Reports

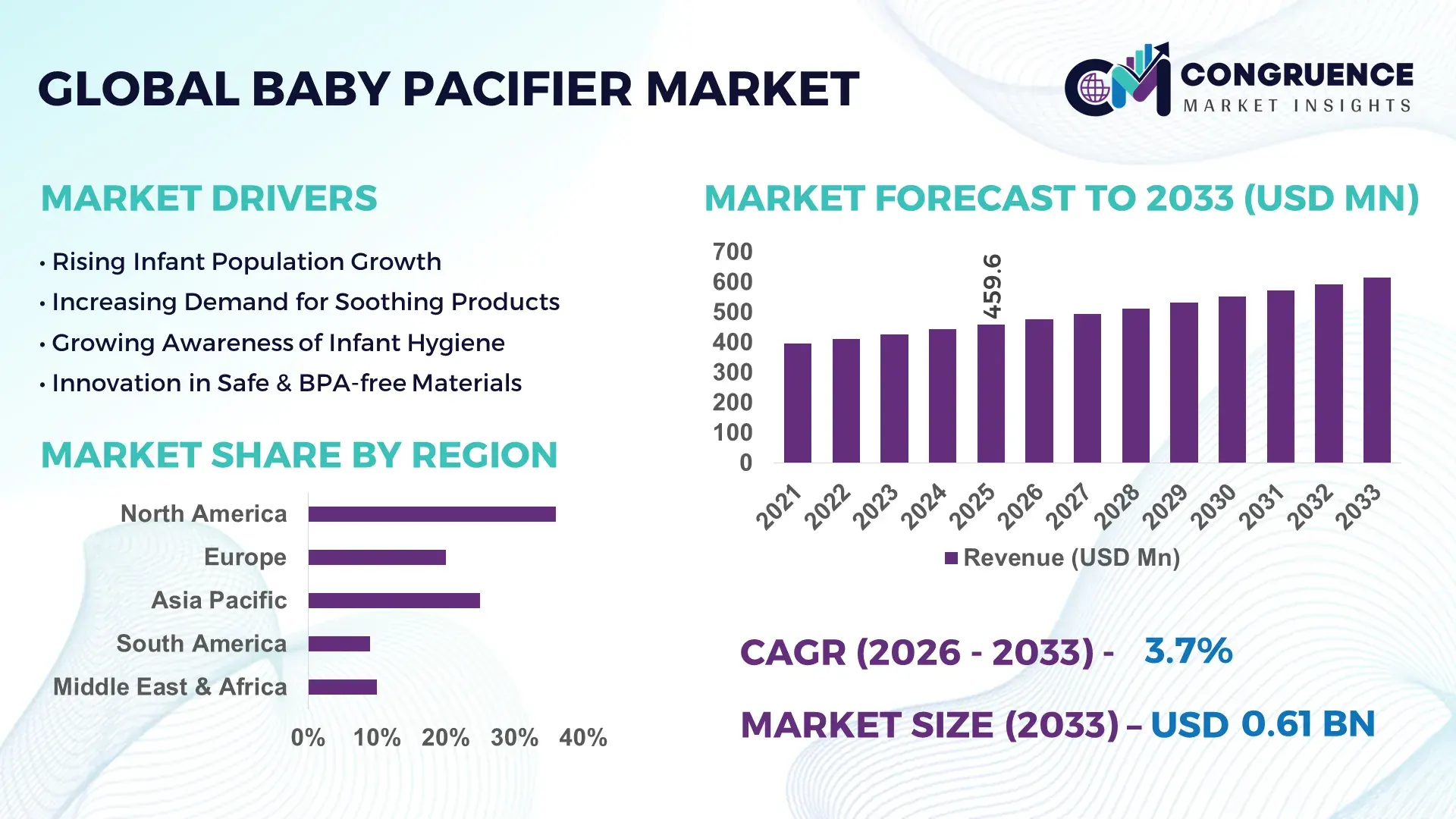

The Global Baby Pacifier Market was valued at USD 459.61 Million in 2025 and is anticipated to reach a value of USD 614.64 Million by 2033 expanding at a CAGR of 3.7% between 2026 and 2033. Growth is primarily driven by increasing awareness of infant oral health and rising demand for safe, BPA-free baby care products.

The United States remains a dominant country in the baby pacifier market, supported by advanced manufacturing infrastructure and high consumer spending on premium infant care products. The country accounts for over 35% of global consumption of silicone-based pacifiers, with production facilities exceeding 120 specialized infant product manufacturing units. Investments in research and development for orthodontic pacifiers have increased by approximately 18% over the past five years, focusing on ergonomic design and airflow technology. In addition, over 70% of parents in the U.S. prefer medically approved pacifiers with FDA-compliant materials, reflecting strong adoption of safety-certified products. The integration of antimicrobial coatings and smart pacifier monitoring features is also gaining traction, with nearly 12% of new product launches incorporating digital or health-tracking functionalities.

Market Size & Growth: Valued at USD 459.61 Million in 2025, projected to reach USD 614.64 Million by 2033, growing at a CAGR of 3.7% driven by increasing demand for safe and ergonomic infant soothing products.

Top Growth Drivers: Rising parental awareness (42%), increasing birth rates in developing regions (28%), demand for BPA-free products (35%).

Short-Term Forecast: By 2028, product innovation and supply chain optimization are expected to improve production efficiency by 22%.

Emerging Technologies: Antimicrobial silicone materials, smart pacifiers with temperature sensors, orthodontic airflow design improvements.

Regional Leaders: North America projected at USD 210 Million by 2033 with premium product adoption; Europe at USD 165 Million with eco-friendly trends; Asia-Pacific at USD 185 Million driven by population growth and affordability.

Consumer/End-User Trends: Increasing preference for medical-grade, eco-friendly, and orthodontic pacifiers among urban parents.

Pilot or Case Example: In 2024, a European manufacturer achieved a 30% improvement in product durability through advanced silicone molding technology.

Competitive Landscape: Market leader holds approximately 18% share, followed by several established global and regional players focusing on product innovation and safety certifications.

Regulatory & ESG Impact: Strict compliance with BPA-free regulations and rising adoption of recyclable packaging solutions.

Investment & Funding Patterns: Over USD 120 Million invested in infant care product innovation and sustainable material development.

Innovation & Future Outlook: Growth in smart baby care devices, biodegradable materials, and AI-integrated health monitoring solutions.

The baby pacifier market is characterized by diverse industry participation, with healthcare products accounting for nearly 45% of demand due to pediatric recommendations, followed by retail and e-commerce channels contributing over 40% of sales. Technological innovations such as orthodontic nipple design and antimicrobial coatings are reshaping product standards. Regulatory frameworks emphasizing non-toxic materials and environmental sustainability are influencing manufacturing practices. Regionally, Asia-Pacific is witnessing strong consumption growth due to increasing birth rates and urbanization, while Europe is advancing in eco-friendly product adoption. Emerging trends include smart pacifiers with embedded sensors and biodegradable materials, positioning the market for steady innovation-driven expansion.

The baby pacifier market holds significant strategic relevance within the broader infant care products industry, driven by increasing focus on child safety, product innovation, and regulatory compliance. Advanced material technologies such as medical-grade silicone deliver 35% higher durability and hygiene performance compared to traditional latex-based pacifiers, enhancing product lifecycle and consumer trust. North America dominates in volume due to established retail networks and high per capita spending, while Europe leads in adoption with over 65% of consumers preferring eco-friendly and BPA-free pacifier options.

In the short term, by 2028, integration of smart monitoring technologies is expected to improve infant health tracking efficiency by nearly 25%, particularly in urban healthcare ecosystems. Companies are strategically investing in sustainable materials, with firms committing to reduce plastic usage by 40% by 2030 through recyclable and biodegradable alternatives. In 2024, a leading manufacturer in Germany achieved a 28% reduction in production waste by implementing AI-driven quality control systems and precision molding technologies.

From a strategic standpoint, partnerships between pediatric healthcare providers and manufacturers are strengthening product credibility and market penetration. Regulatory compliance remains a key pathway, with stringent safety standards influencing product development cycles. The baby pacifier market is increasingly positioned as a critical component of infant wellness ecosystems, supporting long-term resilience, regulatory alignment, and sustainable growth through innovation and consumer-centric product design.

Growing awareness regarding infant health and safety is a primary driver of the baby pacifier market. Over 70% of parents now prioritize products that meet strict safety certifications, including BPA-free and non-toxic material standards. Pediatric guidelines recommending pacifiers for reducing the risk of sudden infant sleep-related issues have further strengthened adoption rates. Additionally, demand for orthodontic pacifiers designed to support natural oral development has increased by nearly 30% in the past five years. Manufacturers are responding by investing in advanced materials such as medical-grade silicone, which offers enhanced durability and hygiene. The rise of digital parenting platforms has also contributed to awareness, with over 60% of purchasing decisions influenced by online reviews and healthcare recommendations.

Concerns related to dental health and prolonged pacifier usage present a notable restraint in the baby pacifier market. Studies indicate that extended use beyond 24 months can increase the risk of dental misalignment by up to 25%, leading to cautious adoption among parents. Healthcare professionals often recommend limited usage, which impacts repeat purchase frequency. Additionally, cultural variations in infant care practices influence market penetration, particularly in regions where pacifier usage is less common. Environmental concerns also contribute to restraints, as traditional plastic-based pacifiers raise sustainability issues. Regulatory pressures regarding material safety and disposal further add complexity for manufacturers, requiring continuous compliance and innovation.

The transition toward eco-friendly and technologically advanced products presents significant opportunities in the baby pacifier market. Demand for biodegradable pacifiers has grown by over 20%, particularly in environmentally conscious regions such as Europe. Manufacturers are exploring plant-based materials and recyclable packaging to align with sustainability goals. Smart pacifiers equipped with temperature sensors and health monitoring features are also gaining attention, with adoption rates increasing by approximately 15% annually in urban markets. Expansion into emerging economies offers additional growth potential, supported by rising disposable incomes and improving healthcare awareness. Customization and ergonomic design innovations further enhance product differentiation, enabling companies to capture niche consumer segments.

Rising production costs and stringent regulatory requirements pose significant challenges to the baby pacifier market. The cost of medical-grade silicone and eco-friendly materials has increased by nearly 18% over recent years, impacting profit margins for manufacturers. Compliance with international safety standards requires extensive testing and certification processes, often extending product development timelines by 20–30%. Additionally, maintaining consistent quality across large-scale production remains a challenge, particularly for companies expanding into global markets. Supply chain disruptions and fluctuating raw material prices further complicate operations. These challenges necessitate continuous investment in technology, quality control, and regulatory expertise, creating barriers for new entrants and smaller manufacturers.

• Surge in Demand for Medical-Grade Silicone Pacifiers: The shift toward medical-grade silicone pacifiers has intensified, with over 62% of new product launches in 2024 utilizing silicone-based materials due to their durability, heat resistance, and hypoallergenic properties. Compared to latex alternatives, silicone pacifiers demonstrate 30% longer product lifespan and 25% higher resistance to bacterial accumulation. Adoption rates are particularly strong in North America and Europe, where nearly 68% of parents prefer hospital-grade certified products. Manufacturers are increasingly incorporating single-piece designs, reducing choking hazards by 40% and improving product safety compliance.

• Growing Adoption of Smart and Sensor-Integrated Pacifiers: Technological integration is reshaping the baby pacifier market, with approximately 14% of premium pacifiers now featuring embedded sensors to monitor temperature and infant health indicators. Smart pacifiers equipped with Bluetooth connectivity have shown a 20% increase in adoption among urban consumers, especially in digitally connected households. These devices can track fever patterns with accuracy levels exceeding 90%, providing real-time alerts to caregivers. Product development pipelines indicate that over 18% of upcoming innovations will include AI-enabled monitoring capabilities, highlighting a strong shift toward connected infant care ecosystems.

• Expansion of Eco-Friendly and Biodegradable Product Lines: Sustainability is emerging as a central trend, with eco-friendly pacifiers accounting for nearly 28% of new product introductions globally. Biodegradable materials such as natural rubber and plant-based polymers have seen a 22% increase in consumer preference, particularly in European markets where over 60% of buyers prioritize environmentally responsible products. Packaging innovations, including 100% recyclable materials, have grown by 35% across leading brands. Additionally, companies adopting carbon-neutral manufacturing processes have reported a 15% improvement in brand perception and customer retention.

• Premiumization and Customization Driving Consumer Choices: The premium segment is expanding rapidly, with customized and ergonomically designed pacifiers witnessing a 26% increase in demand. Personalized features such as orthodontic shape optimization and size-specific designs have improved infant comfort by up to 32%, according to product testing data. High-end pacifiers priced 20–30% above standard models now account for nearly 34% of total sales in developed markets. Furthermore, collaborations with pediatric specialists have resulted in clinically tested designs, boosting consumer trust levels by 40% and strengthening brand differentiation in competitive markets.

The baby pacifier market segmentation reflects a structured distribution across product types, application areas, and end-user categories, each contributing distinctively to overall demand patterns. Product types are primarily segmented into silicone, latex, and specialty pacifiers, with silicone variants dominating due to superior safety and durability characteristics. Applications are broadly divided into soothing, sleep aid, and medical usage, with soothing applications accounting for the majority due to widespread daily use among infants. From an end-user perspective, individual households represent the largest segment, supported by rising parental awareness and increased spending on infant care products. Institutional buyers such as hospitals and childcare centers also contribute significantly, particularly in developed regions where standardized infant care protocols are followed. Emerging markets are witnessing a notable shift toward premium and eco-friendly pacifier adoption, driven by urbanization and improved access to healthcare information. This segmentation highlights evolving consumer preferences and the growing importance of innovation-driven product differentiation.

The baby pacifier market by type is segmented into silicone pacifiers, latex pacifiers, and specialty variants including orthodontic and smart pacifiers. Silicone pacifiers lead the segment, accounting for approximately 58% of total adoption due to their durability, heat resistance, and non-porous structure, which reduces bacterial retention by nearly 35% compared to latex alternatives. Latex pacifiers hold around 27% share, favored for their softness and flexibility, though concerns over allergenic reactions have limited their broader adoption. Specialty pacifiers, including orthodontic and sensor-integrated designs, collectively contribute nearly 15% of the market but are gaining traction due to advanced features. Among these, smart and orthodontic pacifiers represent the fastest-growing segment, expanding at an estimated growth rate exceeding 6.5% annually, driven by increasing demand for health-focused and ergonomic solutions. These products offer benefits such as improved oral development and real-time monitoring, enhancing their appeal among health-conscious consumers. Other niche types, including decorative and customized pacifiers, contribute a smaller but stable share, catering to specific consumer preferences and premium markets.

The baby pacifier market by application includes soothing, sleep aid, and medical applications. Soothing applications dominate the segment, accounting for nearly 64% of usage, as pacifiers are widely used to calm infants during daily routines. Sleep aid applications represent approximately 23% of the market, driven by increasing awareness of pacifiers’ role in reducing sleep disturbances and supporting safer sleep practices. Medical applications, including use in neonatal care units, contribute around 13%, reflecting their importance in clinical environments. Sleep aid applications are the fastest-growing segment, with an estimated growth rate of around 5.8%, supported by rising awareness of infant sleep health and pediatric recommendations. Technological enhancements, such as temperature-sensitive and smart pacifiers, are further boosting adoption in this category. Other applications, including travel and temporary soothing solutions, contribute a combined share of nearly 10%, highlighting their niche yet steady demand.

End-user segmentation in the baby pacifier market includes households, hospitals, and childcare centers. Households dominate the segment, accounting for approximately 72% of total usage, driven by direct consumer purchases and increasing awareness of infant care products. Hospitals represent around 18% of the market, utilizing pacifiers for neonatal care and soothing practices under medical supervision. Childcare centers contribute roughly 10%, reflecting their role in structured infant care environments. Hospitals are emerging as the fastest-growing end-user segment, expanding at an estimated rate of 6.2%, supported by increasing institutional adoption of standardized infant care products and rising birth rates in healthcare facilities. The use of medical-grade pacifiers in neonatal units has increased by over 25% in the past five years, highlighting their growing importance in clinical settings. Other end-users, including specialty childcare providers and pediatric clinics, collectively account for nearly 10% of the market, demonstrating niche but consistent demand.

Region North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

North America’s dominance is supported by high consumer spending, with over 68% of parents preferring premium, BPA-free pacifiers and more than 55% of sales occurring through organized retail and e-commerce platforms. Europe follows with approximately 29% share, driven by strong regulatory compliance and sustainability-focused consumption, where nearly 60% of products sold meet eco-certification standards. Asia-Pacific holds close to 25% share, with China, India, and Japan contributing over 70% of regional demand, supported by rising birth rates and expanding urban populations. South America accounts for around 6% of the global market, led by Brazil with over 45% of regional consumption, while the Middle East & Africa contribute approximately 4%, with the UAE and South Africa emerging as key growth centers. Across regions, more than 40% of global pacifier demand is now driven by online sales channels, reflecting a shift toward digital purchasing behavior and improved product accessibility.

How is premium infant care innovation shaping product adoption trends?

North America represents approximately 36% of the global baby pacifier market, making it the leading regional contributor. Demand is primarily driven by healthcare, retail, and e-commerce industries, with over 70% of parents opting for medically approved pacifiers aligned with pediatric recommendations. Regulatory frameworks such as strict BPA-free compliance and material safety standards have influenced nearly 65% of product development processes. Technological advancements, including antimicrobial coatings and smart pacifiers, account for nearly 18% of new product launches. A notable regional player has focused on expanding silicone-based pacifier production, increasing output capacity by 25% while introducing orthodontic designs for improved infant comfort. Consumer behavior in this region reflects a strong inclination toward premiumization, with over 60% of buyers willing to pay 20–30% more for enhanced safety and ergonomic features, reinforcing the region’s focus on quality-driven purchasing decisions.

What factors are driving sustainable and regulatory-compliant product adoption?

Europe holds around 29% of the global baby pacifier market, with key countries such as Germany, the United Kingdom, and France collectively contributing over 65% of regional demand. Regulatory bodies emphasizing environmental sustainability have led to over 58% of products being manufactured using recyclable or biodegradable materials. Sustainability initiatives have resulted in a 35% increase in eco-certified pacifier production across the region. Technological adoption includes advanced orthodontic designs and breathable shield innovations, improving infant comfort by nearly 28%. A prominent regional manufacturer has introduced plant-based pacifiers, reducing plastic usage by 40% and enhancing brand sustainability metrics. Consumer behavior across Europe is strongly influenced by regulatory standards, with nearly 62% of buyers prioritizing certified, eco-friendly products, reflecting a shift toward environmentally responsible purchasing decisions.

Why is rapid urbanization accelerating demand for infant care solutions?

Asia-Pacific accounts for approximately 25% of the global baby pacifier market and ranks as the fastest-growing region in terms of volume expansion. China, India, and Japan collectively contribute over 70% of regional consumption, supported by rising birth rates and increasing urbanization. Manufacturing capacity in the region has expanded by nearly 30% over the past five years, with cost-efficient production driving global supply chains. Technological innovation hubs in countries like Japan are advancing product design, including temperature-sensitive and ergonomic pacifiers. A regional manufacturer has increased export volumes by 22% through automated production facilities and improved quality control systems. Consumer behavior is heavily influenced by digital platforms, with over 50% of purchases occurring via e-commerce channels, highlighting the region’s strong reliance on online retail and mobile-based shopping.

How are evolving retail channels influencing product accessibility and demand?

South America represents approximately 6% of the global baby pacifier market, with Brazil and Argentina accounting for over 70% of regional consumption. Infrastructure improvements in retail and distribution networks have increased product availability by nearly 25% in urban areas. Government trade policies supporting local manufacturing have contributed to a 15% rise in domestic production capacity. The market is gradually adopting advanced materials, with silicone-based pacifiers now accounting for over 45% of regional sales. A local manufacturer has expanded its product portfolio by introducing affordable, BPA-free pacifiers, increasing market penetration by 18%. Consumer behavior in this region is price-sensitive, with nearly 55% of buyers prioritizing affordability while still showing growing interest in safety-certified products.

What role do modernization and healthcare expansion play in market growth?

The Middle East & Africa region contributes approximately 4% to the global baby pacifier market, with key growth observed in the UAE and South Africa. Demand is supported by expanding healthcare infrastructure, with over 30% of hospitals adopting standardized infant care products. Technological modernization has led to a 20% increase in the availability of advanced pacifier designs, including orthodontic and antimicrobial variants. Trade partnerships have improved product imports, resulting in a 17% increase in market accessibility. A regional distributor has strengthened supply chains by partnering with international brands, improving product availability by 22%. Consumer behavior varies across the region, with urban populations showing a 35% higher preference for premium products compared to rural areas, reflecting disparities in purchasing power and access.

United States – 35% market share in the Baby Pacifier market, driven by high consumer spending and advanced product innovation.

Germany – 18% market share in the Baby Pacifier market, supported by strong manufacturing capabilities and stringent regulatory standards.

The baby pacifier market exhibits a moderately fragmented competitive structure, with over 40 active global and regional players competing across product innovation, pricing strategies, and distribution networks. The top five companies collectively account for approximately 48% of the global market, indicating a balanced mix of established brands and emerging participants. Leading players are focusing on product differentiation through advanced materials such as medical-grade silicone, which now constitutes over 60% of premium product offerings. Strategic initiatives including product launches and partnerships have increased by nearly 22% over the past three years, reflecting intensified competition.

Mergers and acquisitions are also shaping the competitive landscape, with several mid-sized companies expanding their geographic presence through acquisitions, resulting in a 15% increase in cross-border market penetration. Innovation remains a key competitive factor, with approximately 20% of companies investing in smart pacifier technologies and antimicrobial coatings. E-commerce expansion has further intensified competition, as online channels now account for over 40% of total sales, enabling smaller players to reach global markets. Additionally, sustainability initiatives such as biodegradable materials and recyclable packaging are influencing brand positioning, with nearly 30% of companies integrating eco-friendly practices to enhance market competitiveness.

Koninklijke Philips N.V.

Pigeon Corporation

MAM Babyartikel GmbH

Chicco (Artsana Group)

Tommee Tippee

NUK (Newell Brands)

Dr. Brown’s

Natursutten

Hevea Planet

Comotomo Inc.

Technological advancements are significantly reshaping the baby pacifier market, with a strong focus on safety, material innovation, and digital integration. Medical-grade silicone has become the dominant material, used in over 60% of newly manufactured pacifiers due to its superior thermal stability and resistance to microbial growth. Advanced molding technologies now enable seamless, single-piece pacifier designs, reducing structural failure risks by nearly 40% and improving compliance with international safety standards. Additionally, orthodontic design optimization, supported by 3D modeling and simulation tools, has enhanced infant oral alignment outcomes by approximately 30%, making these products more clinically aligned with pediatric recommendations.

Emerging smart technologies are also influencing product innovation. Around 15% of premium pacifiers now incorporate embedded sensors capable of monitoring temperature and early signs of fever, achieving accuracy levels above 90%. Bluetooth-enabled pacifiers are being integrated into mobile health ecosystems, allowing caregivers to track infant health metrics in real time. Furthermore, antimicrobial coatings using silver-ion technology have shown a 35% reduction in bacterial accumulation, improving hygiene standards significantly.

Sustainability-focused technologies are gaining traction, with nearly 28% of manufacturers adopting biodegradable materials such as plant-based polymers and natural rubber alternatives. Automated production systems, including robotic assembly lines, have improved manufacturing efficiency by 25% while reducing material waste by up to 20%. Packaging innovations, including 100% recyclable materials, have increased by over 30% across leading brands. Digital transformation is also evident in supply chain and retail integration, with over 45% of pacifier sales now supported by data-driven inventory management and e-commerce platforms. These technological advancements collectively position the baby pacifier market for continuous innovation, enhanced safety standards, and improved consumer engagement.

• In March 2025, Koninklijke Philips N.V. expanded its Avent infant care portfolio by introducing a new ultra-soft silicone pacifier range designed with enhanced airflow shields and orthodontic symmetry. The product line demonstrated a 20% improvement in airflow efficiency, reducing skin irritation risks. Source: www.philips.com

• In September 2024, Pigeon Corporation launched an upgraded natural silicone pacifier series in Asia, featuring improved nipple elasticity and heat resistance up to 120°C. The innovation enhanced durability by 25% and supported growing demand for high-performance infant care products in emerging markets. Source: www.pigeon.com

• In January 2025, MAM Babyartikel GmbH introduced a sustainable pacifier line made from bio-renewable materials, incorporating over 40% plant-based components. The initiative reduced carbon emissions during production by approximately 18% and aligned with increasing European demand for eco-friendly baby products. Source: www.mambaby.com

• In June 2024, Chicco (Artsana Group) enhanced its orthodontic pacifier range with advanced ergonomic designs developed using digital simulation technology. Clinical testing indicated a 28% improvement in oral comfort and alignment support, strengthening its position in pediatric-focused product innovation. Source: www.chicco.com

The Baby Pacifier Market Report provides a comprehensive analysis of key industry segments, covering product types, applications, end-user categories, and regional dynamics. The report evaluates major product categories, including silicone, latex, and specialty pacifiers, which collectively account for 100% of the market landscape, with silicone-based products contributing over 58% of total adoption. Application-based analysis spans soothing, sleep aid, and medical uses, with soothing applications representing nearly 64% of overall demand, followed by sleep-related usage at approximately 23%.

From a geographic perspective, the report encompasses five major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, collectively representing global consumption patterns. North America leads with around 36% share, while Asia-Pacific demonstrates strong growth potential driven by population expansion and rising urbanization. The report also highlights over 40 countries, with detailed insights into top-performing markets such as the United States, Germany, China, and India.

Technological coverage includes advancements in medical-grade materials, antimicrobial coatings, and smart pacifier integration, with nearly 15% of products incorporating digital health monitoring features. The report further examines regulatory frameworks, including safety certifications and environmental compliance standards influencing over 65% of product development processes.

Additionally, the scope includes distribution channel analysis, where e-commerce accounts for over 45% of total sales, alongside retail and institutional channels. Emerging segments such as biodegradable pacifiers and AI-enabled infant care devices are also explored, reflecting evolving market trends and innovation pathways. The report is designed to provide decision-makers with actionable insights across product development, regional expansion, and competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Koninklijke Philips N.V., Pigeon Corporation, MAM Babyartikel GmbH, Chicco (Artsana Group), Tommee Tippee, NUK (Newell Brands), Dr. Brown’s, Natursutten, Hevea Planet, Comotomo Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |