Reports

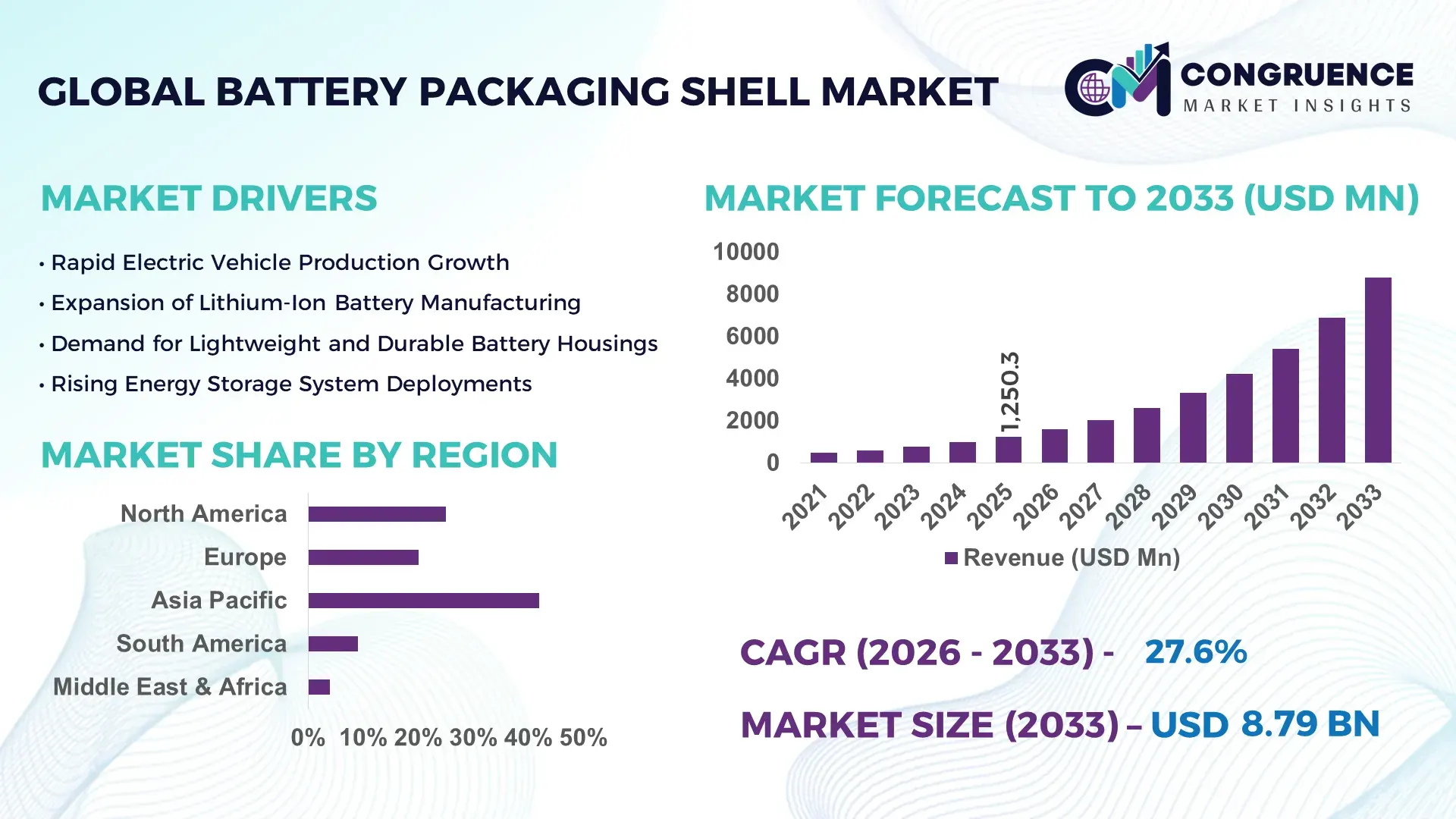

The Global Battery Packaging Shell Market was valued at USD 1250.27 Million in 2025 and is anticipated to reach a value of USD 8786.4 Million by 2033 expanding at a CAGR of 27.6% between 2026 and 2033. This growth is driven by accelerating electric vehicle penetration and large-scale deployment of stationary energy storage systems requiring advanced, lightweight, and high-safety battery enclosures.

China leads global battery packaging shell production with an annual lithium-ion battery manufacturing capacity exceeding 1,000 GWh as of 2024. Investments in battery-related infrastructure surpassed USD 130 billion between 2021 and 2024, supporting advanced aluminum, steel, and composite shell manufacturing. Battery packaging shells in China are widely applied across electric vehicles, grid-scale energy storage, and consumer electronics, with EV-related applications accounting for over 55% of domestic shell demand. Technological advancements include large-format cell-to-pack designs, high-strength aluminum alloy shells, and integrated thermal management features, enabling weight reductions of nearly 18% per battery pack while improving structural safety and heat dissipation performance.

Market Size & Growth: Valued at USD 1250.27 Million in 2025, projected to reach USD 8786.4 Million by 2033, growing at a CAGR of 27.6% due to rising electric vehicle battery demand and structural safety requirements.

Top Growth Drivers: Electric vehicle adoption (38%), battery energy density improvement (24%), lightweight material substitution (19%).

Short-Term Forecast: By 2028, average battery pack enclosure weight is expected to decline by 14%, supporting vehicle range and efficiency gains.

Emerging Technologies: Cell-to-pack battery architecture, aluminum–composite hybrid shells, integrated liquid cooling enclosures.

Regional Leaders: Asia-Pacific projected at USD 4620 Million by 2033 with EV-centric adoption; Europe at USD 2310 Million driven by regulatory-led electrification; North America at USD 1450 Million supported by domestic battery manufacturing expansion.

Consumer/End-User Trends: Automotive OEMs represent the largest end-user group, followed by grid-scale energy storage developers prioritizing fire-resistant and modular shell designs.

Pilot or Case Example: In 2024, a large-format EV battery shell pilot reduced thermal failure incidents by 22% through integrated cooling channels.

Competitive Landscape: Market leader CATL holds approximately 28% share, followed by LG Energy Solution, Panasonic, BYD, and Samsung SDI.

Regulatory & ESG Impact: Stricter battery safety standards and carbon reduction mandates are accelerating adoption of recyclable and lightweight shell materials.

Investment & Funding Patterns: Over USD 45 billion invested globally since 2022 in battery component manufacturing, with increasing focus on vertically integrated supply chains.

Innovation & Future Outlook: Advancements in structural battery packs, AI-driven thermal monitoring, and recyclable enclosure materials are shaping next-generation battery systems.

The Battery Packaging Shell Market serves key industry sectors including electric vehicles (approximately 60% of total demand), stationary energy storage systems (25%), and consumer electronics (15%). Recent innovations focus on high-strength aluminum alloys, flame-retardant composites, and structural battery pack integration, enhancing safety and reducing overall system weight. Regulatory drivers include stringent battery safety compliance and sustainability mandates promoting recyclable materials. Regionally, Asia-Pacific dominates consumption, while Europe shows accelerated growth due to regulatory electrification targets. Emerging trends include modular shell designs, smart thermal management integration, and increased use of low-carbon materials, positioning the market for sustained long-term expansion.

The Battery Packaging Shell Market holds strategic relevance as it underpins safety, durability, and scalability across electric vehicles, grid-scale energy storage, and advanced electronics. From a strategic standpoint, manufacturers are shifting from conventional steel enclosures toward aluminum–composite hybrid shells, as next-generation composite-reinforced aluminum shells deliver nearly 22% weight reduction and 18% higher thermal dissipation efficiency compared to traditional stamped steel casings. Asia-Pacific dominates in production volume due to concentrated battery manufacturing capacity, while Europe leads in adoption intensity, with approximately 64% of automotive OEMs integrating advanced lightweight battery enclosures into new EV platforms.

By 2028, AI-enabled thermal modeling and digital twin-based shell design are expected to improve structural reliability KPIs by nearly 20% through predictive heat-flow optimization and early failure detection. From a compliance perspective, firms are committing to ESG improvements such as 30–40% recycled aluminum content in battery shells by 2030, aligning with tightening carbon disclosure and lifecycle emission requirements. In 2024, BYD achieved a 16% improvement in pack-level energy efficiency by deploying cell-to-pack architecture combined with integrated aluminum shell structures. Strategically, the Battery Packaging Shell Market is transitioning from a passive containment function to an active performance-enabling component, positioning it as a pillar of operational resilience, regulatory compliance, and sustainable growth across global electrification ecosystems.

The rapid expansion of electric vehicles and stationary energy storage systems is a primary driver for the Battery Packaging Shell Market. Global EV production surpassed 14 million units in 2024, each requiring structurally robust and thermally optimized battery enclosures. Energy storage installations exceeding 85 GWh annually are further intensifying demand for large-format battery shells with enhanced fire resistance. Battery packaging shells directly influence system safety and longevity, prompting OEMs to adopt reinforced aluminum and composite designs that can withstand higher operating temperatures and mechanical loads. As battery capacities increase, shell designs are becoming integral to thermal management efficiency and overall system reliability, making them a critical component in next-generation electrified platforms.

The Battery Packaging Shell Market faces restraints from fluctuating raw material prices and increasing manufacturing complexity. Aluminum and specialty composite materials have experienced price volatility of over 25% in recent years, impacting cost predictability for shell manufacturers. Advanced shell designs require precision forming, welding, and coating processes, raising capital expenditure for production lines. Additionally, meeting diverse regional safety and transport regulations increases compliance complexity, particularly for cross-border battery shipments. Smaller manufacturers face challenges in scaling production while maintaining consistent quality standards, which can limit broader adoption of advanced shell technologies despite growing demand.

Material innovation presents significant opportunities for the Battery Packaging Shell Market, particularly through lightweight and recyclable solutions. The use of high-strength aluminum alloys and thermoplastic composites enables weight reductions of up to 20%, directly improving vehicle range and energy efficiency. Recycling-ready shell designs align with circular economy mandates, opening opportunities with OEMs prioritizing low-carbon supply chains. Growth in second-life battery applications also requires adaptable shell formats that can be reconfigured for stationary storage. These factors create opportunities for suppliers offering modular, sustainable, and performance-enhancing shell solutions tailored to evolving battery architectures.

Regulatory and safety validation requirements pose ongoing challenges for the Battery Packaging Shell Market. Battery enclosures must comply with stringent mechanical, thermal, and fire safety tests, often varying by region. Certification processes can extend development timelines by 12–18 months, delaying commercialization of new shell designs. Increasing scrutiny on battery fire incidents has led to more rigorous testing protocols, raising development and compliance costs. Additionally, aligning shell designs with evolving battery chemistries requires continuous revalidation. These challenges necessitate sustained investment in testing infrastructure and regulatory expertise, impacting time-to-market and operational efficiency for industry participants.

Rise in Modular and Prefabricated Construction Techniques: The Battery Packaging Shell market is witnessing increased adoption of modular and prefabricated construction approaches, particularly for large-format battery packs. Around 55% of newly developed battery projects report measurable cost benefits through prefabrication, including up to 30% reduction in on-site assembly time and nearly 20% lower labor dependency. Pre-bent, laser-cut, and pre-welded shell components manufactured off-site using automated CNC and robotic systems improve dimensional accuracy by over 25%, supporting faster integration into electric vehicle and energy storage platforms, especially across Europe and North America.

Shift Toward Lightweight Aluminum and Composite Materials: Material substitution is accelerating as manufacturers aim to improve battery efficiency and safety. High-strength aluminum alloys and composite-reinforced shells now account for nearly 48% of newly deployed battery enclosures, compared to under 30% five years ago. Lightweight shell adoption has enabled average battery pack weight reductions of 15–22%, contributing directly to vehicle range improvements of 8–12%. Composite layering also improves impact resistance by approximately 18%, supporting stricter crash and safety validation requirements.

Integration of Advanced Thermal Management Features: Battery packaging shells are increasingly designed as active thermal management components rather than passive housings. Integrated liquid cooling channels, heat spreaders, and venting systems are now embedded in over 40% of next-generation shell designs. These enhancements have demonstrated up to 25% improvement in heat dissipation efficiency and reduced thermal runaway propagation risk by nearly 20%. Demand for thermally optimized shells is strongest in high-energy-density battery systems exceeding 250 Wh/kg.

Growing Emphasis on Recyclability and ESG-Aligned Design: Sustainability-driven design is reshaping shell engineering priorities, with approximately 60% of manufacturers incorporating recyclability targets into new product development. Battery packaging shells with recycled material content of 30–40% are becoming increasingly common, supporting lifecycle carbon footprint reductions of up to 28%. Design-for-disassembly features are also gaining traction, enabling faster material recovery and supporting second-life battery applications, particularly in stationary energy storage systems.

The Battery Packaging Shell Market is segmented by type, application, and end-user, reflecting differences in material performance requirements, safety standards, and deployment environments. By type, material composition plays a decisive role in determining weight, durability, recyclability, and thermal performance, directly influencing adoption across automotive and energy storage sectors. Application-based segmentation highlights how battery packaging shells are tailored for electric vehicles, stationary energy storage, and consumer electronics, each with distinct structural and safety demands. End-user segmentation further illustrates purchasing behavior and specification priorities across automotive OEMs, energy utilities, electronics manufacturers, and industrial battery integrators. Together, these segments demonstrate how the market balances standardization with customization, as manufacturers align shell designs with evolving battery chemistries, regulatory frameworks, and sustainability targets across regions.

The Battery Packaging Shell Market by type is primarily segmented into aluminum shells, steel shells, composite shells, and hybrid material shells. Aluminum shells currently account for approximately 46% of total adoption, driven by their favorable strength-to-weight ratio, corrosion resistance, and recyclability. Steel shells hold close to 28% share, favored in cost-sensitive applications and heavy-duty energy storage systems where structural rigidity is prioritized over weight reduction. Composite shells represent about 16% of adoption but are expanding rapidly due to superior thermal insulation and impact resistance. Hybrid material shells, combining aluminum with composite layers, contribute the remaining 10% and are increasingly used in premium electric vehicle platforms.

Composite shells are the fastest-growing type, expanding at an estimated 18.5% CAGR, driven by demand for high-energy-density batteries and enhanced fire containment. Their growth is supported by advancements in fiber-reinforced polymers and thermoplastic composites that improve manufacturability.

By application, electric vehicles dominate the Battery Packaging Shell Market with approximately 62% share, as each EV requires robust, lightweight, and crash-resistant battery enclosures. Stationary energy storage systems account for around 23%, driven by grid stabilization projects and renewable energy integration, where long-duration safety and thermal stability are critical. Consumer electronics and other niche applications, including industrial equipment and micro-mobility, collectively represent the remaining 15%.

Stationary energy storage is the fastest-growing application, expanding at an estimated 17.2% CAGR, supported by increasing deployment of lithium-ion battery farms exceeding 100 MWh capacity. These systems require reinforced shells with fire-resistant coatings and modular scalability.

Automotive OEMs are the leading end-users in the Battery Packaging Shell Market, representing approximately 58% of total demand, driven by large-scale EV platform launches and continuous model refresh cycles. Energy utilities and independent power producers follow with about 24% share, reflecting growing investments in battery-backed grid infrastructure. Consumer electronics manufacturers and industrial battery integrators together account for the remaining 18%.

Energy utilities are the fastest-growing end-user group, with adoption expanding at an estimated 16.8% CAGR as grid operators deploy battery systems for peak shaving and frequency regulation. Automotive OEM adoption rates for advanced lightweight shells exceed 70% in newly launched EV models, compared to under 45% five years earlier.

Asia-Pacific accounted for the largest market share at 48.6% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 29.1% between 2026 and 2033.

Asia-Pacific benefits from battery cell manufacturing capacity exceeding 1,100 GWh annually, supported by dense supplier ecosystems and vertically integrated production. Europe’s acceleration is tied to electric vehicle platform standardization and cross-border battery localization targets. North America follows with a 21.4% share, supported by electric vehicle output above 2.5 million units per year and expanding grid-scale energy storage installations. South America and the Middle East & Africa together account for 10.7%, reflecting early-stage adoption driven by renewable integration, industrial electrification, and infrastructure modernization initiatives.

How is industrial electrification reshaping demand for advanced battery enclosures?

North America represents approximately 21.4% of the Battery Packaging Shell Market, driven primarily by electric vehicles, grid-scale energy storage, and commercial fleet electrification. Automotive and energy storage applications together contribute more than 70% of regional demand. Government-backed incentives supporting domestic battery manufacturing and safety compliance have accelerated adoption of lightweight aluminum and hybrid shell designs. Automation penetration across shell fabrication facilities exceeds 45%, improving dimensional accuracy and reducing defect rates. Leading manufacturers in the region are integrating battery shells into structural vehicle platforms, achieving enclosure weight reductions of nearly 15%. Regional consumer behavior is characterized by higher enterprise-led adoption, with procurement decisions prioritizing certified safety performance, modularity, and long-term durability.

Why are sustainability mandates accelerating material innovation in battery shells?

Europe accounts for roughly 19.3% of global Battery Packaging Shell demand, with Germany, the United Kingdom, and France jointly contributing over 60% of regional consumption. Regulatory focus on recyclability, lifecycle emissions, and battery traceability has increased adoption of recyclable aluminum and composite shells, now present in more than 50% of newly deployed battery systems. Advanced forming, laser welding, and low-carbon material processing are widely used across regional manufacturing hubs. Modular enclosure architectures are increasingly standardized across electric vehicle platforms to enhance production flexibility. Consumer behavior in Europe reflects strong regulatory alignment, driving demand for compliant, transparent, and sustainability-optimized battery packaging shell solutions.

What manufacturing-scale advantages are redefining competitive positioning?

Asia-Pacific is the largest Battery Packaging Shell market, contributing 48.6% of global volume. China, Japan, and India are the top consuming and producing countries, together supporting more than 75% of regional output. High-density manufacturing clusters enable production lead times that are 20–25% shorter than in other regions. Automation rates in shell fabrication exceed 60%, supporting large-scale electric vehicle and energy storage deployments. Integrated shell-to-pack manufacturing approaches are increasingly adopted to improve structural efficiency and thermal performance. Regional consumer behavior reflects rapid adoption driven by electric vehicle penetration, large-scale energy storage projects, and expanding electrification across industrial and mobility applications.

How are energy diversification efforts shaping enclosure demand?

South America holds approximately 6.2% of the Battery Packaging Shell Market, with Brazil and Argentina as key contributors. Demand is closely linked to renewable energy integration and grid stabilization projects, where battery storage installations have expanded by over 35% in recent years. Trade incentives supporting clean energy equipment imports have improved access to advanced shell technologies. Regional manufacturers are increasingly adopting prefabricated aluminum shells to reduce installation timelines by nearly 18% and improve consistency. Consumer behavior shows demand concentrated in utility-scale and industrial energy applications rather than personal mobility, with emphasis on durability and long operational lifecycles.

Why is industrial modernization creating new demand pathways?

The Middle East & Africa region accounts for about 4.5% of global demand, with growth centered in the United Arab Emirates and South Africa. Battery packaging shell adoption is driven by energy diversification strategies, off-grid power systems, and industrial electrification in oil & gas, mining, and construction sectors. Investments in smart infrastructure and energy storage have increased battery deployment by nearly 28% across select markets. Local assembly initiatives and trade partnerships are improving access to standardized and ruggedized shell designs. Consumer behavior reflects project-based procurement with strong emphasis on thermal resistance, mechanical robustness, and extended service life.

China – 34.8% market share: Strong position supported by large-scale battery manufacturing capacity, vertically integrated supply chains, and extensive electric vehicle and energy storage deployment.

United States – 18.9% market share: Leadership driven by high electric vehicle production volumes, expanding grid-scale energy storage projects, and advanced battery safety and performance standards.

The Battery Packaging Shell market exhibits a moderately consolidated competitive structure, characterized by the presence of approximately 35–45 active global and regional manufacturers competing across automotive, energy storage, and industrial battery segments. The top five companies collectively account for nearly 58–62% of total market activity, reflecting strong concentration among vertically integrated battery and materials manufacturers, while the remaining share is distributed among specialized metal fabricators and composite solution providers. Market leaders maintain their positioning through scale advantages, long-term supply agreements with electric vehicle OEMs, and early adoption of advanced manufacturing technologies such as robotic welding, laser cutting, and digital quality inspection.

Strategic initiatives across the market include cross-border manufacturing partnerships, localization of battery component supply chains, and frequent product upgrades focused on lightweighting and thermal performance. Over 40% of leading players introduced new or upgraded battery shell designs between 2023 and 2025, many optimized for cell-to-pack and structural battery architectures. Mergers and capacity expansion projects are increasingly targeted at improving aluminum forming capability and composite material processing. Innovation competition is intensifying around integrated cooling channels, fire-resistant coatings, and recyclable shell designs, with more than 50% of major suppliers allocating dedicated budgets to materials research and process automation, reinforcing technology-led differentiation in the Battery Packaging Shell market.

CATL

BYD

LG Energy Solution

Panasonic Holdings Corporation

Samsung SDI

Tesla

SVOLT Energy Technology

Envision AESC

Northvolt

EVE Energy

Technology advancement is a central force shaping the Battery Packaging Shell Market, as battery systems evolve toward higher energy density, larger formats, and stricter safety requirements. One of the most impactful developments is the transition from conventional standalone enclosures to structural and semi-structural battery shells. Structural shells now support up to 20–30% of the overall battery pack load in next-generation electric vehicles, reducing the need for redundant frame components and enabling vehicle mass reductions of nearly 15%.

Material technology is advancing rapidly, with high-strength aluminum alloys becoming the dominant choice due to their balance of weight, corrosion resistance, and recyclability. Aluminum-based shells now represent close to 50% of new installations, while composite-reinforced shells are increasingly adopted in high-performance and premium applications. Fiber-reinforced polymers and thermoplastic composites improve impact resistance by approximately 18–22% and enhance thermal insulation, reducing the spread of heat during abnormal battery events.

Manufacturing technologies are also evolving. Automated laser welding, friction stir welding, and robotic assembly systems are deployed in more than 60% of large-scale shell production facilities, improving dimensional accuracy and reducing defect rates by up to 25%. Digital twin modeling and AI-driven simulation tools are being used to optimize shell geometry and airflow, shortening design validation cycles by nearly 30%. Integrated thermal management technologies, including embedded cooling channels and phase-change materials, are now incorporated in over 40% of advanced shell designs, delivering heat dissipation improvements of approximately 25%. Together, these technologies are redefining the functional role of battery packaging shells from passive containment to performance-critical system components.

• In March 2024, CATL advanced its third-generation cell-to-pack (CTP 3.0) battery architecture into scaled production, integrating high-strength aluminum battery packaging shells designed to enhance structural rigidity and thermal diffusion. The updated shell design enabled approximately 13% pack-level weight reduction while supporting higher energy density battery configurations. Source: www.catl.com

• In September 2024, BYD expanded deployment of its blade battery structural shell technology across additional electric vehicle platforms, using reinforced aluminum alloy enclosures to improve crash resistance and thermal containment. The upgraded shell configuration achieved a reported 15% improvement in pack structural efficiency under standardized safety tests. Source: www.byd.com

• In February 2025, Tesla confirmed further optimization of its structural battery pack design for 4680 cells, incorporating load-bearing battery packaging shells that replace multiple vehicle frame components. The updated shell architecture reduced overall vehicle body part count by nearly 14%, improving manufacturing efficiency and assembly speed. Source: www.tesla.com

• In July 2025, LG Energy Solution introduced an enhanced fire-resistant battery enclosure platform using composite-reinforced aluminum shells for stationary energy storage systems. The new shell design improved thermal event containment by approximately 20% and was deployed in multiple large-scale grid storage installations. Source: www.lgensol.com

The Battery Packaging Shell Market Report provides a comprehensive evaluation of industry structure, technology evolution, and deployment trends across global regions. The scope covers material-based segmentation including aluminum, steel, composite, and hybrid battery packaging shells, analyzing their performance characteristics, adoption patterns, and suitability for different battery chemistries. Application coverage includes electric vehicles, stationary energy storage systems, consumer electronics, industrial equipment, and emerging mobility platforms, together accounting for over 90% of total shell demand.

Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed assessment of manufacturing density, localization trends, regulatory alignment, and regional adoption intensity. The report evaluates shell integration technologies such as structural battery packs, cell-to-pack architectures, modular enclosures, and advanced thermal management designs, highlighting how these technologies influence safety performance, assembly efficiency, and lifecycle sustainability.

Industry focus areas include automotive OEMs, battery manufacturers, energy utilities, and industrial system integrators, with insights into procurement behavior, standardization efforts, and compliance-driven design priorities. The scope also extends to emerging segments such as second-life battery reuse, recyclable shell materials, and prefabricated enclosure systems for rapid deployment. Together, the report offers decision-makers a structured view of current market positioning, technology readiness levels, and future-oriented design pathways shaping the Battery Packaging Shell market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

27.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

CATL, BYD, LG Energy Solution, Panasonic Holdings Corporation, Samsung SDI, Tesla, SVOLT Energy Technology, Envision AESC, Northvolt, EVE Energy |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |