Reports

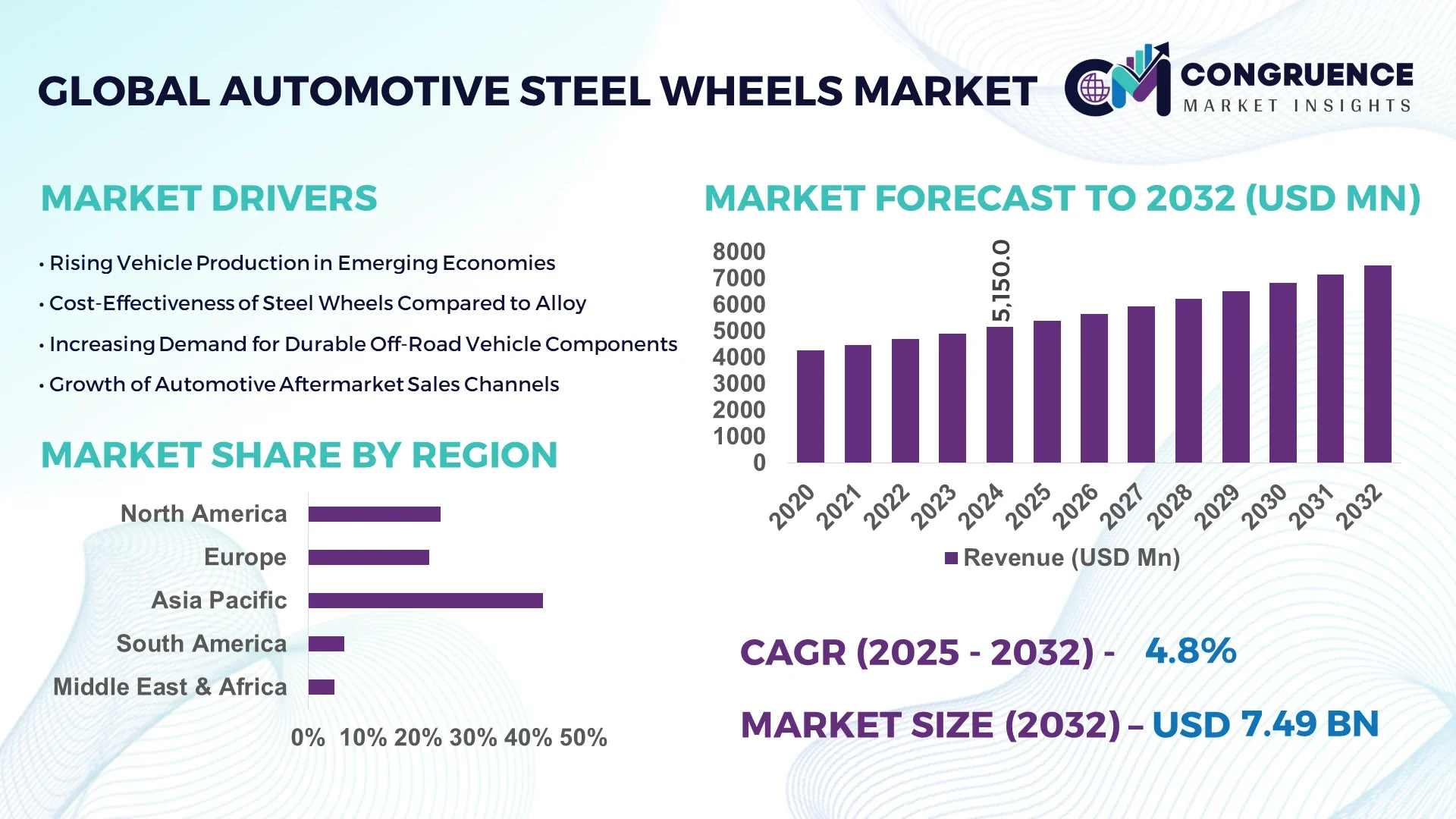

The Global Automotive Steel Wheels Market was valued at USD 5,150 Million in 2024 and is anticipated to reach a value of USD 7,493.72 Million by 2032 expanding at a CAGR of 4.8% between 2025 and 2032.

China leads the global Automotive Steel Wheels Market with a significant share of production, manufacturing over 70% of the world’s automotive steel wheels. The country has a vast manufacturing infrastructure dedicated to steel wheel production, supporting both strong domestic demand and substantial exports. This dominance is reflected in China’s extensive supply chain network and numerous manufacturing plants specializing in automotive steel wheels.

Automotive steel wheels continue to be favored across both OEM and aftermarket segments due to their structural strength, cost-efficiency, and recyclability. In 2024, passenger vehicles represented the largest end-use segment, capturing over 46.2% of the total demand. Commercial vehicles followed closely, fueled by increasing logistics operations and infrastructure development in emerging economies. The aftermarket segment accounted for 61% of the global market, with rising consumer inclination toward affordable wheel replacement solutions driving this trend. Moreover, steel wheels remain a preferred choice for off-road and heavy-duty vehicles due to their resilience under stress. Regions like Asia Pacific and Latin America are witnessing rapid growth in this segment, supported by rising vehicle ownership and local steel production capacity. OEM partnerships with steel suppliers have also contributed to price stability in this market.

AI is playing a transformative role in the automotive steel wheels market by reshaping manufacturing processes, supply chain efficiency, and product innovation. In production, AI-powered predictive maintenance tools are reducing machine downtime by up to 30% through real-time analysis of operational data. These systems alert plant operators before failures occur, minimising disruptions. Smart automation is increasingly used in wheel forming and coating processes to ensure consistent quality and dimensional precision.

Moreover, computer vision systems integrated with AI algorithms are streamlining defect detection, reducing product rejection rates by over 40%. Machine learning is also being applied to optimise logistics and inventory management, improving lead times and lowering warehousing costs. Design engineers are utilising AI-assisted simulation software to test wheel performance under various conditions, allowing for faster prototyping and innovation cycles.

The combination of AI with IoT sensors in wheel testing facilities is also creating more data-rich environments, which enhances quality control and helps manufacturers maintain compliance with international standards. As EVs and lightweight vehicle platforms gain traction, AI will increasingly aid in customising steel wheels for weight reduction without compromising strength.

“In March 2024, German-based wheel manufacturer Maxion Wheels deployed AI-powered visual inspection systems at its Brazilian plant, resulting in a 35% reduction in manual labour and increasing inspection accuracy to 98.6% across all steel wheel lines.”

Emerging economies such as India, Brazil, Indonesia, and Vietnam are experiencing a surge in vehicle production due to urbanization, improved road infrastructure, and expanding middle-class populations. In 2024, India produced over 4.7 million passenger vehicles, with a significant percentage equipped with steel wheels due to their low cost and rugged performance. As vehicle manufacturers scale up production to meet domestic and export demands, the need for durable, affordable wheel solutions continues to grow. Steel wheels also dominate in public transport, utility, and logistics sectors, where reliability and endurance in varied road conditions are crucial, contributing to higher market demand.

The increasing popularity of alloy wheels—known for their lightweight design, fuel efficiency, and visual appeal—is restraining the growth of automotive steel wheels in the passenger car segment. Premium vehicle manufacturers and mid-range OEMs are now offering alloy wheels as standard features, especially in developed markets like Europe and North America. In 2024, over 65% of new sedans in these regions were equipped with factory-fitted alloy wheels. This trend is driven by consumer demand for style, comfort, and efficiency. The weight difference also contributes to improved mileage, especially important in hybrid and electric vehicles, thus reducing the preference for steel alternatives.

The boom in e-commerce and infrastructural development is driving up commercial vehicle demand globally. Countries investing heavily in logistics networks, such as China’s Belt and Road Initiative and India’s PM Gati Shakti scheme, are seeing a rise in fleet expansions. These vehicles often rely on steel wheels for their superior durability and cost-effectiveness under heavy-duty operations. In 2024, heavy and medium commercial vehicles using steel wheels accounted for over 72% of total wheel installations in these segments. As the logistics industry prioritizes vehicle uptime and operational reliability, steel wheels offer a competitive advantage, thus opening up significant revenue potential for suppliers and OEMs alike.

Raw material price instability, particularly for high-grade steel, is posing a major challenge for automotive steel wheel manufacturers. In 2024, the average global price of hot-rolled steel fluctuated between USD 690 to USD 770 per metric ton, affecting procurement costs and squeezing profit margins. Additionally, supply chain disruptions—driven by geopolitical tensions and port congestion—have delayed shipments and extended lead times for wheel production. Manufacturers with limited diversification in their sourcing strategies are particularly vulnerable. The combined pressure of rising input costs and unpredictable supply conditions is forcing companies to rethink procurement, logistics, and production planning, creating ongoing operational complexity.

• Shift Toward Low-Maintenance and Corrosion-Resistant Steel Wheels:

Steel wheel manufacturers are increasingly focusing on surface treatment technologies to enhance corrosion resistance and longevity. In 2024, over 38% of newly produced automotive steel wheels were coated with advanced anti-rust finishes such as zinc-nickel alloys and electrophoretic coatings. These enhancements not only extend product life but also reduce maintenance costs for commercial vehicle fleets, particularly in regions with harsh climatic conditions. This trend is gaining momentum in North America and Northern Europe, where icy roads and salt exposure accelerate corrosion.

• Surge in Demand for Steel Wheels in Budget and Compact Vehicles:

With rising inflation impacting vehicle affordability, OEMs are equipping budget and subcompact models with robust steel wheels to keep production costs manageable. In 2024, steel wheels accounted for 68% of installations in the global subcompact car segment. This trend is especially strong in Latin America, South Asia, and Africa, where consumer preference leans toward durable and cost-effective vehicles. Steel wheels offer unmatched resilience on rough terrains, increasing their adoption in rural transport networks.

• Integration of Smart Manufacturing and Robotics:

The adoption of robotic assembly lines and smart manufacturing systems has transformed steel wheel production efficiency. In 2024, 46% of global production facilities implemented automated rim forming and welding systems, reducing human error and increasing throughput by nearly 30%. These technologies also ensure consistent wheel dimensions and improve fatigue resistance, critical for both passenger and commercial applications. Automation also supports lean manufacturing, enabling quick adaptation to varying wheel sizes and specifications.

• Customized Steel Wheels for Off-Road and Utility Vehicles:

A growing niche within the steel wheels market is the production of customized wheels for off-road SUVs, military transport, and heavy utility vehicles. These applications demand enhanced load capacity, thicker flanges, and reinforced designs. In 2024, the off-road utility segment saw a 21% year-on-year rise in steel wheel demand, particularly in the Middle East and Africa. Customization includes bead lock capabilities, matte finishes, and impact-resistant rims, catering to the functional and aesthetic preferences of adventurous and tactical vehicle users.

The automotive steel wheels market is segmented by type, application, and end-user, each playing a vital role in shaping demand patterns. By type, distinctions include heavy-duty truck wheels, passenger car wheels, and trailer-specific variants. On the application side, OEM and aftermarket channels define production and distribution priorities, while end-user segmentation highlights consumer behavior across personal, commercial, fleet, and industrial vehicle sectors. The growing preference for fuel-efficient yet durable transportation is influencing segment growth differently across regions. In developing nations, OEM demand for standard-size steel wheels is increasing rapidly, while aftermarket sales are soaring in North America and Europe due to seasonal wheel changes and vehicle refurbishments. Customization, corrosion resistance, and compatibility with emerging vehicle platforms such as electric and utility vehicles are further refining market segmentation strategies.

The automotive steel wheels market includes segments such as standard steel wheels, heavy-duty steel wheels, split rim wheels, tube-type steel wheels, and tubeless steel wheels. In 2024, standard steel wheels dominated the market, accounting for nearly 43% of the total volume due to widespread use in passenger cars and light commercial vehicles. Their affordability, ease of manufacturing, and compatibility with various vehicle types make them the preferred choice for OEMs in emerging economies. However, the fastest-growing segment is tubeless steel wheels, particularly in the commercial transport and logistics sectors. Tubeless designs reduce puncture risks and maintenance frequency, offering operational advantages. In 2024, demand for tubeless wheels surged by 18% year-on-year in the Asia-Pacific region. Split rim and tube-type wheels remain relevant in niche applications such as agricultural machinery and trailers, where specific load-bearing and inflation requirements persist. Manufacturers are focusing on innovative forming techniques and hybrid steel-alloy solutions to diversify their offerings in each type segment.

In terms of application, the automotive steel wheels market is segmented into OEM and aftermarket. In 2024, the OEM segment held the largest share, contributing approximately 59% of total global demand. This dominance is driven by the high-volume manufacturing of budget and mid-range vehicles equipped with steel wheels by default, particularly in Asia-Pacific and Latin America. Steel wheels are preferred for their low cost and durability, especially for cars intended for challenging terrains and urban logistics. However, the aftermarket segment is witnessing faster growth, especially in North America and Europe. Seasonal tire changes, wheel damage replacement, and increasing vehicle age are driving demand in this category. In 2024, aftermarket sales of steel wheels grew by 13% year-on-year. The segment also benefits from the rise in DIY vehicle maintenance culture and localized production hubs, which allow for quick turnaround on replacements. Aftermarket players are offering corrosion-resistant and aesthetic steel wheel options to appeal to value-focused consumers.

The automotive steel wheels market serves various end-user categories including individual consumers, commercial fleet operators, public transportation services, and government/military sectors. Among these, individual consumers remain the largest end-user group, accounting for 46% of global sales in 2024. This is due to the wide adoption of steel wheels in entry-level and mid-range personal vehicles, particularly in developing markets. However, the fastest-growing segment is commercial fleet operators, driven by rising logistics and last-mile delivery operations. Fleet managers prefer steel wheels for their durability, low maintenance costs, and resistance to impact damage. In 2024, commercial usage of steel wheels increased by 15% globally. Public transportation systems, including buses and municipal vehicles, also contribute significantly to the market, especially in urban centers where steel wheels help minimize operational downtime. Meanwhile, the military and defense sector demand reinforced steel wheels tailored to off-road and rugged applications, representing a stable, though smaller, segment with specialized procurement cycles.

Asia-Pacific accounted for the largest market share at 42.7% in 2024, however, South America is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2025 and 2032.

The Asia-Pacific region leads due to its high vehicle production volume, cost-sensitive consumer base, and extensive adoption of steel wheels in entry-level cars and two-wheelers. Countries like China and India are major contributors, with growing commercial and passenger vehicle fleets. Meanwhile, South America is witnessing increasing investments in infrastructure and local vehicle production. This trend, coupled with rising automotive exports from Brazil and Argentina, is accelerating the demand for affordable, durable steel wheels. In addition, OEM partnerships with local manufacturers are stimulating regional wheel production. Europe and North America continue to maintain steady growth, largely driven by aftermarket sales and cold-weather applications, while the Middle East & Africa region sees rising adoption in off-road and utility vehicles. Each region reflects distinct demand dynamics based on climate, economic factors, and vehicle fleet composition.

"Aftermarket Demand and Seasonal Wheel Swaps Driving Steel Wheel Sales"

The North American automotive steel wheels market is heavily influenced by strong aftermarket demand, particularly in the U.S. and Canada. In 2024, over 62% of steel wheel sales in the region were attributed to the replacement segment, driven by seasonal tire changes and rising used vehicle ownership. In colder states, consumers prefer steel wheels for winter tire mounting due to their ruggedness and cost-efficiency. Additionally, light trucks and SUVs—common in the U.S.—increasingly adopt steel wheels for base trims and fleet models. Mexico contributes through OEM production facilities supplying steel wheels for both domestic and export markets. With rising repair and maintenance activity and an aging vehicle fleet, aftermarket opportunities continue to grow, especially for corrosion-resistant steel wheel variants. Manufacturers are also developing aesthetic steel wheel designs to capture the attention of budget-conscious drivers seeking alternatives to alloy wheels.

"Steel Wheels Preferred in Cold-Climate and Entry-Level Car Markets"

Europe maintains steady steel wheel adoption driven by cold-climate countries and a strong aftermarket culture. In 2024, Germany, Poland, and Russia collectively contributed over 47% of the region’s steel wheel consumption. Steel wheels are a preferred option for winter tire sets, especially in Northern and Eastern Europe, where harsh winters necessitate seasonal wheel swaps. Additionally, rising demand for economical city cars and compact electric vehicles (EVs) in countries like Italy and France has kept OEM steel wheel installation strong. EU regulations supporting circular economy principles have also prompted refurbishment and resale of steel wheels, boosting aftermarket volume. Regional automakers are optimizing wheel supply chains by sourcing steel domestically, while production hubs in Turkey and Eastern Europe serve as cost-effective manufacturing bases. Fleet leasing companies across the continent also prefer steel wheels due to their low replacement costs and high impact resistance.

"OEM Vehicle Production and Rural Mobility Fueling Market Growth"

Asia-Pacific dominates the global automotive steel wheels market due to its vast automotive production base and rising two-wheeler and utility vehicle demand. In 2024, China alone accounted for 31.6% of global steel wheel production, followed by India at 18.4%. Steel wheels are commonly used in subcompact passenger vehicles, small commercial vans, and three-wheelers catering to rural logistics and daily transport. Regional OEMs like Maruti Suzuki, Geely, and Hyundai are major adopters of steel wheels in base trims. Furthermore, ongoing rural road development programs in Southeast Asia are encouraging vehicle ownership, particularly of durable, low-maintenance vehicles equipped with steel wheels. The two-wheeler segment, especially motorcycles and mopeds, is also a significant contributor to steel wheel demand. Localized manufacturing and government incentives for affordable vehicles continue to bolster market strength. Emerging economies like Indonesia and Vietnam are rapidly scaling up automotive assembly plants that rely heavily on steel wheels for price-sensitive consumer markets.

"Revival of Local Manufacturing Boosting Steel Wheel Adoption"

South America is emerging as the fastest-growing market for automotive steel wheels, with Brazil and Argentina leading the charge. In 2024, Brazil held a 58.2% share of regional steel wheel production, fueled by government support for automotive industrialization and export incentives. OEMs in the region are increasing their focus on low-cost vehicles for domestic and export markets, particularly to Africa and Central America. Steel wheels are extensively used in these models to keep production economical and enhance durability on variable road conditions. Argentina, benefiting from trade agreements and vehicle assembly contracts, contributed over 27% to the region’s demand. The aftermarket is also expanding, as aging vehicles and commercial fleets across rural and urban areas require frequent wheel replacements. Increased mining and agriculture-based transportation is further stimulating the use of reinforced steel wheels in utility and cargo vehicles. Local manufacturers are ramping up production to reduce reliance on imports and improve regional self-sufficiency.

"Rugged Terrain and Military Vehicle Demand Sustaining Steel Wheel Usage"

The Middle East & Africa region continues to exhibit rising demand for automotive steel wheels, particularly in segments involving off-road, commercial, and defense vehicles. In 2024, Saudi Arabia and South Africa jointly accounted for 63.4% of regional market share. Steel wheels are preferred in arid environments where sand, gravel, and extreme temperatures degrade lighter alloys. Military-grade vehicles, mining trucks, and agricultural transport frequently employ thick-gauge steel wheels designed for harsh operational conditions. South Africa remains a major manufacturing and distribution hub, catering to domestic and neighboring African markets. In the Middle East, increasing demand for cost-efficient fleet vehicles used in construction and infrastructure projects is supporting the use of steel wheels. Importers and regional suppliers are introducing customized variants with impact-resistant rims and bead lock designs for all-terrain use. Additionally, government fleet modernization programs are fueling orders for standardized utility vehicles equipped with steel wheels.

The global Automotive Steel Wheels market is highly consolidated with a mix of longstanding manufacturers and regional specialists vying for competitive advantage. The top five players collectively accounted for over 55% of the global market share in 2024. These companies are focusing on strategic expansions, product differentiation, and long-term contracts with leading automakers to strengthen their foothold. Innovation in lightweight steel wheel designs has become a key area of competition, especially among suppliers to passenger and light commercial vehicle OEMs. Additionally, companies are leveraging cost-effective manufacturing processes and increasing investment in fully automated wheel production facilities to reduce labor dependencies and boost volume efficiency.

Asian players dominate the production landscape due to favorable manufacturing costs and strong domestic demand. European manufacturers, meanwhile, are focusing on premium-grade wheels, supplying to luxury and performance vehicle segments. North American competitors are emphasizing sustainability, incorporating recycled materials and compliance with advanced emission norms. Strategic alliances with EV manufacturers are also emerging as a competitive lever, aiming to supply wheels compatible with regenerative braking and low-noise requirements of electric platforms.

Maxion Wheels

Steel Strips Wheels Ltd.

Topy Industries Limited

Iochpe-Maxion

Zhejiang Jingu Co., Ltd.

Accuride Corporation

Klassic Wheels Ltd.

ALCAR Group

Suzhou Zhengxing Wheel Co., Ltd.

Jantsa Jant Sanayi ve Ticaret A.S.

Technological evolution in the automotive steel wheels market is accelerating rapidly, with manufacturers focusing on lighter, stronger, and more durable steel wheel solutions. Advanced metallurgy techniques such as micro-alloying and heat treatment are enabling the production of wheels that offer enhanced fatigue strength while reducing overall vehicle weight. This weight reduction directly contributes to improved fuel economy and lower CO₂ emissions, making steel wheels a competitive alternative to alloy wheels in price-sensitive markets.

Cold forming and flow-forming processes are being adopted at scale, allowing for thinner rim walls without compromising structural integrity. Automated robotic welding systems are also being integrated into production lines to improve consistency and reduce manufacturing defects. Furthermore, the introduction of corrosion-resistant coatings and eco-friendly painting technologies ensures extended lifecycle performance under harsh environmental conditions.

Steel wheels tailored for electric vehicles are another innovation focus, with design adaptations for low rolling resistance and compatibility with regenerative braking systems. Smart manufacturing practices, including IoT-enabled monitoring and AI-driven quality inspection systems, are being implemented to minimize downtime and improve production yield. These advancements are setting new industry benchmarks in terms of safety, efficiency, and sustainability.

In October 2023, Steel Strips Wheels Ltd., an India-based manufacturer of steel wheel rims, acquired AMW Auto Component Limited for $16.5 million. This acquisition aims to strengthen Steel Strips' position in the automotive components sector by leveraging AMW Auto Component's expertise and production capabilities.

In September 2023, Maxion Wheels, a global leader in wheel manufacturing, unveiled its latest innovation, the Maxion BIONIC wheel, at the IAA Mobility event in Germany. This new light vehicle wheel design focuses on reducing weight without compromising strength, aiming to enhance fuel efficiency and lower CO₂ emissions in passenger vehicles.

In February 2024, Austrian steelmaker Voestalpine revised its annual EBITDA guidance downward due to a significant decline in core profit, largely attributed to weak demand in Europe's automotive and construction sectors. The company's steel division experienced a sharp drop in demand following profit warnings from car manufacturers, with a continuous fall in steel prices over the first nine months of the fiscal year ending March 2025.

In April 2024, Cleveland-Cliffs, a major U.S. steel producer, reported benefiting from reduced costs and strong demand from the automotive sector in the second quarter. The company's President and CEO highlighted that despite a temporary strike from service centers, the resilience of U.S. automotive production positively impacted first-quarter results. Cleveland-Cliffs also secured significant federal grants for decarbonization, directed towards two major projects with substantial carbon reduction potential.

The Automotive Steel Wheels Market Report offers a comprehensive analysis of the global market, focusing on key aspects such as market size, segmentation, and regional insights. The report delves into various segments, including vehicle type, rim size, end-user, and regions, providing a detailed understanding of the market dynamics.In terms of vehicle type, the report covers passenger cars and commercial vehicles, highlighting the demand trends and growth prospects in each segment. The rim size segment includes 12”–17”, 18”–21”, and more than 22”, offering insights into the preferences and requirements of different vehicle categories. The end-user segment comprises OEM and aftermarket, analyzing the supply chain and distribution channels in the market.

Regionally, the report encompasses North America, Europe, Asia Pacific (APAC), Latin America (LATAM), and the Middle East and Africa (MEA), examining the market trends, opportunities, and challenges in each region. The report also profiles key players in the market, such as Central Motor Wheel of America, Inc., MAXION Wheels, Klassic Wheels Limited, Accuride Corporation, U.S. WHEEL CORP., Automotive Wheels Ltd, ALCAR WHEELS GMBH, Topy America, Inc., The Carlstar Group, LLC, and Steel Strips Group, providing an overview of their strategies and market positioning. Overall, the Automotive Steel Wheels Market Report serves as a valuable resource for stakeholders, offering in-depth insights into the market's current status and future outlook.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 5150 Million |

|

Market Revenue in 2032 |

USD 7493.72 Million |

|

CAGR (2025 - 2032) |

4.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Maxion Wheels, Steel Strips Wheels Ltd., Topy Industries Limited, Iochpe-Maxion, Zhejiang Jingu Co., Ltd., Accuride Corporation, Klassic Wheels Ltd., ALCAR Group, Suzhou Zhengxing Wheel Co., Ltd., Jantsa Jant Sanayi ve Ticaret A.S. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |