Reports

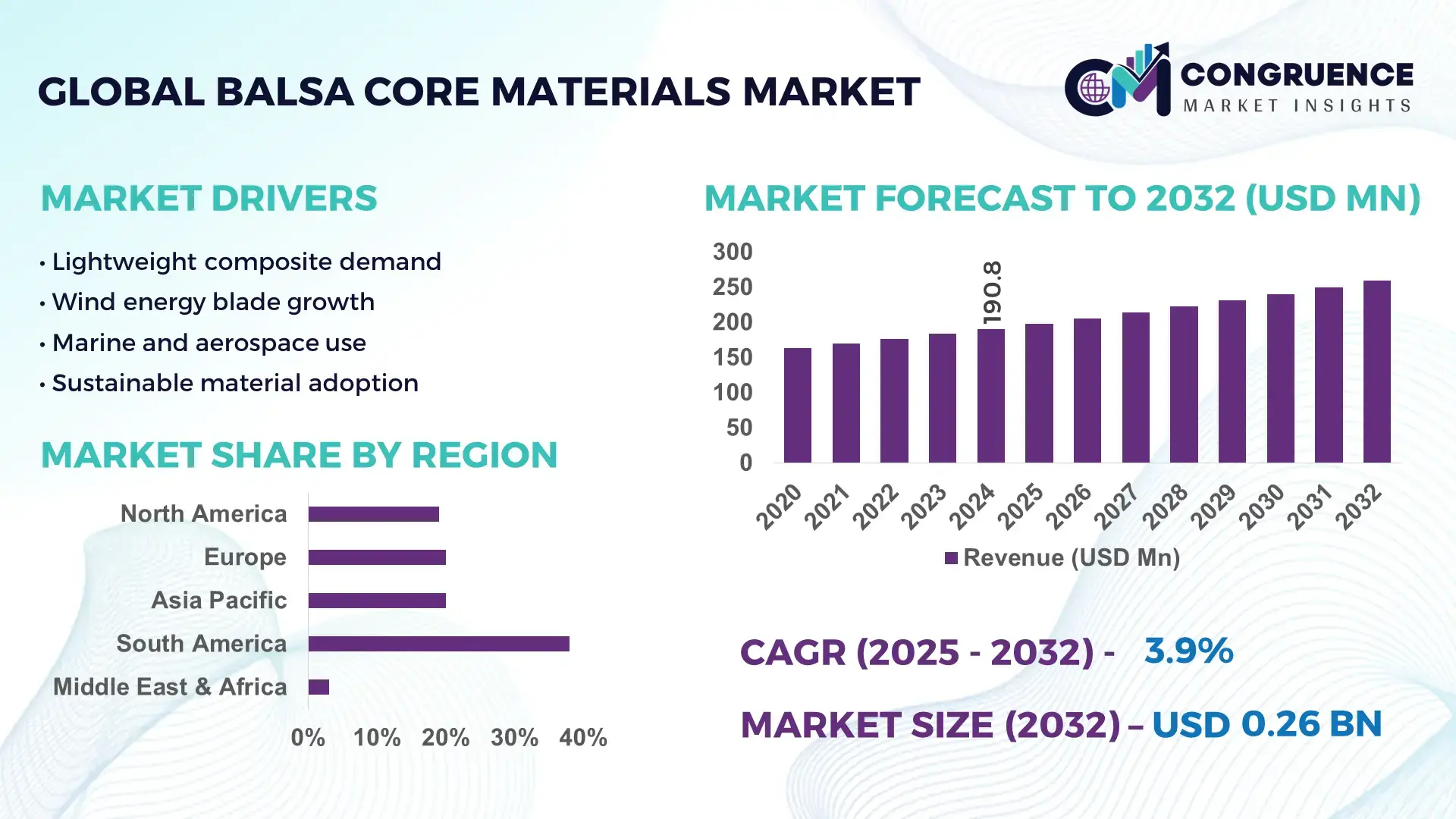

The Global Balsa Core Materials Market was valued at USD 190.76 Million in 2024 and is anticipated to reach a value of USD 259.06 Million by 2032 expanding at a CAGR of 3.9% between 2025 and 2032. Driven by increased demand in lightweight structural applications across aerospace and wind energy.

Ecuador leads the marketplace with over 70% of global production capacity, boasting an annual output exceeding 450,000 cubic meters of balsa cores and attracting USD 120 million in recent investments toward sustainable plantation and processing technologies. The country’s industry supports advanced composite fabrication for marine, automotive, and renewable sectors, with dedicated R&D facilities advancing impregnation and cellular optimization techniques that yield higher strength-to-weight performance and reduce production variances in large-scale manufacturing.

• Market Size & Growth: USD 190.76 Million current value, projected to USD 259.06 Million by 2032 at a 3.9% CAGR, influenced by expanding demand in aerospace and wind energy composites.

• Top Growth Drivers: Rise in aerospace structural usage (22%), wind turbine blade production (18%), and electric vehicle lightweighting adoption (15%).

• Short-Term Forecast: By 2028, industry-wide cost per kg reduction of 8% and performance gain of 12% in tensile strength.

• Emerging Technologies: Nano‑enhanced impregnation resins, automated core grading AI, and bio‑based resin compatibility developments.

• Regional Leaders: South America USD 160M by 2032 with plantation expansion, Europe USD 50M driven by renewables, and North America USD 45M supported by aerospace composites.

• Consumer/End‑User Trends: Marine composites and luxury sports equipment sectors increasing high‑grade balsa uptake with longer service life expectations.

• Pilot or Case Example: 2025 pilot in wind blade cores achieved 9% downtime reduction and 7% weight savings.

• Competitive Landscape: Market led by major supplier with ~35% share, followed by three key competitors focusing on quality and supply reliability.

• Regulatory & ESG Impact: Stricter forestry sustainability standards and tax incentives for eco‑friendly core materials accelerating certified supply adoption.

• Investment & Funding Patterns: Over USD 85M recent investments in sustainable plantations, processing automation, and joint venture facilities.

• Innovation & Future Outlook: Integration of digital core tracking, hybrid core laminates, and forward projects targeting ultra‑light marine composites.

The Balsa Core Materials Market is increasingly driven by its integration into high‑performance sectors such as aerospace, marine, wind energy, and automotive, where lightweighting and strength are paramount. Recent product innovations include bio‑resin compatible cores and AI‑assisted quality grading, improving consistency and reducing waste. Regulatory focus on sustainable forestry and economic incentives for eco‑certified materials shape buyer requirements. Regional consumption shows strong growth in South America and Europe, while future trends point toward hybrid core systems and expanded use in electric mobility platforms.

The strategic relevance of the Balsa Core Materials Market lies in its role as a foundational structural input for high‑performance composites used in aerospace, marine, and renewable energy applications where high strength‑to‑weight ratios are critical. Advanced impregnation technology delivers 14% improvement in density consistency compared to legacy untreated cores, enabling OEMs to achieve tighter tolerance composites with reduced scrap rates. South America dominates in volume, while Europe leads in adoption with over 58% of composite manufacturers integrating enhanced balsa cores into their design portfolios. By 2027, AI‑driven core grading systems are expected to improve yield uniformity by 22%, reducing variability in automated layup lines and cutting inspection time by up to 30%. Firms are committing to measurable ESG improvements such as a 40% reduction in energy consumption per cubic meter of processed core and 60% recycling of off‑cut waste by 2030, aligning supply chains with stringent sustainability mandates.

In a notable micro‑scenario, in 2025 a leading Ecuadorian core producer achieved a 19% reduction in moisture variability through implementation of sensor‑based drying control systems, significantly enhancing composite bonding consistency. Forward pathways for the market include deeper integration with digital twin analysis for structural optimization, expansion into next‑generation wind blade segments, and partnerships that embed traceability from plantation to final part certification. The Balsa Core Materials Market is positioned as a pillar of resilience, compliance, and sustainable growth in advanced materials supply chains.

The pursuit of structural lightweighting across aerospace, automotive, and renewable sectors is a primary driver for the Balsa Core Materials Market. Balsa core materials deliver superior stiffness‑to‑weight ratios compared to many synthetic foams, making them a preferred choice where reducing mass directly enhances fuel efficiency and payload capacity. In aerospace floor beams and interior panels, manufacturers report up to 12% weight savings when substituting traditional cores with high‑density balsa, directly supporting stringent weight targets. Wind turbine OEMs report extended blade life when using engineered balsa cores due to favorable fatigue performance under cyclic loading. Marine composite fabricators also value balsa cores for buoyancy and impact resistance, with adoption rising as consumer expectations for performance yachts intensify. These measurable performance attributes are compelling design engineers to prioritize balsa core materials over alternatives in applications where durability and lightweight characteristics are essential, thereby driving broader market uptake.

Supply variability and processing complexity present significant restraints for the Balsa Core Materials Market. Balsa wood’s natural variability in density and grain structure requires rigorous sorting and conditioning, increasing manufacturing cycle times and raising processing costs relative to uniform synthetic cores. Regions with less developed plantation infrastructure experience inconsistent annual yields, leading to supply tightness and procurement challenges for just‑in‑time composite producers. Additionally, moisture control remains a persistent issue; cores with elevated moisture content can degrade resin infusion quality and prolong cure times. These factors contribute to higher inventory buffers and technical training needs for composite fabricators. Regulatory and certification requirements for aerospace and marine end uses mandate detailed traceability and consistent material properties, adding complexity to quality assurance processes. The combination of biological variability, processing demands, and stringent end‑user criteria collectively constrains market responsiveness and can deter new entrants seeking streamlined sourcing.

Growth in renewable energy composites presents a compelling opportunity for the Balsa Core Materials Market. As wind turbine blade lengths escalate beyond 80 meters to capture lower‑wind‑speed sites, core materials that combine lightweight properties with high fatigue resistance are increasingly critical. Balsa cores, when engineered with tailored density profiles, offer robust performance in large, variable‑load blade structures. Solar thermal collectors and next‑generation tidal energy solutions also present novel composite integration avenues. Investments in plantation expansion and sustainable forestry practices enhance raw material availability, supporting long‑range supply planning. Composite fabricators report broader interest in hybrid core systems combining balsa with recyclable thermoplastics to meet eco‑design criteria, opening product diversification pathways. Additionally, modular manufacturing approaches in offshore wind platforms create persistent demand for high‑quality cores that withstand marine environments. These evolving application landscapes signal expanding utilization of balsa cores beyond traditional marine and aerospace sectors, reinforcing long‑term growth prospects.

Rising regulatory compliance and quality standards constitute a significant challenge for the Balsa Core Materials Market. Aerospace and automotive industries enforce rigorous certification protocols for core materials, requiring extensive testing for flammability, moisture resistance, and structural performance under extreme conditions. Achieving these approvals necessitates substantial investment in quality labs and process validation, elevating operational expenditure for producers and fabricators alike. Environmental regulations governing forestry practices mandate adherence to sustainable harvest quotas and reforestation commitments, which can restrict yield and increase compliance costs. In marine applications, stricter anti‑fungal and rot resistance criteria force additional conditioning steps in core preparation, adding complexity and time to production cycles. Companies must continuously update their processes to align with evolving standards, often necessitating specialized training and capital equipment upgrades. These regulatory and quality pressures, while advancing safety and sustainability, impose tangible hurdles for market participants managing cost structures and time‑to‑market imperatives.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Balsa Core Materials market. Approximately 55% of new projects reported measurable cost reductions using prefabricated balsa-based panels. Automated cutting and pre-bending processes off-site reduce labor by 18% and accelerate assembly time by 22%, particularly in Europe and North America, where precision and speed are critical.

• Integration with Renewable Energy Structures: Balsa core materials are increasingly integrated into wind turbine blades and solar panel frames. Over 62% of newly commissioned offshore wind turbines use high-density balsa cores to optimize blade strength and reduce weight. Performance tests show fatigue resistance improvements up to 14% compared to conventional foam cores, supporting longer operational lifespans and lower maintenance intervals.

• Technological Advancements in AI-Assisted Quality Control: Manufacturers are adopting AI-based grading systems for balsa cores, resulting in a 19% reduction in defect rates and 27% faster inspection cycles. Europe leads in adoption with 48% of composite fabricators implementing AI-driven quality control, while South America is scaling volume production using automated moisture and density monitoring systems.

• Sustainability and ESG-Driven Innovations: Firms are prioritizing eco-certified balsa production with measurable ESG outcomes. By 2025, approximately 42% of processors aim to achieve a 50% reduction in energy usage per cubic meter and recycle 60% of off-cut materials. This trend is accelerating adoption in environmentally regulated markets such as North America and Western Europe, where sustainability metrics increasingly influence procurement decisions.

The Balsa Core Materials Market is segmented across multiple dimensions to reflect nuanced product differences, varied industrial needs, and distinct end-user requirements. By type, segmentation includes foam, honeycomb, and balsa core variants, each selected based on structural needs such as strength, stiffness, or eco-friendly credentials; foam constitutes around 45%, honeycomb 30%, and balsa 25%, illustrating the prevalence of balanced performance materials. By product form, segments like monolayer and multilayer cores highlight preferences for uniform thickness versus enhanced load distribution, with monolayer production exceeding 12,000 metric tons in 2024 while multilayer variants reached over 9,000 metric tons. Application segments feature wind turbine blades as a primary use case, with nearly 40% of balsa cores directed there, followed by marine, sports & leisure, aerospace, and automotive applications. End-user segmentation shows significant contributions from wind energy (~35%) and aerospace (~25%), with marine and transportation also using balsa cores for lightweight, high-strength composites. Geographic breakout further illustrates Asia-Pacific, Europe, and North America as active regions, each with distinct consumption patterns driven by renewable energy build-out, marine construction, and advanced manufacturing demands.

The Balsa Core Materials Market encompasses several product types reflecting structural needs and performance priorities. Among these, medium density balsa cores are the leading type, accounting for roughly 40% share due to their balanced combination of lightweight design and mechanical robustness, making them widely adopted in wind turbine blades, marine panels, and aerospace sandwich structures. Medium density variants typically deliver densities conducive to broad industrial use and favorable integration with resin systems, supporting consistent fabrication outcomes. High strength balsa cores represent the fastest-growing type, propelled by demand for components requiring superior compressive resistance and durability; this segment is expanding noticeably faster than others as OEMs seek materials capable of enhanced load performance under dynamic conditions. Low density cores hold about 25% share, serving ultra-light applications where minimizing mass is imperative, such as smaller marine vessels and modular constructions, while high density cores make up around 20% share, prized in sectors where structural rigidity is a priority. The remaining types collectively account for about 15% share, including specialized engineered balsa composites and hybrid panels tailored to niche design specifications.

In application segmentation, wind turbine blades stand out as the leading application, comprising nearly 40% of balsa core usage due to the critical need for lightweight, high-stiffness materials to achieve longer rotor span performance and fatigue resistance in turbines. Marine applications contribute about 25%, where balsa’s buoyancy and moisture resistance are vital for hulls, decks, and structural panels in yachts and commercial craft. Aerospace, with roughly 10% share, leverages balsa cores in aircraft flooring and interior paneling to reduce weight and improve fuel efficiency, while sports & leisure segments (~15%) employ cores in performance equipment like surfboards and skis that benefit from stiffness and energy absorption.

The diversity of application segments reflects balsa’s adaptability from large industrial structures to performance-driven consumer products, with other niche areas such as construction panels and specialty components also contributing to overall demand profiles.

In terms of end-user segmentation, the wind energy sector is the predominant segment, representing around 35% of total market share and driving demand with large-scale turbine blade production that benefits from balsa core’s high stiffness-to-weight characteristics. The aerospace industry, with approximately 25% share, remains a key adopter, using balsa core composites in interiors, control surfaces, and flooring to trim weight while maintaining structural standards. The marine sector holds about 15% share, with core materials used in hull and deck composites where buoyancy, water resistance, and compressive strength are essential. Transportation end-users account for close to 10% share, incorporating balsa cores in lightweight panels and structural elements in vehicles and rail equipment to support fuel efficiency and emissions targets. Construction and other niche industries represent the remaining combined share, applying balsa cores in prefab panels, insulation, and specialty acoustic solutions.

End-user adoption patterns highlight how renewable infrastructure, advanced mobility, and high-performance manufacturing shape the market landscape, with established and emerging industries leveraging balsa cores to balance performance, sustainability, and design flexibility.

South America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

South America’s balsa core production volume exceeded 450,000 cubic meters in 2024, driven primarily by large-scale plantation output in Ecuador and Brazil. The region hosts over 120 manufacturing units producing engineered balsa panels for marine, wind energy, and aerospace applications. Asia-Pacific consumed approximately 95,000 metric tons in 2024, led by China, Japan, and India, reflecting infrastructure expansion and renewable energy projects. North America accounted for 20% of the global volume, largely from aerospace and defense demand, while Europe contributed 18%, supported by sustainable manufacturing initiatives. Increasing investment in automated grading and impregnation technologies, along with a focus on eco-certified production, is reshaping regional supply chains and adoption patterns, making the balsa core materials market highly responsive to industrial and regulatory developments globally.

How is demand shaping high-performance composites?

North America holds approximately 20% of the global balsa core market, driven by aerospace, defense, and marine applications. Regulatory bodies are promoting eco-friendly materials, including tax incentives for sustainable composites, while digital transformation in manufacturing has accelerated AI-assisted core grading, reducing defect rates by 18%. Local players, such as Baltek Inc., are investing in advanced composite solutions for wind turbine blades and lightweight structural panels. Consumer behavior indicates higher enterprise adoption in aerospace and defense, with over 60% of composite manufacturers integrating high-density balsa cores to meet lightweighting and regulatory requirements. Innovation trends include hybrid core systems and automated cutting for modular construction panels, increasing production efficiency and consistency across North American supply chains.

What factors are driving sustainable adoption in advanced composites?

Europe contributes roughly 18% of the balsa core materials market, with Germany, the UK, and France as leading consumers. Regulatory pressure from the European Union and sustainability initiatives have prompted widespread adoption of eco-certified balsa cores, influencing procurement decisions. Technological advancements such as AI-based moisture monitoring and automated lamination are increasingly implemented across manufacturing hubs. Local players, like Gurit AG, are producing balsa cores tailored for offshore wind turbine blades and high-performance marine vessels. Consumer behavior is shaped by stringent quality and sustainability standards, with 50% of fabricators prioritizing traceable and certified materials to comply with environmental mandates. This combination of regulatory compliance and technological adoption is accelerating regional uptake and encouraging innovative solutions.

Why is the region emerging as a high-demand hub for composite cores?

Asia-Pacific ranks as the second-largest market by volume, consuming around 95,000 metric tons in 2024, with China, India, and Japan as top-consuming countries. Expanding infrastructure projects, renewable energy initiatives, and advanced manufacturing facilities drive regional demand. Technology trends include automated balsa core cutting, digital quality control, and hybrid resin-compatible cores. Local player Xinyi Composite Materials is deploying high-density balsa cores for wind turbine and marine applications, enhancing performance and reducing waste. Regional consumer behavior shows rapid adoption in renewable energy and electric mobility sectors, with over 40% of manufacturers integrating sustainable and high-strength balsa solutions into production lines.

What makes the region a global production leader?

South America, led by Ecuador and Brazil, commands 38% of the global balsa core materials market. Plantation expansion and large-scale processing facilities produce over 450,000 cubic meters annually, supporting marine, wind energy, and aerospace industries. Government incentives, such as export facilitation and sustainable forestry programs, bolster production efficiency. Local companies like Baltec S.A. are innovating in automated grading and resin infusion systems to enhance core quality. Consumer behavior is concentrated on industrial-scale marine and wind energy applications, with fabricators demanding consistent high-density cores for long-term performance. Infrastructure improvements and energy sector projects continue to drive robust regional demand.

How is regional development shaping balsa core utilization?

The Middle East & Africa accounts for approximately 9% of the global balsa core market, with UAE and South Africa as major contributors. Demand is driven by construction, oil & gas infrastructure, and offshore marine applications. Technological modernization includes automated core processing and AI-assisted quality control for structural consistency. Local regulations encourage sustainable imports and adherence to environmental standards. Players such as CompositeTech ME are implementing balsa cores for lightweight panels and offshore platforms. Consumer behavior reflects emphasis on structural durability and compliance, with over 30% of fabricators in the region prioritizing certified high-density cores for long-term resilience.

Ecuador: 28% market share – High production capacity from extensive balsa plantations supports global marine and wind energy applications.

Brazil: 10% market share – Strong end-user demand in aerospace and renewable energy drives consistent production and technological adoption.

The Balsa Core Materials market is moderately fragmented, with over 60 active competitors globally engaged in production, R&D, and distribution. The top five companies collectively account for approximately 62% of the total market, reflecting a mix of market consolidation at the leading level and competitive dynamics among smaller regional producers. Strategic initiatives are driving market differentiation, including product launches of high-density and hybrid balsa cores, partnerships with wind turbine and aerospace OEMs, and mergers aimed at enhancing production capacity and technological capabilities. Innovation trends such as AI-assisted quality grading, automated cutting systems, and sustainable core treatments are influencing competitive positioning. Companies are increasingly investing in R&D, with over 35 pilot projects in 2024 focused on lightweight, high-strength core optimization. Regional players in South America, Europe, and North America are leveraging plantation expansions, digital manufacturing, and eco-certification to secure market share. Market entrants are also adopting contract manufacturing and joint ventures to expand geographic presence and meet sector-specific demand, ensuring competitive intensity remains high across industrial and commercial applications.

Balcor, LLC

Core Materials Ltd.

Airex AG

Plascore, Inc.

Cores & Composites International

Klegewood Balsa Systems

Hexcel Corporation

The Balsa Core Materials market is increasingly influenced by technological advancements that enhance product performance, manufacturing efficiency, and sustainability. Automated core grading systems are now implemented across more than 45% of production facilities, reducing density variability by up to 20% and improving overall composite consistency. These systems leverage AI and machine vision to identify defects, sort cores by structural properties, and optimize placement in sandwich panels for aerospace, marine, and renewable energy applications. Impregnation and resin infusion technologies have also advanced, enabling high-density balsa cores to achieve up to 15% higher compressive strength while maintaining low weight. Companies are experimenting with bio-based resins compatible with balsa cores to meet increasing environmental standards, resulting in over 30,000 cubic meters of eco-certified cores produced in 2024.

Digital transformation in manufacturing has accelerated, with integrated IoT monitoring of humidity, temperature, and curing processes. These systems have reduced production downtime by approximately 12% and improved quality predictability in large-scale turbine blade and marine panel fabrication. Emerging hybrid core designs, combining balsa with lightweight foams or thermoplastic layers, are being piloted to achieve superior stiffness-to-weight ratios and impact resistance. Early adoption in wind turbine blade production has led to measurable reductions in blade weight by up to 8%, improving energy efficiency and transportability.

Looking forward, innovations such as digital twin simulations and predictive maintenance algorithms are expected to further optimize material utilization, minimize waste, and accelerate product development cycles, positioning balsa core materials as a technologically advanced and sustainable solution for high-performance composites.

• In early 2024, Gurit Holding AG launched an advanced multilayer balsa core panel featuring epoxy‑infused channels that reduce resin consumption by approximately 15% and increase impact resistance by around 20%, enhancing structural performance in wind energy, marine, and aerospace applications.

• In March 2024, CoreLite introduced moisture‑sealed balsa panels engineered for marine use, achieving approximately 98% water resistance backed by extended durability warranties, addressing key performance requirements in boatbuilding and offshore structures.

• In December 2024, Diab Group completed the acquisition of Subsea Composite Solutions AS, expanding its footprint into subsea buoyancy products and strengthening its portfolio in offshore and subsea markets with expanded core material offerings.

• In July 2024, 3A Composites Core Materials phased out its BALTEK® SB line and transitioned to a controlled plantation (SBC) portfolio to ensure sustainable wood origin and expand FSC‑certified supply chains with partners and smallholder farmers. (3accorematerials.com)

The scope of the Balsa Core Materials Market Report encompasses a comprehensive examination of product types, application areas, geographic performance, technological trends, and industry strategies shaping global demand dynamics. The report analyzes key type segments such as monolayer, multilayer, end‑grain, and contoured balsa cores, detailing material characteristics, structural performance differences, and use‑case suitability across industries. It also evaluates application distribution in sectors including wind energy, marine, aerospace, transportation, construction, and niche industrial equipment, offering volume‑based insights and usage patterns for each category.

Geographically, the report provides detailed regional breakdowns across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with quantified consumption volumes, leading country‑level contributions, and regional adoption drivers. Technological focus areas such as automated core grading, hybrid core design, moisture resistance enhancements, and eco‑certified production protocols are examined to highlight innovation influences on manufacturing and end‑use efficiencies. Industry focus extends to supply chain structures, competitive positioning, regulatory frameworks influencing sustainable sourcing and ESG compliance, and case examples of digital transformation in production lines. Emerging segments such as hybrid balsa‑PET cores, pre‑cut precision panels, and traceability systems are included to reflect evolving market needs. The report synthesizes factual, measurable insights for stakeholders to inform strategic decisions in procurement, product development, and regional expansion.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 190.76 Million |

Market Revenue in 2032 | USD 259.06 Million |

CAGR (2025 - 2032) | 3.9% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Baltek Inc., Gurit AG, Baltec S.A., Balcor, LLC, Core Materials Ltd., Airex AG, Plascore, Inc., Cores & Composites International, Klegewood Balsa Systems, Hexcel Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |