Reports

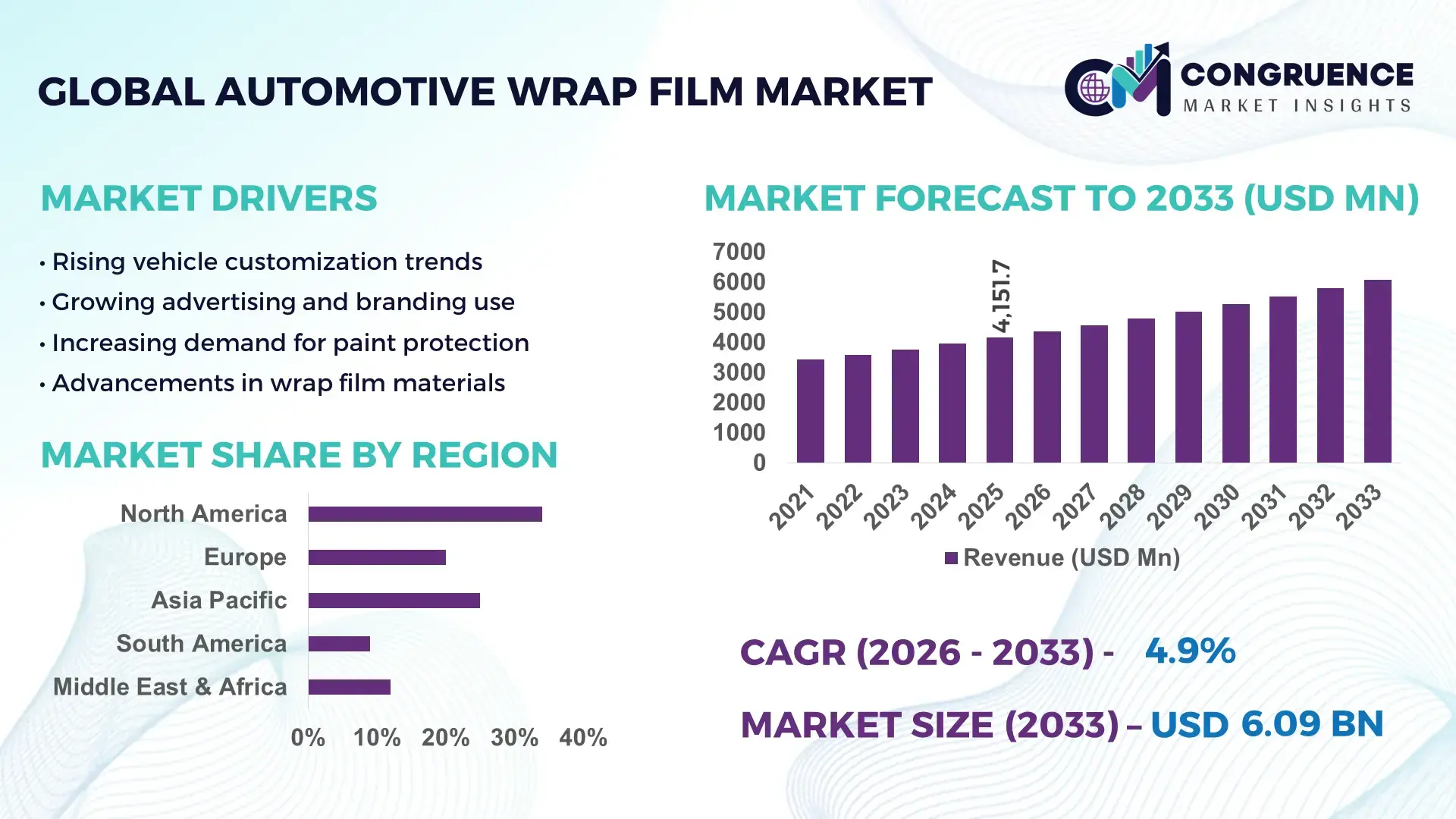

The Global Automotive Wrap Film Market was valued at USD 4151.7 Million in 2025 and is anticipated to reach a value of USD 6087.37 Million by 2033 expanding at a CAGR of 4.9% between 2026 and 2033. This growth is primarily driven by increasing demand for cost-effective vehicle customization and surface protection solutions across commercial and passenger vehicle segments.

The United States continues to demonstrate strong industrial and technological leadership in the automotive wrap film market, supported by advanced manufacturing infrastructure and high consumer adoption of vehicle personalization. Over 35% of modified vehicles in urban regions utilize vinyl wraps instead of traditional paint due to cost savings of up to 40% and faster application times. The country also hosts large-scale production facilities with annual output capacities exceeding 120 million square meters of wrap film. Significant investments in R&D, exceeding USD 500 million annually across polymer and specialty film sectors, have enabled the development of self-healing films and UV-resistant coatings. Automotive fleets, including logistics and ride-sharing services, account for nearly 28% of wrap film applications, driven by branding and protective needs.

Market Size & Growth: USD 4151.7 Million in 2025, projected to reach USD 6087.37 Million by 2033, growing at 4.9% due to rising demand for affordable vehicle customization and protective coatings.

Top Growth Drivers: Vehicle customization demand up by 32%, advertising fleet usage increased by 27%, durability improvements enhancing lifespan by 35%.

Short-Term Forecast: By 2028, installation efficiency is expected to improve by 25% with advanced adhesive technologies.

Emerging Technologies: Self-healing films, nano-coating protective layers, and air-release adhesive systems are reshaping installation and durability standards.

Regional Leaders: North America projected to reach USD 1900 Million by 2033 with strong aftermarket demand; Europe to hit USD 1600 Million driven by eco-friendly films; Asia-Pacific to exceed USD 1800 Million with rising vehicle ownership.

Consumer/End-User Trends: Commercial fleets contribute over 30% adoption, while individual vehicle owners show a 25% increase in aesthetic customization preferences.

Pilot or Case Example: In 2024, a logistics fleet project achieved 20% maintenance cost reduction through full-body wrap adoption.

Competitive Landscape: Market leader holds approximately 22% share, followed by key players specializing in high-performance vinyl and specialty films.

Regulatory & ESG Impact: Increasing restrictions on VOC emissions are pushing adoption of eco-friendly wrap films with up to 50% lower environmental impact.

Investment & Funding Patterns: Over USD 800 million invested in advanced polymer film manufacturing and sustainable materials.

Innovation & Future Outlook: Integration of smart films, improved recyclability, and AI-assisted installation tools are shaping future growth trajectories.

The automotive wrap film market is characterized by diversified applications across passenger vehicles, commercial fleets, motorsports, and advertising industries. Passenger vehicles contribute nearly 45% of total demand, followed by commercial fleets at approximately 30%, and specialty applications including motorsports and luxury customization at around 15%. Recent product innovations include multi-layered films offering over 7 years of durability, temperature resistance ranging from -40°C to 110°C, and improved conformability for complex vehicle surfaces. Regulatory pressure to reduce solvent-based paints is accelerating the shift toward eco-friendly wrap solutions. Asia-Pacific markets are witnessing rapid adoption due to rising disposable income and growing automotive ownership, while Europe emphasizes sustainable and recyclable materials. The future outlook remains strong with increasing integration of digital printing technologies and customization trends.

The automotive wrap film market is gaining strategic importance as industries prioritize cost efficiency, branding flexibility, and environmental compliance. Businesses are increasingly adopting wrap films as an alternative to repainting, with installation costs reduced by up to 40% and downtime minimized by nearly 60%. Advanced polymer-based wrap films deliver 35% higher durability compared to conventional vinyl coatings, while self-healing coatings reduce maintenance frequency by approximately 20%. These measurable benefits position wrap films as a critical component in fleet management and automotive aftermarket services.

North America dominates in volume due to high vehicle ownership and established aftermarket services, while Asia-Pacific leads in adoption with over 38% of new customization service providers entering the market annually. By 2028, AI-driven installation tools and automated cutting systems are expected to improve application accuracy by 30% and reduce material wastage by 18%. Firms are committing to sustainability metrics such as reducing plastic waste by 25% and increasing recyclable film usage by 40% by 2030, aligning with evolving ESG frameworks.

In 2024, a European automotive service provider achieved a 22% reduction in operational costs by deploying digitally printed wrap films combined with automated application systems. The strategic shift toward digital customization, combined with eco-friendly materials, is reshaping industry standards. As innovation accelerates, the automotive wrap film market is emerging as a pillar of operational resilience, regulatory compliance, and sustainable growth across global automotive ecosystems.

The growing demand for vehicle customization is a primary driver of the automotive wrap film market. More than 60% of urban vehicle owners now prefer aesthetic enhancements, including color changes, matte finishes, and branded graphics. Wrap films offer a cost-effective alternative to repainting, reducing expenses by up to 40% while enabling temporary customization. Commercial sectors, particularly logistics and ride-sharing services, have increased wrap film usage by over 30% for branding purposes. The ability to update designs within 24–48 hours without permanent alterations enhances flexibility. Additionally, advancements in digital printing technologies allow high-resolution graphics with over 95% color accuracy, further boosting adoption. This trend is particularly strong among younger consumers and small businesses seeking affordable branding solutions.

The requirement for skilled labor and precise installation techniques presents a significant restraint in the automotive wrap film market. Improper application can lead to air bubbles, peeling, and reduced lifespan, impacting customer satisfaction. Installation errors can increase material wastage by up to 15% and raise operational costs. Training programs for professional installers can take several weeks, limiting workforce scalability. Additionally, high-quality wrap films require controlled environments for optimal application, which may not be accessible in all regions. The lack of standardized certification systems further complicates quality assurance. These factors create entry barriers for small service providers and limit widespread adoption in emerging markets where skilled labor availability remains constrained.

The rapid expansion of commercial fleet operations presents a significant growth opportunity for the automotive wrap film market. Fleet branding through wrap films has increased by over 35% in the past five years, driven by the need for mobile advertising solutions. Companies benefit from up to 70% higher brand visibility compared to static advertising formats. The rise of e-commerce and last-mile delivery services has expanded the addressable market for wrap applications. Technological advancements such as weather-resistant films and UV-protected coatings extend durability to over 7 years, enhancing return on investment. Additionally, the integration of QR codes and digital advertising elements into wrap designs is opening new avenues for interactive marketing, further increasing demand.

Fluctuations in raw material prices, particularly for PVC and specialty polymers, pose a significant challenge to the automotive wrap film market. Price variations of up to 20% annually impact production costs and profit margins. At the same time, stringent environmental regulations targeting plastic usage and VOC emissions are increasing compliance costs. Manufacturers are required to invest in alternative materials and sustainable production processes, which can raise operational expenses by approximately 15%. Recycling infrastructure for wrap films remains underdeveloped, limiting circular economy initiatives. Additionally, regional regulatory differences create complexities for global manufacturers. These challenges necessitate continuous innovation and investment in sustainable materials to maintain competitiveness and regulatory compliance.

• Rapid Adoption of Digitally Printed Custom Wraps Increasing by 38% Across Commercial Fleets:

Digitally printed automotive wrap films are witnessing strong traction, with adoption rates increasing by nearly 38% among logistics and delivery fleets. High-resolution printing technologies now achieve over 95% color accuracy and reduce design turnaround time by approximately 40%. Fleet operators report up to 60% improvement in brand visibility through vehicle advertising, making wraps a preferred alternative to static billboards. Additionally, over 45% of urban commercial vehicles now feature partial or full wrap designs, reflecting a growing shift toward mobile advertising strategies that combine cost efficiency with scalability.

• Rise in Self-Healing and Nano-Coated Films Improving Lifespan by 35%:

Advanced material innovation is driving the adoption of self-healing automotive wrap films, which can repair minor scratches within 24 hours under heat exposure. These films extend operational lifespan by up to 35% compared to conventional vinyl wraps. Nano-coating technologies further enhance resistance to UV radiation, reducing color fading by nearly 50% over five years. Approximately 28% of premium vehicle owners now prefer protective wraps with these features, particularly in regions with high temperature fluctuations, highlighting a strong demand for durability and low maintenance solutions.

• Expansion of Eco-Friendly and PVC-Free Wrap Films Reducing Environmental Impact by 30%:

Sustainability trends are reshaping the automotive wrap film market, with eco-friendly alternatives gaining momentum. PVC-free films and recyclable materials have reduced environmental impact by approximately 30% compared to traditional products. Over 40% of manufacturers have introduced low-VOC adhesive systems to comply with evolving environmental regulations. In Europe, nearly 35% of newly installed wraps now meet stringent emission standards, while global adoption of sustainable wrap solutions is increasing steadily among environmentally conscious consumers and corporate fleets.

• Automation in Installation Processes Enhancing Efficiency by 25%:

The integration of automation technologies in wrap film installation is transforming operational efficiency. Automated cutting systems and AI-assisted application tools have improved installation precision by 25% and reduced material wastage by up to 18%. Training time for technicians has decreased by nearly 20%, enabling faster workforce scalability. Approximately 30% of professional service centers have adopted semi-automated solutions, particularly in North America and Asia-Pacific, where demand for high-volume installations continues to rise. This trend is driving consistent quality standards and reducing dependency on manual expertise.

The automotive wrap film market is segmented based on type, application, and end-user, each contributing distinctively to overall industry expansion. Product types range from cast films to calendered and specialty films, each designed for specific performance requirements such as flexibility, durability, and cost efficiency. Application segmentation highlights strong demand from vehicle customization, advertising, and paint protection, with customization accounting for a significant portion of installations. End-user segmentation includes individual vehicle owners, commercial fleet operators, and automotive service providers, each demonstrating varied adoption patterns. Commercial fleets and branding agencies are increasingly driving large-volume demand, while individual consumers prioritize aesthetics and protection. The segmentation landscape reflects a balance between performance-driven industrial applications and consumer-focused customization trends, supported by continuous product innovation and evolving regulatory frameworks.

The automotive wrap film market by type is primarily segmented into cast films, calendered films, and specialty films. Cast films currently account for approximately 48% of total adoption due to their superior flexibility, conformability, and durability, making them ideal for complex vehicle surfaces and long-term applications. Calendered films hold nearly 32% share, offering a cost-effective solution for short-term use and flat surfaces, particularly in advertising applications. Specialty films, including carbon fiber textures, matte finishes, and chrome wraps, collectively contribute around 20%, catering to premium customization demands.

Cast films remain the leading segment because they provide up to 7–10 years of durability and resist environmental wear more effectively than alternatives. Meanwhile, specialty films represent the fastest-growing segment, expanding at an estimated CAGR of 6.8%, driven by increasing demand for luxury aesthetics and unique finishes among high-end vehicle owners. These films offer enhanced visual appeal and differentiation, particularly in urban markets where customization trends are strong.

Application-wise, the automotive wrap film market is segmented into vehicle customization, advertising and branding, and paint protection. Vehicle customization leads the segment with approximately 44% adoption, driven by rising consumer demand for aesthetic enhancements such as color changes and textured finishes. Advertising and branding account for around 34%, as businesses increasingly use vehicle wraps as mobile marketing tools. Paint protection applications contribute close to 22%, focusing on preserving vehicle surfaces and maintaining resale value.

While customization dominates current usage, advertising and branding is the fastest-growing segment, expanding at an estimated CAGR of 6.2%, fueled by the rapid growth of e-commerce and logistics fleets. Companies are increasingly leveraging vehicle wraps to achieve up to 70% higher visibility compared to traditional outdoor advertising methods. Other applications, including motorsports and specialty vehicle modifications, collectively represent the remaining share, contributing to niche but high-value segments.

The automotive wrap film market by end-user includes individual vehicle owners, commercial fleet operators, and automotive service providers. Commercial fleet operators lead the segment with approximately 46% share, driven by large-scale adoption for branding, advertising, and vehicle protection. Individual vehicle owners account for around 36%, primarily focusing on personalization and aesthetic enhancements. Automotive service providers and dealerships contribute the remaining 18%, facilitating installation and maintenance services.

Commercial fleets dominate due to their high-volume requirements and the ability to standardize branding across multiple vehicles. However, individual vehicle owners represent the fastest-growing segment, with an estimated CAGR of 6.5%, supported by increasing disposable income and rising interest in vehicle customization trends, especially among younger consumers. Other end-users, including government and institutional fleets, contribute modestly but steadily, with adoption rates increasing by approximately 15% in urban transportation systems.

Region North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.3% between 2026 and 2033.

North America’s dominance is supported by over 18 million vehicles undergoing customization annually, with nearly 42% of fleet vehicles utilizing wrap films for branding and protection. Europe follows with approximately 28% share, driven by strict environmental standards and adoption of low-VOC materials across 60% of installations. Asia-Pacific holds close to 26% share, with more than 25 million vehicles eligible for aftermarket customization annually, particularly in China and India. South America and the Middle East & Africa collectively contribute around 12%, supported by increasing demand for mobile advertising and automotive aesthetics. The global installation base exceeds 120 million square meters annually, with over 55% demand originating from urban markets. Regional disparities are influenced by vehicle ownership rates, regulatory policies, and consumer spending patterns, with developed markets emphasizing durability and sustainability, while emerging regions focus on affordability and branding applications.

How are advanced customization trends and fleet branding strategies shaping demand patterns?

North America accounts for approximately 34% of the global automotive wrap film market, with strong demand from commercial fleets, advertising agencies, and individual consumers. The region sees over 40% adoption among logistics and delivery fleets, driven by branding requirements and cost-effective advertising solutions. Key industries include e-commerce logistics, ride-sharing, and automotive aftermarket services. Regulatory frameworks promoting low-VOC emissions have accelerated the adoption of eco-friendly wrap films, with nearly 48% of installations now using compliant materials. Technological advancements such as AI-assisted installation tools and automated cutting systems have improved efficiency by 25%. A notable regional player, Avery Dennison, has expanded its digital wrap film portfolio, enhancing print quality and durability. Consumer behavior reflects a strong preference for premium finishes, with over 30% of vehicle owners opting for matte and textured wraps, indicating a mature and innovation-driven market.

What role do sustainability regulations and premium vehicle customization trends play in shaping demand?

Europe holds around 28% of the automotive wrap film market, with key contributions from Germany, the United Kingdom, and France. Germany alone accounts for over 35% of regional installations due to its strong automotive industry and customization culture. Strict environmental regulations, including limits on VOC emissions, have resulted in over 55% of wrap films being eco-friendly or recyclable. Regulatory bodies across the region are pushing for sustainable materials, leading to increased adoption of PVC-free films. Emerging technologies such as self-healing coatings and UV-resistant films are widely implemented, improving product lifespan by up to 40%. A prominent player, Orafol Europe, has introduced high-performance cast films with extended durability. Consumer behavior in the region is influenced by regulatory compliance, with approximately 45% of customers prioritizing environmentally friendly solutions over traditional options.

Why is rapid vehicle ownership growth and digital customization accelerating industry expansion?

Asia-Pacific ranks as the fastest-growing region, contributing nearly 26% of the global automotive wrap film market. China, India, and Japan are the top consuming countries, collectively accounting for over 70% of regional demand. China alone processes more than 10 million vehicle customization projects annually, while India shows a 25% increase in wrap film adoption among urban consumers. Rapid expansion of automotive manufacturing and aftermarket services is driving demand, with over 50% of installations concentrated in metropolitan areas. The region is also a hub for innovation, with advancements in digital printing technologies improving design efficiency by 35%. A regional player, Nippon Carbide Industries, has developed high-durability films suited for extreme weather conditions. Consumer behavior reflects strong demand for affordable customization, with over 60% of buyers opting for partial wraps rather than full-body applications.

How are advertising-driven applications and urban mobility trends influencing adoption patterns?

South America accounts for approximately 7% of the automotive wrap film market, with Brazil and Argentina leading regional demand. Brazil contributes nearly 60% of regional installations due to its large automotive base and expanding logistics sector. Urban mobility and advertising applications are key drivers, with over 35% of commercial vehicles utilizing wraps for branding purposes. Infrastructure development and increasing urbanization are supporting demand for cost-effective advertising solutions. Government trade policies encouraging automotive aftermarket growth have further boosted adoption. A local market participant has focused on providing affordable wrap solutions for small businesses, increasing accessibility. Consumer behavior in the region is closely tied to advertising needs, with nearly 50% of wrap usage linked to promotional campaigns, reflecting a strong connection between media visibility and automotive applications.

What factors are driving demand across premium automotive and commercial fleet segments?

The Middle East & Africa region contributes around 5% to the global automotive wrap film market, with the UAE and South Africa emerging as key growth centers. Demand is driven by luxury vehicle customization and commercial fleet branding, with over 30% of high-end vehicles in urban areas featuring protective or decorative wraps. The construction and oil & gas sectors indirectly support demand by expanding commercial vehicle fleets. Technological modernization, including advanced heat-resistant films, has improved performance in extreme climates, increasing product adoption by 20%. Trade partnerships and import policies have facilitated access to high-quality materials. A regional distributor has expanded its portfolio to include premium wrap solutions tailored for luxury vehicles. Consumer behavior reflects a preference for high-gloss and chrome finishes, with approximately 40% of customers prioritizing aesthetic enhancement over cost considerations.

United States – 31% market share: Automotive Wrap Film market growth is supported by high fleet branding adoption and advanced manufacturing capabilities.

China – 24% market share: Automotive Wrap Film market expansion is driven by large-scale vehicle ownership and increasing demand for affordable customization solutions.

The automotive wrap film market is moderately fragmented, with over 60 active global and regional competitors competing across product innovation, pricing, and distribution networks. The top five companies collectively account for approximately 52% of the total market share, indicating a competitive yet consolidated upper tier. Leading players focus heavily on research and development, with annual investments exceeding USD 300 million in advanced polymer technologies and sustainable materials. Strategic initiatives such as mergers, partnerships, and product launches are common, with over 25 new product introductions recorded annually in the premium wrap segment alone.

Innovation remains a key differentiator, with companies developing self-healing films, UV-resistant coatings, and eco-friendly alternatives to traditional PVC materials. Digital transformation is also influencing competition, as firms integrate AI-based design tools and automated installation systems to enhance customer experience and operational efficiency. Distribution networks are expanding rapidly, with over 70% of leading companies strengthening their presence in emerging markets through partnerships with local distributors. Additionally, pricing strategies and customization capabilities are critical in capturing market share, particularly in Asia-Pacific and South America. The competitive landscape continues to evolve as companies prioritize sustainability, technological advancement, and customer-centric solutions.

3M Company

Avery Dennison Corporation

Orafol Europe GmbH

Arlon Graphics LLC

Hexis S.A.

KPMF Limited

Ritrama S.p.A.

Fedrigoni Group

Nippon Carbide Industries Co., Inc.

Lintec Corporation

Cosmo Films Ltd.

JMR Graphics Inc.

Technological advancements are playing a pivotal role in transforming the automotive wrap film market, with innovation focused on durability, ease of application, and environmental sustainability. Multi-layered film structures are now widely used, incorporating up to 5–7 functional layers that enhance tensile strength, UV resistance, and conformability. These advanced films can withstand temperature ranges from -40°C to 110°C, making them suitable for diverse climatic conditions. Self-healing technologies have gained traction, allowing minor scratches to disappear within 24–48 hours when exposed to heat, thereby extending product lifespan by up to 35%.

Adhesive technologies have also evolved significantly, with air-release channels reducing installation errors by nearly 20% and improving application speed by 25%. Pressure-sensitive adhesives now offer repositioning capabilities, enabling installers to adjust films multiple times without compromising bonding strength. Digital printing integration has improved customization capabilities, delivering over 95% color accuracy and enabling large-scale fleet branding with faster turnaround times.

Emerging innovations include nano-coatings that enhance hydrophobic properties, reducing dirt accumulation by approximately 30%, and anti-microbial surfaces designed for shared mobility vehicles. Sustainable materials are becoming a major focus, with PVC-free films and bio-based polymers reducing environmental impact by up to 30%. Additionally, smart films embedded with sensors are being explored for temperature monitoring and surface condition analysis, offering potential applications in fleet management and predictive maintenance. Automation technologies, including AI-assisted cutting and installation systems, are improving operational efficiency and reducing material wastage by up to 18%, further optimizing production and application processes.

• In March 2025, Avery Dennison expanded its Supreme Wrapping Film portfolio with enhanced Easy Apply RS adhesive technology, improving installation speed by 20% and reducing air entrapment defects. The upgrade supports faster fleet branding applications and improved surface conformity. Source: www.averydennison.com

• In October 2024, 3M introduced an updated version of its Wrap Film Series 2080 featuring improved scratch resistance and expanded color options, including over 100 finishes. The new films offer up to 25% better durability under UV exposure, supporting long-term outdoor applications. Source: www.3m.com

• In July 2025, Orafol Europe launched a new ORACAL premium cast film series with extended outdoor durability of up to 10 years and enhanced UV stability. The product line targets high-performance automotive and fleet applications requiring long-term protection and visual consistency. Source: www.orafol.com

• In January 2024, Hexis S.A. introduced a next-generation bodyfence protective wrap with self-healing nanotechnology, capable of repairing micro-scratches within 24 hours and improving surface gloss retention by 30%. The innovation is designed for luxury vehicle protection segments. Source: www.hexis-graphics.com

The automotive wrap film market report provides a comprehensive analysis of key industry segments, technological developments, and regional dynamics shaping market growth. The report covers multiple product categories, including cast films, calendered films, and specialty films, collectively accounting for over 100 million square meters of annual global installation volume. It examines applications across vehicle customization, advertising and branding, and paint protection, with customization contributing approximately 40% of total usage, followed by fleet branding and protective solutions.

Geographically, the report evaluates five major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, each analyzed based on production capacity, consumption patterns, and regulatory frameworks. The Asia-Pacific region is highlighted for its rapidly expanding automotive base, while Europe is assessed for its strong emphasis on sustainable and low-emission materials, with over 50% of products meeting environmental compliance standards.

The report also explores end-user segments such as commercial fleets, individual vehicle owners, and automotive service providers, with fleet operators representing nearly 45% of total demand. Technological coverage includes advancements in self-healing films, nano-coatings, and AI-assisted installation systems, which are improving efficiency by up to 25%. Additionally, the scope includes emerging segments such as smart wrap films and bio-based materials, reflecting the industry's shift toward innovation and sustainability. The analysis is designed to support strategic decision-making by providing actionable insights into product development, investment priorities, and competitive positioning within the automotive wrap film market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

3M Company, Avery Dennison Corporation, Orafol Europe GmbH, Arlon Graphics LLC, Hexis S.A., KPMF Limited, Ritrama S.p.A., Fedrigoni Group, Nippon Carbide Industries Co., Inc., Lintec Corporation, Cosmo Films Ltd., JMR Graphics Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |