Reports

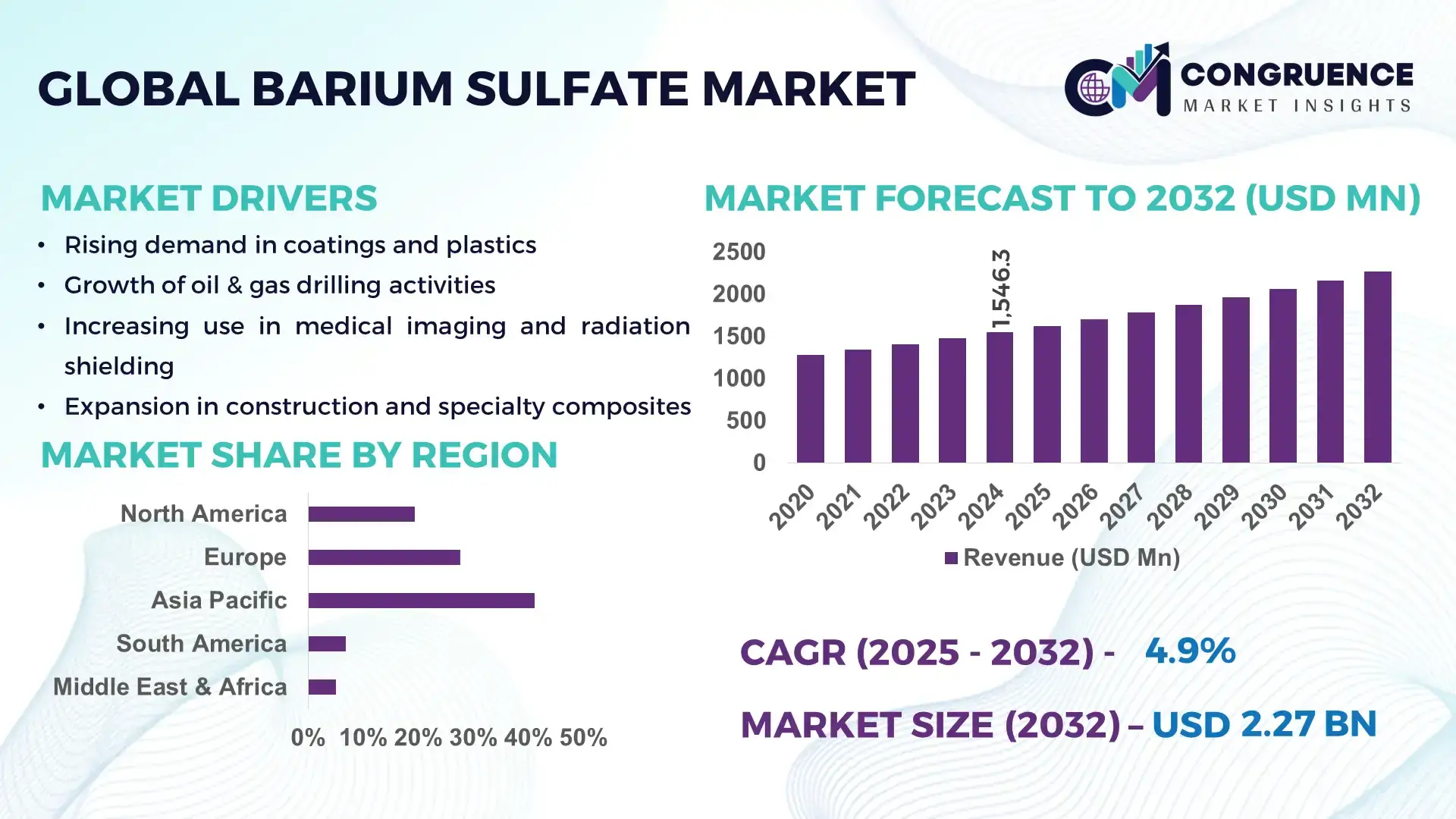

The Global Barium Sulfate Market was valued at USD 1,546.3 Million in 2024 and is anticipated to reach a value of USD 2,267.2 Million by 2032 expanding at a CAGR of 4.9% between 2025 and 2032, according to an analysis by Congruence Market Insights. This expansion is supported by rising demand from coatings, plastics, and advanced material applications.

The dominant country in the Barium Sulfate Market, China, continues to strengthen its position through significant production capacity exceeding 2.8 million metric tons annually, backed by robust investments in high-purity and precipitated grades. The country benefits from the presence of more than 120 large-scale processing facilities, widespread integration with coatings and polymer industries, and rapid technological upgrades such as automated beneficiation and particle-size optimization. China’s end-use sectors, including automotive coatings and engineered plastics, collectively consume over 40 million tons of fillers and additives each year, reinforcing its strong influence over global supply conditions.

Market Size & Growth: Valued at USD 1.54 billion in 2024, projected to reach USD 2.26 billion by 2032 at a 4.9% CAGR, driven by rising demand in high-performance coatings.

Top Growth Drivers: 27% increase in demand from automotive coatings, 18% improvement in filler efficiency in polymers, 22% rise in medical imaging-grade consumption.

Short-Term Forecast: By 2028, formulation efficiency in coatings is expected to improve by 15% due to enhanced particle dispersion technologies.

Emerging Technologies: Advancements include nano-structured barium sulfate and automated precision milling systems improving material uniformity.

Regional Leaders: Asia-Pacific projected to reach USD 1.12 billion by 2032, Europe USD 540 million, North America USD 390 million, each showing rising adoption in specialized applications.

Consumer/End-User Trends: Strong adoption from automotive, construction, and medical imaging sectors driven by performance and durability requirements.

Pilot or Case Example: In 2027, a European coatings manufacturer achieved 21% opacity improvement using a next-generation precipitated grade.

Competitive Landscape: The market leader holds approximately 12% share, followed by prominent competitors including Solvay, Sakai Chemical, ChemChina, and Cimbar.

Regulatory & ESG Impact: Increasing environmental standards are encouraging producers to adopt cleaner beneficiation processes and higher recycling rates.

Investment & Funding Patterns: Over USD 320 million invested recently in upgrading processing plants and nanomaterial-focused production lines.

Innovation & Future Outlook: Innovations in ultrafine particle engineering and high-density filler formulations are reshaping future demand patterns.

The Barium Sulfate Market is increasingly shaped by advanced coatings, engineered polymer applications, and innovations in ultrafine formulations. Regulatory pressure on material purity, coupled with rising environmental standards, is encouraging cleaner processing technologies. Emerging regions show rapid consumption growth linked to industrial expansion and adoption of high-efficiency material systems.

The Barium Sulfate Market holds strong strategic significance due to its role in high-performance coatings, engineered plastics, radiation shielding materials, and advanced medical imaging systems. Increasing precision requirements in end-use industries are accelerating demand for ultra-pure, micronized, and nano-grade barium sulfate. Industries are gradually shifting from conventional filler materials to high-density, high-opacity solutions, reinforcing the long-term relevance of barium sulfate. New technologies such as nano-structured BaSO₄ deliver up to 28% improvement in dispersion quality compared to older milling standards, enabling manufacturers to enhance durability and opacity with lower formulation volumes.

Regional strengths further underscore market potential. Asia-Pacific dominates in volume, while Europe leads in adoption with 61% of enterprises using advanced precipitated grades in specialty coatings. Over the next two to three years, by 2027, automated mineral-processing systems are expected to reduce production waste by nearly 18%, significantly improving cost efficiency across value chains. This shift supports broader industrial modernization efforts and growing investments in premium coating solutions.

Compliance and ESG initiatives are adding momentum as firms commit to cleaner production methodologies, targeting up to 20% reduction in process-related emissions by 2030. A notable example occurred in 2026, when a Japanese materials producer achieved a 16% energy-reduction rate through AI-driven beneficiation optimization. These advancements demonstrate the industry's movement toward sustainable, precision-oriented production models.

Looking ahead, the Barium Sulfate Market is positioned as a cornerstone for industries requiring high purity, performance stability, and environmental compliance. Its evolving technology pathways and ESG-aligned growth strategies are expected to support long-term resilience and sustained global expansion.

The Barium Sulfate Market is influenced by growing demand from coatings, plastics, construction, and medical sectors, each requiring high-performance filler materials. Increasing industrial production, infrastructure development, and advancements in polymer engineering are reshaping consumption patterns. Technological innovations in particle size control, refining processes, and nano-grade development are improving product performance and expanding applications. Rising regulatory focus on material safety and purity is also prompting manufacturers to invest in environmentally compliant production systems. Additionally, the shift toward lightweight and high-strength materials in automotive and manufacturing industries continues to generate consistent demand for finely processed barium sulfate.

Advanced coatings used in automotive, industrial, and architectural applications require materials with high opacity, brightness, and chemical stability, increasing demand for barium sulfate as a reliable performance additive. The adoption of high-solid and low-VOC formulations has pushed manufacturers to prefer micronized and precipitated grades that offer superior dispersion and durability. The automotive sector alone accounts for millions of units produced annually, each requiring multilayer coating systems enhanced through high-density fillers. With engineered polymers and construction coatings witnessing double-digit consumption growth in several emerging economies, barium sulfate is becoming more integral to performance enhancement and protective functionalities across multiple industries.

Environmental regulations on mining, beneficiation, and waste disposal introduce operational constraints for producers. Extracting barite ores requires compliance with increasingly stringent guidelines on land restoration, water use, and particulate emissions. Production facilities must invest heavily in dust-control systems, waste recycling units, and purification technologies to meet updated standards, increasing operating costs. Additionally, global scrutiny of mineral-based additives has pushed industries to adopt cleaner and more traceable supply chains, causing delays and higher certification expenses. These challenges create bottlenecks in expansion plans and limit the speed at which new processing capacities can be added.

Innovations in particle engineering, including nano-scale milling, uniform size distribution technologies, and advanced precipitation techniques, are unlocking new opportunities. These advancements enhance opacity, improve dispersion, and expand compatibility with next-generation polymer matrices. The medical sector is increasingly adopting specialized barium sulfate for diagnostic imaging procedures, benefiting from enhanced contrast and purity levels. The coatings industry is utilizing ultra-fine grades to deliver improved surface finish, durability, and UV resistance. The growing focus on lightweight composite materials also presents substantial opportunities, as barium sulfate enables performance improvements without significant cost inflation or material redesign.

Production costs continue to rise due to raw material price fluctuations, energy-intensive processing, and strict regulatory obligations. The need for precision milling and high-purity formulation increases dependency on advanced machinery and skilled labor. Logistics present additional challenges, as barium sulfate’s high density elevates transportation costs, especially over long international routes. Port handling limitations and regional variations in import practices further slow down supply chains. For industries relying on just-in-time manufacturing, these logistical complexities increase lead times and hinder consistent availability, affecting downstream production schedules.

Shift Toward Ultrafine and Nanoparticle Grades: Ultrafine and nano-structured barium sulfate grades are gaining traction due to measurable performance benefits, including up to 22% improvement in opacity and 15% enhancement in UV resistance. Manufacturers are integrating advanced grinding systems capable of producing particles below 300 nanometers, supporting their adoption in premium coatings and engineered polymers. The market is observing rapid scaling of nano-grade production lines to meet rising demand from automotive and electronics sectors.

Rising Adoption in High-Density Polymer Applications: Barium sulfate is increasingly utilized in high-density polymer systems, where consumption has grown by nearly 19% in the past five years. Its use in thermoplastics and elastomers enhances stiffness, heat resistance, and dimensional stability. Asia-Pacific has seen accelerated integration, with manufacturers reporting over 25% higher utilization of functional fillers in engineered plastics. These applications support advancements in medical devices, automotive interiors, and precision components.

Technological Advancements in Beneficiation and Purification: Producers are deploying automated beneficiation systems and AI-enabled purification technologies that reduce impurities by up to 30%, improving material brightness and consistency. These measures significantly enhance product performance across coatings, plastics, and medical imaging applications. Facilities adopting real-time monitoring technologies have reported operational efficiency gains exceeding 14%, contributing to sustained capacity expansion.

Growing Use in Radiation Shielding Materials: Demand is increasing in radiation shielding applications, particularly in medical and industrial environments. Barium sulfate–based shielding materials have demonstrated 12% better attenuation performance compared to older composites. With global imaging and diagnostic procedures rising at an annual rate above 8%, specialized high-density formulations are becoming more widely used. Construction of diagnostic centers and industrial safety upgrades are further driving demand for enhanced shielding materials.

The Barium Sulfate Market is segmented across type, application, and end-user categories, each reflecting distinct consumption behaviors and performance requirements across industries. Types include precipitated, natural, and modified grades, each selected based on purity, brightness, and functional properties. Applications span coatings, plastics, rubber, medical imaging, and construction materials, driven by rising demand for high-density fillers and improved material durability. End-users range from automotive and construction to healthcare and chemical manufacturing, each adopting specialized grades tailored to performance standards. Industrial users increasingly favor ultra-fine and surface-treated grades, reflecting a broader shift toward high-performance materials supported by evolving regulatory and product quality norms.

Precipitated barium sulfate remains the leading type, accounting for approximately 46% of the market due to its superior particle uniformity, brightness, and compatibility with high-performance coatings and engineered polymers. Natural barium sulfate follows with nearly 32% share, primarily driven by its widespread availability and cost-effectiveness. However, modified grades, including surface-treated and nano-structured variants, represent the fastest-growing type segment, expanding at an estimated CAGR of 6.8% due to rising demand in specialty plastics and advanced material formulations. While the remaining niche categories—including high-purity medical grades and composite-specific formulations—collectively represent around 22% of total consumption, they play a vital role in radiation shielding, imaging, and precision engineering applications.

Coatings represent the dominant application segment, accounting for nearly 41% share supported by rising demand for enhanced opacity, weather resistance, and gloss retention across automotive and architectural sectors. Plastics hold 29% share, while rubber applications represent 17%; however, medical imaging is the fastest-growing application with an estimated CAGR of 7.2% as radiology centers increasingly adopt high-purity grades. Demand in engineered polymers is growing rapidly, expected to exceed 30% adoption by 2032 as industries shift toward lightweight, high-durability components. Consumer adoption trends show that in 2024 more than 38% of manufacturing enterprises reported integrating high-density fillers—including barium sulfate—into performance plastics for improved dimensional stability. In the US, 42% of hospitals reported testing advanced imaging materials built with enhanced contrast media formulations, supporting wider diagnostic use cases. Other applications such as construction materials and sealants collectively hold around 13% share, driven by infrastructure modernization and improved fire-resistant material standards.

Automotive and industrial manufacturing remain the leading end-user segment with approximately 39% share, driven by large-scale use of high-density fillers in coatings, plastics, and vibration-damping components. Construction companies and infrastructure developers hold 28% share, supported by rapid adoption of modified barium sulfate in flooring, sealants, and composite reinforcement applications. Healthcare represents the fastest-growing end-user segment with an estimated CAGR of 7.5%, propelled by rising imaging volumes and growing adoption of specialized contrast media formulations. Meanwhile, other end-users—including electronics, marine, and general engineering—contribute a combined 33% share, each leveraging niche performance properties for specific functional requirements. Industry adoption statistics indicate that in 2024 more than 35% of chemical processing firms globally integrated surface-treated filler materials to improve formulation stability. Additionally, over 60% of new automotive OEMs in Asia reported increased use of advanced filler composites to support lightweighting initiatives.

Asia-Pacific accounted for the largest market share at 41.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.4% between 2025 and 2032.

The global Barium Sulfate market shows strong regional disparities driven by production concentration, demand intensity, and end-use industry clusters. Europe followed with 27.6% market share, supported by its advanced coatings and plastics sectors. North America captured 19.4%, driven by high consumption in the medical imaging and oil & gas sectors, while South America and the Middle East & Africa collectively held 11.8%, primarily due to rising industrialization. Variation in regulatory environments, consumer behavior, and manufacturing capacity further shapes regional competitiveness and long-term growth dynamics.

The North America Barium Sulfate Market accounted for 19.4% share in 2024, driven by strong utilization in diagnostic imaging, paints & coatings, and high-performance polymers. The U.S. continues to dominate regional consumption due to its significant medical imaging volume exceeding 45 million radiology procedures annually. The region benefits from regulatory support encouraging quality-compliant radiopaque agents and advanced coating materials. Technological adoption in drilling technologies and enhanced oil recovery also contributes to uptake. Local players such as Cimbar Performance Minerals continue to expand high-purity, micronized barium sulfate product lines tailored for plastics and automotive coatings. Consumer behavior is marked by higher enterprise adoption in healthcare and precision manufacturing, with industries preferring ultra-high-purity functional additives.

Europe held 27.6% of the global Barium Sulfate market in 2024, with Germany, the UK, and France representing more than 68% of regional demand. Demand is primarily driven by the automotive coatings, plastic compounding, and pharmaceutical sectors. Regulatory bodies such as the European Chemicals Agency (ECHA) mandate strict purity compliance, boosting the adoption of premium grades. Europe is also at the forefront of sustainability initiatives, accelerating demand for eco-compliant fillers and non-toxic radiopaque additives. Countries like Germany continue to modernize coatings technology, integrating advanced dispersion and nano-milling processes. Local producers such as Solvay invest in performance additives engineered for high reflectivity and chemical inertness. Consumer behavior reflects strong preference for regulatory-aligned and environmentally responsible specialty materials, shaping long-term regional demand.

Asia-Pacific dominated the global landscape with 41.2% market share in 2024, ranking as the highest-volume consumer of Barium Sulfate worldwide. China, India, and Japan account for nearly 72% of regional consumption due to robust manufacturing ecosystems, infrastructure expansion, and high coatings demand. China’s thriving plastic compounding and automotive coating sectors further elevate consumption, supported by an annual output of over 4 million metric tons of engineered plastics. The region is also witnessing strong adoption of digital manufacturing technologies and innovation hubs specializing in nano-sizing of functional fillers. Key players like Sakai Chemical Industry Co., Ltd. in Japan continue to upgrade radiopaque and industrial-grade barium sulfate solutions. Consumer behavior is shaped by high-volume industrial usage, rapid e-commerce expansion, and preference for cost-efficient materials across major end-use sectors.

South America accounted for approximately 6.8% of global market share in 2024, with Brazil and Argentina leading consumption. Growth is supported by the region’s strengthened oil & gas activities, construction sector expansion, and rising adoption of specialty coatings for industrial infrastructure. Government trade incentives and material import flexibility have enabled increased availability of high-performance mineral fillers. Brazil’s drilling sector alone contributes to over 58% of regional Barium Sulfate usage, given its role as a weighting agent. Local participants such as Quimbar continue supplying grades suitable for coatings and polymer industries. Consumer behavior shows rising inclination toward language-localized product documentation and application training, supporting broader enterprise adoption across industrial sectors.

The Middle East & Africa region captured around 5.0% of global demand in 2024, primarily driven by oil & gas drilling, construction chemicals, and advanced coating applications. Countries such as the UAE, Saudi Arabia, and South Africa accounted for more than 64% of regional consumption. The region is undergoing rapid modernization in industrial processes, including adoption of automated drilling systems and upgraded coating technologies. Government-backed infrastructure programs worth over USD 120 billion across GCC nations continue to elevate the need for high-density fillers. Local suppliers like Blanc Fixe Mining LLC have been expanding distribution channels for industrial-grade barium sulfate. Consumer behavior shows preference for durability-focused materials, particularly in infrastructure, oilfield services, and industrial coating applications.

China – 31.5% Market Share: Leads due to its massive production capacity, strong plastics and coatings industries, and dominance in global mineral processing.

Germany – 11.4% Market Share: Leadership stems from high demand in automotive coatings and engineered plastics, supported by advanced manufacturing standards.

The global Barium Sulfate market is characterized by a moderately consolidated to fragmented competitive environment, where a handful of major producers co‑exist with many regional and specialized suppliers. There are roughly 20–25 active large and mid‑sized competitors globally producing commercial grades of barium sulfate, ranging from natural barite to ultra-fine precipitated and specialty grades. The top 5 companies collectively control around 45–50% of global production capacity, leaving the remainder distributed among regional and smaller players.

Major players maintain strong positioning through diversified product portfolios, global distribution networks, and strategic initiatives such as capacity expansion, joint ventures, and R&D investments. For instance, in 2024 one leading producer expanded precipitated barium sulfate capacity by 15,000 tonnes per year to support growing demand from automotive coatings and aerospace clients.

Competition increasingly centers on value-added specialty grades — including ultra-fine, surface-modified, and low-dust formulations — rather than commodity-grade barite. Several companies have launched hydrophobic or nano-structured barium sulfate products tailored for high-performance coatings, plastics, or medical applications.

Regional suppliers, especially in Asia, remain competitive through cost-effective production, localized supply chains, and region-targeted product lines. At the same time, global corporations leverage economies of scale, regulatory compliance, and service support to maintain share in high-value segments. The interplay between global leaders and regional specialists defines a dynamic, competitive landscape where innovation, product differentiation, and geographic reach drive market positioning.

Sachtleben Chemie GmbH

Shanxi Fuhua Chem

Sakai Chemical Industry Co., Ltd.

Long Fu Group

Onmillion Nano Material

The Barium Sulfate market is undergoing a technological transformation driven by evolving application requirements and regulatory pressures. A key trend is the proliferation of ultra-fine and nano-structured precipitated barium sulfate grades. These advanced formulations deliver improved dispersion, higher opacity, better surface finish, and greater compatibility with high-performance polymer matrices and specialty coatings. Some manufacturers now produce particles below 300 nanometers, enabling superior brightness and uniformity in coatings and plastics.

Simultaneously, surface-modified and functionalized barium sulfate variants — such as hydrophobic grades for water-based paints or low-dust formulations for rubber compounding — are gaining traction. These technologies address practical manufacturing and environmental challenges, reducing dust-related handling issues, improving mixing consistency, and enabling safer and cleaner production processes.

Production technology is also evolving: newer plants employ closed-loop processes, automated milling, real-time quality control, and energy-efficient precipitation methods. This enhances yield, reduces waste, and improves material purity. Development of low-emission beneficiation and purification systems is helping firms meet tighter environmental compliance and ESG standards, a growing priority for industrial buyers.

On the innovation frontier, some companies are exploring composite fillers combining barium sulfate with other minerals or polymers to impart multifunctional properties — for example, improved density, shielding, and thermal or acoustic performance — for niche applications in medical imaging, radiation shielding, and advanced engineering plastics. Such technology-driven differentiation is shaping competitive advantage and future market evolution, making the Barium Sulfate market increasingly value-driven rather than purely volume-based.

In September 2024, a major European producer expanded its precipitated barium sulfate production capacity by 15,000 tonnes annually to meet rising demand from automotive coatings and aerospace paint customers.

In mid‑2024, a leading U.S.-based mineral supplier completed a 15% increase in its production capacity of ultra-fine barium sulfate, targeting growth in plastics compounding and high-performance masterbatch applications.

In 2023, an Asian specialty chemicals manufacturer introduced a new hydrophobic barium sulfate grade optimized for water-based paints, improving dispersion stability and lowering oil absorption compared to standard grades.

In 2024, a Japanese chemicals firm launched a low-dust formulation of barium sulfate tailored for rubber compounding — reducing dust emissions during processing by approximately 30%, enhancing worker safety and lowering contamination risks.

This Barium Sulfate Market Report covers a comprehensive scope including multiple product types (natural barite, precipitated barium sulfate, modified/surface treated grades, nano-structured variants, low-dust formulations), and a wide range of applications — coatings, plastics, rubber, oil & gas drilling fluids, medical imaging, radiation shielding, construction materials, and specialty composites. Geographic analysis spans all major regions: North America, Europe, Asia-Pacific, Middle East & Africa, South America, and their sub-regions, capturing both upstream supply sources and downstream consumption markets.

The report examines end-user segments such as automotive, construction, medical, industrial manufacturing, oil & gas, and chemical processing — providing insight into demand drivers, consumption patterns, and regional adoption behaviors. It analyzes technology trends including advanced precipitation, nano-sizing, surface modification, closed-loop processing, and composite filler innovations, highlighting how such developments influence product performance, regulatory compliance, and market differentiation.

Additionally, the report addresses market dynamics such as competitive structure, capacity expansions, product launches, and innovation strategies among global and regional players. It also considers regulatory and ESG factors shaping production methods and market acceptance. Niche segments — such as radiation shielding materials, water‑based coatings, and specialty rubbers — are included to reflect emerging demand trends.

Together, the scope presents a holistic view of the Barium Sulfate market’s structure, dynamics, regional variations, product segmentation, technological evolution, and industry-specific end-use applications, offering decision-makers a robust basis for strategic planning, investment assessment, and competitive benchmarking.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,546.3 Million |

| Market Revenue (2032) | USD 2,267.2 Million |

| CAGR (2025–2032) | 4.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory & ESG Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Solvay S.A., Cimbar Performance Minerals, Shenzhou Jiaxin Chemical, Sachtleben Chemie GmbH, Shanxi Fuhua Chem, Sakai Chemical Industry Co., Ltd., Long Fu Group, Onmillion Nano Material |

| Customization & Pricing | Available on Request (10% Customization Free) |