Reports

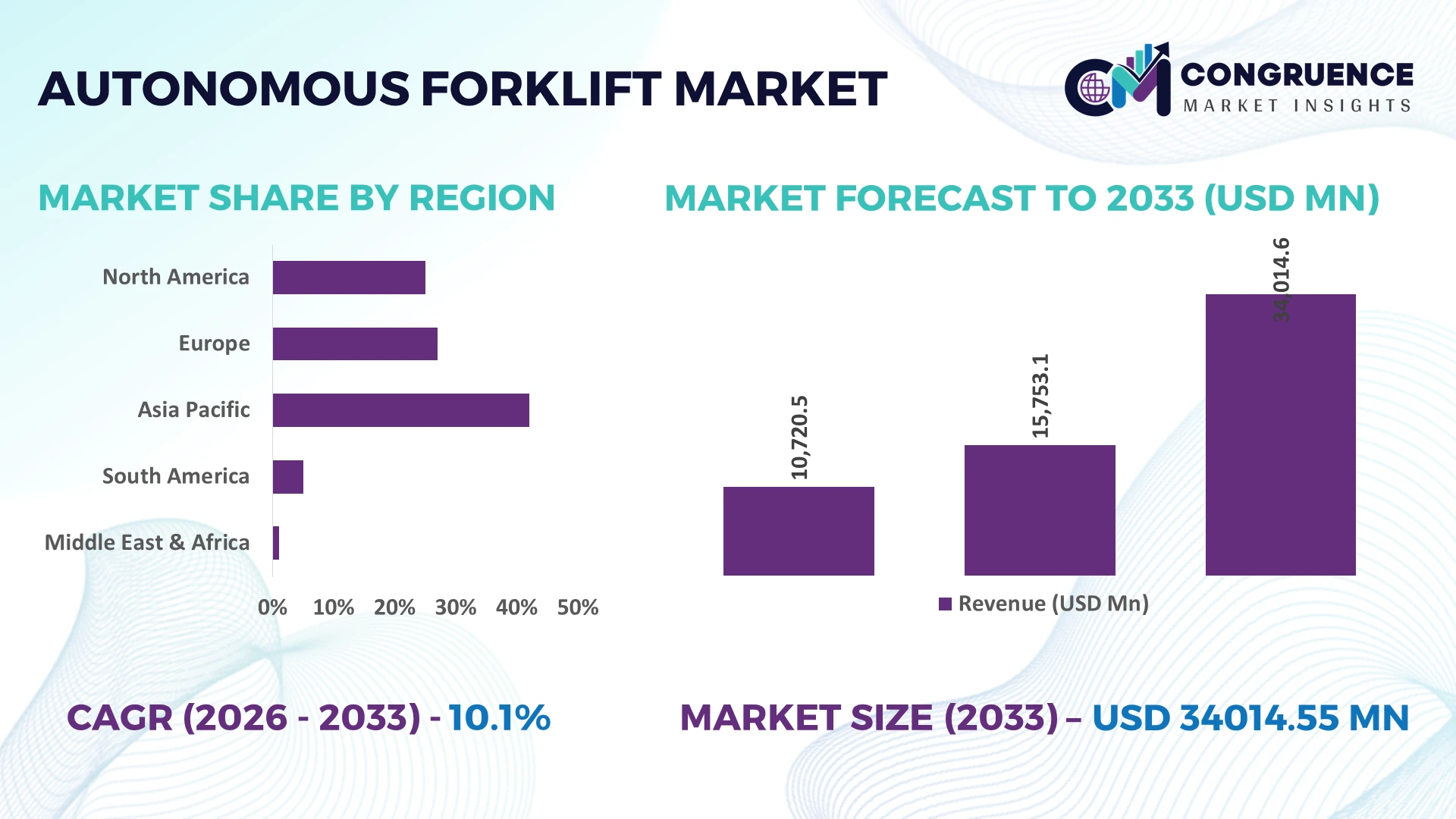

The Global Autonomous Forklift Market was valued at USD 15753.1 Million in 2025 and is anticipated to reach a value of USD 34014.55 Million by 2033 expanding at a CAGR of 10.1% between 2026 and 2033. Growth is driven by accelerated warehouse automation, AI-powered fleet management, labor shortages, and large-scale investments in smart manufacturing and logistics infrastructure.

China leads the global autonomous forklift market with approximately 36% of installed automated warehouse capacity, supported by extensive manufacturing output, logistics investments exceeding USD 15 billion, and rapid deployment across automotive, e-commerce, and electronics sectors. Compared with Germany, where Industry 4.0 initiatives drive high-value adoption, China records nearly 45% higher autonomous warehouse equipment installations. Ongoing supply-chain diversification and post-Red Sea shipping disruptions continue to accelerate regional warehouse automation strategies, strengthening long-term operational resilience.

Organizations investing early in intelligent material-handling infrastructure are securing measurable productivity gains, lower operating costs, and stronger supply-chain competitiveness.

Market Size & Growth: USD 15753.1 Million in 2025 to USD 34014.55 Million by 2033 at 10.1% CAGR, supported by AI-enabled warehouse automation and resilient supply-chain modernization.

Top Growth Drivers: Warehouse automation (+34%), labor shortages (+28%), and smart manufacturing expansion (+25%) continue accelerating global deployment.

Short-Term Forecast: By 2028, warehouse operating costs decline 18% while pallet-handling efficiency improves over 30% through autonomous fleet optimization.

Emerging Technologies: AI navigation, LiDAR perception, digital twins, and 5G connectivity improve routing accuracy by over 35% and fleet utilization by 22%.

Regional Leaders: Asia Pacific exceeds USD 15 billion, Europe approaches USD 8 billion, North America surpasses USD 7 billion, driven by logistics automation expansion.

Consumer/End-User Trends: Nearly 48% of large distribution centers prioritize autonomous forklifts for continuous 24/7 warehouse operations.

Pilot/Case Example: In 2026, an automotive manufacturing deployment improved warehouse throughput by 27% while reducing manual transport errors by 40%.

Competitive Landscape: Toyota Industries holds roughly 18% market share alongside KION Group, Jungheinrich, Mitsubishi Logisnext, and Hyster-Yale.

Regulatory & ESG Impact: Electric autonomous fleets reduce warehouse emissions by nearly 30%, supporting stricter industrial sustainability targets worldwide.

Investment & Funding: More than USD 4 billion supports robotics partnerships, manufacturing expansion, and intelligent warehouse infrastructure across major logistics hubs.

Innovation & Future Outlook: Swarm intelligence, cloud fleet orchestration, and predictive maintenance strengthen next-generation autonomous warehouse ecosystems amid global manufacturing realignment.

Autonomous Forklift Market demand continues expanding across e-commerce fulfillment centers, automotive production facilities, food and beverage warehouses, and third-party logistics operations. AI-powered vision systems, digital fleet orchestration, and battery optimization are improving equipment availability by nearly 20%. Rising warehouse electrification, stricter workplace safety standards, and resilient supply-chain planning are accelerating enterprise deployment, setting the foundation for deeper strategic market analysis.

Autonomous forklift systems are becoming a strategic priority as manufacturers and logistics operators compete to build resilient, digitally connected distribution networks. Supply-chain restructuring following persistent geopolitical disruptions and expanding warehouse automation programs is accelerating capital allocation toward intelligent material handling. AI-enabled fleet orchestration, warehouse management system integration, and predictive analytics are transforming forklifts from standalone equipment into connected operational assets that improve inventory visibility, labor utilization, and throughput consistency across high-volume facilities.

Compared with manually operated forklifts, autonomous models equipped with AI vision and LiDAR reduce transport errors by nearly 40% while improving pallet movement efficiency by approximately 30% and lowering operating costs by around 18%. China continues scaling deployments across large manufacturing parks, whereas Germany emphasizes precision automation within advanced industrial facilities, creating higher software integration intensity despite lower deployment volumes. Over the next two to three years, autonomous fleet penetration within newly automated warehouses is expected to exceed 35%, supported by wider adoption of industrial IoT platforms and edge computing.

Major logistics providers are expanding autonomous warehouse fleets through robotics partnerships, software integration, and infrastructure modernization rather than isolated equipment purchases. Companies increasingly prioritize interoperable automation ecosystems capable of supporting mixed fleets, predictive maintenance, and centralized fleet control. Organizations that align automation investments with digital warehouse strategies will strengthen operational resilience, improve asset productivity, and establish long-term competitive differentiation.

Rapid warehouse automation across manufacturing, retail, and third-party logistics is strengthening demand for autonomous forklifts as companies pursue higher throughput and lower labor dependency. Automated material-handling operations improve warehouse productivity by nearly 30%, reduce transport errors by around 40%, and enhance equipment utilization by over 20%. China's continued investment in intelligent manufacturing and automated logistics parks is reinforcing deployment momentum, while stricter workplace safety standards encourage autonomous vehicle adoption. Equipment manufacturers are responding through AI software development, strategic robotics partnerships, and expanded production capacity, enabling scalable deployments that integrate seamlessly with warehouse management platforms. The strategic advantage increasingly comes from connecting autonomous fleets into enterprise-wide digital operations rather than deploying standalone vehicles.

High implementation costs and infrastructure readiness remain significant barriers to wider autonomous forklift deployment, particularly within legacy warehouse environments. Retrofitting existing facilities can increase project costs by 20–35%, while software interoperability challenges extend deployment timelines by nearly 25%. Semiconductor component availability and industrial sensor sourcing continue facing periodic supply-chain pressure, affecting delivery schedules in several manufacturing countries. Companies are reducing exposure by localizing component procurement, adopting modular automation architectures, and negotiating long-term supplier agreements. Businesses achieving successful interoperability between warehouse management systems, robotics platforms, and autonomous fleets gain faster scalability and improved return on automation investments compared with fragmented implementations.

Next-generation warehouse ecosystems create significant opportunities beyond vehicle automation by integrating AI, digital twins, edge computing, and real-time analytics. AI-assisted fleet optimization improves route efficiency by approximately 22%, while predictive maintenance reduces unplanned equipment downtime by nearly 30%. India and Vietnam are emerging as attractive deployment markets as industrial automation policies and manufacturing expansion stimulate investment in modern logistics infrastructure. Companies are increasing R&D spending, forming software partnerships, and building open automation ecosystems capable of supporting mixed robotic fleets. A notable strategic opportunity lies in autonomous forklifts functioning as connected data platforms that continuously optimize warehouse performance rather than simply replacing manual transport equipment.

Scaling autonomous forklift deployments across multiple facilities requires overcoming complex operational, cybersecurity, and workforce integration challenges. Nearly 45% of large warehouse automation projects require substantial software customization, while cybersecurity incidents targeting connected industrial systems have increased by more than 20% in recent years. Japan and Germany face growing demand for skilled automation engineers capable of managing integrated robotics environments alongside legacy systems. Companies must strengthen digital infrastructure, invest in secure industrial communication networks, and expand workforce training through technology partnerships. Organizations that successfully standardize software architectures and governance frameworks will achieve more consistent deployment, stronger operational resilience, and sustainable long-term automation performance.

AI Fleet Intelligence Expands: Enterprises are replacing isolated vehicle control with AI-driven fleet orchestration platforms that improve fleet utilization by nearly 24%, reduce idle travel by 19%, and shorten order fulfillment time by 16%. Persistent warehouse labor shortages and increasing throughput requirements are accelerating deployment across China and the United States. Equipment suppliers are expanding software partnerships and cloud-based fleet management capabilities to optimize multi-vehicle coordination rather than individual forklift performance.

Battery Automation Becomes Standard: Lithium-ion platforms with automated opportunity charging are transforming warehouse workflows by reducing charging downtime by approximately 35% and increasing equipment availability by over 20%. Rising energy-efficiency regulations and growing electrification targets are encouraging operators to replace lead-acid fleets. Manufacturers are integrating battery monitoring, predictive maintenance, and charging automation into autonomous forklifts, creating lower lifecycle costs while improving continuous warehouse operations across high-volume distribution facilities.

Mixed Fleet Integration Accelerates: Warehouses are increasingly deploying autonomous forklifts alongside manual equipment instead of pursuing complete automation. Hybrid fleet models improve operational flexibility by nearly 28% while reducing deployment disruption by about 22%. German manufacturers and Japanese industrial operators are prioritizing interoperable warehouse management systems capable of coordinating multiple equipment types. Vendors are restructuring software architectures and expanding interoperability partnerships to simplify phased automation strategies and reduce implementation complexity.

Vision-Based Navigation Advances: AI vision systems are replacing infrastructure-dependent navigation, reducing installation requirements by nearly 30% while improving obstacle detection accuracy above 95%. This transition enables faster deployment in brownfield warehouses where structural modifications remain expensive. Companies are increasing investment in sensor fusion, machine learning, and digital mapping technologies, recognizing that adaptable navigation delivers stronger long-term operational value than fixed-path automation in dynamic logistics environments.

Counterbalance autonomous forklifts remain the dominant segment because of their versatility across manufacturing plants, warehouses, and outdoor logistics operations. Their ability to handle diverse pallet sizes without specialized infrastructure supports nearly 38% of autonomous forklift deployments. Integration with warehouse management systems and AI fleet software improves material flow efficiency by approximately 27%, encouraging enterprises to standardize fleet operations. Reach Trucks represent the fastest-growing segment as high-density warehouse designs continue expanding, with storage capacity improvements of nearly 30% driving adoption. Manufacturers are strengthening product portfolios through enhanced navigation systems, modular sensors, and battery optimization to address evolving warehouse configurations.

Pallet Stackers continue gaining traction among small and medium-sized facilities seeking lower automation costs, while Tow Tractors support repetitive production-line logistics with improved workflow consistency. Order Pickers are expanding steadily as omnichannel fulfillment requires higher picking accuracy and faster inventory movement. Companies are prioritizing modular platforms capable of supporting multiple vehicle categories within unified automation ecosystems, reflecting a strategic shift toward scalable fleet interoperability instead of single-equipment optimization.

Warehousing remains the largest application segment as distribution centers prioritize automated pallet movement, inventory accuracy, and continuous operations. Autonomous forklifts improve warehouse throughput by nearly 30% while reducing material transport errors by around 40%, making deployment increasingly essential within large fulfillment networks. E-commerce is the fastest-growing application as rising order volumes require rapid inventory movement, automated replenishment, and continuous operations. Operators are integrating autonomous fleets with warehouse execution software, robotic picking systems, and AI scheduling platforms to improve processing speed and workforce productivity.

Manufacturing continues adopting autonomous forklifts for synchronized production logistics, while Logistics providers expand deployment to strengthen cross-docking efficiency and fleet utilization. Cold Storage facilities increasingly adopt autonomous vehicles because automated operations improve safety and maintain productivity within temperature-controlled environments. Technology providers are tailoring navigation software, battery performance, and environmental sensing capabilities to meet application-specific operational requirements, creating differentiated value across industrial workflows.

Logistics Companies represent the dominant end-user segment because large distribution networks require continuous pallet handling, synchronized warehouse operations, and scalable automation across multiple facilities. Fleet automation improves asset utilization by approximately 25% while reducing manual handling requirements by nearly 35%, supporting high-volume logistics operations. Automotive manufacturers are emerging as the fastest-growing end-user group as smart factories expand automated intralogistics and just-in-time material movement. Equipment suppliers are developing industry-specific software, service contracts, and fleet management solutions to address increasingly complex operational environments.

Manufacturers continue investing in integrated production logistics, while Retailers accelerate autonomous deployment to support omnichannel fulfillment and inventory optimization. Food & Beverage facilities prioritize hygienic automated handling and uninterrupted production, whereas Healthcare organizations increasingly deploy autonomous forklifts within pharmaceutical and medical distribution centers requiring traceability and precision. Companies are strengthening ecosystem partnerships, flexible financing models, and customized automation packages to capture demand across specialized industrial sectors while improving long-term customer retention.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, South America is expected to register the fastest growth, expanding at a CAGR of 12.3% between 2026 and 2033.

Enterprise Warehouse Automation Leadership

North America remains a mature autonomous forklift market supported by advanced logistics infrastructure, large-scale e-commerce fulfillment centers, and widespread industrial automation. The region contributes approximately 28% of global deployments, with adoption concentrated across retail distribution, automotive manufacturing, and third-party logistics providers. Investments in AI-enabled warehouse management systems and industrial IoT integration continue accelerating autonomous fleet deployment, while lithium-ion equipment replacement programs improve fleet availability. During 2026, several enterprise warehouse modernization projects expanded autonomous vehicle fleets by more than 20%, reflecting sustained investment in productivity optimization and labor efficiency rather than warehouse expansion alone.

United States Market Outlook: The United States leads regional adoption through extensive warehouse automation, advanced robotics integration, and large enterprise logistics networks. High-volume fulfillment operators increasingly standardize autonomous forklifts within digitally connected facilities, supported by cloud-based fleet management platforms. More than 50% of newly commissioned high-capacity distribution centers now incorporate autonomous material-handling solutions during initial facility design, strengthening operational scalability while reducing dependency on manual warehouse transport.

Industry 4.0 Integration Strengthens Automation

Europe continues expanding autonomous forklift deployment through smart manufacturing initiatives, sustainability targets, and advanced industrial digitalization. The region represents nearly 24% of global installations, supported by automotive production, precision engineering, and automated logistics facilities. Electrified material-handling equipment, AI fleet coordination, and warehouse digital twins are improving operational consistency across industrial hubs. Manufacturers increasingly integrate autonomous forklifts into connected factory ecosystems, while cross-border logistics modernization strengthens demand for interoperable warehouse technologies and standardized industrial communication platforms.

Germany Market Outlook: Germany maintains regional leadership through Industry 4.0 implementation, advanced manufacturing capacity, and automation engineering expertise. Automotive, machinery, and industrial equipment manufacturers continue integrating autonomous forklifts into intelligent production systems requiring synchronized material flow. Nearly 45% of large smart factory modernization projects now include autonomous internal logistics platforms, encouraging technology providers to expand software integration capabilities and collaborative industrial automation partnerships.

Manufacturing Scale Accelerates Deployment

Asia-Pacific dominates the autonomous forklift market through extensive manufacturing output, rapidly expanding warehouse infrastructure, and large-scale industrial automation investments. The region accounts for approximately 42% of global market activity, supported by electronics, automotive, consumer goods, and e-commerce supply chains. Intelligent logistics parks, automated manufacturing facilities, and expanding export infrastructure continue driving deployment momentum. Enterprise investments in AI navigation, digital warehouse platforms, and autonomous fleet orchestration have improved warehouse productivity by nearly 30%, reinforcing the region's leadership in industrial automation.

China Market Outlook: China remains the largest national market because of its integrated manufacturing ecosystem, extensive logistics infrastructure, and aggressive warehouse modernization initiatives. Industrial enterprises continue expanding autonomous forklift deployments across electronics, automotive, and e-commerce fulfillment operations. More than one-third of newly developed intelligent logistics parks now deploy autonomous material-handling equipment from project commissioning, encouraging domestic manufacturers to strengthen robotics ecosystems and localized AI software development.

Logistics Modernization Drives Adoption

South America is progressing from selective automation toward broader warehouse modernization as retailers, manufacturers, and logistics operators improve supply-chain efficiency. The region currently contributes a modest global share but demonstrates accelerating deployment across distribution centers supporting consumer goods and agricultural exports. Investments in automated warehouse infrastructure and fleet digitalization continue increasing, with several logistics operators reporting handling productivity improvements exceeding 18% following phased automation. Infrastructure limitations and uneven technology readiness remain execution constraints, encouraging gradual deployment strategies instead of complete warehouse transformation.

Brazil Market Outlook: Brazil leads regional demand through expanding logistics infrastructure, manufacturing activity, and modern retail distribution networks. Large warehouse operators increasingly adopt autonomous forklifts to improve inventory flow and reduce operational bottlenecks within high-volume fulfillment centers. Industrial companies are prioritizing scalable automation investments supported by software integration and local service partnerships, enabling phased implementation while maintaining operational continuity across diverse logistics environments.

Infrastructure Investment Reshapes Logistics

The Middle East & Africa market is expanding through industrial diversification, logistics corridor development, and major warehouse infrastructure investments. Growth is supported by free economic zones, advanced distribution hubs, and smart industrial projects designed to strengthen regional supply chains. Autonomous forklift deployment remains concentrated within large logistics facilities, where integrated warehouse technologies improve inventory movement and operational visibility. New logistics infrastructure developments incorporating automation-ready warehouse designs have increased steadily, creating stronger long-term demand for intelligent material-handling systems.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional market development through world-class logistics infrastructure, automated distribution centers, and sustained investment in smart industrial ecosystems. Major logistics hubs continue integrating autonomous forklifts with warehouse management software and digital inventory platforms to improve operational efficiency. Automated warehouse developments within strategic logistics zones are encouraging technology providers to establish regional partnerships, demonstration centers, and localized technical support capabilities to accelerate enterprise adoption.

The autonomous forklift market is led by Toyota Industries, KION Group, Jungheinrich, Mitsubishi Logisnext, and Hyster-Yale, competing against regional automation specialists and robotics innovators offering software-first warehouse solutions. The top five companies collectively control approximately 58% of global market activity through integrated equipment portfolios and extensive service networks. Competition centers on AI navigation, fleet orchestration, battery technology, deployment speed, and lifecycle operating costs rather than equipment pricing alone. Intelligent fleet management improves warehouse productivity by nearly 30%, while predictive maintenance reduces downtime by approximately 25% and AI-assisted routing increases fleet utilization by around 22%. Established OEMs are expanding through robotics partnerships, software acquisitions, localized manufacturing, and vertically integrated digital platforms, while technology-focused entrants differentiate with interoperable automation ecosystems. The competitive landscape is shifting toward software-defined material handling, increasing pressure on hardware-only suppliers. High integration requirements, certification standards, and enterprise service capability remain significant entry barriers. Winning requires scalable automation platforms, proven deployment expertise, seamless software integration, and responsive lifecycle support.

Toyota Industries Corporation

KION Group AG

Jungheinrich AG

Mitsubishi Logisnext Co., Ltd.

Hyster-Yale Materials Handling, Inc.

Crown Equipment Corporation

Hangcha Group Co., Ltd.

Anhui Heli Co., Ltd.

Combilift Ltd.

Seegrid Corporation

Balyo SA

Cyngn Inc.

AGILOX Services GmbH

AI-based navigation, LiDAR, simultaneous localization and mapping (SLAM), and industrial IoT platforms now define the technological foundation of autonomous forklifts. Modern systems improve navigation accuracy by approximately 35% while reducing manual intervention by nearly 40%. More than 45% of newly automated warehouses are deploying cloud-connected fleet management platforms that synchronize vehicles with warehouse execution systems. Businesses benefit from faster pallet movement, improved inventory visibility, and higher equipment utilization across complex logistics environments.

Emerging technologies include digital twins, edge computing, machine vision, and predictive maintenance integrated through unified software ecosystems. Compared with legacy magnetic-guided or fixed-path systems, AI vision and sensor fusion reduce infrastructure modification requirements by nearly 30% while improving operational flexibility by around 25%. Companies deploying adaptive navigation gain a measurable competitive advantage because facilities can reconfigure warehouse layouts without extensive hardware changes, reducing implementation costs and deployment timelines.

Between 2026 and 2028, autonomous forklift innovation will increasingly focus on swarm intelligence, autonomous fleet orchestration, and real-time warehouse optimization. Battery analytics and machine learning are expected to improve equipment availability by approximately 20%, while interoperable automation platforms accelerate enterprise-wide deployment. Organizations investing early in software-driven automation ecosystems will strengthen productivity, scalability, and long-term competitive positioning.

February 2024: Seegrid introduced the Lift CR1 autonomous lift truck at MODEX 2024, featuring a 15-foot lift height and a 4,000 lb payload capacity to expand high-bay warehouse automation. The launch strengthened scalable deployment options for manufacturing and logistics operators. Source: seegrid.com

July 2024: Toyota Material Handling Japan and Fujitsu launched Japan's first AI-powered cloud forklift safety evaluation service through the FORKLORE platform. AI automatically analyzes operator behavior and unsafe driving events, significantly reducing manual video review while improving standardized safety training across logistics operations. Source: fujitsu.com

October 2024: Cyngn completed its first paid DriveMod Forklift deployment at a customer facility using 360° high-definition perception and Virtual Bumper technology. The commercial deployment validated real-world autonomous forklift performance and accelerated the company's transition from pilot testing to broader commercialization. Source: cyngn.com

June 2025: Cyngn showcased next-generation autonomous industrial vehicle technology at Automatica 2025 in collaboration with NVIDIA, integrating the NVIDIA Isaac robotics platform and advanced simulation capabilities. The digital simulation environment accelerated autonomous software validation and shortened development cycles for enterprise deployments.

The report provides comprehensive analysis of the Autonomous Forklift Market across major equipment types, applications, end-users, and key geographical markets between 2026 and 2033. It evaluates Counterbalance, Reach Trucks, Pallet Stackers, Tow Tractors, and Order Pickers while assessing deployment across warehousing, manufacturing, logistics, e-commerce, and cold storage operations. The study also examines adoption patterns among logistics companies, manufacturers, retailers, automotive, food & beverage, and healthcare organizations, supported by operational benchmarks, technology adoption trends, and competitive positioning across more than 20 countries.

The assessment covers AI navigation, LiDAR, machine vision, fleet orchestration, industrial IoT, digital twins, predictive maintenance, and warehouse software integration alongside emerging autonomous material-handling ecosystems. Strategic analysis includes regional deployment intensity, enterprise automation maturity, investment priorities, supply-chain transformation, and competitive benchmarking. The report enables decision-makers to identify high-priority expansion opportunities, evaluate technology readiness, optimize product positioning, and align long-term investment strategies with evolving industrial automation requirements and enterprise warehouse modernization initiatives.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 15753.1 Million |

|

Market Revenue in 2033 |

USD 34014.55 Million |

|

CAGR (2026 - 2033) |

10.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Toyota Industries Corporation, KION Group AG, Jungheinrich AG, Mitsubishi Logisnext Co., Ltd., Hyster-Yale Materials Handling, Inc., Crown Equipment Corporation, Hangcha Group Co., Ltd., Anhui Heli Co., Ltd., Combilift Ltd., Seegrid Corporation, Balyo SA, Cyngn Inc., AGILOX Services GmbH |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |