM batteries, with planned annual production of up to 745,000 units beginning in late 2026. The agreement reinforces long-term OEM relationships and strengthens premium battery technology leadership.

January 2025 EnerSys received a U.S. Department of Energy award worth USD 199 million to establish a lithium-ion gigafactory in South Carolina. The project expands domestic battery manufacturing capacity and supports localized battery supply-chain development across advanced energy applications.

March 2025 Clarios introduced its next-generation Enhanced Flooded Battery (EFB) technology delivering approximately 20% higher charge acceptance and improved cycle life for start-stop vehicles. The innovation strengthens product competitiveness while supporting higher-performance automotive battery platforms across major vehicle markets.

This report provides comprehensive analysis of the Battery Plate Market across Positive Plates, Negative Plates, Flat Plates, Tubular Plates, and AGM Plates, together with detailed assessment of Automotive Batteries, Industrial Batteries, UPS Systems, Energy Storage, and Telecom Backup applications. It evaluates demand across Automotive, Industrial, Telecommunications, Energy & Utilities, and Data Centers while examining competitive positioning of leading manufacturers operating throughout North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 50% of the analysis emphasizes manufacturing efficiency, supply-chain resilience, and technology adoption trends.

The study further assesses automation, advanced alloy development, AI-enabled manufacturing, digital quality control, and recycling integration shaping operational competitiveness between 2026 and 2033. Strategic evaluation includes regional deployment patterns, enterprise expansion initiatives, production localization, partnership activity, and evolving procurement strategies. Business stakeholders gain practical insights supporting investment prioritization, product portfolio optimization, manufacturing expansion, supply-chain planning, competitive benchmarking, and long-term positioning across established and emerging battery plate application segments.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 3410 Million |

Market Revenue in 2033 | USD 33386.23 Million |

CAGR (2026 - 2033) | 33% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Clarios, Exide Industries Limited, EnerSys, GS Yuasa Corporation, East Penn Manufacturing, Amara Raja Energy & Mobility, Leoch International Technology Limited, Camel Group Co., Ltd., Chaowei Power Holdings Limited, Tianneng Holding Group, Hoppecke Batteries GmbH & Co. KG, Crown Battery Manufacturing Company |

Customization & Pricing | Available on Request (10% Customization is Free) |