Reports

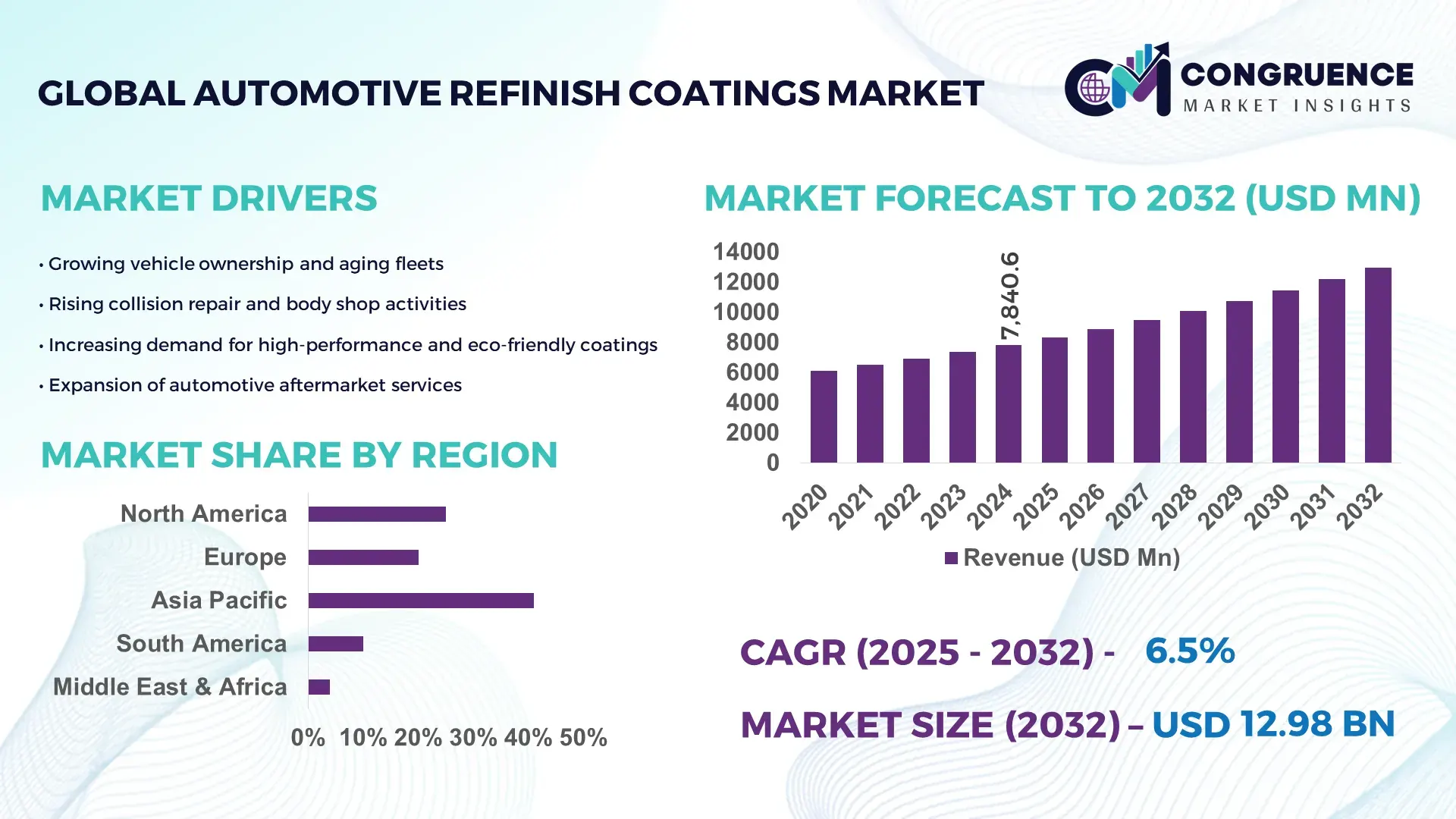

The Global Automotive Refinish Coatings Market was valued at USD 7840.55 Million in 2024 and is anticipated to reach a value of USD 12976.08 Million by 2032 expanding at a CAGR of CAGR of 6.5%% between 2025 and 2032. This growth is largely driven by rising demand for vehicle repair, refurbishment, and enhanced durability in aging vehicle fleets worldwide.

China continues to lead the market in scale and infrastructure for automotive refinish coatings. In 2024, China operated more than 12 large-scale refinish-coating manufacturing facilities with a combined annual production capacity of approximately 450,000 tonnes. Between 2022 and 2024, government-backed investment programmes injected about USD 420 million to modernize production lines and adopt advanced water-borne and low-VOC coating technologies. Major applications include collision-repair centres and multi-brand service workshops, which account for around 65 % of output usage. Chinese manufacturers have recently started rolling out nano-ceramic binder technologies that improve scratch resistance and shorten cure-times by 15–20 %.

Market Size & Growth: Current market valued at USD 7,840.55 M, projected to reach USD 12,976.08 M by 2032; 6.5 % CAGR driven by accelerating repair-and-refinish demand and stricter emission standards.

Top Growth Drivers: rising vehicle maintenance frequency (+28 %), greater adoption of eco-friendly paints (+22 %), increasing fleet refurbishment activities (+35 %).

Short-Term Forecast: By 2028, expected average refinish-coating formulation cost reduction of 12 % and performance gains (durability & gloss retention) of 18 %.

Emerging Technologies: water-borne/co-solvent-borne coatings, low-VOC and ultra-low-VOC formulations, nano-ceramic and polymer-enhanced coatings improving scratch resistance and curing speed.

Regional Leaders: Asia-Pacific – USD 4,750 M by 2032 (rapid adoption in China and India); Europe – USD 2,200 M (stricter emissions & environmental regulations); North America – USD 1,800 M (expanding aftermarket and collision-repair demand).

Consumer/End-User Trends: Growth concentrated in collision-repair workshops, fleet refurbishment services and used-vehicle reconditioning; rising preference for quick-dry and environmentally compliant coatings.

Pilot or Case Example: In 2023, a major European auto-service chain reduced rework downtime by 22 % using low-VOC, fast-curing refinish coatings across 150 sites.

Competitive Landscape: Market leader ~25 % share — followed by 3–5 major competitors including large global coating firms and specialized regional producers.

Regulatory & ESG Impact: Growing regulation on VOC emissions, incentives for low-emission paint adoption, and brand mandates for sustainable repair solutions.

Investment & Funding Patterns: Approximately USD 500 M in new investments between 2022–2025 for upgrading coating lines; increasing use of project financing and joint-venture funding for technological upgrades.

Innovation & Future Outlook: Integration of smart-coating technologies, digital colour-matching systems, robotic spray systems, and growing focus on sustainable, recycled-content coatings to drive future market evolution.

Automotive refinish coatings now serve a broad range of sectors — collision repair, fleet refurbishment, used-vehicle reconditioning, and vehicle customization — with collision repair and refurbishment contributing over 60 % of global demand. Recent product innovations, such as low-VOC water-borne coatings and nano-ceramic scratch-resistant finishes, are reducing environmental impact and improving durability. Strict environmental regulations, rising costs of new vehicles, and growing demand for sustainable and high-performance coatings are prompting faster adoption in both developed and emerging markets. Regional consumption grows strongest in Asia-Pacific, supported by expanding used vehicle markets, while Europe and North America prioritize regulatory compliance and premium finish quality. Emerging trends point to automated application systems, real-time colour-matching technology, and increased usage of recycled raw materials, positioning the market for steady long-term growth through 2032.

The strategic relevance of the Automotive Refinish Coatings Market continues to intensify as global vehicle lifespans increase and refurbishment cycles shorten, driving elevated demand for high-performance coating systems. The industry is moving toward technology-led transformation, with measurable improvements shaping competitive advantage. Advanced nano-ceramic coating technology delivers up to 30% improvement in scratch resistance compared to conventional solvent-borne systems, accelerating adoption across professional repair networks. Asia-Pacific dominates in volume, while Europe leads in adoption with nearly 48% of enterprises using eco-compliant refinish formulations. By 2027, AI-enabled colour-matching platforms are expected to improve first-time accuracy by 35%, reducing costly rework and material wastage. Firms are committing to ESG-aligned metrics, including targeted 25% VOC reduction and 18% recycling improvements by 2030, aligning production with tightening sustainability mandates. In 2024, Japan achieved a 20% cycle-time reduction through automated robotic application systems integrated with digital curing controls. Forward pathways include wider integration of digital workflows, increased penetration of low-VOC technologies, and supply chain modernization that enhances traceability and compliance. As environmental pressures, automotive aftermarket expansion, and technological innovation converge, the Automotive Refinish Coatings Market stands positioned as a pillar of resilience, regulatory readiness, and sustainable long-term growth.

Sustainability-focused transformation is significantly influencing the Automotive Refinish Coatings Market as regulatory agencies push for rapid VOC reduction and safer coating chemistries. Water-borne refinish systems, which contain up to 70% fewer hazardous emissions than older solvent-borne coatings, are being adopted widely across repair centres. This shift supports improved workshop conditions, reduced environmental impact, and more consistent finish quality. Increased consumer preference for environmentally responsible repair solutions has also contributed to accelerating technology upgrades within body shops. Manufacturers introducing ultra-low-VOC clearcoats and primers have reported efficiency gains of up to 18% through faster drying times and reduced energy use, strengthening market demand. The combined impact of regulation, technology, and consumer alignment continues to reinforce growth across global regions.

A growing shortage of skilled application technicians remains a major restraint for the Automotive Refinish Coatings Market. Modern coating systems require precision, especially with advanced water-borne and nano-structured formulations that demand specialized training to achieve optimal results. Surveys from major service networks indicate that nearly 42% of workshops struggle to recruit qualified refinish personnel, contributing to slower job throughput and higher operational costs. Errors caused by insufficient technical skill can lead to material wastage ranging between 8–12% per job, directly affecting profitability. Limited availability of structured training programs, combined with the fast pace of new coating technologies, amplifies this workforce gap. As repair facilities attempt to integrate advanced digital colour-matching and robotic systems, the skill deficit becomes even more pronounced, slowing modernization in key markets.

The Automotive Refinish Coatings Market is experiencing expanding opportunities from the rapid integration of digital platforms and automation. AI-driven colour-matching tools now provide accuracy levels above 95%, significantly reducing rework and paint wastage. The rise of automated spray robots capable of improving coating uniformity by 25–30% offers new efficiency advantages for high-volume repair facilities. Additionally, connected workflow management systems are enabling body shops to optimize material planning, track curing performance, and monitor environmental compliance in real time. Regions with strong aftermarket expansion, such as Southeast Asia and Latin America, present fertile ground for these advancements as service centres upgrade operations. The growing shift toward predictive maintenance, faster turnaround expectations, and sustainable production practices positions digitalization as a major catalyst for future market expansion.

Rising raw material prices and persistent supply-chain volatility present significant challenges for the Automotive Refinish Coatings Market. Fluctuations in the cost of key inputs such as resins, pigments, and additives have reached increases between 10–18% in several regions, placing pressure on manufacturers and repair operators. Global supply disruptions, particularly in resin and chemical intermediates, have led to extended lead times and inconsistent stock availability for workshops. These constraints complicate production planning and increase dependency risks across distributors and service networks. Additionally, transportation bottlenecks and inconsistent delivery cycles strain inventory stability, forcing many body shops to increase safety stock levels. These challenges slow market scalability and hinder timely adoption of advanced coatings, especially in regions sensitive to price movements and import dependency.

• Rapid Transition Toward Low-VOC and Water-Borne Technologies: The Automotive Refinish Coatings Market is witnessing accelerated adoption of low-VOC and water-borne formulations, with usage increasing by more than 32% between 2021 and 2024 across major repair networks. Workshops implementing water-borne basecoats have reported up to 28% reduction in drying time and nearly 18% lower material wastage. In Europe alone, over 46% of certified repair centres now operate primarily on low-emission coating systems, driven by tightening environmental standards and performance gains that support faster turnaround cycles and consistent finish quality.

• Expansion of Digital Colour-Matching and AI-Based Refinishing Tools: Advanced digital colour-matching tools continue to reshape operational efficiency, with AI-enabled scanners achieving accuracy rates exceeding 94% compared to manual shade-matching methods. Body shops integrating predictive colour algorithms have reduced rework frequency by approximately 21%, improving throughput during peak service seasons. Adoption of digital shade libraries has increased by 38% globally since 2022, enabling technicians to match complex metallic and pearlescent finishes more reliably. Automated tinting machines, now deployed in more than 27% of high-volume workshops, further standardize outcomes and lower operator dependency.

• Growing Integration of Automated Spray Systems and Robotics: Robotics-driven refinishing processes are gaining prominence as repair networks focus on consistency, precision, and safety. Automated spray robots have demonstrated up to 30% improvement in coating uniformity and a 25% reduction in overspray. Facilities incorporating robotic arms for primer and clearcoat applications report productivity enhancements of 22% due to reduced manual intervention. North America and Japan remain early adopters, with more than 18% of large repair facilities already applying robotic systems for high-volume refinishing operations.

• Surge in Demand for High-Performance and Nano-Structured Coating Materials: Technological advancements in nano-structured clearcoats and abrasion-resistant formulations are transforming product innovation. Nano-infused coatings deliver up to 35% greater scratch resistance and retain gloss levels 28% longer under accelerated testing conditions. Adoption of ultra-durable topcoats has risen by 31% since 2020 in premium repair networks catering to luxury and commercial fleets. Additionally, weather-resistant formulations capable of withstanding UV exposure 40% longer are gaining traction in regions with harsher climates, supporting increased lifecycle performance and reduced maintenance frequency.

The Automotive Refinish Coatings Market is segmented across types, applications, and end-user categories, each demonstrating distinct performance characteristics shaped by technology advances, regulatory pressure, and evolving repair practices. Type-based segmentation highlights the shift toward sustainable and high-performance formulations, as workshops increasingly favor systems that improve curing speed and finish durability. Application-level segmentation reflects stronger demand in collision repair centers, fleet maintenance operations, and refurbishment services, supported by rising global vehicle usage and shorter cosmetic repair cycles. End-user segmentation indicates rising adoption among professional body shops, OEM-authorized service centers, and fleet operators, each contributing to material consumption patterns. Together, these segments emphasize measurable transformation through digitalization, sustainability compliance, and material optimization in modern refinishing environments.

Solvent-borne coatings remain the leading type, accounting for approximately 44% of total adoption due to their compatibility with a wide range of substrates and their established performance in high-demand repair environments. Their dominance is supported by consistent usage in regions with slower regulatory transitions away from solvent-based formulations. In comparison, water-borne coatings hold around 33% adoption, reflecting strong regulatory and environmental momentum, while UV-curable coatings currently represent nearly 12%, driven by rapid curing cycles and energy efficiency. Powder coatings and specialty nano-clearcoats collectively contribute the remaining 11%, primarily used in niche restoration, luxury detailing, and high-durability applications. UV-curable formulations are the fastest-growing type, expanding at an estimated 9.2% growth rate due to improved durability metrics and 40–60% faster curing times compared to traditional systems.

Collision repair dominates the application landscape, representing nearly 51% of overall market use due to increasing vehicular density and high annual repair frequency. In comparison, automotive restoration accounts for roughly 28% of adoption, driven by rising refurbishment activity across used-car markets, while fleet maintenance applications hold approximately 17%. Specialty applications—including performance vehicles, custom finishing, and restoration workshops—account for the remaining 4%. Fleet maintenance is the fastest-growing application category, progressing at an estimated 8.4% growth rate as fleet operators expand preventive and cosmetic maintenance programs. Digital colour-matching, fast-curing materials, and energy-efficient ovens are supporting this acceleration.

Professional body shops represent the leading end-user segment, accounting for nearly 48% of total adoption due to their high service turnover, investment in digital tools, and skilled operator networks. OEM-authorized service centers follow with around 31% adoption, providing advanced repair capabilities supported by standardized materials and calibrated colour systems. Independent repair garages and commercial fleet operators collectively hold the remaining 21% of market use, each contributing to rising demand for quick-turnaround coating materials and enhanced durability specifications. Fleet operators are the fastest-growing end-user group, expanding at an estimated 8.7% growth rate as large-scale operators invest in cosmetic maintenance programs and durability-optimized coatings that reduce long-term operational wear. Industry adoption data indicates that over 36% of large transportation fleets upgraded to high-resistance coatings in 2024 to extend maintenance intervals by measurable margins.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, Europe is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

Asia-Pacific’s strong automotive production base, with more than 58 million vehicles manufactured in 2023, continues to drive higher refinishing material consumption. North America followed with a 27% share, supported by over 275 million vehicles in operation requiring regular repair cycles, while Europe captured nearly 24% with advanced sustainability-led refinishing systems. South America and the Middle East & Africa jointly contributed 8%, with rising investments in repair infrastructure and aftermarket expansion. Across regions, digital refinishing tools, water-borne systems, and automated colour-matching adoption increased by 18–34% between 2022 and 2024, highlighting the global transition to high-efficiency processes.

How are technological upgrades transforming refinishing systems across industries?

North America captured nearly 27% of the Automotive Refinish Coatings Market in 2024, driven by strong demand from collision repair networks, commercial fleets, and OEM-certified service centers. The region benefits from high adoption of digital shade-matching tools, with more than 52% of professional body shops now using AI-enabled scanners to improve accuracy. Regulatory standards promoting low-VOC coatings also support steady material transition. A leading regional player introduced fast-curing clearcoat systems in 2023, reducing booth cycle times by 22%. Consumer behavior shows higher uptake in technologically advanced repair services, with adoption exceeding 48% among enterprises in sectors such as logistics and mobility services.

Why is regulatory stringency accelerating technology-driven refinishing adoption?

Europe holds approximately 24% of the Automotive Refinish Coatings Market, driven by Germany, France, Italy, and the UK, each showing high penetration of water-borne and low-VOC coating systems. EU sustainability initiatives have accelerated the shift, with compliance-related coatings usage rising by over 36% between 2021 and 2024. Digital colour-automation and robotic spray systems are being adopted in more than 29% of high-volume repair shops across Western Europe. A regional manufacturer recently deployed nano-reinforced clearcoat lines, delivering 28% higher surface durability in local trials. Consumer behavior shows strong preference for eco-compliant refinishing, with adoption rates among professional workshops reaching nearly 55%.

How are expanding vehicle fleets reshaping refinishing consumption patterns?

Asia-Pacific represents the largest regional market with around 41% share, supported by China, India, Japan, and South Korea—collectively accounting for over 60% of global vehicle production. Rapid expansion of manufacturing hubs and aftermarket workshops has increased demand for high-durability coatings and fast-curing refinishing solutions. The region is also a leader in digital adoption, with more than 33% of organized repair centers using automated tinting and colour-matching systems. A major regional producer recently introduced advanced heat-resistant clearcoats tailored for tropical climates, improving gloss retention by 26%. Consumer behavior indicates strong growth from e-commerce-enabled repair booking platforms and mobile service providers.

What factors are driving the modernization of refinishing services in emerging markets?

South America accounted for nearly 5% of the Automotive Refinish Coatings Market, led by Brazil and Argentina, which together represent more than 70% of the region’s vehicle repair demand. Continued investment in automotive infrastructure and expanding urban mobility fleets are increasing consumption of basecoats, primers, and clearcoats. Government incentives for local manufacturing of coating materials have boosted regional availability. A local manufacturer in Brazil launched corrosion-resistant refinishing systems in 2024, improving vehicle surface longevity by 19%. Consumer behavior shows increasing demand for cost-efficient refinishing, with high adoption in aftermarket repair chains and used-vehicle refurbishment centers.

How is industrial expansion influencing refinishing system upgrades in the region?

The Middle East & Africa region contributed around 3% of the Automotive Refinish Coatings Market in 2024, driven by key countries such as the UAE, Saudi Arabia, and South Africa. Growing automotive service networks, high-temperature climate conditions, and increased use of commercial fleets are raising demand for heat-resistant coating materials. Adoption of automated spray technologies is expanding, with more than 17% of advanced workshops integrating digital monitoring systems. A regional supplier introduced UV-resistant clearcoats engineered for desert environments, offering 23% longer protection against surface degradation. Consumer behavior reflects growing preference for premium refinishing in luxury and commercial segments.

China – 24% market share

Strong production capacity and extensive aftermarket repair networks support the country’s leadership in the Automotive Refinish Coatings Market.

United States – 18% market share

High vehicle ownership volumes and technologically advanced repair ecosystems reinforce the country’s dominant market position.

The Automotive Refinish Coatings market features a moderately consolidated structure, with the top five companies collectively accounting for approximately 55–60% of the global market share. More than 40 active competitors operate across global and regional levels, with market leaders positioned strongly through extensive distribution networks, advanced product portfolios, and long-term OEM and body shop partnerships. Competitive intensity is driven by rapid adoption of low-VOC, waterborne, and high-performance coatings, supported by sustained investments in R&D exceeding 3–5% of annual revenue among leading manufacturers. Mergers, acquisitions, and technology collaborations have risen steadily, with over 20 notable strategic deals recorded between 2022 and 2024, aimed at enhancing color-matching technology, digital repair solutions, and eco-efficient formulations. Companies are increasingly adopting AI-based color retrieval systems, UV-cure technologies, and automated mixing systems to differentiate themselves in high-volume markets. Regional players continue gaining traction by offering cost-effective, regulatory-aligned products, particularly in Latin America, Southeast Asia, and Eastern Europe. The competitive landscape is expected to further intensify as sustainability mandates tighten and digital repair ecosystems expand worldwide.

AkzoNobel

PPG Industries

BASF Coatings

Axalta Coating Systems

Sherwin-Williams

Nippon Paint Holdings

Kansai Paint

3M

KCC Corporation

RPM International

Tikkurila

Jotun

Technological advancements in the Automotive Refinish Coatings market are reshaping product performance, application efficiency, and environmental compliance. One of the most influential developments is the rapid shift toward waterborne coating technologies, which now account for more than 30% of total refinish coatings used globally due to their lower VOC levels and improved worker safety. High-solid formulations have also gained traction, representing an estimated 25–28% of total usage because they offer stronger film build, faster drying, and reduced emissions. UV-cure refinish coatings are emerging as a high-growth segment, enabling curing times as low as 2–5 minutes compared to traditional drying cycles of 20–40 minutes, significantly boosting body shop throughput. Digitalization is accelerating technological transformation, with over 50% of leading body shops adopting digital color-matching systems capable of scanning more than 200,000 color formulations with high precision. AI-driven color retrieval tools are becoming increasingly common, reducing mismatches and improving repair quality. Automation is another major trend, with robotic spray systems improving application consistency and reducing material waste by nearly 20–25%.

Nano-coatings and ceramic-based protective layers are gaining market acceptance owing to their enhanced scratch resistance, hydrophobic behavior, and longer service life. These technologies are particularly valuable in regions with harsh climates, where coating durability is a priority. Hybrid coating systems that combine polyurethane and acrylic chemistries are also expanding, offering better flexibility and chemical resistance for frequent-use vehicles. Sustainability-focused innovations continue to dominate R&D pipelines, including bio-based resins and low-energy curing systems that support regulatory alignment. Collectively, these technologies are strengthening operational efficiency, reducing environmental impact, and enabling manufacturers and repair centers to deliver higher-quality refinishing outcomes across diverse global markets.

In September 2024, BASF Coatings introduced the first‑ever refinish clearcoats manufactured using recycled waste‑tire feedstock via its proprietary ChemCycling® technology under the brands Glasurit and R‑M, enabling body shops to reduce CO₂ emissions while maintaining high performance in drying and finish quality. (BASF)

In April 2024, BASF launched a new generation of eco‑efficient clearcoats and undercoats for the Asia Pacific refinish market, produced through a biomass‑balance approach to replace fossil feedstock — targeting significant CO₂ reduction and supporting sustainability mandates in high‑growth regions. (BASF)

In November 2024, 3M and BASF Coatings announced a collaboration to develop standard operating procedures (SOPs) and training content for collision repair shops worldwide, aiming to reduce material waste, VOC emissions, and non‑productive time while enhancing overall repair process sustainability and efficiency. (basf-coatings.com)

In 2023, PPG Industries rolled out its PPG DP7000 Air‑Dry Primer across European, Middle Eastern and African refinish markets — a two‑pack acrylic primer that dries up to twice as fast as legacy primers, allowing bodyshops to operate in diverse humidity conditions and reducing energy consumption for curing.

The Automotive Refinish Coatings Market Report encompasses a comprehensive analysis across multiple product types — including primers, basecoats, clearcoats, and specialty coatings — along with emerging sub‑segments such as waterborne systems, biomass‑balanced coatings, UV‑curable and recycled‑feedstock formulations. It covers application segments including collision repair, fleet maintenance, used vehicle refurbishment, restoration workshops, and custom finishing for premium or specialty vehicles. Geographic scope spans all major global regions: North America, Europe, Asia‑Pacific, South America, and Middle East & Africa — allowing comparison of regional consumption behaviour, regulatory influence, and technology adoption trends.

The report also evaluates technology trends shaping the future of refinishing, such as digital colour‑matching platforms, automated mixing and spray systems, eco‑efficient formulations, and sustainability‑driven innovations including circular‑economy feedstock and low‑VOC/waterborne paints. Regulatory and ESG‑compliance aspects form another core dimension, assessing how environmental policies influence manufacturer and body shop choices.

Industry focus areas include aftermarket repair shops, OEM‑authorized service centers, fleet operators, and independent garages — enabling decision‑makers to gauge demand drivers, end‑user adoption behavior, and market potential by segment and region. The report incorporates recent developments, strategic initiatives by leading players, and innovation trajectories, providing a holistic view of competitive environment, market readiness for new technologies, and long-term outlook for sustainable growth and regulatory alignment.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 7840.55 Million |

|

Market Revenue in 2032 |

USD 12976.08 Million |

|

CAGR (2025 - 2032) |

6.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

AkzoNobel, PPG Industries, BASF Coatings, Axalta Coating Systems , Sherwin-Williams , Nippon Paint Holdings, Kansai Paint, 3M, KCC Corporation , RPM International, Tikkurila, Jotun |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |