Reports

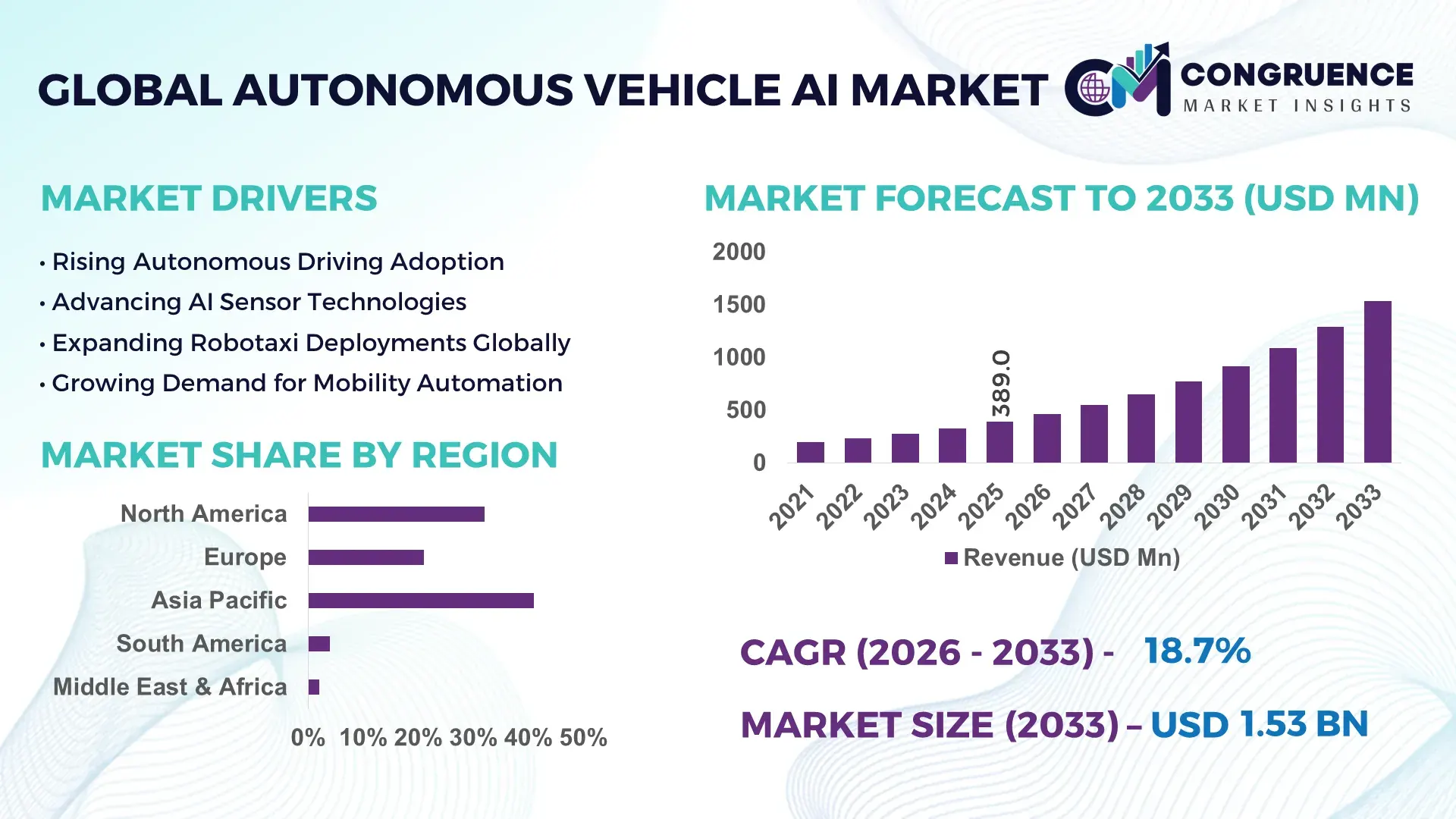

The Global Autonomous Vehicle AI Market was valued at USD 389.0 Million in 2025 and is anticipated to reach a value of USD 1,533.0 Million by 2033 expanding at a CAGR of 18.7% between 2026 and 2033. The market is accelerating as Level 3 and Level 4 autonomous driving deployments expand across passenger mobility, logistics fleets, and commercial transportation networks, while AI-driven perception systems now improve object recognition accuracy by more than 35% compared to earlier rule-based driving architectures. The industry is also benefiting from rapid advancements in edge computing, sensor fusion, and high-performance automotive processors that reduce decision latency by nearly 40%, enabling safer real-time vehicle operations. Between 2024 and 2026, tightening vehicle safety regulations in North America, Europe, and Asia-Pacific, alongside increasing geopolitical competition in semiconductor manufacturing and AI infrastructure, has reshaped autonomous vehicle development priorities. Automotive OEMs are accelerating software-defined vehicle programs while reducing dependency on fragmented supply chains through localized chip sourcing and strategic AI partnerships.

China continues to dominate the global Autonomous Vehicle AI ecosystem with an estimated 34% market share in autonomous testing activity and over 20 major smart-city autonomous mobility zones. More than 65% of advanced robotaxi pilot programs launched across Asia are concentrated in Chinese metropolitan regions, supported by multi-billion-dollar investments in intelligent transportation infrastructure. Compared with North America, China operates significantly larger real-world autonomous driving datasets, exceeding several billion kilometers of recorded driving scenarios annually. Meanwhile, the United States remains a leader in AI algorithm development and autonomous software innovation, accounting for over 40% of advanced autonomous driving patents filed globally. This dual leadership structure is redefining competitive dynamics across the global market.

As AI becomes the primary differentiator in vehicle intelligence rather than hardware capability alone, companies that control autonomous driving data, computing platforms, and scalable software ecosystems are securing the strongest long-term competitive positions.

Market Size & Growth: USD 389.0 Million in 2025 reaching USD 1,533.0 Million by 2033, driven by AI-enabled perception systems, software-defined vehicles, and autonomous logistics expansion.

Top Growth Drivers: Sensor fusion adoption exceeds 42%, autonomous fleet deployment rises 38%, and AI processor integration expands 35% across next-generation vehicles.

Short-Term Forecast: By 2028, autonomous driving computing efficiency improves 45% while real-time processing latency declines nearly 30%.

Emerging Technologies: Generative AI training models, edge AI computing, and multimodal perception systems improve detection precision by over 35%.

Regional Leaders: Asia-Pacific surpasses USD 580 Million, North America exceeds USD 460 Million, and Europe crosses USD 320 Million with smart mobility investments accelerating.

Consumer/End-User Trends: More than 48% of premium vehicle buyers actively prefer advanced autonomous assistance and AI-powered safety functions.

Pilot/Case Example: In 2025, robotaxi deployments improved route efficiency by 27% and reduced idle operating time by 22%.

Competitive Landscape: Top players control nearly 52% of advanced autonomous AI deployments, led by NVIDIA, Alphabet, Tesla, Mobileye, and Baidu.

Regulatory & ESG Impact: Autonomous optimization lowers fleet energy consumption by 18% while advanced safety regulations increase AI integration rates by 31%.

Investment & Funding: Global investments exceed USD 20 Billion, driven by strategic partnerships, semiconductor expansion, and autonomous mobility programs.

Innovation & Future Outlook: End-to-end AI architectures and self-learning driving models are reducing software training cycles by nearly 40%.

Autonomous Vehicle AI adoption is increasingly concentrated across passenger transportation, logistics, and smart mobility ecosystems, which collectively account for more than 70% of operational deployments. Advanced perception software now contributes nearly 45% of autonomous decision-making capability, while edge AI processors reduce response latency by approximately 30%. Demand remains strongest across Asia-Pacific and North America as governments accelerate intelligent transportation initiatives. Simultaneously, regulatory standardization and localized semiconductor manufacturing are reshaping deployment strategies, positioning scalable AI-driven vehicle platforms as the next competitive frontier for automotive and mobility leaders.

Autonomous Vehicle AI is rapidly transforming from an experimental automotive capability into a core strategic asset that determines future competitiveness across transportation, logistics, defense mobility, and intelligent infrastructure ecosystems. As software increasingly defines vehicle value, manufacturers, technology providers, and mobility operators are shifting capital allocation toward AI-driven autonomy platforms capable of delivering scalable operational intelligence. The competitive landscape is accelerating as companies race to secure proprietary driving datasets, advanced AI chips, and high-performance software stacks that enable real-world autonomous deployment.

Simultaneously, semiconductor localization efforts, stricter vehicle safety mandates, and growing geopolitical competition around AI infrastructure are forcing automotive companies to restructure supply chains and prioritize vertically integrated technology strategies. End-to-end autonomous driving AI improves processing efficiency by nearly 45% while reducing computing costs by approximately 30% compared to legacy modular autonomous systems, enabling faster deployment and lower operating complexity.

Asia-Pacific leads in deployment volume with more than 40% of global autonomous testing programs, while North America leads in software innovation and advanced AI platform adoption with nearly 37% of global autonomous technology investments. Over the next three years, commercial autonomous fleet utilization rates are expected to increase by more than 28%, while real-time AI decision accuracy continues improving through larger-scale training datasets and advanced simulation environments.

ESG performance is becoming a measurable competitive advantage, with AI-optimized fleet operations reducing fuel consumption and operational emissions by approximately 15%. In a recent autonomous logistics pilot, route optimization algorithms improved delivery efficiency by 24% while reducing vehicle idle time by 19%, demonstrating immediate operational value. Industry leaders are aggressively expanding AI development centers, increasing semiconductor partnerships, and investing in autonomous mobility ecosystems to secure long-term market leadership. The companies that successfully integrate AI software, vehicle platforms, and intelligent transportation infrastructure will define the next generation of global mobility and capture disproportionate competitive advantage as autonomous transportation becomes mainstream.

The Autonomous Vehicle AI Market is undergoing a structural transformation driven by the convergence of artificial intelligence, high-performance computing, advanced sensors, and connected mobility infrastructure. Market dynamics are increasingly shaped by the race to improve autonomous decision-making accuracy, reduce operational risk, and accelerate commercialization across passenger vehicles, logistics fleets, and urban mobility platforms. AI-enabled perception systems, predictive analytics, and real-time environmental mapping are becoming central differentiators among vehicle manufacturers and technology providers. At the same time, growing regulatory scrutiny, cybersecurity requirements, and semiconductor supply constraints continue influencing deployment timelines. Strategic alliances between automotive OEMs, cloud providers, semiconductor companies, and autonomous software developers are accelerating ecosystem expansion. As intelligent transportation initiatives gain momentum globally, companies are increasingly focusing on scalable AI architectures, simulation-based training environments, and software-defined vehicle platforms to strengthen market positioning and operational efficiency.

The primary growth engine of the Autonomous Vehicle AI Market is the rapid advancement of AI-powered perception, prediction, and decision-making systems that significantly improve autonomous driving performance. Advanced neural network architectures now enhance object recognition accuracy by over 35%, while sensor fusion technologies improve environmental awareness by nearly 30% across complex driving conditions. The global shift toward software-defined vehicles is further accelerating AI integration, enabling continuous over-the-air system optimization and performance upgrades. The semiconductor localization movement triggered by global supply chain restructuring has intensified investment in automotive AI chips and edge computing infrastructure. In response, automotive manufacturers are expanding AI development capabilities and establishing strategic partnerships with semiconductor and cloud computing providers. More than 50% of leading autonomous mobility programs now prioritize proprietary AI software development to strengthen competitive differentiation. This shift is accelerating deployment readiness, improving vehicle intelligence, and redefining future transportation ecosystems.

Despite significant technological progress, infrastructure readiness remains a major constraint limiting widespread autonomous vehicle deployment. Advanced autonomous systems require high-performance computing platforms that increase onboard processing costs by approximately 25% compared to conventional vehicle electronics. In addition, autonomous driving systems generate massive volumes of data, requiring substantial cloud processing, storage, and validation resources. Regulatory fragmentation across regions continues creating deployment complexity, with testing requirements differing significantly between North America, Europe, and Asia-Pacific. Autonomous validation cycles can extend development timelines by nearly 20%, delaying commercialization efforts and increasing operational costs. Furthermore, advanced semiconductor concentration within limited global manufacturing hubs exposes companies to supply disruptions and component shortages. To mitigate these risks, manufacturers are diversifying semiconductor sourcing, increasing simulation-based testing programs, and adopting modular AI architectures that reduce infrastructure dependency. Companies are also pursuing long-term supplier agreements and localized manufacturing strategies to improve operational resilience and deployment scalability.

The strongest market opportunities are emerging within autonomous logistics, robotaxi services, industrial transportation, and smart-city mobility infrastructure. AI-enabled fleet optimization systems improve route efficiency by more than 25%, creating significant cost advantages for logistics operators managing large-scale transportation networks. Simultaneously, urban mobility platforms are accelerating autonomous shuttle and robotaxi deployment programs across high-density metropolitan regions.Advanced generative AI training environments are reducing autonomous model development cycles by approximately 35%, enabling faster deployment and more efficient scenario validation. Emerging markets are increasingly investing in intelligent transportation systems, creating new demand centers for autonomous vehicle AI technologies. More than 40% of planned smart mobility infrastructure projects now include autonomous transportation integration components. Technology providers are responding through aggressive R&D investment, ecosystem partnerships, and expansion of autonomous simulation platforms. Companies that establish integrated software, infrastructure, and mobility ecosystems are positioning themselves to capture long-term market leadership as autonomous transportation networks become increasingly interconnected and scalable.

The most significant challenge facing the Autonomous Vehicle AI Market is achieving consistent real-world performance across diverse environments while maintaining regulatory compliance and operational safety. Autonomous systems must process millions of driving scenarios with near-perfect reliability, yet performance variability remains a critical concern across unpredictable weather conditions, complex urban environments, and mixed traffic ecosystems. Advanced validation requirements can account for nearly 30% of total autonomous development timelines, while cybersecurity protection requirements continue expanding as connected vehicle ecosystems grow. Public trust also remains a critical adoption barrier, with consumer confidence levels varying significantly across regions despite measurable improvements in system performance. The increasing complexity of AI model training, data labeling, and software verification is forcing companies to invest heavily in simulation platforms, digital twins, and safety validation frameworks. To remain competitive, organizations must optimize infrastructure investments, strengthen cross-industry partnerships, and continuously improve AI explainability, reliability, and scalability. Long-term market leadership will depend on successfully balancing technological innovation with operational safety, regulatory compliance, and deployment efficiency.

42% Increase in End-to-End AI Architecture Adoption Reshaping Vehicle Software Development. Automotive manufacturers are replacing modular autonomous stacks with unified end-to-end AI models, reducing software integration complexity by nearly 30% and improving real-time decision accuracy by 25%. Companies are expanding AI training infrastructure and simulation environments to accelerate deployment cycles while optimizing software-defined vehicle performance.

35% Growth in Edge AI Computing Deployment Optimizing Real-Time Processing. Advanced automotive AI processors are reducing perception latency by approximately 28% while improving onboard computing efficiency by 33%. Semiconductor localization initiatives and supply chain diversification efforts are forcing companies to redesign computing architectures around energy-efficient edge processing rather than cloud-dependent decision systems.

31% Expansion in Autonomous Fleet Operations Redefining Commercial Mobility Models. Logistics providers and mobility operators are scaling autonomous fleet programs, increasing vehicle utilization rates by 22% and lowering idle operating time by 18%. Companies are restructuring fleet management strategies around AI-driven predictive maintenance and dynamic routing systems to maximize operational efficiency.

27% Rise in Strategic Mobility Ecosystem Partnerships Accelerating Deployment Execution. Automotive OEMs, semiconductor manufacturers, and cloud technology providers are expanding collaborative development programs to shorten validation timelines by nearly 20%. A non-obvious shift is emerging as transportation infrastructure providers increasingly participate in autonomous ecosystem development, reshaping how intelligent mobility networks are deployed and managed.

The Autonomous Vehicle AI Market is segmented across technology types, operational applications, and end-user deployment categories, reflecting the industry's transition from experimental autonomy toward scalable commercial implementation. Demand remains heavily concentrated in advanced perception, machine learning, and decision-making platforms that collectively account for more than 60% of AI integration activity. Application demand is increasingly shifting toward autonomous passenger mobility, logistics automation, and fleet intelligence solutions as operators prioritize efficiency and safety optimization. End-user adoption remains strongest among automotive manufacturers and mobility service providers, although commercial fleet operators are rapidly expanding implementation initiatives. More than 45% of new autonomous development programs now prioritize integrated AI ecosystems rather than standalone software solutions. This shift is driving greater investment in scalable computing architectures, intelligent transportation infrastructure, and autonomous mobility platforms, reinforcing the strategic importance of AI as the core operating layer of next-generation transportation systems.

The market is primarily segmented into Machine Learning, Computer Vision, Natural Language Processing, and Context-Aware Computing technologies. Computer Vision dominates the market with approximately 38% share due to its foundational role in object detection, lane recognition, pedestrian identification, and real-time environmental mapping. Its integration across nearly all autonomous driving architectures makes it the most critical operational technology segment. Machine Learning represents the fastest-expanding segment, with adoption growth exceeding 32% as autonomous systems increasingly rely on predictive analytics, behavioral modeling, and adaptive decision-making capabilities. The contrast between Computer Vision and Machine Learning highlights the market's transition from perception-focused autonomy toward predictive intelligence and autonomous reasoning. Meanwhile, Natural Language Processing and Context-Aware Computing collectively account for nearly 27% of market deployment activity, supporting advanced human-machine interaction and situational awareness functions. Companies are accelerating investment in integrated AI stacks that combine multiple technologies rather than relying on isolated solutions. As autonomous systems evolve toward higher autonomy levels, demand is shifting from perception-centric architectures toward adaptive intelligence platforms capable of continuous learning and contextual decision-making, making Machine Learning a key strategic investment area.

The Autonomous Vehicle AI Market is segmented across Passenger Vehicles, Commercial Vehicles, Robotaxis, Logistics & Delivery Vehicles, and Industrial Autonomous Mobility applications. Passenger Vehicles maintain the leading position with approximately 41% market share due to large-scale integration of advanced driver assistance systems and autonomous driving features across premium and next-generation vehicle platforms. However, Logistics & Delivery Vehicles represent the fastest-expanding application segment, with deployment growth exceeding 34% as operators seek efficiency gains, labor optimization, and route automation benefits. Passenger Vehicle deployments emphasize safety enhancement and consumer convenience, while Logistics & Delivery Vehicles prioritize operational efficiency and fleet productivity. Robotaxi deployments are also expanding rapidly across major metropolitan regions, contributing to the growing shift toward mobility-as-a-service models. Commercial Vehicles and Industrial Autonomous Mobility applications collectively account for nearly 33% of deployment activity, supported by increasing automation initiatives across transportation and industrial operations. Companies are repositioning product strategies toward scalable commercial deployments where measurable productivity gains justify investment. Demand is increasingly moving toward high-utilization operational environments where autonomous AI delivers direct cost and efficiency advantages.

Automotive OEMs represent the largest end-user segment with approximately 44% share, driven by large-scale investment in autonomous platform development, software-defined vehicle architectures, and integrated AI ecosystems. Their dominant position reflects direct control over vehicle design, autonomous software integration, and commercialization strategies. Mobility Service Providers are emerging as the fastest-growing end-user category, with adoption growth exceeding 36% as autonomous ride-hailing, robotaxi, and shared mobility programs accelerate globally. The contrast between Automotive OEMs and Mobility Service Providers reflects a shift from vehicle manufacturing toward service-oriented autonomous ecosystems. Fleet Operators and Logistics Companies collectively account for nearly 31% of market demand, driven by operational efficiency requirements, predictive maintenance adoption, and route optimization initiatives. Technology companies are increasingly tailoring solutions through strategic partnerships, platform customization, and scalable subscription-based deployment models. Purchasing decisions are increasingly influenced by software scalability, AI performance, and operational cost reduction rather than hardware capability alone. Future demand is shifting toward ecosystem-based deployments where AI platforms, fleet operations, and mobility services operate within integrated intelligent transportation networks.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 19.4% between 2026 and 2033.

Asia-Pacific leads global autonomous vehicle AI deployment volume due to large-scale manufacturing capacity, smart-city mobility investments, and aggressive autonomous testing programs across China, Japan, and South Korea. North America accounts for nearly 32% of market demand and remains the innovation hub for autonomous software, AI computing platforms, and robotaxi ecosystems. Europe holds approximately 21% share, driven by regulatory-led vehicle intelligence adoption and advanced mobility safety standards. Semiconductor localization initiatives, AI infrastructure expansion, and transportation digitalization programs are reshaping regional competitiveness. While Asia-Pacific dominates scale, North America leads AI innovation intensity and Europe leads compliance-driven deployment, pushing companies to expand globally through regionalized technology, supply chain, and mobility strategies.

North America represents nearly 32% of global Autonomous Vehicle AI demand, supported by large-scale robotaxi programs, autonomous logistics expansion, and software-defined vehicle adoption. The United States remains the primary innovation center, accounting for more than 40% of global autonomous driving patent activity and advanced AI model development. Regulatory support for autonomous testing and AI infrastructure investment is accelerating deployment readiness across commercial mobility networks. Companies are increasingly adopting end-to-end AI driving systems, reducing perception-processing latency by approximately 28%. Strategic investment activity remains strong, with autonomous fleet deployments increasing more than 30% across major metropolitan regions. Enterprise buyers prioritize scalability, software reliability, and operational efficiency, making North America a critical market for AI platform providers seeking technology leadership and large-scale commercialization.

Europe accounts for approximately 21% of the Autonomous Vehicle AI Market, led by Germany, France, and the United Kingdom. Strict vehicle safety regulations, emissions targets, and digital mobility frameworks are accelerating adoption of AI-powered autonomous technologies. More than 46% of advanced vehicle development programs across the region now integrate AI-enabled safety and predictive driving functions. Compliance requirements are pushing manufacturers toward high-accuracy perception systems and intelligent driver monitoring technologies that improve operational safety by nearly 25%. Automotive companies are expanding autonomous validation facilities and AI simulation capabilities to meet increasingly complex certification requirements. Enterprise buyers prioritize regulatory compliance, system transparency, and operational reliability, forcing technology providers to innovate faster and making Europe a key region for next-generation autonomous mobility standardization.

Asia-Pacific leads the Autonomous Vehicle AI Market with approximately 41% share and remains the largest deployment region globally. China, Japan, and South Korea dominate regional activity through strong automotive production capacity, intelligent transportation investments, and advanced semiconductor ecosystems. More than 60% of large-scale autonomous pilot programs across the global market are concentrated within Asia-Pacific. Regional manufacturers are accelerating localized AI chip production and autonomous software integration, reducing deployment costs by nearly 20% compared to import-dependent models. Autonomous mobility infrastructure projects continue expanding across urban transportation networks, while commercial fleet operators increasingly prioritize speed, scalability, and cost optimization. For global companies, Asia-Pacific remains the most important region for production scale, autonomous testing volume, and long-term deployment expansion.

South America contributes approximately 4% of global Autonomous Vehicle AI demand, with Brazil and Argentina leading regional adoption initiatives. Demand is primarily concentrated in logistics optimization, commercial transportation, and urban mobility modernization programs. However, infrastructure limitations and uneven regulatory frameworks continue constraining large-scale autonomous deployment. More than 55% of regional investment activity remains focused on fleet efficiency and intelligent transportation upgrades rather than full autonomy programs. Companies are increasingly deploying AI-assisted driving technologies that improve route productivity by nearly 18% while lowering operational inefficiencies. Enterprise buyers remain highly price-sensitive, prioritizing practical cost reduction over advanced autonomy capabilities. The region presents attractive long-term growth opportunities, but successful expansion requires localized deployment models and infrastructure-focused investment strategies.

The Middle East & Africa region accounts for approximately 2% of global Autonomous Vehicle AI activity but is rapidly strengthening its strategic position through infrastructure modernization and smart mobility initiatives. The United Arab Emirates and Saudi Arabia are leading autonomous transportation investments, particularly across urban mobility, logistics, and intelligent city development programs. More than 35% of regional smart-city projects now incorporate AI-enabled transportation technologies. Governments and enterprise operators are expanding autonomous mobility pilots to improve operational efficiency and reduce transportation bottlenecks. Infrastructure investments continue accelerating, with several large-scale autonomous testing corridors under development. Organizations increasingly favor advanced mobility platforms that combine operational intelligence with long-term infrastructure scalability, making the region an emerging strategic destination for future autonomous transportation deployment.

China – 34% Market share: Supported by large-scale autonomous testing zones, smart-city mobility investments, and extensive autonomous driving data generation capabilities.

United States – 29% Market share: Driven by advanced AI software innovation, robotaxi deployment leadership, and strong autonomous vehicle ecosystem development.

The Autonomous Vehicle AI Market is defined by intense competition between AI platform leaders, automotive OEMs, autonomous driving specialists, and semiconductor innovators. Major players including NVIDIA, Tesla, Alphabet (Waymo), Mobileye, Baidu, and Qualcomm collectively control nearly 52% of advanced autonomous AI deployment activity. Competition is increasingly centered on AI computing performance, autonomous driving accuracy, training data scale, and software ecosystem integration rather than vehicle hardware alone.

Technology leaders are competing through vertically integrated AI stacks that improve perception efficiency by over 30%, while semiconductor providers focus on reducing processing latency by nearly 28%. Automotive manufacturers are strengthening partnerships with AI software firms and chip developers to accelerate commercialization timelines. The market is rapidly shifting toward end-to-end autonomous architectures, forcing companies to expand simulation capabilities, data infrastructure, and AI training environments.

Strategic alliances, autonomous fleet expansion, AI model optimization, and localized semiconductor sourcing are becoming primary competitive weapons. High validation costs, safety certification requirements, and access to large-scale driving datasets remain significant barriers to entry. Winning in this market increasingly depends on controlling autonomous data ecosystems, AI compute platforms, and scalable software deployment networks rather than traditional automotive manufacturing strength alone.

Tesla

Waymo

Mobileye

Baidu

Qualcomm

Aurora Innovation

Pony.ai

WeRide

Zoox

Nuro

Motional

Wayve

Autonomous Vehicle AI technology is rapidly shifting toward end-to-end neural driving architectures that integrate perception, prediction, planning, and control within a unified AI framework. These systems improve decision accuracy by nearly 35% while reducing software complexity by approximately 25% compared with legacy modular autonomous stacks. More than 45% of advanced autonomous development programs now prioritize end-to-end AI training models due to their scalability and ability to process real-world driving variability.

Edge AI computing is emerging as a critical competitive technology layer. Advanced automotive AI processors reduce perception latency by nearly 30% while improving onboard processing efficiency by over 33%. Adoption of edge-based autonomous computing has surpassed 40% across next-generation autonomous testing programs, allowing real-time vehicle intelligence without excessive cloud dependency. Companies controlling high-performance AI compute ecosystems are gaining substantial deployment advantages.

Another disruptive trend is the expansion of synthetic data generation and AI simulation environments. Advanced simulation platforms reduce validation timelines by approximately 28% while enabling autonomous systems to train across millions of virtual driving scenarios. This capability is becoming essential as companies attempt to solve rare edge-case driving conditions more efficiently.

Between 2026 and 2028, multimodal AI models, physical AI systems, and self-learning autonomous architectures will increasingly redefine vehicle intelligence. Companies with access to large-scale driving datasets, simulation ecosystems, and proprietary AI chips will secure stronger competitive positioning as autonomous mobility transitions from pilot deployments toward commercial-scale operations.

January 2026 – Mobileye announced the acquisition of Mentee Robotics to strengthen physical AI capabilities across autonomous vehicles and robotics. The deal expanded Mobileye’s automotive pipeline by more than 40% compared to 2023 levels, accelerating autonomous intelligence development and commercialization plans. [Physical AI Expansion] Source: www.mobileye.com

October 2025 – NVIDIA partnered with Uber, Mercedes-Benz, Stellantis, and Lucid to accelerate Level 4 autonomous vehicle deployment. Uber targeted scaling up to 100,000 autonomous vehicles globally beginning in 2027, significantly strengthening robotaxi ecosystem expansion and AI infrastructure integration. [Robotaxi Scale-Up]

April 2026 – Mobileye reported a 27% year-over-year increase in first-quarter revenue while advancing its VW ID.Buzz robotaxi ecosystem and securing new autonomous platform design wins. The development reinforced demand momentum for advanced AI-enabled driving systems and fleet autonomy solutions. [Platform Execution]

May 2026 – Waymo launched passenger operations for its sixth-generation Ojai robotaxi platform across multiple U.S. cities. The vehicle uses a reduced yet more capable sensor architecture designed for large-scale deployment, improving production efficiency while expanding autonomous mobility service capacity. [Fleet Modernization]

The Autonomous Vehicle AI Market Report delivers comprehensive coverage across core technology segments, operational applications, end-user categories, and regional deployment ecosystems shaping the future of intelligent transportation. The report evaluates Machine Learning, Computer Vision, Natural Language Processing, and Context-Aware Computing technologies while assessing demand patterns across passenger vehicles, commercial transportation, robotaxis, logistics fleets, and industrial autonomous mobility systems. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing detailed regional positioning and competitive intelligence.

The report analyzes more than 10 major industry participants and multiple autonomous deployment categories, covering adoption intensity, market share positioning, infrastructure readiness, and technology integration trends. Over 45% of current autonomous development programs are focused on scalable AI ecosystems, while nearly 40% prioritize advanced edge computing and real-time decision intelligence. Special attention is given to emerging areas including physical AI, autonomous simulation platforms, end-to-end neural driving models, and software-defined vehicle architectures.

From a strategic perspective, the report supports investment planning, market expansion, competitive benchmarking, partnership evaluation, and technology positioning decisions. It provides forward-looking coverage of deployment pathways, ecosystem shifts, and innovation priorities expected to influence autonomous mobility development between 2026 and 2033, enabling decision-makers to identify high-impact growth opportunities and competitive advantage areas with greater precision.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 389.0 Million |

| Market Revenue (2033) | USD 1,533.0 Million |

| CAGR (2026–2033) | 18.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | NVIDIA; Tesla; Waymo; Mobileye; Baidu; Qualcomm; Aurora Innovation; Pony.ai; WeRide; Zoox; Nuro; Motional; Wayve |

| Customization & Pricing | Available on Request (10% Customization Free) |