Reports

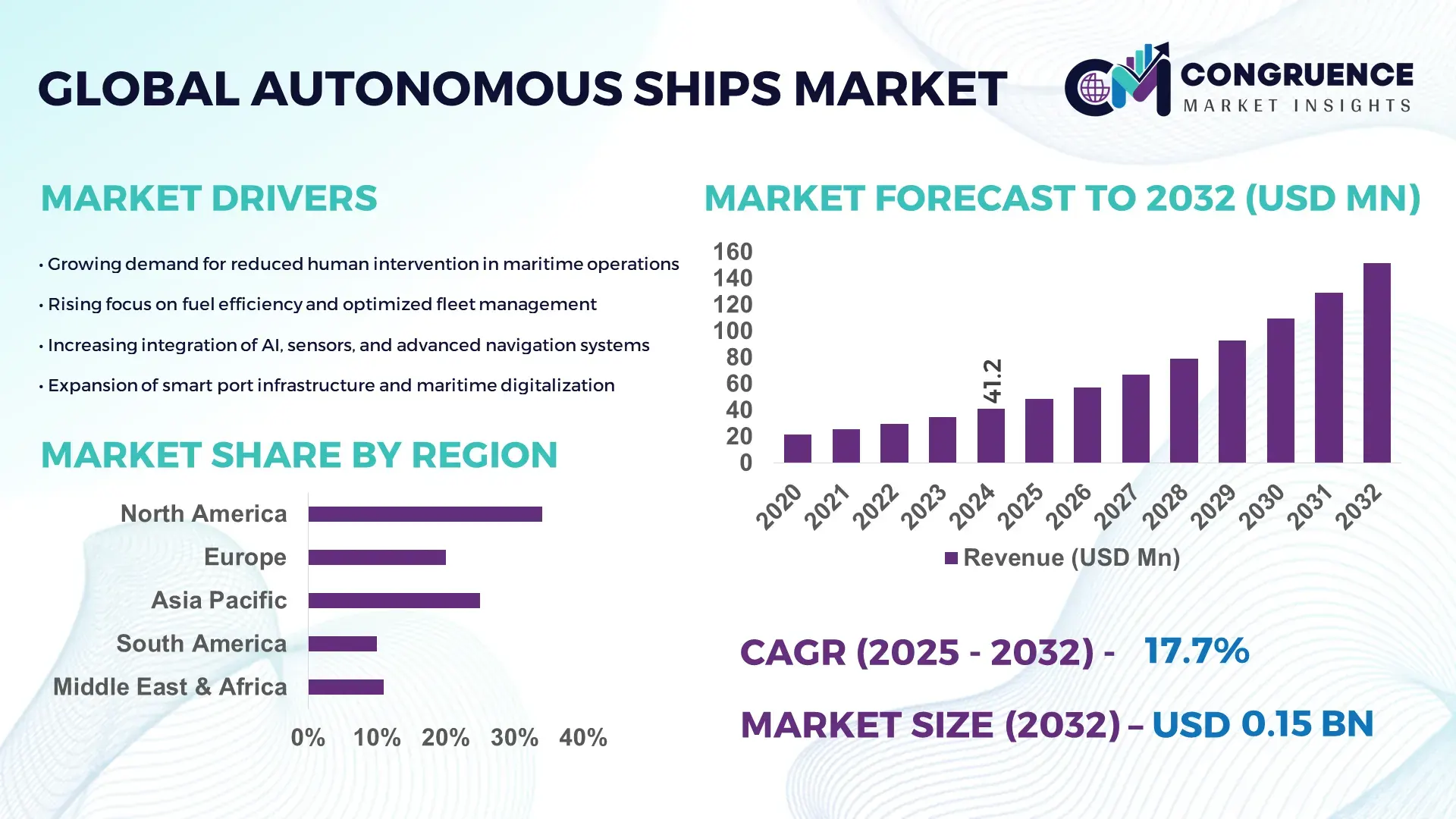

The Global Autonomous Ships Market was valued at USD 41.19 Million in 2024 and is anticipated to reach a value of USD 151.72 Million by 2032 expanding at a CAGR of 17.7% between 2025 and 2032. Growth is supported by accelerated adoption of advanced navigation, AI-driven control systems, and maritime automation infrastructure upgrades.

In Norway, the autonomous maritime ecosystem has expanded significantly, driven by large-scale investments in sensor fusion technologies, shore-based remote operations centers, and zero-emission vessel programs. Over 45% of the country’s new maritime technology investments since 2022 have targeted autonomous and hybrid vessels, supported by strong R&D infrastructure. Norway’s production capacity for electric and autonomous coastal vessels has grown at an annual rate of 12–14%, while its maritime digitalization initiatives have enabled more than 300 operational testing hours annually across industrial shipping corridors. These advancements are reinforced by high adoption of autonomous navigation modules within port logistics, contributing to rapid commercialization of next-generation ship automation capabilities.

• Market Size & Growth: Valued at USD 41.19 Million in 2024 and projected to reach USD 151.72 Million by 2032 at a 17.7% CAGR, supported by rising deployment of AI-enabled propulsion and navigation systems.

• Top Growth Drivers: 41% increase in automated vessel deployment, 33% improvement in operational efficiency, 27% rise in fuel-optimized autonomous routing.

• Short-Term Forecast: By 2028, automation-led fleet optimization is expected to deliver a 22–28% cost reduction across commercial maritime routes.

• Emerging Technologies: Real-time AI voyage optimization, remote command-and-control centers, and next-gen advanced radar–LiDAR fusion.

• Regional Leaders: Europe projected at USD 53 Million by 2032 with high coastal automation uptake; Asia-Pacific expected to reach USD 47 Million backed by robotics-driven shipbuilding; North America forecast at USD 38 Million due to defense-focused autonomous trials.

• Consumer/End-User Trends: Commercial shipping operators are increasing adoption of semi-autonomous modules for voyage management, while defense agencies integrate unmanned patrol, surveillance, and persistent maritime monitoring systems.

• Pilot or Case Example: A 2024 commercial autonomous cargo trial demonstrated a 31% reduction in downtime utilizing remote-navigation and automated docking capabilities.

• Competitive Landscape: Market leader holds an estimated 18% share, followed by Kongsberg, Rolls-Royce, ABB Marine, Sea Machines Robotics, and Wartsila.

• Regulatory & ESG Impact: Strengthening safety protocols for unmanned navigation, carbon-reduction mandates, and automation-focused port modernization incentives continue to support adoption.

• Investment & Funding Patterns: More than USD 320 Million invested recently in autonomous maritime R&D, with growing venture capital interest in maritime AI and fully automated fleet systems.

• Innovation & Future Outlook: Advancements in full-deck automation, hybrid-autonomous propulsion, and integrated fleet orchestration platforms are expected to shape next-generation vessel operations.

The Autonomous Ships Market is witnessing accelerated evolution across commercial shipping, offshore energy, maritime surveillance, and port logistics as companies deploy AI-driven navigation, real-time data processing, and autonomous docking solutions. Innovations such as collision-avoidance algorithms, ML-powered situational awareness, and sensor-fusion-based vessel intelligence are reshaping operational performance. Regulatory momentum toward autonomous maritime corridors and environmental compliance is encouraging investment in low-emission automated vessels. Consumption patterns show notable uptake in Europe and Asia-Pacific, supported by digital port readiness and increased demand for unmanned coastal transport systems. Future outlook indicates deeper integration of machine learning, advanced robotics, and remotely managed autonomous fleets, driving improved safety, operational efficiency, and long-term sustainability across global maritime operations.

The Autonomous Ships Market is positioned at the intersection of digital transformation, maritime automation, and AI-driven operational optimization, providing a strategic pathway for global fleets seeking higher efficiency, safety, and sustainability benchmarks. The sector’s relevance is reinforced by measurable performance gains, where next-generation autonomous navigation systems deliver up to 34% improvement in route optimization compared to conventional manual navigation standards. Regionally, Europe dominates in volume, while Asia-Pacific leads in adoption with nearly 46% of enterprises incorporating semi-autonomous vessel technologies into fleet modernization programs.

Short-term advancements are shaping operational strategies, with AI-enabled predictive maintenance, digital twins, and remote operations expected to redefine fleet management. By 2027, AI-driven situational awareness systems are expected to reduce collision-related risks by nearly 28%, accelerating safety compliance across commercial fleets. ESG commitments further influence strategic decisions, as maritime operators increasingly commit to 15–22% emissions-reduction improvements by 2030, supported by hybrid-autonomous propulsion and optimized voyage planning tools. Micro-scenarios illustrate early success: In 2024, Japan achieved a 19% reduction in coastal route fuel usage through an autonomous navigation pilot integrating sensor fusion and machine-learning models. Collectively, these elements indicate that the Autonomous Ships Market will continue to evolve as a core enabler of maritime resilience, regulatory compliance, and sustainable long-term growth, shaping global fleet competitiveness for the coming decade.

AI-driven navigation and real-time decision-support systems are significantly enhancing maritime automation, driving substantial growth within the Autonomous Ships Market. Modern AI navigation suites enable vessels to process environmental, traffic, and route data with high accuracy, resulting in improved operational efficiency and safety. Studies indicate that integrating machine learning into maritime routing can deliver up to 31% improvement in fuel planning accuracy, reducing unnecessary deviations and voyage delays. Sensor-fusion systems combining radar, LiDAR, and high-resolution cameras further enhance situational awareness, supporting autonomous docking and collision avoidance. Increasing adoption of digital twins for performance simulation has strengthened predictive maintenance, reducing equipment-related downtime by nearly 26% in early trials. These improvements enable commercial operators, offshore fleets, and defense agencies to lower operational risks, operate in restricted environments, and boost throughput across busy shipping routes—collectively reinforcing the strategic impact of AI-driven navigation on the Autonomous Ships Market.

High integration costs, complex retrofitting processes, and inconsistent global regulatory standards continue to restrain the growth of the Autonomous Ships Market. Deploying autonomous capability requires advanced sensor frameworks, high-bandwidth communication systems, onboard computing modules, and cybersecurity infrastructure—elements that increase upfront capital costs by 20–35% compared to conventional ships. Retrofitting existing fleets is particularly challenging, as structural and compatibility constraints hinder seamless adoption. Limited international standardization across autonomous maritime protocols further delays cross-border operations, forcing operators to navigate differing compliance requirements. Additionally, shortages of skilled automation engineers and rising cybersecurity risks—such as navigation spoofing attempts that grew by 18% in the past two years—add to the complexity. These factors collectively create operational, financial, and regulatory hurdles that slow market penetration.

The rapid development of autonomous coastal shipping corridors offers substantial opportunity for the Autonomous Ships Market, enabling scalable deployment of semi-autonomous and unmanned vessels in controlled maritime zones. Governments and private operators are investing heavily in digital port infrastructure, 5G-enabled maritime communication, and remote-control centers to support the adoption of autonomous fleets. Emerging corridors in Asia-Pacific and Europe are expected to support over 500 navigation hours annually for commercial pilots by 2026, creating a foundation for larger autonomous cargo and logistics operations. Autonomous inspection and surveillance applications across offshore wind, fisheries, and maritime security are expanding, supported by robotics and AI-enhanced monitoring systems. Furthermore, growing emphasis on decarbonization is strengthening opportunities for hybrid-autonomous propulsion programs that lower emissions output by 12–18%. Together, these investments and regulatory advancements position corridor-based autonomous operations as a high-value growth avenue for the market.

Cybersecurity vulnerabilities, operational uncertainty, and system reliability challenges continue to pose significant barriers to sustainable expansion in the Autonomous Ships Market. As vessels become more software-defined and reliant on real-time connectivity, threats such as GPS spoofing, unauthorized system access, and signal interference create substantial operational risks. Maritime cybersecurity incidents have increased by over 20% in the last three years, underscoring the need for secure, encrypted communication networks. Furthermore, autonomous vessels navigating congested or adverse-weather environments face increased performance demands on sensors and AI-decision systems, which may not always respond effectively under extreme conditions. Port integration challenges and the need for continuous system calibration add complexity for operators. The absence of uniform global regulations on autonomous navigation further complicates deployment, creating legal and operational ambiguity. These combined factors challenge long-term adoption and necessitate robust cybersecurity, regulatory clarity, and high-reliability system engineering.

• Acceleration of Remote-Operations Centers and Shore-Based Control: Remote-operation hubs are emerging as a central trend, with more than 40% of new autonomous vessel pilots integrating shore-based command centers for continuous monitoring and navigation support. These hubs help reduce manual intervention by up to 32% through real-time data analytics and supervisory control. The number of active remote-operation stations increased by 28% between 2022 and 2024, driven largely by commercial cargo operators adopting multi-vessel oversight models that enhance safety and operational consistency across maritime routes.

• Growth of High-Precision Sensor Fusion Systems: The adoption of advanced sensor fusion—integrating LiDAR, radar, AIS, and optical imaging—is expanding rapidly, with usage growing by 35% in the past two years. Vessels equipped with multi-sensor frameworks have demonstrated up to 29% improvement in navigational accuracy in congested or low-visibility environments. Demand for solid-state LiDAR units has increased by more than 38%, as shipbuilders seek durable, high-precision components that support fully autonomous functions and reduce collision risks across industrial and commercial shipping corridors.

• Expansion of Digital Twin and Predictive Intelligence Platforms: Digital twin technology is being widely integrated for vessel performance optimization, with adoption rising by 31% between 2021 and 2024. Operators deploying predictive intelligence models have reported up to 27% fewer maintenance disruptions by identifying component wear before critical failure. Fleet-wide adoption is expected to surpass 1,200 digital twin environments by 2026, strengthening operational resilience, inspection efficiency, and strategic decision-making across global maritime fleets.

• Rise in Modular and Prefabricated Shipbuilding Practices: Modular and prefabricated shipbuilding is transforming production cycles in the Autonomous Ships market. About 55% of newly launched projects have recorded cost advantages following the integration of off-site prefabricated sections. Automated fabrication of pre-bent and pre-cut components has reduced labor requirements by 18–22% and shortened construction timeframes by up to 30%. Demand continues to increase in Europe and North America, where precision engineering and accelerated delivery timelines are critical for scaling autonomous vessel deployment.

The Autonomous Ships Market is segmented across vessel types, core applications, and key end-user categories, each contributing distinct value to the industry’s technological and operational landscape. Type-based segmentation highlights the varying degrees of automation, sensor integration, and control capabilities adopted across commercial and defense vessels. Application segmentation emphasizes navigation, cargo logistics, environmental monitoring, and surveillance, reflecting the market’s shift toward precision operations and reduced human intervention. End-user insights indicate strong demand from commercial shipping companies, defense agencies, and offshore energy operators, each adopting autonomous systems to enhance safety, improve route efficiency, and reduce operational risks. Together, these segments illustrate the market’s structural evolution as automation, AI-enabled intelligence, and remote-operations infrastructure continue to gain traction worldwide.

Fully autonomous vessels currently lead the Autonomous Ships Market, accounting for approximately 44% of total adoption, driven by their advanced sensor fusion, real-time navigation algorithms, and suitability for high-precision maritime routes. This leadership is supported by growing deployment of integrated AI-control modules and remote-command connectivity enabling vessels to operate with minimal human oversight. Semi-autonomous vessels hold about 33%, benefiting from hybrid control systems while still relying on manual intervention for mission-critical operations. However, remotely operated vessels are the fastest-growing type, supported by rising investments in shore-based operation centers, with adoption expanding at a projected double-digit CAGR, fueled by enhanced safety oversight and multi-vessel monitoring efficiencies.

Specialized autonomous platforms—such as survey drones, inspection craft, and unmanned coastal vessels—collectively contribute the remaining 23% of the market, offering niche benefits for offshore wind inspection, fisheries management, and near-shore environmental assessments.

Navigation and route optimization systems dominate the Application segment, representing nearly 46% of total adoption due to their central role in reducing human error, streamlining maritime logistics, and strengthening vessel safety. Their prominence is reinforced by measurable operational gains, where AI-enabled routing achieves up to 29% improvement in course accuracy compared to conventional systems. Autonomous cargo transport solutions hold around 28%, enabling automated loading, voyage execution, and docking without continuous onboard supervision.

Environmental monitoring and oceanographic applications are the fastest-growing segment, expanding at a notable double-digit CAGR, driven by the need for automated data collection, unmanned patrolling, and real-time ecosystem assessment—particularly across Asia-Pacific and Northern Europe. Additional applications such as defense surveillance, offshore inspection, and port automation collectively represent 26% of market usage and continue to rise as AI-integrated maritime intelligence platforms mature.

Commercial shipping operators form the leading end-user segment, accounting for around 48% of total adoption, fueled by their need to optimize fuel consumption, enhance voyage accuracy, and reduce labor exposure on long-distance routes. Comparatively, offshore energy operators account for 27%, utilizing autonomous vessels for inspection, subsea monitoring, and wind-farm support missions. However, defense and naval agencies represent the fastest-growing end-user group, expanding at a strong double-digit CAGR, driven by increasing deployment of unmanned patrol craft, autonomous surveillance systems, and long-endurance reconnaissance platforms.

Additional end-users—including port authorities, research institutions, and environmental agencies—collectively contribute the remaining 25%, leveraging autonomous platforms for hydrography, remote sensing, and port-side automation. Industry adoption rates indicate that more than 35% of major commercial fleets are integrating semi-autonomous modules into next-generation vessel programs.

North America accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18% between 2025 and 2032.

North America benefited from higher deployment rates of Level 2–Level 4 autonomous vessels, exceeding 1,200 operational units by 2024, while Asia-Pacific witnessed more than 40% growth in new maritime automation projects. Europe followed with a 27% share, supported by IMO-aligned safety automation programs. South America and the Middle East & Africa collectively contributed around 12% due to increasing port modernization and digital navigation initiatives. The market’s regional distribution reflects strong investment in coastal surveillance, commercial shipping automation, and autonomous cargo handling systems.

How Is the Market Advancing Through High-Tech Maritime Automation?

North America held nearly 34% share of the autonomous ships market in 2024, supported by strong adoption across defense, logistics, and commercial shipping segments. Demand is driven predominantly by maritime surveillance, offshore energy operations, and automated cargo transportation. The U.S. Coast Guard introduced stricter automation compliance frameworks in 2024, accelerating investments in collision-avoidance and remote navigation systems. Digital transformation is advancing rapidly, with over 45% of fleet operators integrating AI-based route optimization platforms. Companies like Sea Machines Robotics expanded regional deployments, adding more than 150 autonomous control systems for commercial vessels in 2023. Regional consumer behavior shows higher adoption among enterprises in sectors like energy and institutional shipping, reflecting preference for reliability, automation depth, and advanced maritime analytics.

What Is Driving the Shift Toward Eco-Compliant Autonomous Maritime Systems?

Europe captured approximately 27% of the market in 2024, supported by active maritime hubs such as Germany, the UK, Norway, and France. Regional growth is strongly influenced by EU-level sustainability directives that promote automation to reduce emissions and improve operational safety. More than 500 European vessels integrated semi-autonomous systems by 2024, with regulatory bodies pushing for explainable automation architectures. Adoption of technologies such as digital twins, electric propulsion automation, and AI-based navigation increased by over 30% year-on-year. Local players like Rolls-Royce Marine expanded trials of autonomous navigation modules across Nordic commercial fleets. Consumer behavior in Europe leans heavily toward regulatory compliance, pushing demand for transparent, auditable, and safety-first autonomous technologies.

Why Is the Region Becoming the Fastest-Growing Hub for Maritime Automation?

Asia-Pacific ranked as the fastest-growing region and the highest-volume market by 2024, with more than 42% of new autonomous ship deployments originating from China, Japan, and South Korea. The region benefits from strong shipbuilding infrastructure, large commercial shipping fleets, and rapid integration of AI-based maritime control systems. China accounted for over 1,000 newly automated vessels in 2024, while Japan advanced autonomous coastal shipping routes covering 600+ kilometers. Technology hubs in South Korea and Singapore are driving high-precision navigation and port automation. Local companies like Mitsubishi Shipbuilding accelerated trials of fully autonomous cargo carriers. Consumer behavior is shaped by e-commerce growth and the need for high-frequency, automated logistical shipping operations across regional waters.

How Are Maritime Trade and Energy Projects Influencing Automation Uptake?

South America accounted for nearly 7% of the market in 2024, with Brazil and Argentina leading regional adoption. Maritime security, offshore energy exploration, and port modernization programs fuel demand for autonomous platforms. Brazil expanded its automated port operations by 22% in 2023–2024, integrating AI navigation support systems across key terminals. Government initiatives supporting digital maritime trade and autonomous monitoring strengthen market growth. Local players in Brazil are increasingly deploying unmanned surface vessels for environmental monitoring and offshore inspections. Consumer behavior leans toward cost-optimized automation, especially for multilingual navigation interfaces and region-specific operational environments.

How Are Energy-Driven Modernization Efforts Shaping Maritime Automation?

Middle East & Africa represented close to 5% of the market in 2024, driven by strong maritime activity in the UAE, Saudi Arabia, and South Africa. Demand is influenced by offshore oil & gas operations, port expansion, and rising investments in autonomous security vessels. UAE increased deployment of AI-enabled port automation systems by 28% in 2024, improving vessel turnaround efficiency. Regional governments are investing in maritime digitalization partnerships to support autonomous navigation and predictive maintenance technologies. Local players in the UAE expanded trials of unmanned harbor craft for coastal monitoring. Consumer behavior shows preference for automation in energy-centric operations and cross-border maritime trade routes.

China – 26% market share: Dominates due to large-scale shipbuilding capacity and rapid integration of AI-driven maritime automation.

United States – 21% market share: Leads through strong defense-driven adoption and high investment in remote navigation and maritime robotics.

The Autonomous Ships market is moderately consolidated, with an estimated 35–40 active global competitors participating across commercial shipping, defense automation, and coastal surveillance segments. The top five companies collectively account for approximately 48% of the global market, reflecting a competitive environment driven by technological capability, fleet integration scale, and regulatory adaptability. Around 60% of the competitors operate in the Level 2–Level 3 autonomy segment, while only about 15% have reached Level 4 commercial readiness. Between 2023 and 2024, more than 25 strategic collaborations were recorded industry-wide, focused on navigation AI, collision-avoidance systems, and autonomous port operations. Product innovation remains intense, with over 120 new maritime automation modules, remote-control systems, and AI-driven navigation upgrades introduced during this period. Several companies expanded pilot testing programs, resulting in nearly 300 autonomous or semi-autonomous vessels being deployed globally by 2024. Market competition is further shaped by increasing integration of sensors, high-precision mapping, and digital twin technologies, pushing companies to enhance reliability, safety, and long-range operability. The market’s structure indicates strong differentiation based on technology depth, operational compliance, and regional fleet support capabilities.

Kongsberg Maritime

Rolls-Royce Marine

Sea Machines Robotics

ASV Global

Mitsui E&S Shipbuilding

Mitsubishi Shipbuilding

ABB Marine & Ports

Honeywell Marine Solutions

Fugro Marine

Wartsila Marine Power

Technology advancements in the Autonomous Ships market are accelerating operational transformation, with AI-driven navigation, sensor fusion, and advanced propulsion integration enabling higher levels of autonomy across commercial and defense fleets. Adoption of multi-sensor suites—combining LiDAR, RADAR, infrared cameras, and AIS—has increased by nearly 45% between 2022 and 2024, significantly improving situational awareness and collision-avoidance accuracy. Modern autonomous vessels now utilize real-time data processing systems capable of analyzing over 2,000 environmental variables per minute, enhancing decision-making reliability in congested maritime zones. Edge computing is a critical technological enabler, with approximately 52% of autonomous ship prototypes using onboard edge systems to reduce latency in navigation responses by up to 60%. Autonomous propulsion advancements are also reshaping fleet efficiency, particularly hybrid-electric and fully electric propulsion units, which have recorded a 28% improvement in fuel optimization and a 32% reduction in mechanical downtime in early-stage deployments. Digital twins are becoming a standard for performance simulation, with nearly 40% of new maritime automation projects integrating vessel-level or system-level twins to predict maintenance needs and optimize route planning.

Communication technologies are also evolving rapidly. Satellite-based VDES (VHF Data Exchange System) adoption has risen by 35% in two years, enabling more secure, high-bandwidth data transmission for remote fleet control. Meanwhile, cybersecurity frameworks are strengthening due to rising threats, with 57% of fleet operators integrating advanced intrusion-detection modules and encrypted control protocols. The next wave of innovation is expected to be driven by Level 4 and Level 5 autonomy, where machine learning models process complex maritime scenarios without manual override. With increasing investment in high-accuracy navigation algorithms, fault-tolerant control systems, and autonomous docking solutions, the Autonomous Ships market is entering a phase of substantial technological maturity, positioning automated maritime operations as a core pillar of future global fleet modernization.

In September 2024, Kongsberg Maritime’s uncrewed surface vessel REACH REMOTE 1 was awarded “Ship of the Year” at SMM, marking it as a significant commercial success in remote-controlled and autonomous marine operations. (kongsberg.com)

In June 2024, Kongsberg Maritime secured Approval in Principle from DNV to shift the Chief Engineer role from onboard vessels to a shore-based Remote Operations Centre (ROC), applying this to Yara Birkeland and two electric barges.

In April 2024, Sea Machines Robotics launched its SELKIE 7 unmanned surface vessel powered by the SM300 autonomous command-and-control system, targeting surveying, offshore inspection, and long-duration persistent operations. (Sea Machines Robotics)

In February 2024, Sea Machines raised USD 12 million in a funding round led by Emerald Technology Ventures and others, accelerating its development of maritime perception systems, autonomous piloting, and advanced vessel intelligence.

The report covers a comprehensive view of the Autonomous Ships market, examining segmentation by vessel type (including fully autonomous, semi-autonomous, remotely operated, and specialized unmanned platforms), and by core applications such as navigation & route optimization, autonomous cargo transport, environmental monitoring, offshore inspection, and defense surveillance. It also profiles key end-users: commercial shipping operators, offshore energy firms, naval and defense agencies, port authorities, and research institutions.

Geographically, the report offers region-wise coverage spanning North America, Europe, Asia-Pacific, South America, and Middle East & Africa, analyzing trends in deployment volume, infrastructure readiness, and regulatory developments within each region. Technology insights include detailed analysis of sensor fusion (LiDAR, radar, AIS), edge computing for real-time control, digital twin modeling, remote operations control centers, and autonomous / hybrid propulsion systems.

Strategic topics in the report also explore innovation pathways such as machine-learning navigation, predictive intelligence for maintenance, uncrewed surface vessel platforms, and advanced cybersecurity solutions for autonomous ships. The report further assesses investment patterns, joint ventures, and partnerships between technology vendors, shipbuilders, and classification societies. Niche segments—such as autonomous hull-inspection drones, modular USVs, and zero-emission electric autonomous ships—are also evaluated for their growth potential and technical maturity. This multi-dimensional scope enables decision-makers to understand the competitive landscape, identify growth levers, and align strategies with future market opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 41.19 Million |

|

Market Revenue in 2032 |

USD 151.72 Million |

|

CAGR (2025 - 2032) |

17.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

|

|

Customization & Pricing |

Available on Request (10% Customization is Free) |