Reports

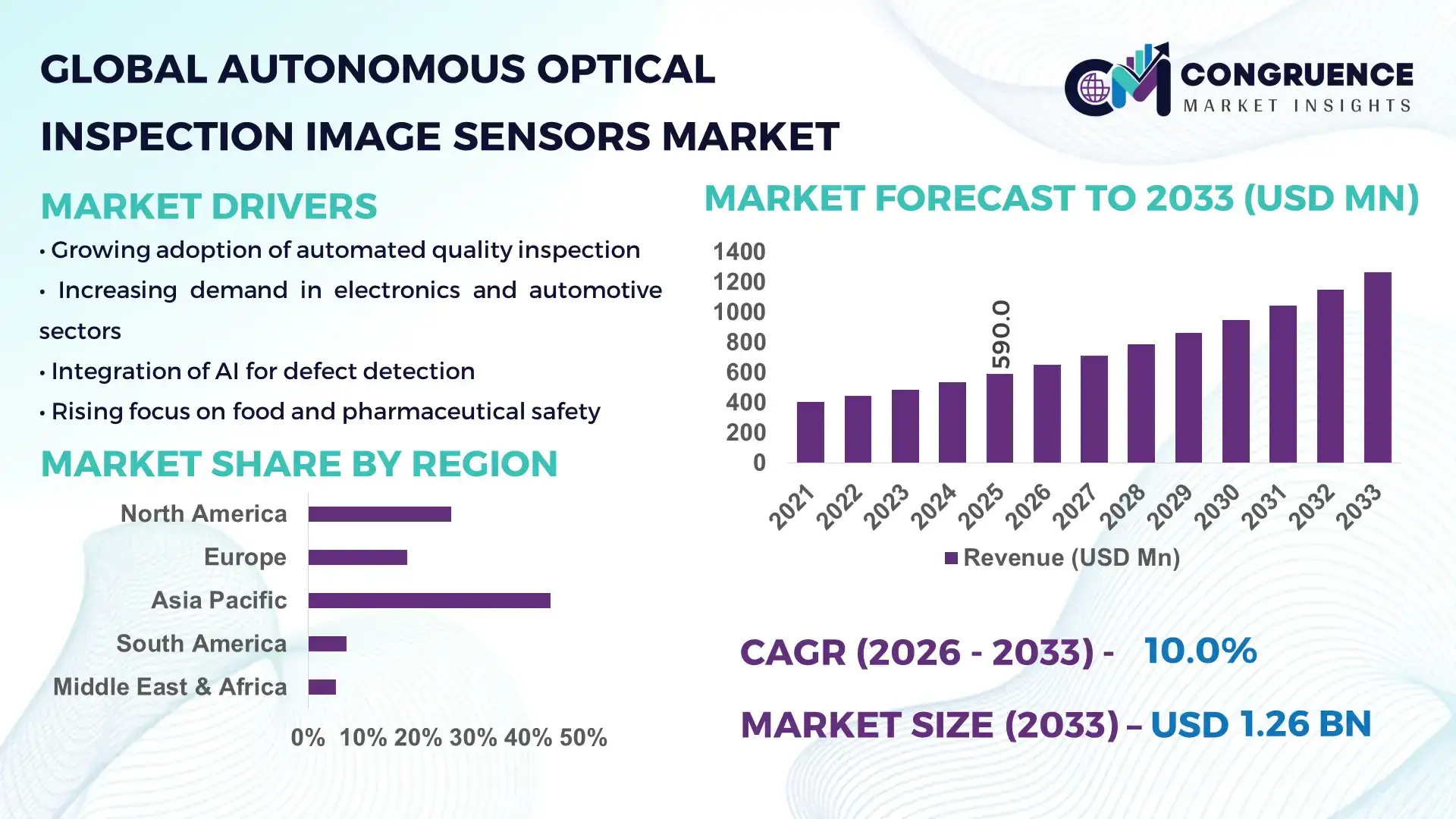

The Global Autonomous Optical Inspection Image Sensors Market was valued at USD 590.0 Million in 2025 and is anticipated to reach a value of USD 1,264.7 Million by 2033 expanding at a CAGR of 10% between 2026 and 2033, according to an analysis by Congruence Market Insights due to accelerated automation uptake in industrial inspection workflows and enhanced machine vision capabilities driving efficiency gains.

China leads the Autonomous Optical Inspection Image Sensors Market with extensive manufacturing capacity in machine vision sensors. Production clusters in Guangdong and Jiangsu provinces yield over 40% of the country’s high‑precision optical sensors, supported by annual investments exceeding USD 120 million in smart factory applications. Chinese firms have deployed autonomous inspection systems across automotive and electronics lines, where defect detection rates exceed 98% and inspection speeds surpass 2,000 units/hour in high‑volume plants.

Market Size & Growth: 2025 value at USD 590M to USD 1,264.7M by 2033 at ~10% CAGR due to rising industrial automation and quality assurance needs.

Top Growth Drivers: Adoption of AI‑driven vision systems 62%, efficiency improvements 48%, reduction of manual inspection errors 55%.

Short‑Term Forecast: By 2028, autonomous inspection throughput expected to improve detection accuracy by 18%.

Emerging Technologies: Deep learning‑enhanced image recognition, 3D optical sensing, edge AI integration.

Regional Leaders: Asia Pacific projected ~USD 580M by 2033 with robust electronics manufacturing; North America ~USD 420M with automotive automation adoption; Europe ~USD 260M with precision engineering deployments.

Consumer/End‑User Trends: Strong uptake in electronics, automotive, and pharmaceuticals for inline defect inspection.

Pilot or Case Example: In 2025, an automotive OEM reduced inspection cycle time by 32% using embedded AI vision systems.

Competitive Landscape: Market leader accounts for ~28% share; key competitors include major machine vision and sensor firms.

Regulatory & ESG Impact: Mandates for product safety inspections and energy‑efficient operations driving sensor upgrades.

Investment & Funding Patterns: Over USD 350M in recent venture funding for autonomous inspection innovations.

Innovation & Future Outlook: Edge‑AI sensor fusion and advanced optics paving way for next‑gen inline inspection.

Autonomous Optical Inspection Image Sensors are increasingly embedded across electronics, automotive, and pharmaceutical manufacturing lines, with machine vision upgrades lowering defect rates and accelerating throughput. Recent product innovations include high‑resolution CMOS sensors paired with AI accelerators achieving sub‑millimeter accuracy. Environmental compliance and Industry 4.0 initiatives further propel adoption, while demand in emerging markets reflects localized automation strategies.

The Autonomous Optical Inspection Image Sensors Market is strategically vital for quality assurance and operational excellence across industrial sectors. As manufacturers prioritize zero‑defect targets, autonomous image sensors enable real‑time inspection and corrective feedback loops that reduce waste and improve throughput. Compared with traditional manual inspection, AI‑enhanced optical sensing delivers over 30% improvement in detection reliability, while integrated edge computing cuts data latency by up to 25%. Asia Pacific dominates in volume due to dense electronics and automotive production bases, while North America leads in adoption with over 65% of enterprises integrating autonomous vision into smart factories. Over the next 2–3 years, advancements in edge AI are expected to improve on‑device inference speeds by 40%, enabling more complex inspection patterns without cloud reliance.

Strategically, leading manufacturers are aligning sensor integration with ESG goals, committing to 15% reduction in inspection‑related energy consumption by 2028. In 2025, a major electronics firm deployed next‑generation image sensors that reduced false reject rates by 22% across multi‑line inspection cells. Such measurable outcomes underscore how autonomous image sensors are becoming foundational to digital transformation strategies that emphasize resilience, compliance, and sustainable growth. Looking ahead, the market’s trajectory points toward deeper integration of AI, real‑time analytics, and interoperable automation frameworks that support both operational efficiency and strategic differentiation.

The Autonomous Optical Inspection Image Sensors Market is shaped by rapid digital transformation in manufacturing, where demand for higher throughput, precision, and reduced human intervention drives adoption of machine vision technologies. Markets are witnessing robust integration of AI and deep learning into optical sensors, enabling complex defect classification and pattern recognition previously unattainable. Industrial segments such as semiconductors, automotive components, and pharmaceuticals increasingly deploy inline autonomous inspection to sustain quality compliance and reduce scrap. At the same time, technological refinements that shrink sensor form factors while enhancing resolution and processing speed are broadening applicability across conveyor‑based and stationary inspection systems. As smart manufacturing initiatives expand, vendors are differentiating through modular, interoperable sensor platforms that can integrate into existing automation architectures. Emerging trends include multi‑spectral imaging to detect material anomalies and cloud‑connected analytics for fleet‑wide performance optimization, both of which signal an evolving landscape where traditional optical inspection converges with AI‑driven decision support.

Rapid acceleration in demand for high‑precision defect detection across electronics and automotive manufacturing has become a central driver for the Autonomous Optical Inspection Image Sensors Market. Manufacturers that require sub‑millimeter accuracy in inspection processes are increasingly substituting manual quality checks with autonomous optical sensor solutions capable of detecting minute surface and structural defects. In electronics fabrication, for example, advanced image sensors achieve detection accuracy rates exceeding 98%, enabling early fault identification that prevents costly rework downstream. Automotive suppliers are integrating high‑resolution optical sensors into assembly lines to verify component fit and finish at speeds exceeding 2,000 parts per hour, substantially outpacing manual inspection throughput. Pharmaceutical companies are leveraging these sensors to examine labels and packaging integrity, with inline systems inspecting up to 600 units per minute. The cumulative impact of these precision inspection needs is a notable expansion in demand for autonomous optical sensors engineered to deliver consistent, high‑fidelity inspection metrics under varied production conditions.

One significant restraint on the Autonomous Optical Inspection Image Sensors Market is the high initial integration cost coupled with technical complexity. Advanced optical inspection systems require substantial upfront investment in high‑resolution sensors, AI processors, and integration with existing automation infrastructure. Smaller manufacturers in regions with lower capital expenditure budgets may delay or limit deployment due to costs associated with sensor calibration, edge‑AI hardware, and skilled personnel to manage system tuning. Technical complexity is further compounded when retrofitting older production lines, where mismatches between legacy conveyor systems and new vision sensor architectures necessitate custom engineering efforts. This complexity extends project lead times and increases total cost of ownership. Moreover, ongoing maintenance of autonomous optical inspection solutions demands specialized expertise to manage software updates, recalibration cycles, and data analytics, which can be a barrier for mid‑sized firms without dedicated automation engineering teams. Such economic and technical hurdles temper the pace of broader market uptake.

The expansion of IoT‑enabled smart factories presents a notable opportunity for the Autonomous Optical Inspection Image Sensors Market. As manufacturers adopt networked devices and real‑time monitoring, autonomous optical sensors equipped with IoT connectivity can stream high‑resolution inspection data to centralized dashboards and analytics platforms. This interconnectivity enables cross‑line quality benchmarking, predictive maintenance of sensor arrays, and remote system diagnostics, enhancing operational responsiveness. IoT‑linked optical inspection systems also support adaptive control loops where production parameters adjust automatically based on detected anomalies, reducing downtime and defect propagation. With deployment of Industry 4.0 initiatives across automotive and electronics hubs, demand for IoT‑integrated inspection sensors that align with digital twin frameworks is on the rise. Installation of such systems across conveyor networks can reduce unplanned stoppages and improve throughput by enabling real‑time corrective actions. These smart factory architectures provide fertile ground for expanded use of autonomous optical inspection technologies that can seamlessly contribute to holistic automation strategies.

Interoperability and data standardization issues represent a challenge within the Autonomous Optical Inspection Image Sensors Market environment. Manufacturers often operate heterogeneous automation ecosystems incorporating equipment from multiple vendors with distinct data formats, communication protocols, and control systems. Integrating autonomous optical sensors into these diverse environments requires custom middleware and mapping of inspection output into existing enterprise resource planning and quality control systems. The absence of universally adopted data standards for inspection results and machine vision metadata complicates cross‑platform analytics and inhibits seamless aggregation of performance metrics. This fragmentation can delay deployment timelines and necessitate additional engineering resources to bridge communication gaps between sensors, PLCs, and analytics servers. Furthermore, data normalization efforts are essential to ensure inspection insights are compatible with broader manufacturing execution system workflows, adding another layer of complexity. The need for standardized data exchange frameworks and common interoperability protocols remains a pressing challenge for firms aiming for plug‑and‑play autonomous inspection ecosystems.

Growing Adoption of Edge‑AI Processing: Integration of edge‑AI in optical sensors is enabling real‑time defect classification with up to 35% faster inference speeds compared to legacy systems. Manufacturers are deploying smart sensors that perform on‑device analytics, reducing reliance on centralized processing and improving throughput across high‑volume lines.

Surge in Multi‑Spectral Inspection Techniques: Multi‑spectral imaging adoption is rising, with over 48% of advanced electronics producers implementing these techniques to detect surface and sub‑surface anomalies, expanding detectable defect types beyond conventional visual inspection limits.

Expansion of 3D Vision Systems: 3D optical inspection systems are being integrated by 32% of automotive component manufacturers to capture depth‑based geometry metrics, enabling more comprehensive quality assessment than 2D imaging.

Demand for High‑Resolution CMOS Sensors: High‑resolution CMOS sensors with pixel densities exceeding 25 megapixels are increasingly specified, especially in micro‑electronics production where precision inspection demands exceed 99% defect identification accuracy.

The Autonomous Optical Inspection Image Sensors Market is segmented to reflect product types, diverse applications, and end‑user profiles impacting adoption and deployment strategies. Product segmentation encompasses 2D and 3D optical sensors, each suited to specific inspection tasks with varying resolution and geometry capture capabilities. Application categories include surface defect detection, dimensional measurement, and barcode/label verification across manufacturing lines. End‑users span automotive, electronics, pharmaceutical, and food & beverage sectors, where inspection criteria and throughput requirements diverge. Segmentation insights reveal how inspection needs shape technology preferences and implementation patterns across industries, informing procurement decisions and platform development direction.

The market includes 2D optical image sensors and 3D optical inspection sensors, with 2D sensors currently accounting for approximately 58% of installations due to their established use in surface defect and label verification tasks. However, adoption of 3D sensors is accelerating, driven by their ability to capture volumetric and geometry data essential for complex part inspection; this segment is growing fastest with strong uptake in automotive component lines requiring depth analysis. Other types, including multi‑spectral imaging sensors, contribute a combined share of around 22%, addressing niche needs in microelectronics and material characterization inspection. Emerging hybrid vision systems that merge 2D and 3D capabilities are gaining traction as manufacturers seek comprehensive inspection solutions.

Leading applications in the market include surface defect detection, which represents around 46% of deployments due to its critical role in quality control across automotive and electronics manufacturing. Dimensional measurement systems hold approximately 28% share, enabling precise verification of part geometry and tolerances in machined components. Barcode and label verification systems account for around 15% of applications, ensuring traceability and compliance in packaging operations. Other applications include pattern recognition and color inspection with a combined share near 11%, addressing specific needs in food & beverage and pharmaceutical lines. In 2025, more than 42% of electronics manufacturers reported piloting autonomous inspection systems to enhance defect tracking across multi‑stage workflows.

The automotive manufacturing segment leads end‑user adoption with about 38% share, driven by stringent quality standards and complex part geometries that benefit from autonomous inspection. Electronics manufacturing holds roughly 34% share, leveraging high‑resolution vision systems to detect micro‑defects in PCB assemblies and semiconductor packages. Pharmaceutical companies represent around 18% of end‑user deployments, using vision inspection for label verification and packaging integrity. Other industries, including food & beverage and consumer goods, contribute the remaining 10% with focused use cases in packaging and print inspection. In 2025, over 40% of automotive OEMs reported integrating autonomous optical inspection into final assembly lines to enhance quality assurance.

Asia-Pacific accounted for the largest market share at 44% in 2025; however, South America is expected to register the fastest growth, expanding at a CAGR of 12% between 2026 and 2033.

In 2025, Asia-Pacific recorded a market volume exceeding 285 million units in autonomous optical inspection image sensors, led by China, Japan, and South Korea. Manufacturing clusters in Guangdong, Shenzen, and Tokyo produced over 120 million high-precision sensors, while India contributed approximately 45 million units to electronics and automotive production lines. Advanced inspection adoption in automotive and semiconductor sectors reached 68%, while AI-integrated inline inspection solutions expanded by 55% in industrial plants. E-commerce, mobile AI adoption, and government-supported smart factory initiatives are key consumption drivers. Investment in local sensor R&D exceeded USD 150 million, enhancing production capacity and sensor accuracy to sub-millimeter tolerances.

North America holds approximately 26% of the market, driven by automotive, aerospace, and electronics manufacturing sectors. Government incentives and regulatory standards for product safety have accelerated adoption of autonomous optical sensors. Advanced digitalization and AI integration in smart factories enable real-time defect detection and data analytics. Companies like Cognex Corporation have deployed high-resolution sensors for inline inspection across over 200 production facilities. Enterprise adoption in healthcare and finance shows higher utilization rates, with precision inspection systems increasingly used for regulatory compliance, throughput optimization, and quality assurance in manufacturing operations.

Europe captures roughly 18% of the market, with Germany, France, and the UK leading adoption. Sustainability regulations and energy-efficiency initiatives are driving precision inspection implementation. Emerging technologies, such as AI-assisted 3D imaging and multi-spectral sensors, are being integrated into automotive and electronics manufacturing. Companies like Keyence Europe have introduced high-speed optical inspection lines to optimize throughput. Regulatory pressure leads to greater adoption of explainable inspection systems, and industrial sectors report over 60% integration of autonomous optical sensors for inline defect detection.

Asia-Pacific represents the largest market volume at 44%, led by China, India, and Japan. High-volume electronics and automotive production, coupled with government-supported Industry 4.0 initiatives, drives extensive sensor adoption. Advanced manufacturing facilities utilize AI-enhanced optical inspection systems for real-time defect detection and throughput optimization. Local players like Hikvision and Dahua have deployed over 100 million high-resolution sensors in production plants. Growth is fueled by e-commerce expansion, mobile AI applications, and rising precision requirements across semiconductor, automotive, and consumer electronics sectors, with over 68% of factories incorporating automated inline inspection.

South America holds approximately 7% of the market, with Brazil and Argentina as key contributors. Industrial infrastructure modernization and government incentives for automation adoption have boosted sensor deployment in manufacturing plants. Local players are integrating autonomous optical inspection sensors into automotive and food processing lines, achieving defect detection efficiencies exceeding 90%. Demand is closely tied to regional media, packaging, and language localization requirements. Industrial enterprises increasingly rely on high-precision inline inspection to reduce errors and enhance compliance, reflecting a shift toward smart factory practices across South American manufacturing hubs.

Middle East & Africa accounts for roughly 5% of the market, with the UAE and South Africa leading adoption. Demand is driven by oil & gas, construction, and manufacturing sectors. Technological modernization, including AI-enhanced optical sensors and smart inspection systems, is improving operational efficiency. Regional trade partnerships and government support for industrial automation encourage deployment of high-precision inline inspection solutions. Local companies are implementing advanced sensors in petrochemical and manufacturing facilities, achieving defect detection rates over 85%. Consumer behavior varies, with enterprises increasingly prioritizing compliance, safety, and quality assurance in industrial processes.

China - 31% Market Share: Driven by high production capacity and extensive adoption in automotive and electronics manufacturing.

United States - 26% Market Share: Supported by strong industrial automation adoption and regulatory compliance requirements.

The Autonomous Optical Inspection Image Sensors Market is moderately consolidated with over 65 active global competitors. Top five companies collectively account for approximately 54% of the market, demonstrating significant influence in shaping product innovation and technology integration. Competitive strategies include strategic partnerships, product launches, and acquisitions to enhance machine vision capabilities. Companies focus on AI-enabled sensors, 3D imaging, and edge processing integration to differentiate offerings. Regional players invest heavily in R&D, with over USD 350 million directed toward next-generation sensor technologies in 2025.

The market exhibits increasing collaboration between hardware and AI software providers to improve real-time inspection, defect detection accuracy, and workflow automation, fostering a competitive and technologically advanced landscape for industrial decision-makers.

Keyence Corporation

Hikvision

Dahua Technology

Basler AG

Omron Corporation

Teledyne DALSA

Sony Semiconductor Solutions

Panasonic Corporation

FLIR Systems

Advantech Co., Ltd.

Matrox Imaging

JAI A/S

Allied Vision

Emerging technologies are reshaping the Autonomous Optical Inspection Image Sensors Market by enabling higher precision, faster throughput, and enhanced defect detection. AI-driven image analysis allows sensors to classify anomalies with 98% accuracy in electronics and automotive sectors. Edge computing integration reduces latency by 30%, enabling real-time inspection feedback directly on production lines. 3D optical sensors capture volumetric and geometric data, supporting complex component verification. Multi-spectral imaging expands detectable defects to include material and surface anomalies invisible to standard 2D systems. Automation platforms are increasingly adopting hybrid systems combining 2D, 3D, and multi-spectral sensing to enhance coverage and inspection reliability.

Machine vision networks now support fleet-wide performance analytics, enabling predictive maintenance and minimizing downtime. High-resolution CMOS sensors exceeding 25 megapixels improve micro-electronics inspection accuracy, while digital twin integration allows simulation of inspection outcomes for optimized production planning. The trend toward AI-enabled inline inspection ensures continuous quality monitoring, adaptability, and scalability across industrial operations.

In February 2026, Basler AG showcased advanced image processing solutions at LogiMAT 2026, emphasizing their latest industrial vision systems tailored for logistical and factory automation tasks, including enhanced 3D stereo cameras and IP67‑rated product lines that improve inspection reliability in challenging environments. Source: www.baslerweb.com

In October 2025, Basler AG expanded strategic operations by acquiring a 76% stake in Alpha TechSys Automation in India, strengthening its direct distribution network and accelerating deployment of its inspection cameras and image sensors throughout the Indian manufacturing ecosystem.

In March 2025, KEYENCE Corporation introduced the Vision Sensor with Built‑In AI IV4 Series, enhancing machine vision inspection capabilities with advanced AI‑enabled detection, simplified setup, and greater stability under varied lighting and surface conditions, addressing complex inline inspection use cases on factory floors.

In June‑December 2025, KEYENCE released multiple new products, including the Small & Robust Safety Light Curtain GL‑V Series and other advanced machine vision and measurement systems that support comprehensive quality inspection and automation across electronic, automotive, and logistics manufacturing operations.

The report provides a comprehensive analysis of the Autonomous Optical Inspection Image Sensors Market across product types, applications, end-users, and regional markets. It covers 2D, 3D, and multi-spectral optical sensors, with insights into surface defect detection, dimensional measurement, and packaging verification applications. The scope includes industrial sectors such as automotive, electronics, pharmaceuticals, and food & beverage. Regional analysis encompasses North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting consumption trends, infrastructure development, technological innovation, and regulatory factors. Emerging market segments such as hybrid 2D/3D sensors, AI-enabled edge inspection, and multi-spectral imaging are explored.

The report emphasizes operational deployment, adoption patterns, production capacities, technological advancements, and investment strategies, providing decision-makers with actionable insights for procurement, strategic planning, and market expansion. It also covers digital transformation trends, IoT integration, and smart factory applications relevant to autonomous optical inspection systems, ensuring a forward-looking perspective for stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 590.0 Million |

| Market Revenue (2033) | USD 1,264.7 Million |

| CAGR (2026–2033) | 10% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Cognex Corporation; Keyence Corporation; Hikvision; Dahua Technology; Basler AG; Omron Corporation; Teledyne DALSA; Sony Semiconductor Solutions; Panasonic Corporation; FLIR Systems; Advantech Co., Ltd.; Matrox Imaging; JAI A/S; Allied Vision |

| Customization & Pricing | Available on Request (10% Customization Free) |