Reports

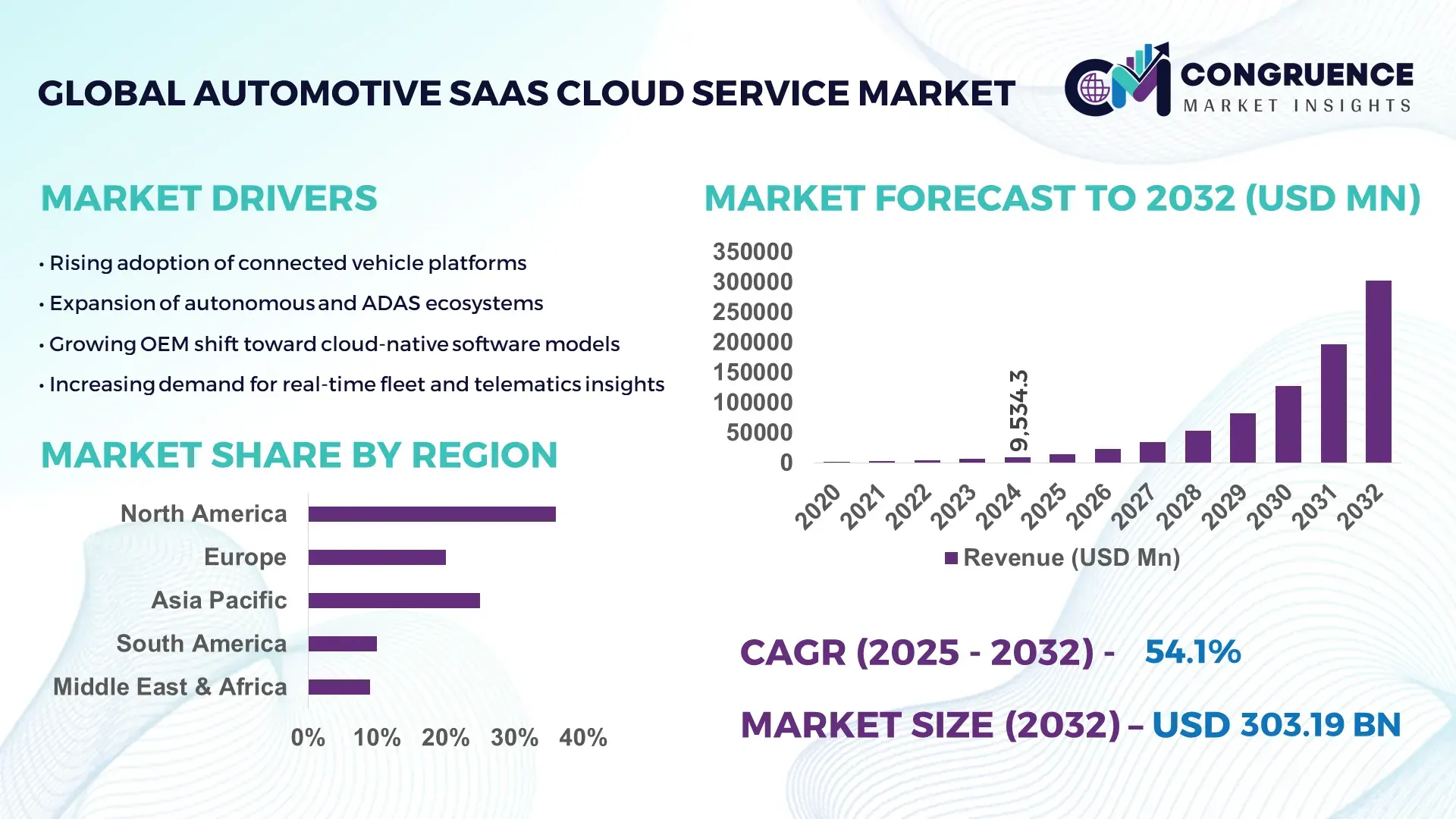

The Global Automotive SaaS Cloud Service Market was valued at USD 9,534.34 Million in 2024 and is anticipated to reach a value of USD 303,187.95 Million by 2032, expanding at a CAGR of 54.1% between 2025 and 2032. This growth is primarily driven by accelerating adoption of connected‑vehicle platforms and increasing integration of cloud‑native telematics solutions across OEMs globally.

In the United States, the automotive software cloud ecosystem has witnessed over USD 2.4 billion in direct investment during 2024, with more than 350 million vehicle-miles managed via cloud-based fleet telematics services. Leading OEMs have deployed integrated cloud‑SaaS platforms capable of processing up to 1 petabyte of driving and diagnostic data monthly, enabling predictive maintenance and OTA updates. U.S.-based commercial fleet operators report average operational-cost reductions of 18–24% after migrating to SaaS cloud solutions, reflecting high production capacity, deep capital investment, and advanced application of AI-enabled analytics and real-time vehicle data orchestration.

• Market Size & Growth: USD 9,534.34 M in 2024 → USD 303,187.95 M by 2032, CAGR 54.1%; fueled by surging demand for connected-car software ecosystems.

• Top Growth Drivers: adoption of connected-fleet SaaS platforms (45%), regulatory compliance automation (30%), scalable cloud infrastructure cost savings (25%).

• Short-Term Forecast: By 2028, average fleet software maintenance costs expected to decrease by 22%.

• Emerging Technologies: Edge-computing integration with cloud SaaS, AI-powered predictive maintenance, OTA update orchestration.

• Regional Leaders: North America projected ~USD 115 B by 2032 — early cloud-native adoption; Europe ~USD 82 B — strong regulatory push; Asia-Pacific ~USD 70 B — rapid EV & mobility-as-a-service uptake.

• Consumer/End-User Trends: OEMs, commercial fleet operators, mobility services increasingly rely on cloud platforms; usage patterns favor subscription-based telematics and real-time diagnostics.

• Pilot or Case Example: In 2025, a major U.S. automotive OEM deployed a cloud SaaS telematics system reducing fleet downtime by 18%.

• Competitive Landscape: Market leader holds ~28% share; major competitors include three to five established global SaaS automotive vendors.

• Regulatory & ESG Impact: Emissions tracking mandates, data privacy laws, and incentives for efficient telematics adoption accelerate SaaS deployment.

• Investment & Funding Patterns: Over USD 4.2 B invested globally in 2024; growing venture funding and project financing support cloud-native automotive solutions.

• Innovation & Future Outlook: Trends include integration with 5G, autonomous driving data pipelines, hybrid edge-cloud architectures, and subscription-based mobility-software bundles.

Automotive SaaS cloud services are increasingly adopted across connected vehicles, fleet management, mobility services, and after-sales diagnostics. Recent innovations include AI-driven predictive maintenance, real-time OTA software update orchestration, and edge-cloud hybrid architectures enabling ultra-low-latency telematics. Regulatory drivers such as emissions compliance, data security laws, and government incentives for efficient fleet operations shape broader adoption. Regionally, growing EV penetration in Asia-Pacific, strong fleet modernization in North America, and regulatory alignment in Europe drive demand. Emerging trends point to deeper integration with autonomous platforms, mobility-as-a-service models, and utilization-based subscription licensing, indicating a robust outlook for SaaS-based automotive cloud solutions through 2032.

The strategic relevance of the Automotive SaaS Cloud Service Market stems from its capacity to transform vehicle and fleet operations into dynamic, data-driven, and scalable platforms that generate measurable operational efficiency and compliance advantages. The edge‑cloud hybrid telemetry platform delivers 35% improvement in data processing latency compared to legacy on‑premises telematics servers, enabling real‑time diagnostics, predictive maintenance, and rapid over‑the‑air updates. North America dominates in volume, while Asia‑Pacific leads in adoption with approximately 60% of new commercial fleets onboarded to SaaS platforms. By 2027, integration of AI-powered predictive maintenance is expected to cut fleet downtime by up to 28%, significantly improving uptime reliability and maintenance KPI metrics. Firms are committing to ESG goals such as a 15% reduction in carbon emissions per vehicle by 2028 through optimized driving patterns and efficient telematics-enabled route planning. In 2025, a major European logistics operator achieved a 22% reduction in fuel consumption through deployment of cloud‑based route optimization and predictive maintenance SaaS services. These trends underscore that Automotive SaaS Cloud Service is not simply a cost-reduction tool but a strategic backbone for resilience, regulatory compliance, and sustainable growth across automotive, mobility, and logistics sectors worldwide.

Demand for real-time fleet analytics has surged as commercial fleet operators, ride‑sharing providers, and logistics firms increasingly focus on operational efficiency, safety, and predictive maintenance. Real-time analytics supports continuous monitoring of vehicle health, driver behavior, route optimization, and fuel consumption — enabling cost savings, lower downtime, and enhanced safety oversight. Organizations utilizing SaaS‑based analytics platforms report up to 20% fewer unscheduled maintenance events within the first 12 months and roughly 15% lower fuel consumption through optimized routing and driving behavior. The ability of SaaS platforms to onboard new vehicles rapidly without heavy infrastructure investment allows fleet scaling with minimal overhead, making growth economically viable. This demand for actionable, real-time insight strongly accelerates adoption of cloud SaaS platforms across diverse mobility segments, driving market expansion and migration from legacy systems.

Although Automotive SaaS Cloud Service platforms offer powerful analytics and connectivity, rising concerns about data privacy, regulatory compliance, and cross-border data transfer impose significant restraints. Diverse jurisdictions enforce different data‑protection laws and vehicle tracking regulations. Telematics data — including driver behavior, location history, and vehicle maintenance logs — can be subject to strict storage, anonymization, or user consent requirements, complicating unified global deployments. The associated compliance burden increases operational complexity and may delay platform rollout or require costly adaptations. Operators in regions with stringent data‑residency or telematics regulation may hesitate to adopt cloud-based systems. This regulatory variability and privacy risk can limit full-scale SaaS adoption, slowing conversion from legacy or on‑premises telemetry solutions and reducing overall market penetration.

The shift toward electric vehicles (EVs), shared mobility, and mobility-as-a-service (MaaS) models presents substantial opportunity for Automotive SaaS Cloud Service solutions. EV fleets generate unique data streams — battery health, charge cycles, energy consumption, regenerative braking metrics — requiring specialized cloud analytics and management tools. SaaS platforms tailored for EV fleets can offer battery monitoring, charging‑station scheduling, energy‑use optimization, and maintenance forecasting, addressing a growing need as EV adoption rises globally. Shared mobility and MaaS operators require dynamic fleet allocation, real‑time usage tracking, predictive maintenance, and flexible billing — all supported by SaaS cloud architectures. As urban mobility policies evolve and fleet electrification accelerates, demand for scalable SaaS solutions tailored to EV and shared‑mobility operations is expected to grow substantially, offering vendors a major growth runway.

Many existing fleets and OEM operations rely on legacy infrastructure — on‑prem telematics servers, proprietary software stacks, and non‑standardized data formats. Migrating from such heterogeneous, entrenched systems to modern cloud SaaS solutions raises integration complexity, potential downtime, data migration risks, and training overhead. Older vehicles lacking modern connectivity hardware cannot readily generate necessary telemetry data without retrofit investments. This retrofit cost, along with compatibility issues and varied hardware standards, presents a significant barrier, especially for small to mid‑size operators with limited capital. Integration hurdles are compounded when multiple regional regulations, hardware standards, and OEM data protocols must be reconciled, increasing deployment timelines and costs. As a result, some operators remain reluctant to commit to full SaaS migration, limiting market penetration and slowing adoption rates despite clear long-term benefits.

• Expansion of AI-Driven Predictive Maintenance: AI-powered predictive maintenance platforms are increasingly deployed in fleets, with over 62% of commercial fleets adopting AI algorithms for real-time diagnostics and failure prevention. These systems reduce unplanned downtime by up to 28% and optimize maintenance scheduling, enabling operators to save 15–20% on operational costs while improving vehicle lifespan and fleet reliability.

• Growth in OTA Software Updates and Remote Vehicle Management: Over-the-air (OTA) software deployment has become standard in connected vehicles, with 45% of new models in North America and Europe supporting automated OTA updates. This trend minimizes physical service visits, reducing downtime by 18% and improving feature rollout speed by 35% compared to traditional manual updates. Adoption is accelerating in fleet and mobility-as-a-service segments where operational continuity is critical.

• Increasing Integration of Edge Computing with Cloud SaaS: Automotive SaaS platforms are integrating edge computing to handle high-volume sensor data in real-time. Around 58% of telematics data is now processed at the edge before cloud aggregation, reducing latency by 33%. This is particularly critical for autonomous vehicle trials and high-speed fleet monitoring in regions like Asia-Pacific and North America.

• Adoption of Subscription-Based and Modular Fleet Management Models: Flexible, subscription-based SaaS solutions are replacing traditional licensing, with over 40% of medium-to-large fleets adopting modular, pay-as-you-go platforms. These models enable operators to scale systems rapidly, reduce upfront investments by 20–25%, and align software capabilities with evolving operational needs, particularly in shared mobility and urban logistics markets.

The market segmentation for Automotive SaaS Cloud Service can be meaningfully structured by type of service, application domain, and end‑user category. Service types vary from fleet management and telematics SaaS platforms to over‑the‑air (OTA) update services, predictive maintenance, connected infotainment, and usage‑based insurance telematics. Applications span commercial fleets, ride‑sharing and shared mobility, OEM software management, insurance telematics, and consumer after‑sales services. End‑users include logistics and transport companies, mobility service providers, vehicle manufacturers (OEMs), insurance firms, and vehicle owners seeking connected vehicle services. Distinct segmentation helps stakeholders tailor solutions, investments, and go‑to‑market strategies based on demand patterns, operational scale, and regulatory or mobility‑as‑a‑service trends.

The dominant service type in this market is fleet management and telematics platforms, accounting for approximately 38% share of all Automotive SaaS Cloud Service deployments. This leadership is due to the widespread need among commercial transport operators for real‑time vehicle tracking, fleet utilization analytics, and operational scheduling. The fastest‑growing type is over‑the‑air (OTA) software update services, which currently exhibit a 22% CAGR, driven by increasing demand for remote diagnostics, recall management, and feature upgrades without requiring physical workshop visits. Connected infotainment and navigation services contribute around 18%, offering value in consumer vehicles and shared mobility fleets. Predictive maintenance and diagnostics services hold about 12%, serving operators wanting to reduce unplanned breakdowns, while usage‑based insurance telematics and value‑added services fill the remaining 10% share.

Commercial fleet operations remain the leading application area, representing roughly 44% of total service utilization, as logistics companies and transport providers rely on cloud‑based telematics and management platforms for scheduling, route optimization, and fleet oversight. The fastest-growing application is ride‑hailing and shared mobility fleet management, with a 25% CAGR, fueled by urbanization, mobility‑as‑a‑service (MaaS) expansion, and increasing EV‑fleet adoption in urban centers. Other application segments include OEM software lifecycle management (about 15%), insurance usage‑based telematics (12%), and consumer after‑sales connected services (9%).

Logistics and commercial fleet companies constitute the largest end‑user segment, with about 41% share, as these organizations derive the highest operational benefit from telematics, maintenance scheduling, and fleet management suites. The fastest-growing end‑user segment is ride‑hailing and mobility‑as‑a‑service providers, experiencing a 27% CAGR, driven by rising urban mobility demand and fleet electrification. Other important end‑users include OEMs and vehicle manufacturers (20%), insurance companies leveraging usage‑based telematics (18%), and after‑sales service providers or dealers (10%).

North America accounted for the largest market share at ~35–42% in 2024; however, Asia‑Pacific is expected to register the fastest growth, expanding at a higher pace between 2025 and 2032.

The global distribution shows North America leading, followed by Europe, Asia‑Pacific, Latin America, and Middle East & Africa, with Asia‑Pacific gaining momentum due to rising vehicle connectivity demand and expanding manufacturing and fleet penetration. In 2024, Asia‑Pacific’s share of automotive cloud‑SaaS deployments was estimated at about 26%, while North America remained dominant with roughly 35%. The shift toward electric vehicles (EVs), connected fleets, and smart mobility in Asia‑Pacific—especially in countries like China, India, and Japan—is boosting cloud SaaS adoption. Meanwhile, in North America, mature vehicle fleets, advanced regulatory compliance requirements, and dense connected‑vehicle infrastructure sustain high volumes. This regional variation underscores both established demand in mature markets and rapid growth potential in emerging regions, offering strategic opportunities for SaaS providers focusing on scalability, localization, and regional compliance.

What Makes North America a Hub of Advanced Fleet Connectivity?

North America holds approximately 35–38% share of the global Automotive SaaS Cloud Service market. Demand is driven primarily by commercial fleets, logistics and delivery services, ride‑sharing networks, and OEMs deploying cloud‑based telematics and fleet management. Regulatory emphasis on vehicle safety, emissions tracking, and telematics compliance encourages broader adoption of cloud platforms. Technological transformation is supported by widespread 5G and high broadband penetration, enabling real‑time data collection, OTA updates, and predictive maintenance. Local cloud‑service providers and telematics vendors collaborate with automakers and fleet operators to offer integrated solutions; for instance, major fleet‑management companies leverage cloud SaaS to manage over 65 million vehicles with optimized routing and diagnostics. Enterprise adoption is strong, particularly among large logistics firms and commercial operators, reflecting a shift from one‑time software installs to subscription‑based, scalable services tailored for high-volume fleets.

How Is Europe Shaping SaaS Adoption Through Regulation and Innovation?

Europe accounts for roughly 29–30% of the global Automotive SaaS Cloud Service market. Key markets include Germany, the UK, France, Italy, and Spain — all showing steady demand for cloud‑based fleet management, telematics, and connected‑car services. Strict environmental regulations, emissions control mandates, data privacy laws, and safety compliance requirements drive demand for secure, standardized cloud platforms. European OEMs and fleet operators increasingly adopt enterprise-grade cloud solutions for predictive maintenance, energy optimization (especially for EV fleets), and data‑compliance reporting. Technological adoption includes hybrid cloud and private-cloud deployments to satisfy data‑residency and compliance needs. Several regional players collaborate with OEMs to deploy telematics services across fleets and consumer vehicles, adapting cloud SaaS offerings to meet European compliance standards. Consumer behavior reflects strong demand for structured, transparent, and privacy‑compliant connected‑vehicle services, particularly in urban mobility and commercial transportation segments.

Why Is Asia‑Pacific Emerging as the Fastest Growing Automotive Cloud Region?

Asia‑Pacific represents roughly 26% of the global Automotive SaaS Cloud Service market as of 2024 and ranks as the fastest-growing region over 2025–2032. Leading countries driving demand include China, India, Japan, and South Korea. The region’s growth is propelled by rapid urbanization, rising vehicle production, expansion of commercial fleets, and growing interest in connected mobility and EV adoption. Infrastructure investments in 5G networks, smart‑city initiatives, and urban logistics modernization support cloud‑native telematics and fleet‑management deployments. Local telematics and SaaS vendors collaborate with OEMs to integrate cloud platforms into both new vehicles and retrofitted fleets. In countries like India and China, rising consumer demand for affordable connected services and mobility‑as‑a‑service models drives uptake among private and commercial users alike. The regional consumer behavior shows preference for scalable, cost‑effective subscription‑based SaaS solutions rather than heavy upfront investments, especially among small and mid‑size fleet operators and mobility service providers.

Could South America Define a New Growth Frontier for Connected Fleets?

In South America — with key countries like Brazil and Argentina — the adoption of Automotive SaaS Cloud Services remains nascent but shows promising growth potential. The regional market share remains modest relative to established regions but is gradually increasing due to rising vehicle ownership, expanding logistics and delivery services, and interest in fleet optimization solutions. Infrastructure improvements and trade‑policy liberalization are encouraging fleet operators to explore cloud‑based telematics and fleet‑management platforms. Local players and service providers are beginning to offer tailored SaaS solutions addressing regional needs — such as route optimization for varying terrain, fuel‑efficiency tracking, and usage‑based insurance telematics. Consumer behavior leans toward pragmatic solutions: fleets and businesses prioritize cost‑efficiency, maintenance predictability, and flexible subscription terms over large upfront software investments.

Is Middle East & Africa Poised for a Connected-Fleet Upsurge?

In Middle East & Africa, the market share in 2024 remains relatively small but is gradually growing, as regional demand emerges in oil & gas logistics, transport, and urban mobility services. Major growth countries include UAE, Saudi Arabia, South Africa, and a few Gulf Cooperation Council (GCC) states. Technological modernization trends — including deployment of telematics for fleet management, cargo monitoring, and remote diagnostics — are gaining traction. Government‑backed smart‑transport and smart‑city programs are encouraging adoption, along with trade partnerships that facilitate import of telematics hardware and SaaS platforms. Local enterprises increasingly leverage cloud‑based fleet services to optimize logistics, track vehicles across long‑distance routes, and manage regional transport challenges. Regional consumer behavior reflects demand from logistics operators, freight companies, and transport services rather than individual vehicle owners, with emphasis on reliability, low‑maintenance, and remote‑management capabilities.

United States — ~24–25% share in global Automotive SaaS Cloud Service market; dominance driven by advanced automotive manufacturing, high fleet density, and early adoption of connected‑vehicle technologies.

China — ~14–16% share (within Asia‑Pacific leading segment); large and growing vehicle parc, aggressive investment in connected mobility infrastructure, and rising EV and fleet telematics adoption.

The Automotive SaaS Cloud Service market is characterized by a moderately consolidated competitive structure, with the top five players collectively accounting for approximately 38–45% of total market influence. The broader ecosystem includes more than 55–65 active competitors globally, spanning cloud-native SaaS vendors, telematics providers, connected-vehicle technology firms, and OEM-backed software divisions. Competitive pressure is shaped by rapid innovation cycles, with companies launching an estimated 120+ new software updates, platform enhancements, and AI-enabled analytics features annually. Strategic partnerships remain a core differentiator, with over 40% of leading players engaging in collaborations with automakers, telecom operators, and cloud-infrastructure providers. The market is witnessing an uptick in M&A transactions, particularly in advanced telematics, cybersecurity, and predictive-analytics capabilities, as companies attempt to strengthen vertical integration. Competition is also influenced by the rising demand for scalable subscription models, resulting in accelerated investment in API-driven architectures and cross-platform interoperability. With increasing emphasis on fleet automation, remote diagnostics, and EV-charging analytics, vendors that offer integrated and modular SaaS solutions are gaining measurable competitive advantage across both emerging and mature regions.

Bosch Mobility

Siemens Digital Industries Software

Continental AG

Harman International

BlackBerry QNX

Aptiv

Trimble

TomTom

Airbiquity

Garmin

Geotab

Wind River

KPIT Technologies

TTTech Auto

The Automotive SaaS Cloud Service market is being reshaped by rapid advancements in connected vehicle platforms, AI-driven mobility solutions, edge-to-cloud integrations, and cybersecurity frameworks tailored for automotive environments. A major technological shift is being driven by the rising adoption of software-defined vehicles (SDVs), with over 70% of new global vehicle models now incorporating SDV-ready electronic architectures that support continuous over-the-air (OTA) updates, cloud-native applications, and centralized compute platforms. Automakers are increasingly deploying domain and zonal controller architectures that streamline software management and reduce system complexity, enabling faster integration of third-party SaaS solutions. AI and machine learning technologies are now embedded across vehicle health monitoring, ADAS calibration, real-time analytics, and predictive maintenance services. More than 55% of new connected vehicles launched in 2023–2024 include AI-powered diagnostics or data-driven service automation. The growth of V2X communication frameworks, supported by 5G rollouts in key markets such as the U.S., China, and Europe, is accelerating the demand for cloud platforms capable of managing high-throughput, low-latency data streams between vehicles, infrastructure, and backend systems.

The emergence of edge cloud computing is reducing latency in mission-critical automotive functions, enabling sub-10 millisecond response times for connected mobility applications. This is further complemented by containerization and microservices architectures that allow SaaS providers to deliver modular, scalable applications for fleet operations, navigation, cybersecurity, and infotainment ecosystems. Cybersecurity technologies have also become central to SaaS cloud platforms, with over 65% of OEMs adopting secure OTA frameworks, encryption-based telematics modules, and intrusion detection systems designed specifically for connected vehicles. Additionally, digital twin simulations, API-driven integration frameworks, and cross-OEM interoperability standards are gaining traction, supporting large-scale data harmonization across mobility ecosystems. Overall, the market is moving toward a fully cloud-native, AI-oriented technology stack that prioritizes scalability, automation, and real-time intelligence for next-generation automotive services.

The Automotive SaaS Cloud Service Market Report provides comprehensive coverage of the ecosystem surrounding cloud-delivered automotive software services. It examines key solution categories including telematics and fleet-management platforms, OTA and FOTA update systems, connected-infotainment applications, predictive-maintenance analytics, usage-based insurance telematics, and data-service APIs. The scope extends across major application areas such as commercial transport fleets, ride-hailing and shared-mobility operators, OEM software lifecycle management, insurance underwriting and risk assessment, dealer service networks, and municipal mobility programs. Geographically, the report spans North America, Europe, Asia-Pacific, South America, the Middle East, and Africa, incorporating country-level assessments for more than 20 significant markets. It includes comparative insight into connected-vehicle penetration, telematics adoption levels, regulatory requirements, and digital-mobility readiness across regions.

Technology coverage includes cloud-native architectures, edge-computing deployments achieving sub-10 ms processing latency, V2X and 5G-enabled data ecosystems, AI-powered maintenance diagnostics, cybersecurity and secure-OTA frameworks, containerized microservices, digital-twin modeling for fleet operations, and standardization initiatives enabling cross-OEM interoperability. The report evaluates operational performance indicators such as reduction in unplanned downtime, improvements in route efficiency, increases in telematics utilization rates, and measurable enhancements in software-deployment cycles.

It also outlines commercial models—modular subscription plans, usage-based SaaS licensing, and integration economics for retrofitting legacy fleets—together with industry-specific requirements for logistics, last-mile delivery, rental fleets, and EV-centric mobility operators. Additionally, it covers M&A activity, strategic partnerships, vendor benchmarking across more than 50 active competitors, and over 120 documented platform enhancements introduced between 2023 and 2024. The scope emphasizes emerging segments including autonomous-fleet data orchestration, EV battery-cloud services, and AI-driven mobility-risk analytics, providing decision-grade evaluation for procurement, investment planning, and long-term product strategy.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 9534.34 Million |

|

Market Revenue in 2032 |

USD 303187.95 Million |

|

CAGR (2025 - 2032) |

54.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bosch Mobility , Siemens Digital Industries Software , Continental AG, Harman International, BlackBerry QNX , Aptiv, Trimble, TomTom, Airbiquity, Garmin, Geotab, Wind River, KPIT Technologies, TTTech Auto |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |