Reports

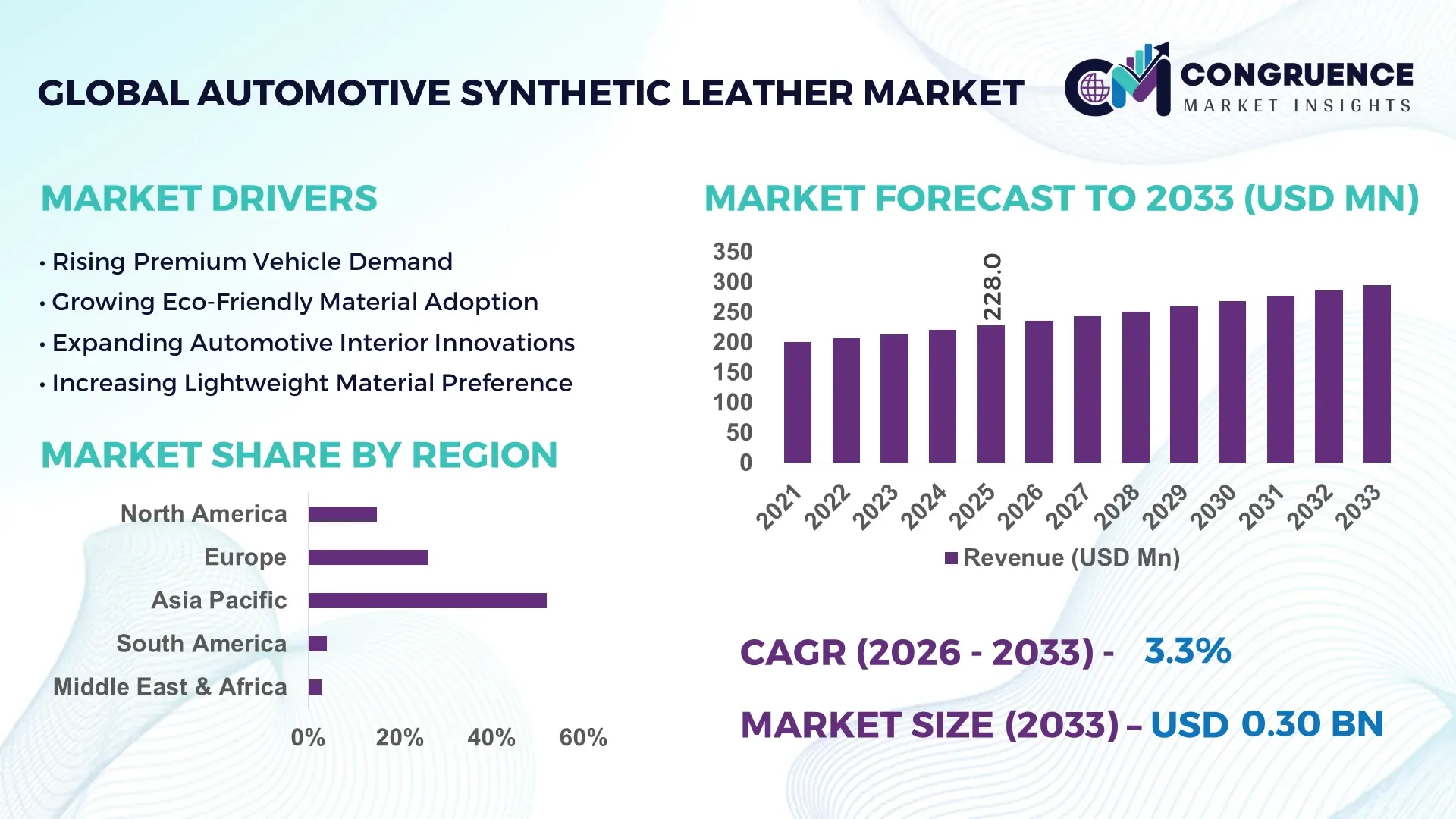

The Global Automotive Synthetic Leather Market was valued at USD 228.0 Million in 2025 and is anticipated to reach a value of USD 295.6 Million by 2033 expanding at a CAGR of 3.3% between 2026 and 2033. Rising electric vehicle production, lightweight interior material adoption, and the automotive industry’s transition away from animal-derived upholstery are accelerating demand for advanced polyurethane-based synthetic leather across passenger and premium mobility segments. Between 2024 and 2026, supply-chain realignment across Asia and Europe, combined with stricter vehicle sustainability mandates under EU circular economy frameworks, is reshaping sourcing and material innovation strategies. OEMs are shifting toward bio-based and solvent-free synthetic leather manufacturing to comply with tightening emission standards and evolving ESG procurement benchmarks.

China continues to dominate the global automotive synthetic leather ecosystem, accounting for nearly 34% of global production capacity due to its integrated polyurethane supply chain, large-scale EV manufacturing base, and export-oriented automotive component industry. More than 62% of domestic EV manufacturers in China adopted premium synthetic interior materials in 2025 to align with sustainability-focused consumer preferences. In comparison, Germany leads in high-performance automotive interior innovation, where over 45% of premium vehicle platforms now integrate low-emission synthetic upholstery technologies. Japan and South Korea are also strengthening advanced microfiber synthetic leather deployment for luxury and autonomous vehicle cabins.

The market is increasingly transforming from a cost-substitution industry into a strategic automotive materials segment where durability, sustainability, and lightweight engineering define competitive positioning for OEMs and suppliers.

Market Size & Growth: USD 228.0 Million in 2025 reaching USD 295.6 Million by 2033, driven by EV interior adoption and lightweight material integration across high-volume automotive platforms.

Top Growth Drivers: EV production expansion (+28%), premium interior demand (+21%), and bio-based polyurethane adoption (+17%) are accelerating global automotive synthetic leather deployment.

Short-Term Forecast: By 2028, solvent-free production processes are projected to reduce VOC emissions by 30% while improving manufacturing efficiency by 18%.

Emerging Technologies: AI-assisted coating systems, microfiber polyurethane composites, and recycled polymer integration are improving durability by 25% and reducing material waste by 16%.

Regional Leaders: Asia-Pacific exceeds USD 110 Million driven by EV scaling, Europe surpasses USD 78 Million through sustainability mandates, while North America advances premium interior customization adoption.

Consumer/End-User Trends: Over 54% of EV buyers now prefer vegan or sustainable interior materials, reshaping OEM upholstery sourcing priorities globally.

Pilot/Case Example: In 2025, a leading Asian automotive supplier improved coating-line productivity by 22% using automated solvent-free synthetic leather processing systems.

Competitive Landscape: Top five players control nearly 48% market share, led by Kuraray, Toray Industries, Teijin, Continental, and Mayur Uniquoters through material innovation and OEM contracts.

Regulatory & ESG Impact: EU low-emission interior mandates reduced solvent-based synthetic leather usage by 19%, accelerating transition toward recyclable polyurethane technologies.

Investment & Funding: Over USD 1.1 Billion in automotive interior material investments focused on sustainable coatings, regional manufacturing expansion, and EV-focused supply-chain localization.

Innovation & Future Outlook: High-growth bio-based synthetic leather and smart interior materials are redefining automotive cabin strategies as OEMs optimize sustainability and luxury positioning.

Automotive seating applications contribute nearly 46% of total synthetic leather consumption, followed by dashboards and door trims at approximately 31%, reflecting rising integration across premium and electric vehicle interiors. Water-based polyurethane technologies improved manufacturing efficiency by 20% between 2024 and 2026, while Asia-Pacific accounted for over 52% of global production activity due to localized supply-chain expansion. Increasing regulatory scrutiny on solvent emissions and shifting consumer preference toward vegan interiors are accelerating next-generation material innovation, positioning the market for deeper strategic transformation across automotive manufacturing ecosystems.

The Automotive Synthetic Leather Market is rapidly becoming a strategic battleground for automotive OEMs, chemical manufacturers, and advanced material suppliers as vehicle interiors evolve into a critical differentiator for brand value, sustainability, and consumer experience. Accelerating EV penetration, premium interior demand, and tightening environmental regulations are transforming synthetic leather from a low-cost substitute into a high-performance engineered material essential for competitive automotive positioning. Automakers are aggressively optimizing cabin materials to reduce weight, improve durability, and align with ESG mandates, forcing suppliers to accelerate innovation cycles and regional production strategies.

Global supply-chain restructuring and stricter European solvent-emission regulations are intensifying pressure on manufacturers to shift toward water-based and bio-derived polyurethane systems. Advanced microfiber synthetic leather now improves abrasion resistance by 32% while reducing production cost by 18% compared to conventional PVC-coated materials. Asia-Pacific leads in production volume with over 52% market concentration due to integrated manufacturing ecosystems, while Europe leads in sustainability-driven adoption, where more than 48% of premium EV interiors utilize low-emission synthetic materials.

Over the next three years, automated coating technologies and solvent-free processing lines are expected to improve manufacturing throughput by nearly 24% while reducing waste generation by 20%. ESG compliance is also emerging as a direct competitive advantage, as recyclable synthetic interior materials lower lifecycle emission exposure and strengthen OEM access to sustainability-focused markets. A major Japanese automotive supplier recently upgraded its automated coating operations, improving material consistency by 27% and reducing defect rates by 15% across EV seating programs. Simultaneously, leading automotive material companies are accelerating capital allocation toward regional production hubs, strategic OEM partnerships, and next-generation bio-polymer technologies to secure long-term contracts. The market is no longer competing solely on cost efficiency; it is reshaping around sustainability performance, supply-chain control, and advanced material engineering that define future automotive interior leadership.

The Automotive Synthetic Leather Market is being reshaped by evolving automotive interior standards, sustainability-driven procurement strategies, and the rapid expansion of electric vehicle manufacturing worldwide. OEMs are increasingly replacing traditional leather with advanced polyurethane and microfiber synthetic alternatives to improve durability, reduce weight, and comply with tightening environmental regulations. More than 54% of premium EV platforms launched between 2024 and 2026 integrated synthetic interior materials as automakers prioritized vegan-friendly and low-emission cabin solutions.

Material innovation, automation in coating technologies, and regional supply-chain localization are significantly influencing competitive dynamics. Asia-Pacific continues dominating large-scale production due to integrated raw material availability and lower conversion costs, while Europe is driving high-performance sustainable material adoption under stringent VOC and recyclability standards. Simultaneously, fluctuating petrochemical feedstock prices, regulatory scrutiny on solvent-based production, and growing pressure for circular manufacturing are redefining supplier strategies. Companies are accelerating investment in water-based polyurethane systems, recyclable coatings, and bio-derived polymers to strengthen long-term market positioning while maintaining operational scalability and cost competitiveness.

The rapid transformation of automotive interiors toward sustainable, lightweight, and premium cabin materials is becoming the primary growth engine for the Automotive Synthetic Leather Market. Electric vehicle manufacturers are aggressively replacing traditional leather with polyurethane-based synthetic alternatives to reduce vehicle weight by nearly 12% while improving manufacturing scalability and design flexibility. More than 58% of newly launched premium EV models in 2025 incorporated synthetic leather seating and trim systems due to rising consumer preference for vegan and low-emission interiors. The global shift toward sustainable mobility and tightening environmental standards across Europe and North America are forcing automotive suppliers to restructure sourcing and production strategies. EU emission frameworks and VOC reduction mandates accelerated water-based synthetic leather adoption by approximately 26% between 2024 and 2026. This regulatory push is directly increasing demand for recyclable and solvent-free coating technologies. In response, manufacturers are accelerating production expansion, regionalizing supply chains, and forming strategic partnerships with EV OEMs. Leading suppliers in China, Japan, and South Korea expanded microfiber synthetic leather production capacities by over 20% to secure long-term automotive contracts. The combination of sustainability pressure, EV scaling, and premium interior differentiation is structurally redefining material demand across the automotive value chain.

The Automotive Synthetic Leather Market faces significant structural constraints due to petrochemical feedstock dependency, volatile polyurethane pricing, and increasingly stringent environmental regulations targeting solvent-intensive production methods. Polyurethane resin prices fluctuated by nearly 18% between 2024 and 2025 as geopolitical instability and supply disruptions affected upstream chemical availability across Asia and Europe. These cost fluctuations are compressing supplier margins and limiting pricing flexibility for automotive interior manufacturers. At the same time, regulatory pressure surrounding VOC emissions and non-recyclable polymer waste is forcing companies to redesign production systems. More than 34% of legacy solvent-based production lines across Europe required operational modifications to meet updated environmental compliance standards. Smaller manufacturers with limited capital resources are struggling to absorb conversion costs and maintain competitive production efficiency. Supply concentration also remains a major risk factor, particularly in Asia-Pacific where a large share of polyurethane precursor production is clustered within a limited supplier network. This concentration exposes automakers to procurement delays and inventory instability during global trade disruptions. To mitigate these risks, companies are diversifying raw material sourcing, negotiating long-term supply contracts, and accelerating development of bio-based and recycled polymer alternatives to reduce dependency on volatile petrochemical markets.

The emergence of bio-based synthetic leather technologies and intelligent automotive interior systems is creating high-impact growth opportunities across the Automotive Synthetic Leather Market. Automotive OEMs are increasingly integrating recyclable polyurethane materials, plant-derived coatings, and sensor-compatible upholstery systems to strengthen sustainability positioning while enhancing cabin functionality. Bio-based synthetic leather adoption increased by nearly 24% between 2024 and 2026 as automakers accelerated ESG-aligned sourcing strategies. Advanced synthetic materials integrated with heating sensors, ambient lighting compatibility, and antimicrobial coatings are also reshaping premium vehicle interior design. Smart interior technologies improved cabin durability and user experience metrics by approximately 19% across luxury EV platforms. Simultaneously, water-based coating technologies reduced manufacturing waste generation by nearly 21%, creating measurable operational cost advantages for suppliers. Emerging automotive production hubs in India, Southeast Asia, and Eastern Europe are opening additional demand pockets due to localized EV manufacturing expansion and rising middle-class vehicle consumption. In response, leading manufacturers are expanding R&D spending, establishing regional technical centers, and forming ecosystem partnerships focused on recyclable materials and intelligent interior systems. Companies positioning early in bio-based and smart-surface technologies are capturing stronger OEM integration opportunities and long-term supply advantages.

The Automotive Synthetic Leather Market faces growing execution challenges linked to scalability, quality consistency, and evolving regulatory compliance requirements. While demand for sustainable interior materials is accelerating, maintaining uniform product performance across large-scale automotive programs remains a critical operational hurdle. Defect rates in high-speed synthetic leather coating processes still range between 8% and 12% in several emerging production facilities, directly impacting OEM quality benchmarks and delivery schedules. Infrastructure limitations and energy-intensive manufacturing processes are further constraining operational efficiency. Water-based polyurethane systems require specialized drying infrastructure and advanced automation, increasing production transition costs by approximately 16% compared to conventional systems. Simultaneously, labor shortages in advanced coating and polymer engineering segments are slowing deployment of next-generation manufacturing technologies. Regulatory fragmentation across regions also creates long-term uncertainty for suppliers managing multinational automotive contracts. Europe prioritizes recyclability and low-emission standards, while emerging markets remain heavily cost-driven, forcing manufacturers to balance sustainability investment with pricing competitiveness. Companies that fail to modernize production systems, secure diversified supply networks, and strengthen R&D capabilities risk losing strategic OEM partnerships as the industry shifts toward higher-performance and ESG-compliant automotive interiors.

32% Rise in Water-Based Polyurethane Adoption Reshaping Production Lines: Automotive interior manufacturers are rapidly shifting from solvent-based coatings toward water-based polyurethane systems, with adoption increasing by 32% between 2024 and 2026. This transition reduced VOC emissions by nearly 28% while improving coating consistency by 16%. Suppliers are restructuring manufacturing lines, automating drying systems, and regionalizing raw material sourcing to comply with tightening European sustainability mandates and evolving OEM procurement standards.

27% Expansion in EV-Focused Synthetic Interior Integration Accelerating Material Innovation: Electric vehicle manufacturers increased synthetic leather integration across seating, dashboards, and door trims by 27% as lightweight cabin strategies gained priority. Premium EV platforms achieved nearly 14% lower interior component weight through microfiber synthetic materials. Automotive suppliers are scaling sensor-compatible upholstery, antimicrobial coatings, and recyclable composites to optimize cabin functionality while responding to sustainability-focused consumer demand patterns.

21% Increase in Asia-Pacific Capacity Localization Redefining Supply Dynamics: Automotive synthetic leather manufacturers expanded localized production capacity across China, India, and Southeast Asia by 21% to reduce logistics costs and improve supply reliability. Companies are shifting away from single-region dependency following recent supply-chain disruptions. Faster lead times, lower transportation exposure, and integrated polymer ecosystems are enabling regional manufacturers to strengthen OEM contract competitiveness and export efficiency.

18% Growth in Premium Vegan Interior Programs Restructuring Automotive Branding: Luxury and mid-range automotive brands increased vegan interior program deployment by 18% as consumer sustainability expectations intensified. More than 52% of younger EV buyers prioritized animal-free cabin materials during vehicle selection. Automakers are responding through strategic branding partnerships, customizable synthetic upholstery programs, and advanced texture-engineering technologies that closely replicate premium leather aesthetics while lowering maintenance requirements.

The Automotive Synthetic Leather Market is segmented by type, application, and end-user demand patterns, with each category reflecting evolving automotive interior priorities around durability, sustainability, and lightweight engineering. Polyurethane-based materials continue dominating global demand due to superior flexibility and low-emission performance, while microfiber synthetic leather is gaining traction in premium EV interiors because of enhanced abrasion resistance and luxury aesthetics. Seating applications account for the largest share of material deployment, representing nearly 46% of total consumption, as automakers increasingly prioritize comfort-focused cabin upgrades and vegan interior positioning.

Demand is shifting toward advanced applications integrated with smart interior technologies, antimicrobial coatings, and recyclable polymer systems. Passenger vehicle manufacturers remain the primary end-user segment, accounting for over 63% of total demand, while premium electric mobility platforms are accelerating adoption of high-performance synthetic upholstery. Automotive suppliers are strategically expanding production capacities, investing in solvent-free technologies, and repositioning product portfolios toward sustainable interior solutions to align with OEM procurement transformation and tightening environmental regulations.

Polyurethane (PU) synthetic leather dominates the Automotive Synthetic Leather Market with approximately 58% market share due to its superior flexibility, lightweight properties, lower VOC emissions, and compatibility with advanced automotive interior applications. PU-based materials are increasingly preferred across passenger and electric vehicle interiors because they improve design versatility while reducing interior component weight by nearly 12% compared to traditional treated leather systems. Manufacturers are aggressively expanding water-based PU production capacity to comply with tightening sustainability regulations and OEM procurement requirements. Microfiber synthetic leather is emerging as the fastest-growing type, recording adoption growth above 19% due to rising demand from premium EV and luxury vehicle manufacturers seeking high abrasion resistance, premium tactile feel, and improved durability. Compared to PVC-based alternatives, microfiber materials deliver nearly 25% higher wear resistance and stronger thermal stability, accelerating integration into high-end seating and dashboard applications. PVC synthetic leather and other specialty coated materials collectively account for nearly 42% of market demand, maintaining relevance in cost-sensitive vehicle categories and commercial automotive applications where affordability and scalability remain critical. However, demand is gradually shifting away from solvent-intensive PVC systems as environmental compliance pressure intensifies. Companies are responding through product portfolio diversification, recyclable polymer innovation, and strategic investment in bio-based synthetic leather technologies, signaling a decisive transition toward sustainable, premium-focused automotive interior materials.

Seating applications lead the Automotive Synthetic Leather Market with nearly 46% share due to high material consumption intensity, direct consumer visibility, and rising demand for premium automotive comfort solutions. Automakers increasingly prioritize synthetic leather seating across electric and luxury vehicles because advanced polyurethane materials improve stain resistance, reduce maintenance requirements, and enable lightweight interior engineering. More than 54% of newly launched EV models integrated synthetic seating systems in 2025 as sustainability-focused consumers accelerated demand for vegan interiors. Dashboard and door trim applications represent the fastest-evolving segment, with adoption expanding by approximately 18% due to increasing use of soft-touch surfaces, integrated ambient lighting compatibility, and sensor-enabled interior technologies. Compared to traditional hard polymer surfaces, advanced synthetic leather trim materials improve interior aesthetics and perceived cabin quality while supporting modular assembly efficiency. Other applications, including steering wheel covers, gear systems, and headliners, collectively account for nearly 29% of market demand and maintain strategic importance in premium customization programs. Automotive suppliers are adapting by scaling microfiber coating technologies, expanding recyclable material integration, and strengthening OEM co-development partnerships focused on advanced cabin personalization. Demand is shifting toward multifunctional and sustainable interior applications where performance, aesthetics, and regulatory compliance increasingly influence procurement decisions.

Passenger vehicle manufacturers dominate the Automotive Synthetic Leather Market with approximately 63% market share due to large-scale production volumes, rising premiumization trends, and accelerating electric vehicle adoption. High demand concentration exists because synthetic leather has become a critical differentiator in consumer-facing vehicle interiors, particularly across mid-range and luxury automotive segments. More than 57% of EV-focused passenger vehicle platforms launched in 2025 integrated advanced polyurethane or microfiber upholstery systems to strengthen sustainability branding and cabin comfort positioning. Luxury and premium automotive OEMs represent the fastest-growing end-user category, with adoption increasing by nearly 21% as brands intensify focus on vegan interiors, lightweight engineering, and intelligent cabin experiences. Compared to commercial vehicle manufacturers, premium OEMs invest more aggressively in recyclable materials, antimicrobial coatings, and sensor-compatible upholstery technologies to enhance brand differentiation and regulatory alignment. Commercial vehicle and fleet operators collectively account for roughly 37% of market demand, primarily emphasizing durability, maintenance efficiency, and cost optimization. Suppliers are responding through customized product configurations, region-specific pricing strategies, and long-term OEM partnerships targeting scalable interior programs. Demand behavior is shifting toward sustainability-certified and performance-engineered materials, creating strategic opportunities for manufacturers capable of balancing cost efficiency with advanced automotive interior innovation.

Asia-Pacific accounted for the largest market share at 52% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2026 and 2033.

Asia-Pacific continues leading in production scale due to integrated polyurethane supply chains, expanding EV manufacturing capacity, and cost-efficient automotive component ecosystems across China, Japan, South Korea, and India. Europe accounts for nearly 26% of global demand and leads in sustainable material innovation, driven by low-emission automotive interior regulations and accelerating recyclable synthetic leather adoption. North America contributes approximately 15% share, supported by rising premium SUV demand and increasing vegan interior preferences among EV buyers. Meanwhile, supply-chain diversification and regional manufacturing localization are accelerating across emerging markets as automotive OEMs reduce dependence on concentrated sourcing hubs. Global companies are strategically prioritizing Asia-Pacific for scale, Europe for innovation, and North America for high-margin premium automotive interior programs.

North America represents nearly 15% of the global Automotive Synthetic Leather Market, supported by rising EV adoption, premium SUV demand, and increasing preference for sustainable automotive interiors. More than 49% of premium EV buyers in the U.S. now prioritize vegan or low-emission cabin materials, accelerating synthetic leather integration across seating and dashboard systems. Tightening sustainability commitments from automotive OEMs and supplier localization strategies are reshaping procurement decisions across the region. Manufacturers are increasingly adopting automated coating systems and recyclable polyurethane technologies, improving production efficiency by approximately 17%. Several automotive interior suppliers expanded regional production capacity between 2024 and 2026 to reduce import dependency and strengthen supply-chain resilience. Enterprise buyers are favoring durable, lightweight, and customizable interior materials that support both sustainability positioning and long-term maintenance efficiency. This combination of premiumization and operational optimization is driving continued investment and strategic expansion across North America.

Europe accounts for approximately 26% of the Automotive Synthetic Leather Market and remains the global benchmark for sustainability-driven automotive interior innovation. Germany, France, and Italy are leading adoption due to aggressive low-emission mobility targets and increasing demand for recyclable cabin materials. More than 44% of premium vehicle platforms across Europe integrated low-VOC synthetic leather systems in 2025 to comply with tightening environmental standards and evolving consumer sustainability expectations. Regulatory pressure surrounding solvent emissions and circular manufacturing is forcing suppliers to accelerate water-based polyurethane deployment and recyclable polymer integration. Automotive interior manufacturers improved VOC reduction performance by nearly 29% through advanced coating technologies and solvent-free processing upgrades. European automotive buyers increasingly prioritize compliance-certified, premium-quality interior solutions over low-cost alternatives. As a result, the region is becoming a strategic innovation hub where suppliers must continuously optimize material performance, recyclability, and ESG alignment to secure long-term OEM partnerships.

Asia-Pacific dominates the Automotive Synthetic Leather Market with nearly 52% global share due to large-scale automotive manufacturing, integrated raw material supply networks, and aggressive EV production expansion. China, Japan, South Korea, and India collectively account for the majority of global automotive synthetic leather processing capacity, supported by cost-efficient manufacturing ecosystems and export-oriented automotive supply chains. Localized production and rapid OEM integration are accelerating execution-level transformation across the region. More than 61% of EV manufacturers in China adopted synthetic leather interior systems in 2025 to align with sustainability-focused consumer trends and premium cabin expectations. Regional suppliers expanded polyurethane and microfiber coating capacity by over 20% to support rising domestic and international automotive demand. Enterprise buyers across Asia-Pacific prioritize speed, scalability, and cost efficiency, driving rapid supplier consolidation and technology deployment. The region remains strategically critical for companies seeking production scale, supply-chain resilience, and long-term automotive interior expansion opportunities.

South America contributes approximately 4% of the Automotive Synthetic Leather Market, led primarily by Brazil and Argentina where automotive assembly activity and aftermarket interior demand remain concentrated. Rising demand for affordable passenger vehicles and commercial fleet modernization is supporting gradual synthetic leather adoption across seating and trim applications. Nearly 38% of regional automotive interior demand is concentrated within mid-range passenger vehicle categories emphasizing durability and maintenance efficiency. However, currency volatility, import dependency for specialty polymers, and infrastructure limitations continue constraining large-scale market expansion. Production lead times increased by approximately 11% during recent supply-chain disruptions, pressuring regional suppliers and OEM sourcing strategies. In response, manufacturers are increasing localized assembly operations and strengthening regional distribution partnerships to improve supply stability. Buyers remain highly price-sensitive, prioritizing cost-effective and durable synthetic upholstery solutions. The region presents attractive long-term expansion potential but requires disciplined pricing strategies and localized operational execution to capture sustainable market share growth.

The Middle East & Africa accounts for nearly 3% of the Automotive Synthetic Leather Market, supported by growing infrastructure development, expanding commercial mobility sectors, and rising demand for durable automotive interiors in harsh climatic conditions. The UAE, Saudi Arabia, and South Africa are emerging as key demand centers due to increasing passenger vehicle imports and fleet modernization initiatives across logistics and construction industries. Automotive distributors and fleet operators are accelerating adoption of heat-resistant and low-maintenance synthetic upholstery systems to improve long-term operational durability. More than 22% of commercial fleet interior upgrades across Gulf markets incorporated advanced synthetic seating materials between 2024 and 2026. Regional investment in automotive service ecosystems and localized aftermarket partnerships is also strengthening market accessibility. Enterprise buyers prioritize durability, maintenance efficiency, and lifecycle cost optimization over luxury positioning. As infrastructure spending and mobility investments accelerate, the region is evolving into a strategic growth opportunity for suppliers focused on resilient and performance-engineered automotive interior solutions.

China – 34% Market share: Due to integrated polyurethane supply chains, dominant EV production capacity, and large-scale automotive component manufacturing ecosystems.

Germany – 14% Market share: Driven by premium automotive production, advanced sustainable interior technologies, and strict low-emission vehicle material standards.

The Automotive Synthetic Leather Market is characterized by intense competition between global advanced material leaders, regional cost-focused manufacturers, and automotive interior technology innovators. Major players including Kuraray, Toray Industries, Teijin, Continental, and Mayur Uniquoters collectively control nearly 48% of the global market through strong OEM relationships, integrated polyurethane capabilities, and premium synthetic upholstery technologies. Japanese and European companies compete aggressively on durability, sustainability performance, and advanced microfiber engineering, while Chinese and Indian manufacturers emphasize production scale, pricing flexibility, and rapid supply responsiveness.

Competition is increasingly shifting from pure cost advantage toward sustainable material innovation and supply-chain control. More than 41% of leading suppliers expanded water-based polyurethane production capacity between 2024 and 2026 to align with evolving ESG and low-emission automotive procurement standards. Vertical integration strategies are accelerating as manufacturers secure upstream polymer sourcing and regionalize production operations to reduce logistics exposure and improve delivery reliability.

Strategic partnerships with EV OEMs, automated coating technologies, and recyclable material development are becoming decisive competitive differentiators. High capital requirements for advanced coating infrastructure and compliance-certified manufacturing remain key entry barriers. Winning in this market increasingly depends on balancing scalable production, sustainability leadership, and rapid OEM customization capabilities simultaneously.

Toray Industries, Inc.

Teijin Limited

Continental AG

Mayur Uniquoters Limited

San Fang Chemical Industry Co., Ltd.

Alfatex Italia SRL

Benecke-Kaliko AG

Fujian Polytech Technology Corp.

Responsive Industries Ltd.

Nan Ya Plastics Corporation

Zhejiang Hexin Holdings Co., Ltd.

Kolon Industries, Inc.

HR Polycoats Pvt. Ltd.

Advanced polyurethane engineering, water-based coating systems, and microfiber composite technologies are becoming the technological foundation of the Automotive Synthetic Leather Market. Water-based polyurethane systems improved VOC reduction efficiency by nearly 30% while reducing hazardous solvent dependency across automotive interior production lines. More than 46% of newly installed automotive synthetic leather manufacturing systems now integrate automated digital coating technologies to improve consistency, reduce waste, and optimize throughput efficiency.

Microfiber synthetic leather is rapidly replacing traditional PVC-coated materials in premium automotive interiors due to superior abrasion resistance, thermal durability, and lightweight performance. Compared to legacy PVC systems, advanced microfiber technologies improve durability by approximately 25% while reducing maintenance exposure and improving tactile quality. Automotive OEMs focused on EV and luxury vehicle programs are increasingly deploying multilayer synthetic composites compatible with ambient lighting, heating sensors, and smart interior systems.

Bio-based polymer innovation is also emerging as a disruptive technology trend between 2026 and 2028. Manufacturers are accelerating development of partially plant-derived polyurethane formulations capable of reducing carbon-intensive petrochemical inputs by nearly 18%. Companies leading sustainable coating innovation and recyclable material integration are securing stronger OEM partnerships and compliance advantages across Europe and North America.

AI-enabled inspection systems and automated defect detection technologies are further optimizing manufacturing precision. Advanced machine-vision systems reduced coating defect rates by approximately 15%, enabling faster production scalability and stronger quality assurance performance. Suppliers capable of integrating sustainability, automation, and smart interior compatibility are positioned to dominate next-generation automotive interior material competition.

March 2026 – Kuraray Co., Ltd. accelerated expansion of its CLARINO advanced man-made leather portfolio for automotive and mobility applications, strengthening lightweight premium interior material positioning amid rising EV demand. The company highlighted durability-focused microfiber technologies capable of improving wear resistance and long-term surface performance across high-use cabin components. [Premium Microfiber Push] Source: www.kuraray.com

June 2025 – Toray Industries, Inc. reinforced its future mobility materials strategy through advanced lightweight composite technologies designed to improve strength-to-weight efficiency and reduce vehicle material load. Toray highlighted next-generation thermoplastic composite systems supporting durability, sustainability, and high-performance mobility integration across automotive platforms. [Future Mobility Materials]

October 2025 – Toray Industries, Inc. signed a strategic joint development agreement with Hyundai Motor Group focused on advanced mobility materials and high-performance interior component innovation. The collaboration strengthens automotive-grade advanced material commercialization and expands Toray’s future mobility ecosystem integration capabilities. [Strategic OEM Alliance]

2025 – Continental AG continued scaling sustainable automotive interior surface technologies including Benova Eco Protect, a vegan-certified low-emission material offering nearly 20% weight savings versus conventional surface materials. The company intensified focus on recyclable, low-carbon interior solutions supporting EV-focused automotive cabin transformation. [Sustainable Interior Shift]

The Automotive Synthetic Leather Market report provides comprehensive coverage of the global automotive interior materials ecosystem, analyzing demand trends across polyurethane synthetic leather, microfiber materials, PVC-coated systems, and emerging bio-based alternatives. The report evaluates key applications including seating, dashboards, door trims, steering components, and advanced smart interior surfaces, while assessing demand behavior across passenger vehicles, luxury automotive OEMs, and commercial transportation segments. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with strategic focus on manufacturing concentration, regional supply-chain shifts, and sustainability-driven adoption patterns.

The study delivers deep analytical insight through evaluation of more than 20 strategic market indicators, including regional production concentration, material adoption trends, recyclable coating integration, and evolving OEM procurement priorities. Asia-Pacific accounts for over 52% of global production activity, while premium EV interior programs exceeded 54% synthetic material integration across leading automotive platforms. The report also profiles major automotive interior material suppliers, technology innovators, and regional manufacturers shaping competitive positioning.

Future-focused analysis between 2026 and 2033 highlights next-generation technologies including water-based polyurethane systems, AI-enabled coating automation, recyclable polymer integration, and bio-derived synthetic leather innovations. The report supports investment planning, production expansion, competitive benchmarking, and long-term automotive material strategy development for manufacturers, OEMs, investors, and supply-chain decision-makers operating within the global automotive interior ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 228.0 Million |

| Market Revenue (2033) | USD 295.6 Million |

| CAGR (2026–2033) | 3.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Kuraray Co., Ltd.; Toray Industries, Inc.; Teijin Limited; Continental AG; Mayur Uniquoters Limited; San Fang Chemical Industry Co., Ltd.; Alfatex Italia SRL; Benecke-Kaliko AG; Fujian Polytech Technology Corp.; Responsive Industries Ltd.; Nan Ya Plastics Corporation; Zhejiang Hexin Holdings Co., Ltd.; Kolon Industries, Inc.; HR Polycoats Pvt. Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |