Reports

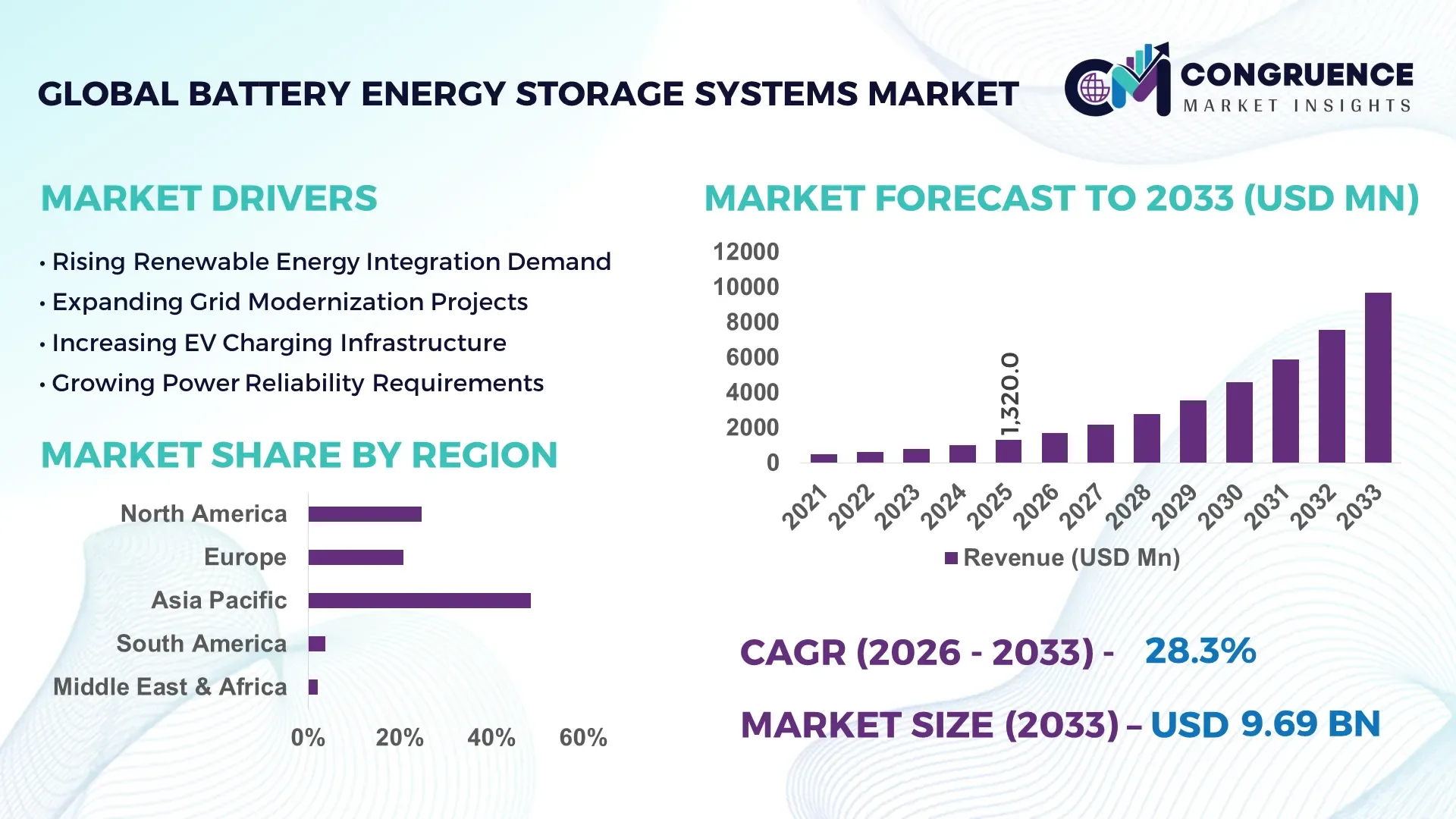

The Global Battery Energy Storage Systems Market was valued at USD 1,320.0 Million in 2025 and is anticipated to reach a value of USD 9,691.4 Million by 2033 expanding at a CAGR of 28.3% between 2026 and 2033. Growth is driven by accelerating grid-scale renewable integration, utility-led transmission upgrades, and large-scale deployment of lithium-ion storage for frequency regulation, peak shaving, and energy resilience.

China remains the dominant market, accounting for approximately 42% of global installed battery energy storage capacity, supported by multi-gigawatt renewable projects, strong domestic battery manufacturing, and national energy security initiatives. In comparison, the United States holds nearly 18% of installed capacity, driven by utility-scale deployments and Inflation Reduction Act incentives, while China's manufacturing scale enables faster project execution and lower system costs.

Strategic investment priorities increasingly favor localized supply chains, advanced battery technologies, and grid modernization to strengthen long-term market competitiveness.

Market Size & Growth: USD 1,320.0 Million (2025) to USD 9,691.4 Million (2033) at 28.3% CAGR, driven by advanced grid-scale renewable integration and utility storage expansion.

Top Growth Drivers: Renewable integration exceeds 35%, lithium-ion cost reductions surpass 80% over the past decade, and grid modernization investments continue above 20% annually.

Short-Term Forecast: By 2028, battery system costs decline nearly 25% while round-trip efficiency exceeds 92% across advanced installations.

Emerging Technologies: AI-powered energy management, solid-state battery development, and predictive asset analytics improve operational performance and asset utilization.

Regional Leaders: Asia-Pacific (~USD 4.4 Billion) leads manufacturing, North America (~USD 2.7 Billion) accelerates utility deployment, and Europe (~USD 1.8 Billion) expands grid-balancing projects.

Consumer/End-User Trends: More than 40% of new commercial renewable projects integrate battery storage to enhance energy reliability.

Pilot/Case Example: 2025 utility-scale hybrid renewable project improved renewable utilization by 30% through integrated battery storage.

Competitive Landscape: CATL holds roughly 35% battery manufacturing leadership alongside BYD, Tesla Energy, LG Energy Solution, and Sungrow amid global supply-chain expansion.

Regulatory & ESG Impact: Clean-energy incentives support over 50% of new utility-scale storage projects while reducing grid carbon intensity.

Investment & Funding: More than USD 35 Billion supports manufacturing expansion, strategic partnerships, and domestic battery supply-chain localization.

Innovation & Future Outlook: Long-duration storage, sodium-ion batteries, and AI-based grid optimization strengthen next-generation energy infrastructure and competitive differentiation.

Battery Energy Storage Systems have become essential across renewable power plants, commercial facilities, utility networks, and industrial microgrids where flexible energy management is increasingly prioritized. AI-enabled battery management systems, sodium-ion chemistry, and long-duration storage technologies are improving operational performance, while more than 45% of newly commissioned utility renewable projects now incorporate storage. Supply-chain diversification beyond East Asia is also reshaping procurement strategies and accelerating regional manufacturing investments, setting the stage for broader strategic market transformation.

Battery Energy Storage Systems have become a strategic infrastructure asset as utilities, industries, and governments modernize electricity networks for higher renewable penetration and greater grid resilience. Growing investments in transmission upgrades, domestic battery manufacturing, and supply-chain restructuring are strengthening energy security while reducing dependence on conventional peaking assets. Regulatory support for clean electricity and flexible grid operations is further accelerating commercial deployment across developed and emerging economies.

Modern lithium-ion systems deliver round-trip efficiencies exceeding 92%, compared with nearly 75–80% for several legacy storage alternatives, while digital battery management platforms significantly improve asset utilization and maintenance planning. China continues to lead large-scale manufacturing and deployment, whereas North America emphasizes grid reliability, long-duration storage, and utility modernization. Over the next two to three years, hybrid renewable-plus-storage installations are expected to account for a substantially larger share of newly commissioned utility-scale clean energy projects.

Utilities are increasingly deploying battery storage alongside solar and wind farms to stabilize grid frequency, reduce renewable curtailment, and improve peak-load management. Equipment manufacturers are expanding regional production, securing long-term mineral supply agreements, and forming technology partnerships to strengthen delivery capabilities. Companies that combine localized manufacturing, advanced energy management software, and scalable storage solutions will establish stronger competitive positioning while delivering operational efficiency, grid flexibility, and long-term infrastructure value.

Rapid expansion of renewable power generation is accelerating deployment of battery energy storage systems as utilities prioritize grid flexibility, frequency regulation, and peak-load optimization. More than 45% of newly commissioned utility-scale solar projects now integrate battery storage, while lithium-ion battery pack prices have declined by over 85% during the past decade, improving project economics. In China, mandatory storage requirements for new renewable projects are strengthening large-scale installations and encouraging domestic manufacturing expansion. This structural shift improves renewable utilization, reduces curtailment losses, and enhances grid reliability. In response, leading companies are expanding gigafactory capacity, securing long-term mineral supply agreements, and forming strategic partnerships with utilities to deliver integrated energy storage platforms. The competitive advantage increasingly depends on combining advanced battery chemistry with intelligent energy management software to maximize operational performance.

Battery production continues to face structural pressure from concentrated supplies of lithium, nickel, and graphite, creating procurement uncertainty and fluctuating manufacturing costs. More than 70% of global lithium processing capacity remains concentrated in China, while battery-grade graphite refining exceeds 80%, increasing supply-chain exposure for international manufacturers. Periodic raw-material price swings directly affect project economics, procurement planning, and contract profitability for utility-scale deployments. Lengthy permitting processes and inconsistent grid interconnection standards further delay commercial installations in several countries. To reduce operational risk, manufacturers are localizing production, diversifying sourcing through Australia and Canada, investing in battery recycling facilities, and accelerating development of sodium-ion and lithium iron phosphate technologies that reduce dependence on scarce critical minerals while improving long-term supply resilience.

The next phase of market expansion is being shaped by long-duration energy storage, AI-enabled battery optimization, and digital grid orchestration. Advanced battery management systems can improve asset utilization by nearly 20%, while predictive maintenance reduces unexpected downtime by approximately 30% across utility installations. India is rapidly expanding storage procurement through renewable energy auctions, creating opportunities for integrated storage developers and technology providers. Companies are investing in sodium-ion batteries, hybrid storage architectures, and virtual power plant platforms that aggregate distributed energy resources into flexible grid assets. A less obvious opportunity lies in commercial and industrial microgrids, where intelligent storage enables demand-response participation, lower electricity procurement costs, and improved energy resilience, creating recurring service-based business models beyond conventional equipment sales.

Successfully integrating battery storage into increasingly digital electricity networks requires sophisticated control systems, cybersecurity protection, and highly skilled operational expertise. Grid operators report that nearly 35% of advanced storage deployments require customized integration with legacy infrastructure, while battery management software can account for over 15% of total project engineering effort. In the United States, growing interconnection queues continue to delay grid-scale storage commissioning despite strong deployment pipelines. As storage fleets expand, maintaining interoperability across multiple hardware suppliers and software platforms becomes increasingly complex. Companies must strengthen digital infrastructure, invest in cybersecurity frameworks, standardize communication protocols, and collaborate with utilities and transmission operators to ensure reliable long-term asset performance, scalable deployment, and consistent grid stability.

AI-Driven Battery Optimization Battery operators are rapidly integrating AI-powered energy management platforms to improve dispatch accuracy, battery health monitoring, and predictive maintenance. Advanced analytics have reduced unplanned downtime by nearly 30% while increasing asset utilization by around 20% across utility-scale projects. Growing renewable penetration and grid-balancing requirements are accelerating digitalization, prompting companies to expand software partnerships and integrate cloud-based monitoring systems that shorten response times and optimize operating cycles.

LFP Chemistry Gains Momentum Lithium iron phosphate (LFP) batteries now account for more than 80% of newly commissioned stationary battery projects because of improved thermal stability and lower dependence on nickel and cobalt. Chinese manufacturers continue expanding global production capacity, while system integrators diversify procurement to reduce supply-chain exposure. Companies are redesigning product portfolios around standardized LFP platforms, lowering manufacturing complexity and improving installation speed for utility and commercial deployments.

Domestic Manufacturing Expansion Government-backed localization initiatives are reshaping battery supply chains as countries seek greater energy security. The United States has announced manufacturing projects capable of supporting more than 100 GWh of annual battery production, while India continues expanding domestic cell manufacturing under production-linked incentive programs. Equipment suppliers are increasing regional production, securing long-term raw-material contracts, and forming strategic joint ventures to improve delivery reliability and reduce import dependence.

Hybrid Renewable Storage Projects Utilities are increasingly combining solar, wind, and battery storage into integrated energy assets to improve grid flexibility and maximize renewable utilization. Hybrid projects have demonstrated renewable curtailment reductions exceeding 25% while improving system availability by approximately 15%. Developers are responding by scaling turnkey EPC capabilities, adopting modular battery architectures, and strengthening partnerships with grid operators to accelerate deployment schedules and simplify long-term asset management.

Lithium-ion Battery remains the leading segment, representing nearly 88% of newly installed battery energy storage capacity due to its high energy density, long cycle life, rapid response time, and declining manufacturing costs. The technology integrates efficiently with renewable energy projects and utility-scale grid infrastructure, making it the preferred solution for frequency regulation, peak shaving, and energy arbitrage. Manufacturers continue expanding LFP-based product portfolios because they provide improved thermal stability and lower lifecycle costs. Lead-acid Battery maintains relevance in backup power applications where lower upfront investment remains important, although its deployment continues to decline compared with advanced chemistries. Flow Battery is emerging as the fastest-growing segment as utilities increasingly seek storage durations exceeding six hours for long-duration energy storage projects. Sodium Sulfur (NaS) Battery also retains strategic importance in high-capacity industrial applications requiring extended discharge periods. Together, these technologies account for nearly 12% of new deployments but continue gaining attention through pilot programs and grid modernization initiatives. Companies are accelerating R&D investments, expanding manufacturing partnerships, and commercializing next-generation battery chemistries to diversify portfolios beyond conventional lithium-ion systems.

Renewable Energy Integration represents the largest application segment as utilities increasingly deploy battery storage alongside solar and wind generation to improve grid stability and reduce renewable curtailment. More than 90% of newly commissioned utility-scale battery projects are paired directly with renewable generation or designed to support renewable balancing functions. The segment benefits from rapid response capability, flexible dispatch, and improved grid reliability. Grid Services continue to account for a significant share of installations, particularly frequency regulation, voltage support, and ancillary service markets where batteries outperform conventional generation assets. UPS & Data Centers is the fastest-growing application as hyperscale data center expansion and AI infrastructure increase demand for uninterrupted power supply. Behind-the-Meter installations continue expanding across commercial and industrial facilities seeking energy cost optimization, while EV Charging Infrastructure and Microgrids & Off-grid Systems gain momentum through electrification and decentralized energy deployment. Companies are integrating advanced energy management software, modular storage platforms, and automated control systems to improve operational efficiency while expanding turnkey deployment capabilities.

Utilities constitute the dominant end-user segment, accounting for approximately 80% of newly deployed battery energy storage capacity as transmission operators and electricity providers strengthen grid resilience and integrate larger shares of renewable generation. Large-scale deployment, centralized asset management, and participation in ancillary service markets continue supporting utility investment. Independent Power Producers (IPPs) also maintain a significant presence by integrating storage with renewable portfolios to maximize electricity market participation and improve dispatch flexibility across competitive wholesale markets. Commercial & Industrial (C&I) is the fastest-growing end-user segment as manufacturers, logistics facilities, hospitals, and data centers prioritize energy resilience and peak-demand management. Residential adoption is increasing steadily through rooftop solar integration, while Government & Public Infrastructure projects expand battery deployment for critical infrastructure and emergency backup systems. Companies are introducing customized storage platforms, flexible financing models, and long-term service agreements while strengthening partnerships with EPC contractors and utilities to accelerate market penetration across diverse customer segments.

Asia-Pacific accounted for the largest market share at 48.6% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 29.6% between 2026 and 2033.

North America represented approximately 24.8% of the global Battery Energy Storage Systems market in 2025, supported by accelerating renewable integration, transmission modernization, and increasing investments in domestic battery manufacturing. Utility-scale projects account for nearly 82% of regional deployments, reflecting strong demand for frequency regulation, peak-load management, and grid resilience. The United States and Canada continue expanding battery manufacturing capacity through strategic public-private investments, while digital energy management platforms are improving dispatch efficiency and asset utilization. Utilities are increasingly deploying four-hour storage systems alongside solar and wind farms, strengthening grid flexibility and reducing dependence on conventional peaking generation.

United States Market Outlook: The United States remains the regional leader due to large-scale utility procurement, strong project financing, and extensive renewable deployment. California and Texas account for a significant share of installed storage capacity, while domestic manufacturing investments now exceed 100 GWh of planned annual battery cell production. Companies continue expanding vertically integrated supply chains, strengthening lithium processing capabilities, and deploying AI-enabled battery management systems to improve operational performance and project economics.

Europe accounted for nearly 20.7% of the global market in 2025, supported by ambitious decarbonization policies, electricity market reforms, and rapid renewable capacity additions. More than 65% of newly installed battery systems are integrated with renewable generation or flexibility services, helping stabilize increasingly decentralized electricity networks. Battery deployments are expanding across utility-scale and commercial applications as grid operators seek greater energy security and balancing capacity. Companies are investing in localized battery manufacturing, advanced recycling infrastructure, and strategic technology partnerships to reduce supply-chain dependence while improving long-term sustainability.

Germany Market Outlook: Germany leads the European market through its advanced renewable energy ecosystem, battery manufacturing investments, and industrial electrification strategy. Commercial battery installations continue expanding alongside rooftop solar adoption, while utility operators increasingly deploy large-scale storage to stabilize the national grid. Domestic manufacturers are strengthening European battery value chains through localized production, recycling initiatives, and partnerships supporting next-generation energy storage technologies.

Asia-Pacific dominated the global Battery Energy Storage Systems market with approximately 48.6% share in 2025, supported by unmatched battery manufacturing capacity, expanding renewable installations, and large-scale utility deployment. The region produces over 75% of global lithium-ion battery cells, creating significant cost advantages and supply-chain efficiency. China, Japan, South Korea, and India continue investing in integrated battery manufacturing ecosystems, while utilities accelerate deployment of grid-scale storage to improve renewable utilization. Companies are expanding gigafactories, increasing automation, and securing long-term raw material supply agreements to strengthen competitive positioning.

China Market Outlook: China remains the world's largest Battery Energy Storage Systems market through its integrated manufacturing ecosystem, large domestic demand, and supportive energy transition policies. The country accounts for more than 70% of global lithium-ion battery manufacturing capacity and continues commissioning multi-gigawatt storage projects supporting renewable energy integration. Leading manufacturers are expanding overseas production, advancing sodium-ion battery commercialization, and investing heavily in intelligent battery management technologies to maintain global leadership.

South America accounted for approximately 3.8% of the global market in 2025 as renewable energy expansion increased demand for flexible electricity infrastructure. Utility developers are integrating battery storage with solar and wind projects to improve grid stability, particularly in regions with transmission constraints. More than 40% of recently announced utility renewable projects include battery storage components, reflecting growing emphasis on dispatchable clean energy. Companies are strengthening partnerships with power producers while introducing modular storage platforms suited to remote and distributed electricity networks.

Brazil Market Outlook: Brazil leads the regional market through its large electricity network, rapidly expanding renewable generation, and supportive regulatory developments. Utility companies continue evaluating battery storage for grid balancing, transmission support, and renewable integration, while commercial users increasingly adopt storage for power reliability. Energy developers are partnering with technology providers to accelerate hybrid renewable projects and improve electricity system flexibility across major industrial centers.

The Middle East & Africa represented approximately 2.1% of the global market in 2025, supported by utility modernization, renewable diversification strategies, and infrastructure investment programs. Battery storage is increasingly deployed alongside large-scale solar developments to improve grid stability and reduce dependence on conventional generation. Several national energy transition programs are accelerating utility procurement, while industrial users adopt battery systems to improve operational reliability. Companies are expanding regional partnerships, establishing service capabilities, and deploying containerized storage solutions designed for harsh operating environments.

Saudi Arabia Market Outlook: Saudi Arabia is the leading market in the region due to its large renewable energy pipeline, grid modernization initiatives, and strategic investments under national energy diversification programs. Utility-scale battery storage is becoming a core component of integrated solar projects, while international technology providers continue forming joint ventures with local enterprises. Ongoing investments in smart grid infrastructure and advanced energy management systems are strengthening long-term deployment potential and supporting the country's transition toward a more flexible electricity network.

The Battery Energy Storage Systems market is led by CATL, BYD, Tesla Energy, Fluence Energy, and Sungrow, collectively controlling approximately 58% of global utility-scale deployments. Chinese manufacturers compete primarily on manufacturing scale and cost efficiency, while Tesla Energy and Fluence compete through software integration, digital optimization, and project execution. Regional integrators challenge global leaders by offering customized solutions and faster local deployment. Competition centers on battery cost, system efficiency, supply-chain control, and lifecycle performance, with battery management software improving operational efficiency by nearly 20% and LFP batteries reducing lifecycle costs by approximately 25% compared with conventional chemistries. Companies continue expanding gigafactories, securing long-term lithium supply agreements, pursuing vertical integration, and forming utility partnerships to strengthen project pipelines. Market competition is shifting toward integrated energy platforms combining hardware, software, and lifecycle services rather than standalone battery supply. High capital requirements, mineral sourcing security, and certification standards remain critical entry barriers. Sustainable leadership depends on scalable manufacturing, digital intelligence, resilient supply chains, and reliable project execution.

BYD

Tesla Energy

Fluence Energy

Sungrow Power Supply Co., Ltd.

LG Energy Solution

Samsung SDI

Panasonic Energy

ABB Ltd.

Siemens AG

Wärtsilä

Hitachi Energy

Eaton Corporation

GE Vernova

Lithium iron phosphate (LFP) technology remains the dominant battery chemistry, accounting for more than 80% of newly commissioned stationary storage projects because of superior thermal stability, longer cycle life, and lower material costs. AI-enabled battery management systems are improving asset utilization by nearly 20% while predictive maintenance reduces unexpected downtime by approximately 30%. Cloud-connected energy management platforms are increasingly integrated with utility control systems, enabling automated dispatch, real-time monitoring, and faster response to grid fluctuations. Companies combining battery hardware with advanced software platforms are achieving stronger operational differentiation and higher customer retention.

Emerging technologies include sodium-ion batteries, long-duration flow batteries, silicon carbide power electronics, and digital twin-based asset optimization. Compared with conventional lithium-ion systems, advanced power electronics improve conversion efficiency by nearly 3–5%, while next-generation battery management algorithms extend usable battery life by approximately 15%. Utilities, independent power producers, and hyperscale data center operators are accelerating adoption to improve grid flexibility and reduce lifecycle operating costs. Manufacturers are increasing investment in modular system architectures that simplify maintenance and accelerate deployment.

Between 2026 and 2028, intelligent hybrid energy storage platforms integrating AI, distributed energy resources, and advanced battery chemistries will become a primary competitive differentiator. Companies investing early in software-defined energy storage, long-duration technologies, and localized manufacturing will strengthen supply resilience, shorten project delivery timelines, and secure strategic advantages as utilities increasingly prioritize integrated, digitally optimized energy storage ecosystems over standalone battery installations.

February 2025 – BYD signed an agreement with the Saudi Electricity Company to deploy 12.5 GWh of grid-scale battery energy storage, one of the world's largest announced BESS contracts. The project significantly strengthens BYD's global utility-scale portfolio while accelerating renewable grid integration across the Middle East. Source: www.polinovelbess.com

July 2025 – LG Energy Solution secured a USD 4.3 billion multi-year agreement to supply LFP batteries for Tesla's energy storage systems, with production scheduled from its U.S. manufacturing facilities. The agreement expands localized battery supply, reduces dependence on Chinese imports, and strengthens North American energy storage manufacturing.

December 2025 – CATL expanded its leadership in stationary energy storage after securing a 200 GWh multi-year battery cell supply agreement with HyperStrong, later extended to include 60 GWh of sodium-ion BESS cells. The deal reinforces CATL's leadership in advanced battery chemistry and large-scale utility deployments.

September 2025 – SK On entered its first dedicated stationary storage agreement by signing a contract with Flatiron Energy to supply up to 7.2 GWh of LFP batteries between 2026 and 2030. The partnership diversifies SK On beyond electric vehicles and expands its presence in the rapidly growing utility-scale energy storage market.

This report provides a comprehensive assessment of the global Battery Energy Storage Systems market between 2026 and 2033, covering key technology, deployment, and competitive developments across the value chain. It analyzes major battery types including lithium-ion, lead-acid, sodium sulfur, flow batteries, and other emerging chemistries, along with applications such as renewable energy integration, grid services, behind-the-meter systems, UPS & data centers, EV charging infrastructure, and microgrids. The study further evaluates demand across utilities, commercial & industrial, residential, independent power producers, and public infrastructure, with regional analysis spanning North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The report examines technology adoption patterns, where lithium-ion systems account for over 85% of new installations, while long-duration storage solutions continue expanding across utility projects. It delivers strategic insights into manufacturing capacity expansion, supply-chain localization, digital energy management, and battery innovation, supported by competitive benchmarking of leading industry participants. The analysis enables stakeholders to identify high-potential investment opportunities, optimize expansion strategies, evaluate competitive positioning, and anticipate evolving deployment priorities and technology transitions shaping the Battery Energy Storage Systems market throughout the forecast period.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,320.0 Million |

| Market Revenue (2033) | USD 9,691.4 Million |

| CAGR (2026–2033) | 28.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | CATL; BYD; Tesla Energy; Fluence Energy; Sungrow Power Supply Co., Ltd.; LG Energy Solution; Samsung SDI; Panasonic Energy; ABB Ltd.; Siemens AG; Wärtsilä; Hitachi Energy; Eaton Corporation; GE Vernova |

| Customization & Pricing | Available on Request (10% Customization Free) |