Reports

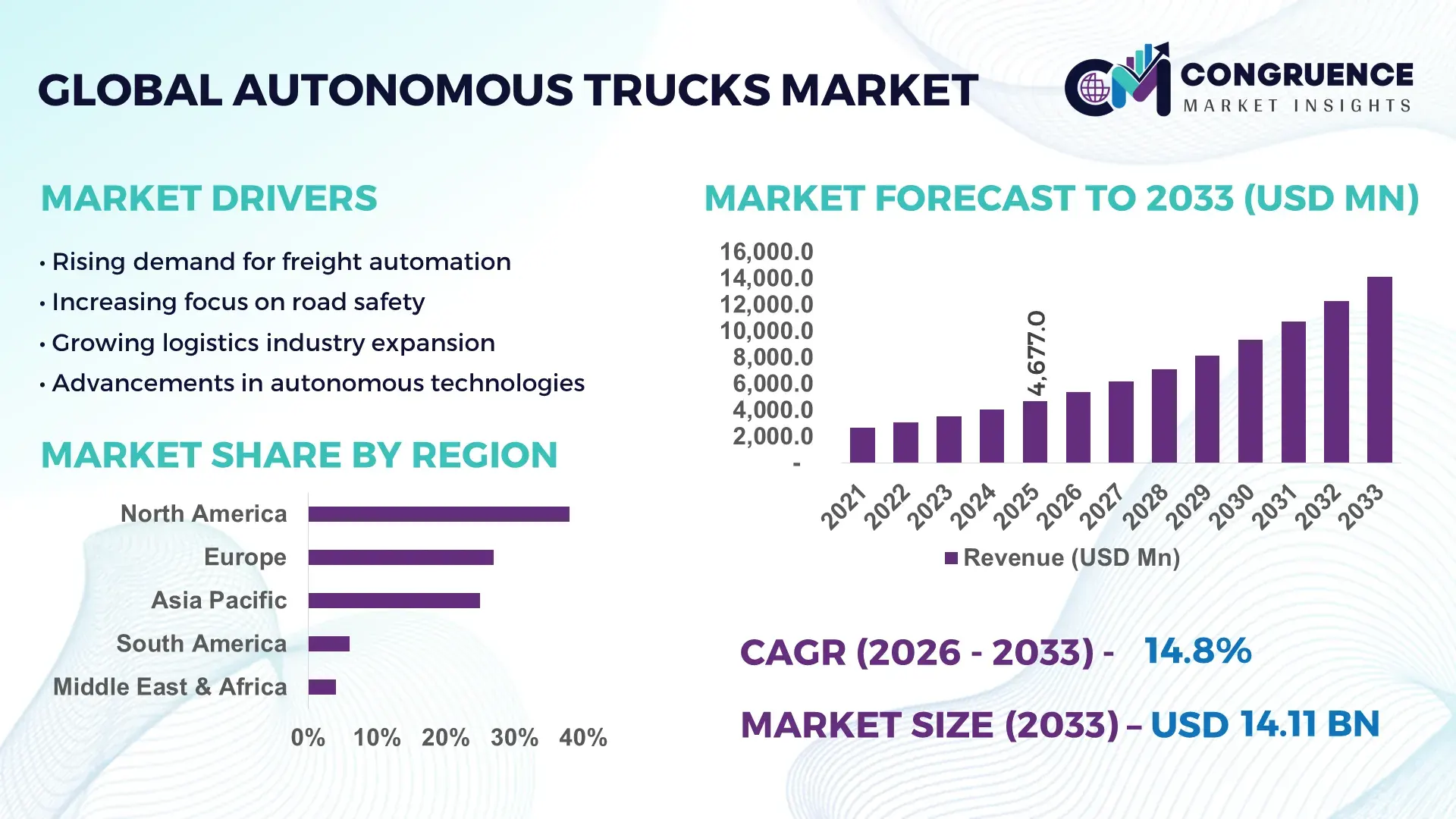

The Global Autonomous Trucks Market was valued at USD 4,677.0 Million in 2025 and is anticipated to reach a value of USD 14,109.2 Million by 2033 expanding at a CAGR of 14.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by increasing demand for cost-efficient freight transportation and advancements in AI-based driving systems.

The United States plays a pivotal role in the Autonomous Trucks Market with over 35% of global pilot deployments concentrated across key freight corridors such as Texas and California. More than 65% of logistics companies in the country have initiated autonomous fleet trials, with over 12,000 autonomous-enabled trucks tested across highways by 2025. Investment levels exceed USD 5 billion annually in autonomous mobility technologies, with applications spanning long-haul freight, mining logistics, and port operations. Additionally, over 40% of warehouse-to-hub deliveries in major logistics hubs incorporate semi-autonomous driving features, reflecting strong industrial integration and technological maturity.

Market Size & Growth: USD 4,677.0 Million in 2025, projected to reach USD 14,109.2 Million by 2033 at 14.8% CAGR, driven by logistics automation demand.

Top Growth Drivers: Fleet automation adoption (~48%), fuel efficiency gains (~22%), driver shortage mitigation (~35%).

Short-Term Forecast: By 2028, logistics cost reduction expected by 18% due to autonomous fleet integration.

Emerging Technologies: AI-based perception systems, LiDAR advancements, V2X communication integration.

Regional Leaders: North America (~USD 5.8 Billion by 2033), Asia-Pacific (~USD 4.6 Billion), Europe (~USD 3.1 Billion) with varying adoption trends.

Consumer/End-User Trends: Logistics firms and e-commerce companies account for over 55% adoption due to high delivery frequency.

Pilot or Case Example: In 2025, a US-based logistics pilot reduced fuel consumption by 12% and delivery time by 9%.

Competitive Landscape: Market leader holds ~18% share, followed by 4–5 major competitors focusing on AI integration.

Regulatory & ESG Impact: Emission reduction policies driving adoption with ~20% fleet electrification mandates.

Investment & Funding Patterns: Over USD 12 Billion invested globally in autonomous mobility ventures since 2023.

Innovation & Future Outlook: Integration of electric and autonomous trucks expected to reshape fleet economics.

Autonomous trucks are increasingly adopted across logistics (52%), mining (18%), and construction (11%) sectors, supported by AI-driven navigation and real-time fleet optimization. Regulatory frameworks promoting emission reductions and driver safety are accelerating adoption. North America leads consumption, while Asia-Pacific shows rapid infrastructure expansion. Advancements in LiDAR and 5G connectivity are enhancing operational precision, positioning autonomous trucking as a critical enabler of future smart logistics ecosystems.

The Autonomous Trucks Market holds strategic relevance as global supply chains prioritize efficiency, safety, and cost optimization. Autonomous driving systems leveraging advanced AI and sensor fusion technologies are enabling logistics providers to achieve operational improvements exceeding 25% in route efficiency. Compared to traditional manually driven trucks, AI-enabled autonomous navigation delivers nearly 30% improvement in fuel optimization and reduces idle time significantly. This transformation is particularly critical for industries such as e-commerce, mining, and manufacturing, where delivery precision and turnaround time are key performance indicators.

North America dominates in volume, while Asia-Pacific leads in adoption with over 42% of logistics enterprises actively testing or deploying autonomous truck solutions. Governments across regions are introducing regulatory sandboxes and safety frameworks, allowing faster commercialization of Level 4 and Level 5 autonomous vehicles. By 2028, edge AI and real-time data analytics are expected to improve fleet utilization rates by 20%, reducing empty miles and enhancing profitability for logistics operators.

Sustainability goals are also shaping the market trajectory, with firms committing to reducing fleet emissions by up to 30% by 2030 through the integration of electric autonomous trucks. In 2025, a major logistics operator in the United States achieved a 15% reduction in operational costs by deploying AI-enabled route optimization systems combined with semi-autonomous trucking technologies.

Looking ahead, the Autonomous Trucks Market is positioned as a critical pillar for resilient, technology-driven, and sustainable logistics infrastructure. Its integration with smart transportation networks, digital supply chains, and ESG-driven strategies will continue to redefine freight mobility and long-term industry competitiveness.

The Autonomous Trucks Market is influenced by rapid technological advancements, evolving regulatory frameworks, and growing demand for efficient logistics solutions. Increasing integration of artificial intelligence, machine learning, and sensor-based technologies is enabling higher levels of automation in freight transportation. Industry players are focusing on reducing operational costs, improving delivery timelines, and enhancing safety standards. Additionally, the expansion of e-commerce and global trade is driving demand for autonomous logistics systems capable of handling high volumes with minimal human intervention. Infrastructure development, including smart highways and connected transportation systems, further supports market expansion. However, regulatory inconsistencies across regions and high initial deployment costs remain significant considerations for stakeholders. Overall, the market is undergoing a transition from pilot testing to early commercialization, supported by strategic collaborations between automotive manufacturers, technology providers, and logistics companies.

The increasing demand for logistics automation is a key driver of the Autonomous Trucks Market. Over 60% of global logistics companies are investing in automation technologies to enhance operational efficiency and reduce human dependency. Autonomous trucks enable continuous operations, reducing delivery times by up to 20% compared to traditional trucking systems. Additionally, driver shortages—estimated to impact over 2 million positions globally—are accelerating adoption of autonomous solutions. Automation also improves fuel efficiency by approximately 10–15% through optimized driving patterns and route planning. Large-scale logistics providers are deploying autonomous trucks for long-haul routes, where consistent speeds and minimal interruptions lead to measurable productivity gains. The integration of AI-driven fleet management systems further enhances route optimization, reduces idle time, and increases overall asset utilization, making autonomous trucking a critical component of modern supply chain strategies.

High infrastructure and deployment costs remain a major restraint for the Autonomous Trucks Market. The development and integration of advanced sensors, LiDAR systems, high-performance computing units, and AI software significantly increase the upfront cost of autonomous trucks, often exceeding 40% higher than conventional vehicles. Additionally, the need for specialized infrastructure such as smart highways, dedicated lanes, and advanced communication networks adds to the overall investment burden. Maintenance costs are also elevated due to the complexity of autonomous systems and the need for regular calibration and software updates. Smaller logistics companies face challenges in adopting these technologies due to limited capital resources. Furthermore, insurance and liability concerns associated with autonomous driving systems contribute to increased operational costs, limiting widespread adoption, particularly in emerging economies where infrastructure readiness is still developing.

The integration of autonomous trucks with electric vehicle technology presents significant opportunities for market expansion. Electric autonomous trucks can reduce fuel costs by up to 35% while simultaneously lowering emissions, aligning with global sustainability goals. Governments worldwide are offering incentives and subsidies to promote electric vehicle adoption, encouraging logistics companies to transition toward cleaner and more efficient transportation solutions. Additionally, the combination of autonomous driving and electrification enables optimized energy consumption through predictive route planning and regenerative braking systems. Industries such as mining and port logistics are increasingly adopting electric autonomous trucks to improve operational efficiency and reduce environmental impact. The growing availability of charging infrastructure and advancements in battery technology further support the adoption of electric autonomous trucks, creating a strong foundation for long-term growth in the market.

Regulatory and safety concerns pose significant challenges to the Autonomous Trucks Market. Different countries have varying standards and regulations regarding autonomous vehicle testing and deployment, creating complexity for manufacturers and logistics providers. Safety validation of autonomous systems requires extensive testing, often exceeding millions of miles, to ensure reliability under diverse driving conditions. Public concerns regarding accident risks and cybersecurity threats also hinder acceptance of autonomous trucks. Additionally, liability issues in case of accidents involving autonomous vehicles remain unclear in many jurisdictions, complicating insurance frameworks. Data security is another critical challenge, as autonomous trucks rely heavily on real-time data exchange, making them vulnerable to cyberattacks. These challenges necessitate robust regulatory frameworks, advanced safety protocols, and continuous technological improvements to build trust and enable large-scale adoption.

• Increased deployment of Level 4 autonomy in logistics fleets: Over 38% of newly tested autonomous trucks in 2025 operate at Level 4 autonomy, enabling fully driverless operations in controlled environments. Fleet operators report up to 22% improvement in delivery consistency and a 17% reduction in operational delays, especially across long-haul freight corridors.

• Expansion of autonomous trucking in mining and industrial sectors: Approximately 28% of global mining operations have adopted autonomous haul trucks, improving productivity by 20% and reducing operational downtime by 15%. Industrial logistics hubs are also integrating automation to streamline bulk material transport processes.

• Integration of 5G connectivity and V2X communication systems: Around 45% of autonomous truck pilots now utilize 5G-enabled communication, enhancing real-time data exchange and reducing latency by nearly 30%. This advancement improves navigation accuracy and enables safer interaction with surrounding vehicles and infrastructure.

• Growth in electric autonomous truck deployments: Nearly 32% of newly deployed autonomous trucks in 2025 are electric-powered, contributing to a 25% reduction in emissions compared to diesel counterparts. Logistics companies are increasingly combining electrification with automation to achieve sustainability targets and reduce operating costs.

The Autonomous Trucks Market is segmented based on type, application, and end-user, each contributing uniquely to market expansion. Different levels of autonomy define product segmentation, while applications span across logistics, mining, and construction sectors. End-users include logistics companies, industrial operators, and government entities. Adoption patterns vary significantly across regions and industries, with logistics dominating due to high freight demand. Mining and industrial applications are gaining traction due to their controlled environments, enabling faster deployment of autonomous systems. Increasing digitalization and infrastructure development are further supporting segmentation growth, with companies focusing on tailored solutions to meet specific operational needs.

The Autonomous Trucks Market is categorized into semi-autonomous trucks and fully autonomous trucks. Semi-autonomous trucks currently dominate the market, accounting for approximately 62% of total adoption due to their compatibility with existing infrastructure and lower deployment complexity. These systems provide driver assistance features such as adaptive cruise control, lane-keeping, and collision avoidance, making them suitable for gradual transition toward full autonomy. Fully autonomous trucks represent the fastest-growing segment, expected to expand at a CAGR of 18.5% due to advancements in AI, LiDAR, and sensor fusion technologies. These trucks operate without human intervention in predefined environments, significantly improving operational efficiency and reducing labor dependency. Other niche segments, including remote-operated and platooning-enabled trucks, collectively account for around 38% of the market, offering specialized use cases such as convoy driving and remote monitoring.

• In 2025, over 8,000 semi-autonomous trucks were deployed across North American highways, demonstrating large-scale real-world implementation of assisted driving technologies.

The Autonomous Trucks Market finds applications in logistics & freight transportation, mining, construction, and port operations. Logistics & freight transportation leads the segment with approximately 58% share due to increasing demand for efficient and timely deliveries. Autonomous trucks enable continuous operations, reducing transit times and improving fleet utilization. Mining applications are the fastest-growing, expected to expand at a CAGR of 17.2%, driven by the need for automation in hazardous environments and large-scale material transport. Construction and port operations collectively contribute around 42% of the market, focusing on controlled and repetitive operations suitable for automation. In 2025, over 41% of global logistics firms reported pilot testing autonomous trucking solutions, while nearly 36% of mining companies integrated automation into haulage operations.

• In 2025, a large mining operator deployed over 300 autonomous haul trucks, improving material transport efficiency by 19% across multiple sites.

Logistics companies dominate the Autonomous Trucks Market with a share of approximately 55%, driven by high demand for efficient freight movement and last-mile delivery optimization. These companies are investing heavily in automation to reduce operational costs and improve delivery speed. The mining sector is the fastest-growing end-user segment, projected to expand at a CAGR of 16.8%, supported by increasing adoption of autonomous haulage systems in large-scale mining operations. Other end-users, including construction companies and government organizations, collectively account for around 45% of the market, leveraging automation for infrastructure development and public transportation projects. In 2025, more than 48% of large enterprises globally reported integrating autonomous trucking solutions into their logistics operations, while 34% of industrial firms adopted automation for material handling.

• In 2025, over 500 logistics companies implemented AI-driven fleet management systems integrated with autonomous trucks, enhancing route optimization and reducing fuel consumption by 14%.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2026 and 2033.

North America leads due to early adoption of autonomous technologies, strong infrastructure, and high investment levels exceeding USD 5 billion annually. Europe follows with a 27% share, driven by regulatory support and sustainability initiatives, while Asia-Pacific holds around 25% share, supported by rapid industrialization and logistics expansion. South America and the Middle East & Africa collectively contribute approximately 10% of the market, with growing investments in mining and infrastructure sectors. Increasing cross-border trade, expansion of e-commerce, and government-backed smart transportation initiatives are further driving regional market growth, with notable advancements in AI integration and autonomous vehicle testing across major economies.

North America holds approximately 38% share of the Autonomous Trucks Market, driven by advanced logistics infrastructure and high technology adoption. Key industries such as e-commerce, retail, and manufacturing are actively deploying autonomous trucks to optimize supply chains. Regulatory frameworks in the United States support pilot programs and commercial testing, enabling faster innovation cycles. Technological advancements including AI-based navigation and 5G connectivity are widely implemented. A leading regional player has deployed over 1,000 autonomous trucks across interstate highways, improving delivery efficiency by 15%. Consumer behavior reflects high enterprise adoption, particularly in logistics and retail sectors, where automation is prioritized for cost reduction and operational efficiency.

Europe accounts for approximately 27% of the Autonomous Trucks Market, with key markets including Germany, the UK, and France. Regulatory bodies emphasize emission reduction and road safety, encouraging adoption of autonomous and electric trucks. Sustainability initiatives and strict environmental policies are driving innovation in low-emission autonomous vehicles. Advanced technologies such as AI-based safety systems and V2X communication are widely adopted. A major European manufacturer has introduced autonomous electric trucks for urban logistics, reducing emissions by 20%. Consumer behavior is influenced by regulatory pressure, leading to increased demand for transparent and explainable autonomous systems.

Asia-Pacific ranks as the fastest-growing region, accounting for around 25% of the Autonomous Trucks Market. Key countries including China, India, and Japan are investing heavily in infrastructure and smart transportation systems. The region benefits from strong manufacturing capabilities and expanding logistics networks. Technological innovation hubs are driving advancements in AI and autonomous vehicle technologies. A regional player has deployed autonomous trucks in industrial corridors, improving freight efficiency by 18%. Consumer behavior highlights growth driven by e-commerce expansion and mobile-based logistics platforms, supporting widespread adoption of autonomous trucking solutions.

South America contributes approximately 6% to the Autonomous Trucks Market, with Brazil and Argentina leading adoption. The mining and energy sectors are primary drivers, utilizing autonomous trucks for material transport in remote locations. Infrastructure development and government incentives are supporting automation initiatives. A local operator has implemented autonomous haul trucks in mining operations, improving productivity by 16%. Consumer behavior indicates demand driven by industrial applications and resource-based industries, where automation enhances efficiency and reduces operational risks.

The Middle East & Africa region accounts for around 4% of the Autonomous Trucks Market, with key growth countries including the UAE and South Africa. Demand is driven by oil & gas, construction, and logistics sectors. Governments are investing in smart infrastructure and digital transformation initiatives to support autonomous mobility. Technological modernization, including AI and IoT integration, is gaining traction. A regional logistics provider has piloted autonomous trucks for port operations, improving turnaround time by 12%. Consumer behavior reflects increasing adoption in industrial sectors seeking efficiency and cost optimization.

United States – 35% Market share: strong investment in autonomous mobility and large-scale logistics adoption.

China – 22% Market share: high manufacturing capacity and rapid infrastructure development supporting automation.

The Autonomous Trucks Market is moderately consolidated, with the top five companies collectively accounting for approximately 55% of the global market share. Over 30 active competitors are operating across various segments, including technology providers, automotive manufacturers, and logistics companies. Market leaders are focusing on strategic partnerships, mergers, and acquisitions to strengthen their technological capabilities and expand market presence. Collaborative initiatives between automotive OEMs and AI technology firms are accelerating product development and commercialization.

Companies are investing heavily in research and development, with over USD 2 billion allocated annually toward autonomous driving technologies. Innovation trends include the development of advanced sensor systems, AI-based decision-making algorithms, and electric autonomous truck platforms. Competitive differentiation is driven by technological advancements, scalability of solutions, and regulatory compliance capabilities, enabling companies to capture larger market shares and establish long-term industry leadership.

Waymo

Embark Trucks

Aurora Innovation

Volvo Autonomous Solutions

Daimler Truck AG

PACCAR Inc.

Navistar International

PlusAI

Kodiak Robotics

Einride AB

Scania AB

FAW Group

The Autonomous Trucks Market is driven by rapid advancements in artificial intelligence, sensor technologies, and connectivity solutions. AI-powered perception systems process over 1 terabyte of data daily per vehicle, enabling real-time decision-making and improved navigation accuracy. LiDAR sensors, capable of detecting objects up to 250 meters away, are widely used to enhance safety and situational awareness. Radar and camera systems complement LiDAR, providing multi-layered sensing capabilities for robust performance in diverse environments.

Edge computing plays a critical role in reducing latency by up to 40%, allowing autonomous trucks to respond instantly to dynamic road conditions. The integration of 5G connectivity enables high-speed data transmission, supporting vehicle-to-everything (V2X) communication and improving coordination with surrounding infrastructure. Autonomous trucks are increasingly equipped with advanced driver-assistance systems (ADAS), which include features such as lane-keeping assistance, collision avoidance, and adaptive cruise control.

Electrification is another key technological trend, with battery-powered autonomous trucks offering up to 30% lower operational costs compared to diesel counterparts. Additionally, digital twin technology is being used to simulate and optimize fleet operations, reducing maintenance costs by 15%. Continuous innovation in AI algorithms and hardware components is expected to further enhance the performance, safety, and scalability of autonomous trucking solutions.

• In April 2025, Daimler Truck delivered the latest autonomous-ready version of its Fifth Generation Freightliner Cascadia platform to Torc Robotics, featuring redundant safety systems and expanded testing routes across Texas, New Mexico, and Arizona as part of its commercialization strategy. Source: www.daimlertruck.com

• In April 2025, Volvo Autonomous Solutions and Aurora advanced their partnership to industrialize the Volvo VNL Autonomous truck integrated with the Aurora Driver, focusing on deep hardware-software integration to enable scalable Level 4 autonomous freight operations.

• In December 2024, Volvo Autonomous Solutions launched autonomous freight operations with DHL Supply Chain in Texas using the Volvo VNL Autonomous powered by Aurora Driver, marking a critical step toward validating full-scale autonomous logistics ecosystems in real-world conditions.

• In December 2025, Kodiak Robotics announced the transition from development to scaled commercial deployment, operating 10 fully driverless trucks with over 3 million autonomous miles and 5,200 hours of paid driverless service, representing one of the largest real-world autonomous truck fleets.

The Autonomous Trucks Market Report provides a comprehensive analysis of key industry segments, technologies, and regional dynamics shaping the market landscape. The report covers various types of autonomous trucks, including semi-autonomous and fully autonomous systems, along with niche categories such as platooning and remote-operated vehicles. It evaluates applications across logistics, mining, construction, and port operations, highlighting their respective contributions and operational characteristics.

Geographically, the report analyzes major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into regional adoption patterns, infrastructure development, and technological advancements. It also examines key countries within each region, focusing on industrial capabilities, regulatory frameworks, and investment trends.

The report further explores technological innovations such as AI-based perception systems, LiDAR, radar, and 5G connectivity, detailing their impact on autonomous trucking performance and scalability. It includes analysis of end-user industries, adoption rates, and operational benefits, providing a holistic view of market demand. Additionally, the report highlights emerging trends such as electrification, digital twin technology, and smart transportation systems, offering strategic insights for stakeholders. Overall, the report serves as a valuable resource for decision-makers, enabling informed planning and investment in the evolving autonomous trucking ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,677.0 Million |

| Market Revenue (2033) | USD 14,109.2 Million |

| CAGR (2026–2033) | 14.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Tesla; Waymo; TuSimple; Embark Trucks; Aurora Innovation; Volvo Autonomous Solutions; Daimler Truck AG; PACCAR Inc.; Navistar International; PlusAI; Kodiak Robotics; Einride AB; Scania AB; FAW Group |

| Customization & Pricing | Available on Request (10% Customization Free) |