Reports

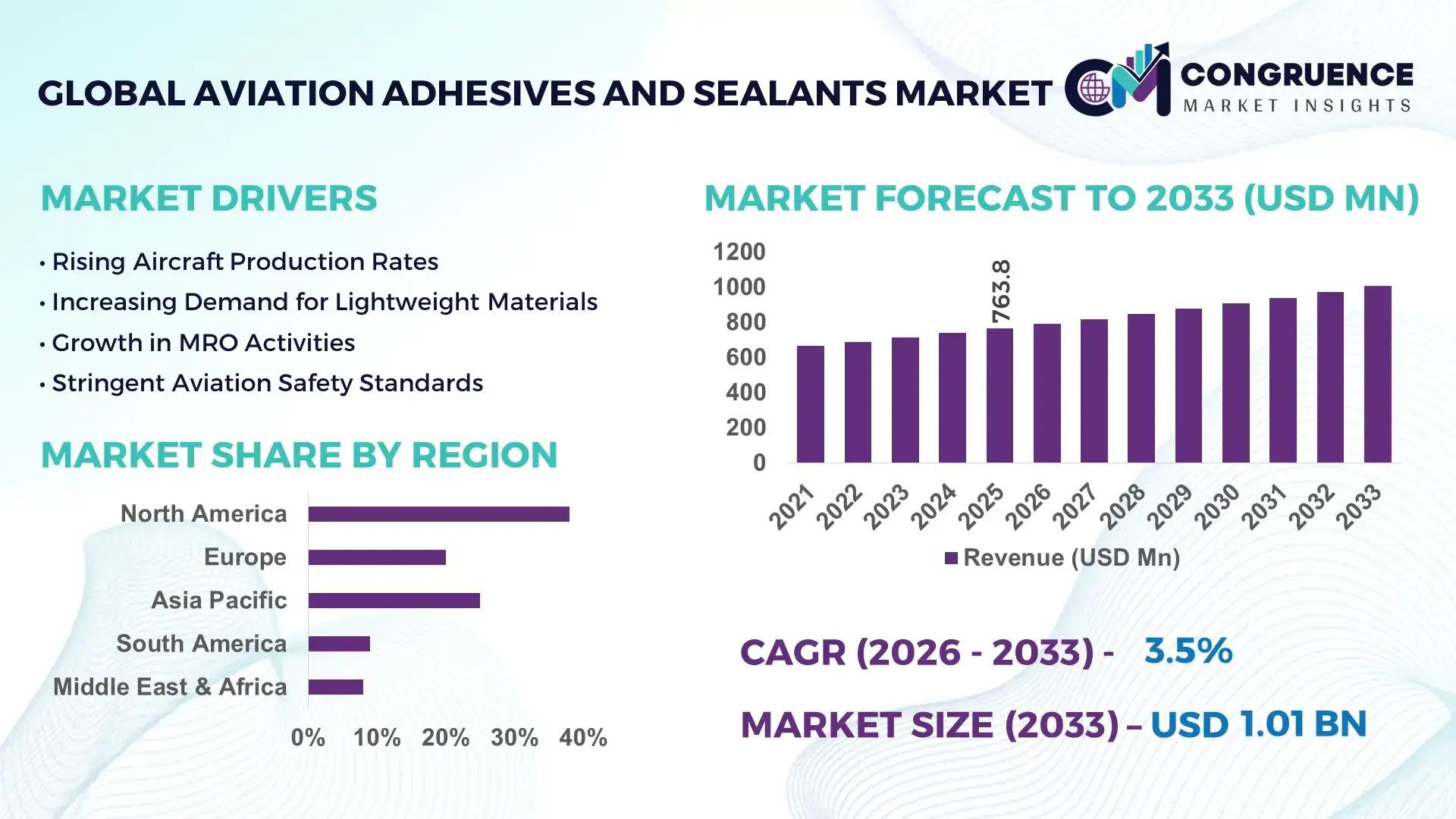

The Global Aviation Adhesives and Sealants Market was valued at USD 763.78 Million in 2025 and is anticipated to reach a value of USD 1005.75 Million by 2033 expanding at a CAGR of 3.5% between 2026 and 2033. The growth is primarily driven by increasing aircraft production rates and the shift toward lightweight composite materials in modern aviation structures.

The United States continues to lead the aviation adhesives and sealants market due to its extensive aerospace manufacturing ecosystem and high defense spending. The country hosts over 2,000 aerospace manufacturing facilities and accounts for a significant portion of global aircraft production capacity. Investments exceeding USD 50 billion annually in aerospace R&D have accelerated the adoption of advanced bonding technologies. Commercial aviation accounts for nearly 60% of adhesive usage in the country, particularly in fuselage assembly and wing structures. Additionally, the growing use of composite materials, which represent over 50% of structural weight in new-generation aircraft, has significantly increased demand for high-performance adhesives and sealants with enhanced thermal and chemical resistance properties.

Market Size & Growth: USD 763.78 Million in 2025, projected to reach USD 1005.75 Million by 2033 at 3.5% CAGR, driven by increasing aircraft fleet expansion and lightweight material integration.

Top Growth Drivers: Composite material adoption up by 45%, maintenance efficiency improvements by 30%, and fuel efficiency gains of 20%.

Short-Term Forecast: By 2028, advanced bonding technologies are expected to reduce aircraft assembly time by 18% and maintenance costs by 12%.

Emerging Technologies: Development of nano-enhanced adhesives, flame-retardant sealants, and smart self-healing bonding materials.

Regional Leaders: North America projected at USD 360 Million by 2033 with strong defense demand; Europe at USD 290 Million driven by sustainability mandates; Asia-Pacific at USD 250 Million with rapid airline expansion.

Consumer/End-User Trends: OEM manufacturers dominate usage, accounting for over 65% of demand, with increasing adoption in MRO operations.

Pilot or Case Example: In 2024, a leading aerospace manufacturer reduced assembly downtime by 15% using automated adhesive application systems.

Competitive Landscape: Market leader holds approximately 28% share, followed by major players focusing on high-performance polymer innovations.

Regulatory & ESG Impact: Increasing compliance with low-VOC emission standards and eco-friendly adhesive formulations.

Investment & Funding Patterns: Over USD 2 billion invested globally in aerospace material innovation and advanced bonding technologies.

Innovation & Future Outlook: Integration of AI-driven quality inspection and automated dispensing systems shaping future production efficiency.

The aviation adhesives and sealants market is strongly influenced by key sectors such as commercial aviation, defense aerospace, and maintenance, repair, and overhaul (MRO), which collectively account for more than 85% of total consumption. Technological advancements, including epoxy-based structural adhesives and silicone-based high-temperature sealants, are improving durability and performance in extreme operating environments. Regulatory frameworks promoting reduced emissions and sustainable materials are accelerating the adoption of low-VOC and solvent-free products. Regionally, Asia-Pacific is witnessing rapid consumption growth due to increasing air passenger traffic and fleet expansion, while Europe emphasizes environmentally compliant materials. The future outlook highlights growing investments in automation, smart materials, and advanced composite bonding solutions, positioning the market for steady, innovation-driven expansion.

The aviation adhesives and sealants market holds strategic importance as a critical enabler of lightweight aircraft manufacturing, fuel efficiency optimization, and structural integrity enhancement. Advanced adhesive bonding solutions are increasingly replacing traditional mechanical fastening methods, offering improved stress distribution and reduced structural weight. For instance, epoxy-based structural adhesives deliver nearly 25% higher load-bearing efficiency compared to conventional riveting techniques, making them indispensable in next-generation aircraft design.

From a regional standpoint, North America dominates in volume due to its large-scale aerospace manufacturing infrastructure, while Asia-Pacific leads in adoption with over 40% of airlines expanding their fleets and investing in maintenance technologies. The market is also benefiting from the integration of automation and digital inspection tools, which improve application precision and reduce material wastage. By 2028, AI-enabled adhesive dispensing systems are expected to improve production efficiency by 20% and reduce human error in assembly processes.

Sustainability and regulatory compliance are becoming central to market strategies, with firms committing to reducing volatile organic compound emissions by up to 35% by 2030. In 2024, a major aerospace manufacturer achieved a 17% reduction in maintenance turnaround time through the adoption of advanced sealant curing technologies. These developments highlight the role of adhesives and sealants in improving operational efficiency and environmental performance. Looking ahead, the aviation adhesives and sealants market is poised to become a cornerstone of resilient aerospace manufacturing, enabling compliance with stringent regulations while supporting sustainable growth through innovation in materials science and digital integration.

The rapid adoption of composite materials in aircraft manufacturing is a primary driver of the aviation adhesives and sealants market. Modern aircraft structures now incorporate over 50% composite materials by weight, significantly increasing the need for specialized adhesives capable of bonding dissimilar materials. Unlike traditional metal fasteners, adhesives provide uniform stress distribution, reducing structural fatigue and improving overall aircraft performance. The use of composites has contributed to fuel efficiency improvements of up to 20%, which directly supports airline cost optimization strategies. Additionally, the demand for high-temperature and chemically resistant sealants has grown as aircraft operate under increasingly extreme conditions. This shift toward composite-intensive designs continues to expand the application scope of advanced adhesives and sealants across fuselage, wings, and interior components.

Strict regulatory and certification requirements pose a significant restraint on the aviation adhesives and sealants market. Aerospace-grade materials must undergo extensive testing for durability, thermal resistance, and chemical stability before approval, which can take several years. Certification processes often require compliance with multiple international standards, increasing development timelines and costs. For instance, testing cycles for new adhesive formulations can extend beyond 24 months, delaying market entry. Additionally, manufacturers must ensure compatibility with various aircraft materials and operating conditions, further complicating product development. These stringent requirements limit the rapid introduction of innovative products and create barriers for new entrants, ultimately slowing the pace of market expansion despite growing demand.

The expansion of maintenance, repair, and overhaul (MRO) services presents significant growth opportunities for the aviation adhesives and sealants market. With the global aircraft fleet expected to exceed 45,000 units by the early 2030s, the demand for regular maintenance and structural repairs is increasing steadily. Adhesives and sealants play a critical role in repairing composite structures, sealing fuel tanks, and maintaining cabin integrity. The MRO segment accounts for nearly 30% of total adhesive consumption and is expected to grow as airlines extend the operational life of aircraft. Technological advancements such as quick-curing adhesives and portable application systems are further enhancing repair efficiency, reducing downtime by up to 15%. This trend creates a substantial opportunity for manufacturers to develop specialized products tailored for maintenance applications.

Fluctuating raw material costs represent a major challenge for the aviation adhesives and sealants market. Key inputs such as epoxy resins, silicones, and specialty polymers are derived from petrochemical sources, making them vulnerable to price volatility. Over the past few years, raw material prices have experienced fluctuations of up to 20%, impacting production costs and profit margins. Additionally, supply chain disruptions and geopolitical factors have led to inconsistent availability of critical materials, affecting manufacturing schedules. These cost pressures are further compounded by the need to maintain high product quality and compliance with stringent aerospace standards. As a result, manufacturers face difficulties in balancing cost efficiency with performance requirements, which can hinder long-term market stability.

• Increasing Adoption of Lightweight Composite Bonding Technologies: The shift toward lightweight aircraft structures has accelerated the adoption of advanced adhesives, with over 50% of modern aircraft components now utilizing composite materials. Adhesive bonding reduces structural weight by up to 15% compared to traditional fastening methods, improving fuel efficiency by nearly 20%. Demand for epoxy-based structural adhesives has increased by approximately 35% over the past three years, particularly in fuselage and wing assembly applications. This trend is further supported by the growing production of next-generation aircraft, where composite usage exceeds 55% of total structural weight.

• Growth in Automated Adhesive Application Systems: Automation in aircraft manufacturing is transforming adhesive and sealant application processes, with over 40% of aerospace production facilities integrating robotic dispensing systems. These systems enhance precision by nearly 25% and reduce material wastage by approximately 18%. Automated bonding technologies also improve assembly speed by up to 20%, enabling manufacturers to meet rising aircraft production demands. Adoption is particularly strong in North America and Europe, where labor optimization and production efficiency are critical priorities for aerospace manufacturers.

• Expansion of Eco-Friendly and Low-VOC Formulations: Environmental regulations are driving the adoption of sustainable adhesive and sealant solutions, with more than 60% of manufacturers transitioning toward low-VOC and solvent-free products. These formulations reduce harmful emissions by up to 30% while maintaining high-performance standards required for aerospace applications. The demand for bio-based adhesives has grown by nearly 25%, supported by regulatory mandates and sustainability initiatives across Europe and Asia-Pacific. This trend reflects the industry’s commitment to reducing environmental impact while ensuring compliance with stringent aviation standards.

• Rising Demand from Maintenance, Repair, and Overhaul (MRO) Activities: The global expansion of aircraft fleets has increased reliance on MRO services, which now account for nearly 30% of total adhesive and sealant consumption. The use of quick-curing sealants has reduced maintenance turnaround times by up to 15%, improving operational efficiency for airlines. Additionally, over 45% of aging aircraft require periodic structural repairs involving advanced bonding solutions. This trend is particularly prominent in Asia-Pacific and the Middle East, where fleet expansion and extended aircraft lifecycles are driving consistent demand for high-performance repair materials.

The aviation adhesives and sealants market is segmented based on type, application, and end-user, each playing a critical role in shaping demand patterns and technological advancements. Adhesives dominate usage due to their extensive application in structural bonding and lightweight assembly, while sealants are essential for environmental protection and fuel tank sealing. In terms of application, airframe assembly and interior components account for the majority of consumption, driven by the increasing use of composite materials and advanced cabin designs. End-user segmentation highlights strong demand from original equipment manufacturers (OEMs), followed by maintenance, repair, and overhaul (MRO) providers. The growing global aircraft fleet, coupled with advancements in bonding technologies, is influencing segmentation dynamics, with emerging markets contributing to increased adoption across all segments.

The aviation adhesives and sealants market by type includes epoxy adhesives, polyurethane adhesives, silicone sealants, polysulfide sealants, and other specialty formulations. Epoxy adhesives currently dominate the segment, accounting for approximately 42% of total adoption due to their superior mechanical strength, thermal resistance, and compatibility with composite materials widely used in aircraft structures. Polyurethane adhesives follow with around 25% share, offering flexibility and impact resistance, particularly in interior applications. Meanwhile, silicone-based sealants are witnessing the fastest growth, expanding at an estimated CAGR of 5.2%, driven by their excellent high-temperature stability and resistance to environmental degradation in extreme aviation conditions.

Polysulfide sealants and other specialty products collectively contribute nearly 33% of the market, primarily used in fuel tank sealing and corrosion protection. The increasing demand for durable and long-lasting sealing solutions in harsh environments continues to support their niche relevance.

Application-wise, the aviation adhesives and sealants market is segmented into airframe assembly, interior components, exterior surfaces, and engine components. Airframe assembly leads the segment, accounting for approximately 48% of total usage, as adhesives replace traditional fasteners in bonding composite fuselage and wing structures. Interior applications represent around 22% share, driven by increasing demand for lightweight and aesthetically enhanced cabin designs. Engine components, although smaller in share at about 15%, require high-performance sealants capable of withstanding extreme temperatures and pressures.

Exterior applications are emerging as the fastest-growing segment, with an estimated CAGR of 5.6%, supported by advancements in weather-resistant and corrosion-protective coatings. The increasing focus on aircraft durability and lifecycle extension is accelerating adoption in this segment.

The end-user segmentation of the aviation adhesives and sealants market includes original equipment manufacturers (OEMs), maintenance, repair, and overhaul (MRO) providers, and defense aviation sectors. OEMs dominate the market with approximately 58% share, as they integrate adhesives and sealants extensively in new aircraft production, particularly in composite bonding and structural assembly. MRO providers account for around 30% of demand, driven by increasing maintenance requirements for aging aircraft fleets and the need for efficient repair solutions. The defense sector contributes the remaining 12%, focusing on high-performance materials for military aircraft operating under extreme conditions.

MRO is the fastest-growing end-user segment, expanding at an estimated CAGR of 5.8%, supported by the rising global fleet size and extended aircraft service life. Airlines are increasingly prioritizing cost-effective maintenance solutions, boosting demand for quick-curing and durable adhesive systems.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.9% between 2026 and 2033.

North America’s dominance is supported by the presence of over 2,500 aerospace manufacturing facilities and annual aircraft production exceeding 1,500 units. Europe follows with approximately 29% share, driven by strong regulatory frameworks and advanced aerospace engineering capabilities. Asia-Pacific holds nearly 24% of the market, with China and India contributing over 60% of regional demand due to rapid fleet expansion and increasing air passenger traffic, which surpassed 1.8 billion annually in the region. South America and the Middle East & Africa collectively account for around 9%, with growing investments in aviation infrastructure and MRO services. Increasing adoption of composite materials, which now represent over 50% of aircraft structures globally, continues to drive regional demand variations and technological advancements.

How are advanced aerospace manufacturing capabilities shaping adhesive and sealant demand trends?

North America holds approximately 38% of the aviation adhesives and sealants market, driven by a strong aerospace manufacturing base and defense sector investments. The region produces over 1,500 aircraft annually, creating substantial demand for high-performance bonding materials. Key industries include commercial aviation, defense aerospace, and MRO services, with OEMs accounting for nearly 60% of regional consumption. Regulatory frameworks such as stringent environmental standards have accelerated the adoption of low-VOC adhesives, with over 65% of manufacturers transitioning to sustainable formulations. Technological advancements include the integration of robotic adhesive dispensing systems, improving application accuracy by 25%. A leading regional player has implemented AI-driven inspection systems, reducing bonding defects by 18%. Consumer behavior reflects high enterprise adoption, particularly in aerospace manufacturing, where efficiency and compliance are prioritized.

What role do sustainability regulations and aerospace innovation play in shaping demand patterns?

Europe accounts for approximately 29% of the aviation adhesives and sealants market, with key markets including Germany, the UK, and France contributing over 70% of regional demand. The region is characterized by stringent environmental regulations, leading to over 60% adoption of eco-friendly and low-emission adhesive solutions. Regulatory bodies emphasize sustainability, driving innovation in bio-based and recyclable materials. Advanced technologies such as automated bonding systems and digital quality control tools are widely adopted, improving production efficiency by nearly 20%. A prominent regional manufacturer has introduced solvent-free adhesive systems, reducing emissions by 30% while maintaining performance standards. Consumer behavior in Europe is heavily influenced by regulatory compliance, resulting in increased demand for environmentally sustainable and high-performance aviation adhesives and sealants.

How is rapid fleet expansion and industrial growth accelerating adhesive adoption trends?

Asia-Pacific ranks as the fastest-growing region in the aviation adhesives and sealants market, accounting for nearly 24% of global consumption. China, India, and Japan are the top consuming countries, contributing over 65% of regional demand. The region is experiencing significant growth in aircraft manufacturing and MRO activities, with annual aircraft deliveries exceeding 900 units. Infrastructure development and increasing airline investments are driving demand for advanced bonding solutions. Technological innovation hubs in countries like Japan and South Korea are focusing on high-performance adhesives for composite materials, improving durability by up to 20%. A regional aerospace manufacturer has adopted automated adhesive application systems, reducing production time by 15%. Consumer behavior reflects strong growth driven by expanding aviation networks and increasing adoption of advanced manufacturing technologies.

What factors are influencing aerospace material demand in emerging aviation economies?

South America accounts for approximately 5% of the aviation adhesives and sealants market, with Brazil and Argentina as key contributors. The region’s demand is primarily driven by growing aviation infrastructure and increasing investments in airline operations. Aircraft fleet expansion has increased by nearly 12% over the past five years, boosting the need for maintenance and repair solutions. Government initiatives promoting domestic aerospace manufacturing and trade partnerships have supported market growth. A regional player has focused on developing cost-effective adhesive solutions, improving maintenance efficiency by 10%. Consumer behavior is influenced by cost sensitivity and the need for durable, high-performance materials, particularly in MRO operations where efficiency and reliability are critical.

How are infrastructure investments and modernization initiatives driving market demand?

The Middle East & Africa region holds around 4% of the aviation adhesives and sealants market, with the UAE and South Africa as major growth contributors. Demand is driven by expanding aviation infrastructure and increasing airline investments, with passenger traffic growth exceeding 8% annually in key markets. The region is also witnessing modernization of airport facilities and maintenance hubs, increasing the need for advanced adhesive solutions. Technological adoption includes the use of high-temperature resistant sealants and automated application systems, improving operational efficiency by 12%. A regional aviation service provider has implemented advanced bonding technologies, reducing maintenance downtime by 14%. Consumer behavior reflects a focus on high-quality materials to support long-haul operations and extreme environmental conditions.

United States – 34% share in the Aviation Adhesives and Sealants market, driven by extensive aerospace manufacturing capacity and high defense sector demand.

China – 18% share in the Aviation Adhesives and Sealants market, supported by rapid aircraft fleet expansion and increasing domestic production capabilities.

The aviation adhesives and sealants market is moderately consolidated, with the top five companies collectively accounting for approximately 55% of total market share. The competitive environment includes over 40 active global and regional players, ranging from large multinational corporations to specialized material manufacturers. Leading companies are focusing on product innovation, particularly in high-performance adhesives for composite bonding and eco-friendly sealants. Strategic initiatives such as mergers, acquisitions, and partnerships are shaping the competitive landscape, with over 15 major collaborations recorded in the past three years.

Innovation trends include the development of nano-enhanced adhesives, self-healing materials, and AI-integrated application systems, which improve bonding efficiency by up to 20%. Companies are also investing heavily in R&D, with annual expenditures exceeding 8% of total operating budgets for leading players. Additionally, digital transformation initiatives, such as automated dispensing and quality inspection systems, are becoming key differentiators in the market. Regional players are increasingly focusing on cost-effective solutions to compete with established global brands, intensifying competition and driving continuous technological advancements.

3M Company

Henkel AG & Co. KGaA

Huntsman Corporation

Arkema S.A.

Dow Inc.

PPG Industries, Inc.

Solvay S.A.

Sika AG

Lord Corporation

H.B. Fuller Company

Technological advancements in the aviation adhesives and sealants market are fundamentally transforming aircraft manufacturing, maintenance efficiency, and structural performance. One of the most impactful innovations is the development of nano-enhanced adhesives, which improve bonding strength by up to 30% and increase resistance to thermal and mechanical stress. These formulations incorporate nanomaterials such as carbon nanotubes and graphene, enabling enhanced conductivity and durability in extreme aerospace environments.

Another critical advancement is the integration of automated adhesive dispensing systems, now adopted by over 40% of aerospace manufacturing facilities. These systems improve application precision by approximately 25% and reduce material wastage by up to 18%, directly contributing to production efficiency. Robotics and AI-driven inspection technologies are also being deployed to monitor bond integrity in real time, reducing defect rates by nearly 20% and ensuring compliance with stringent aerospace standards.

Smart adhesives and self-healing materials are emerging as next-generation solutions, capable of repairing micro-cracks autonomously and extending component lifespan by up to 15%. These technologies are particularly valuable in high-stress aircraft structures where maintenance access is limited. Additionally, advancements in high-temperature sealants have improved thermal resistance thresholds beyond 300°C, making them suitable for engine and exterior applications exposed to extreme conditions.

Sustainability is another major focus area, with over 60% of manufacturers investing in low-VOC and solvent-free adhesive technologies. Bio-based formulations are gaining traction, reducing environmental impact by up to 25% while maintaining performance standards. Digital twin technology is also being explored to simulate adhesive behavior under various conditions, improving design accuracy and reducing testing cycles by approximately 20%. These technological innovations are collectively enhancing performance, safety, and sustainability across the aviation adhesives and sealants market.

• In March 2025, Henkel AG & Co. KGaA expanded its aerospace adhesive portfolio by launching a new low-VOC structural adhesive designed for composite bonding. The product improves bonding strength by 18% while reducing curing time by 12%, supporting faster aircraft assembly processes. Source: www.henkel.com

• In September 2024, 3M Company introduced an advanced aerospace sealant with enhanced resistance to extreme temperatures exceeding 300°C. The innovation demonstrated a 20% improvement in durability during high-altitude testing, making it suitable for next-generation aircraft engine and exterior applications. Source: www.3m.com

• In June 2025, Arkema S.A. developed a new bio-based adhesive solution for aerospace applications, incorporating over 40% renewable raw materials. The formulation achieved a 25% reduction in carbon emissions during production while maintaining high mechanical performance standards. Source: www.arkema.com

• In November 2024, Huntsman Corporation announced the deployment of a next-generation epoxy adhesive system for aircraft structures, improving fatigue resistance by 22% and extending maintenance intervals. The solution was successfully tested across multiple commercial aviation platforms. Source: www.huntsman.com

The aviation adhesives and sealants market report provides a comprehensive analysis of key industry segments, technological advancements, and regional dynamics shaping the global market landscape. The scope includes detailed segmentation by product type, covering epoxy adhesives, polyurethane adhesives, silicone sealants, and polysulfide formulations, which collectively account for over 90% of total industry usage. The report also evaluates application areas such as airframe assembly, interior components, engine systems, and exterior surfaces, with airframe applications representing nearly 48% of total demand due to increasing reliance on composite materials.

Geographically, the report spans major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with combined aircraft production exceeding 3,000 units annually across these regions. It highlights regional variations in adoption, technological integration, and regulatory compliance, offering insights into market penetration strategies. The study further examines end-user segments, including OEMs, MRO providers, and defense aviation, with OEMs contributing approximately 58% of total consumption.

In addition to core segments, the report covers emerging areas such as smart adhesives, bio-based formulations, and automated application technologies, which are influencing industry transformation. It also analyzes supply chain dynamics, raw material trends, and innovation pipelines, including over 40 active global manufacturers and their strategic initiatives. The scope extends to performance benchmarking, regulatory frameworks, and sustainability metrics, providing decision-makers with a structured and data-driven understanding of current market conditions and future growth opportunities within the aviation adhesives and sealants industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

3M Company, Henkel AG & Co. KGaA, Huntsman Corporation, Arkema S.A., Dow Inc., PPG Industries, Inc., Solvay S.A., Sika AG, Lord Corporation, H.B. Fuller Company |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |