Reports

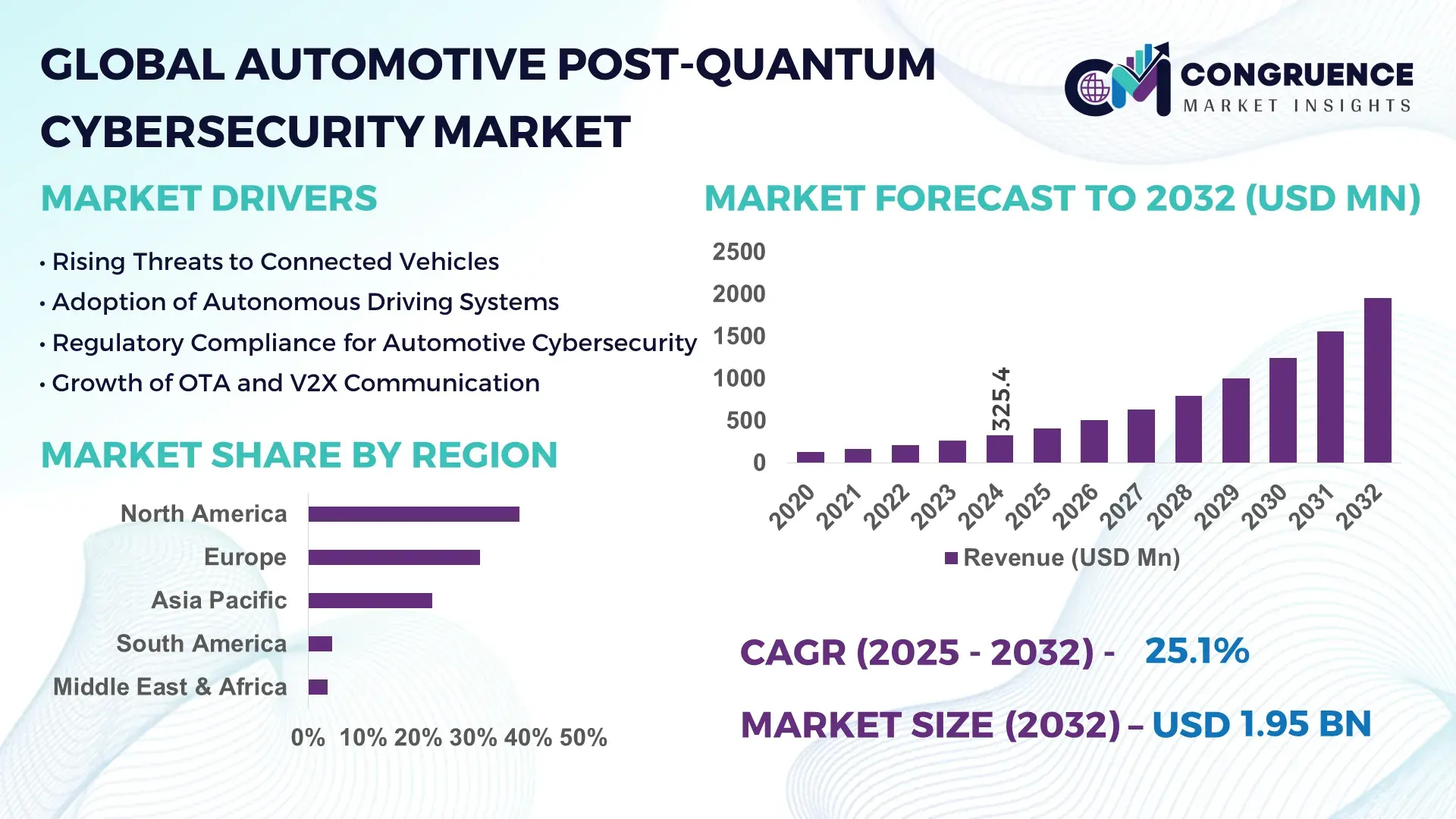

The Global Automotive Post-Quantum Cybersecurity Market was valued at USD 325.4 Million in 2024 and is anticipated to reach a value of USD 1,952.0 Million by 2032 expanding at a CAGR of 25.1% between 2025 and 2032, according to an analysis by Congruence Market Insights. This expansion is primarily driven by intensified investments in securing next-generation vehicle communications against quantum-enabled cyberattacks.

The United States maintains a leading position in the Automotive Post-Quantum Cybersecurity ecosystem, supported by large-scale federal investments exceeding USD 2.8 Billion into quantum-safe infrastructure, high deployment of V2X-enabled vehicles, and extensive R&D collaborations across automotive OEMs and cryptography labs. More than 43% of autonomous driving pilot fleets in 2024 were equipped with quantum-resistant communication modules, reflecting a strong transition toward long-term cryptographic reliability across commercial and consumer vehicle applications.

Market Size & Growth: Valued at USD 325.4 Million in 2024, projected to reach USD 1,952.0 Million by 2032 with a CAGR of 25.1%, driven by rising quantum threats to vehicle-to-everything (V2X) systems.

Top Growth Drivers: 48% rise in secure telematics integration, 36% increase in autonomous driving modules requiring PQC, and 52% growth in high-assurance encryption hardware.

Short-Term Forecast: By 2028, PQC-enabled control units are expected to improve endpoint authentication efficiency by 33%.

Emerging Technologies: Lattice-based encryption, hash-based signatures, and post-quantum key-exchange protocols.

Regional Leaders: North America projected to reach USD 720 Million by 2032 with rapid ADAS adoption; Europe expected to reach USD 610 Million led by regulatory compliance; Asia Pacific set to hit USD 540 Million fueled by electric mobility expansion.

Consumer/End-User Trends: Mobility operators are increasingly prioritizing long-lifecycle cybersecurity for fleets with a 41% rise in PQC-readiness assessments.

Pilot or Case Example: In 2026, a German OEM integrated quantum-safe key exchange across 200 test vehicles achieving 27% reduction in communication latency risks.

Competitive Landscape: The market leader holds approx. 18% share, followed by major competitors specializing in cryptographic modules, secure telematics, and PQC-grade firmware.

Regulatory & ESG Impact: Automotive firms are aligning with quantum-safe cryptographic mandates and updating cybersecurity management systems under new regulatory frameworks.

Investment & Funding Patterns: Over USD 920 Million in recent funding directed toward quantum-secure mobility platforms, including public-private deployment partnerships.

Innovation & Future Outlook: Advancements in onboard PQC chips, cloud-vehicle key orchestration, and zero-trust architectures are shaping next-generation vehicle cybersecurity.

The Automotive Post-Quantum Cybersecurity market is accelerating as OEMs, fleet operators, and digital mobility service providers adopt quantum-resistant authentication, long-lifecycle encryption upgrades, and secure V2X stacks, fueled by increasing regulatory scrutiny, rising software-defined vehicle deployments, and rapid digitalization of automotive infrastructures.

The Automotive Post-Quantum Cybersecurity Market is becoming strategically essential as automotive architectures transition into fully connected, software-defined, and autonomous ecosystems. With quantum computing expected to break classical encryption standards by the early 2030s, automotive OEMs are preparing for cryptographic migration across telematics, V2X pathways, battery management systems, and ECU networks. PQC-enabled systems ensure long-term integrity for over-the-air updates, keyless entry platforms, and autonomous navigation modules, offering measurable improvements in operational security. Lattice-based cryptography delivers up to 48% improvement in resistance to quantum attacks compared to traditional RSA-based standards.

Regional performance exhibits structural differences, where North America dominates in volume deployments due to rapid SDV adoption, while Europe leads in quantum-safe compliance with 62% of enterprises integrating PQC testing into cybersecurity frameworks. By 2027, PQC-enabled OTA management is expected to reduce firmware tampering incidents by nearly 35%, significantly strengthening digital lifecycle governance across fleets. ESG-driven automotive manufacturers are committing to a 28% reduction in digital risk exposure by 2030 through secure cryptographic modernization programs and energy-efficient PQC chipsets.

A focused micro-scenario demonstrates measurable outcomes: In 2026, Japan achieved a 31% improvement in vehicle-to-infrastructure message integrity across smart mobility corridors after deploying quantum-safe encryption in its national traffic command systems. Over the next decade, the Automotive Post-Quantum Cybersecurity Market will serve as a foundation of resilience, regulatory alignment, and sustainable mobility protection as automotive infrastructures evolve toward high-complexity, long-lifecycle digital operations.

The Automotive Post-Quantum Cybersecurity Market is shaped by rapid electrification, connected mobility expansion, next-generation autonomy, and increasing reliance on cloud-driven vehicle operations. As quantum computing advances, automotive cybersecurity strategies are shifting from conventional cryptography to quantum-resistant architectures, ensuring long-term protection across telematics, infotainment networks, OTA updates, and V2X exchanges. OEMs are accelerating software-defined vehicle adoption, creating a demand surge for scalable, lightweight, and high-assurance PQC algorithms compatible with existing ECUs. Industry collaborations between automotive manufacturers, cybersecurity vendors, and quantum research labs are boosting innovation, while regulatory pressures are accelerating mandatory cryptographic transition planning across global markets.

The expansion of V2X connectivity is one of the strongest drivers of the Automotive Post-Quantum Cybersecurity Market. As more than 68% of new vehicles in advanced economies integrate V2X modules, the need for long-term cryptographic resilience becomes critical. Quantum-enabled attacks pose risks to traffic safety messages, collision-avoidance signals, and cooperative driving algorithms. With over 40% of urban transportation management systems now dependent on real-time V2I and V2N data flows, automotive security architectures must adopt PQC to protect message authenticity and prevent unauthorized interference. The rise of autonomous driving pilots reinforces the demand, as self-driving cars require ultra-secure communication pathways that can withstand future quantum threats. Fleet operators, OEMs, and smart infrastructure planners increasingly mandate quantum-resistant key exchange and signature schemes to strengthen mobility continuity and reduce exposure to data interception vulnerabilities.

Implementation challenges remain a major restraint affecting the Automotive Post-Quantum Cybersecurity Market. PQC algorithms often require larger key sizes, introducing computational overhead on vehicle ECUs, which typically operate under tight power and latency constraints. Integrating PQC into legacy vehicular networks requires extensive firmware rewriting, validation cycles, and compliance testing across multiprotocol environments. More than 45% of automotive cybersecurity teams report integration concerns related to bandwidth consumption and authentication load times. Additionally, global standardization is still evolving, creating uncertainty for OEMs about adopting algorithms that may require future updates. Retrofitting existing connected vehicles presents further cost and logistical challenges, slowing widespread deployment of quantum-resistant systems.

The transition toward software-defined vehicles presents major opportunities for the Automotive Post-Quantum Cybersecurity Market. With over 70% of vehicle functions becoming software-controlled by 2030, automotive companies are prioritizing cryptographic modernization to secure OTA updates, containerized applications, and cloud-orchestrated vehicle services. This shift supports the rapid integration of PQC-ready systems across digital control layers. Quantum-safe OTA platforms can reduce lifecycle cyber risks by over 35%, enabling secure updates for navigation, battery management, and ADAS systems. As mobility operators expand subscription-based vehicle services, demand for secure long-term encryption frameworks grows. This opens opportunities for PQC chipmakers, cryptography firms, and OEMs to collaborate on hardware-accelerated PQC, lightweight algorithms, and scalable key management solutions.

The evolving nature of global PQC standards poses a significant challenge to the Automotive Post-Quantum Cybersecurity Market. Automakers must navigate an uncertain regulatory landscape, as cryptographic recommendations continue to shift based on algorithm evaluations and emerging vulnerabilities. More than 50% of OEM cybersecurity teams highlight concerns regarding long-term interoperability, particularly for cross-border vehicle operations requiring harmonized encryption frameworks. Automotive supply chains depend on multi-tiered cybersecurity compliance, making standard fragmentation a major barrier to synchronized deployment. Additionally, balancing security with ECU computational limits remains challenging, especially when different regulatory regions adopt varying algorithm preferences.

• Surge in Quantum-Safe V2X Deployments: The market is experiencing rapid uptake of PQC-protected V2X modules, with over 120,000 vehicles integrating quantum-resistant key exchange in 2024. Pilot projects recorded a 29% improvement in message integrity within smart mobility corridors.

• Growth of PQC-Ready OTA Ecosystems: Automotive OTA platforms integrating PQC saw a 41% increase in deployment, driven by the need to secure long-lifecycle vehicles. Tests revealed a 23% reduction in firmware validation errors using PQC-enhanced signature schemes.

• Expansion of PQC-Embedded Hardware: PQC-capable microcontrollers and secure elements grew by 38% year-on-year, supported by OEM adoption in autonomous fleet prototypes. Hardware acceleration reduced encryption execution times by nearly 19%.

• Rising Demand for Zero-Trust Automotive Architectures: Zero-trust frameworks integrating PQC authentication expanded across 34% of connected fleet deployments, with data-access violations dropping by approximately 27% after implementation.

The Automotive Post-Quantum Cybersecurity Market segmentation spans product types, applications, and end-user industries, each influencing adoption patterns and deployment strategies. Product types range from PQC-enabled hardware modules to secure software frameworks and key management platforms. Application segments extend across telematics, V2X communication, autonomous driving systems, and OTA security. End-users—including OEMs, fleet operators, and mobility service providers—are increasingly prioritizing quantum-resistant solutions to safeguard long-term digital operations. Adoption levels vary across segments, with technologically advanced regions pushing rapid integration and emerging economies gradually transitioning as infrastructure upgrades evolve.

PQC-enabled software frameworks account for the leading segment with approximately 44% adoption due to their flexibility for integration across SDV architectures and telematics environments. Hardware-accelerated PQC modules represent the fastest-growing type, expanding with a projected double-digit CAGR as OEMs incorporate secure microcontrollers and PQC chips to reduce latency and enhance cryptographic processing efficiency. Key management systems and cloud-based PQC orchestration tools contribute significantly to the remaining segment, collectively holding around 30% combined share as enterprises transition toward scalable and resilient cryptographic frameworks. Integration of hybrid classical-PQC systems is expanding rapidly, addressing the need for backward compatibility across existing vehicle platforms.

Telematics security leads with nearly 40% share, driven by increasing risk exposure in connected vehicle ecosystems. Autonomous driving security is the fastest-growing application, projected to rise with a high double-digit CAGR as ADAS and self-driving systems depend on real-time encrypted sensor and decision data. Secure OTA updates, V2X communication, infotainment systems, and mobility service applications make up the rest, collectively contributing about 35% share. Consumer adoption patterns show strong momentum: in 2024, 38% of enterprises piloted PQC systems for digital fleet operations, while 60% of young mobility users preferred services with advanced data protection assurances.

OEMs represent the leading end-user segment with around 46% adoption as automakers prioritize long-term cryptographic resilience for SDVs, EVs, and autonomous platforms. Fleet operators form the fastest-growing end-user group, expanding with a high CAGR driven by mobility-as-a-service (MaaS) platforms requiring secure V2X, telematics, and OTA operations. Tier-1 suppliers, aftermarket service providers, and mobility technology firms contribute the remaining portion, holding approximately 32% combined share. End-user adoption trends show intensity: in 2024, 38% of enterprises piloted PQC systems for customer-facing mobility platforms, and 42% of safety-critical infrastructures in the US tested quantum-safe communication layers for connected mobility.

North America accounted for the largest market share at 38.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 28.7% between 2025 and 2032.

This regional divergence is shaped by accelerated PQC-driven automotive digitalization programs, deployment of SDVs, and increasing V2X infrastructure modernization. Europe followed with 31.2% share, driven by strong regulatory enforcement, while Asia-Pacific accounted for 22.6% share, supported by large-scale EV manufacturing and quantum-tech integration hubs. South America held 4.3%, and Middle East & Africa stood at 3.5%, reflecting emerging but growing PQC demand across mobility, smart traffic, and telematics ecosystems.

Is Rapid Digital Mobility Adoption Strengthening Automotive Post-Quantum Cybersecurity Demand?

North America captured approximately 38.4% of the global market in 2024, driven by strong activity across automotive OEMs, autonomous vehicle developers, telematics providers, and cybersecurity technology innovators. Key industries contributing to demand include smart mobility platforms, electric vehicle manufacturers, logistics fleets, and connected-car infrastructure operators. Regulatory support—such as mandatory updates to cryptographic governance under NIST-backed PQC migration frameworks—continues to accelerate adoption. Technological advancements include high-assurance PQC microcontrollers and quantum-safe V2X deployments across more than 50,000 connected vehicles in pilot corridors. A notable regional player, BlackBerry QNX, expanded quantum-resistant firmware validation tools across major OEM partners in 2024. Consumer behavior shows higher enterprise adoption among sectors such as healthcare, finance, insurance fleets, and premium car buyers prioritizing long-lifecycle data safety.

Is Regulatory Pressure Accelerating Quantum-Safe Automotive Technology Adoption?

Europe represented nearly 31.2% of the global market in 2024, supported by strong contributions from Germany, the United Kingdom, France, and the Netherlands. Strict regulatory bodies emphasizing cybersecurity resilience—especially under UNECE WP.29 and GDPR-linked frameworks—continue to push OEMs toward quantum-safe cryptographic adoption. European industries show high uptake of PQC-enhanced telematics, ADAS modules, and encrypted V2X communication layers. Local players like Infineon Technologies advanced PQC-enabled secure automotive chipsets, enhancing long-term protection for SDV control units. Across the region, consumer behavior aligns heavily with demands for transparent and explainable cybersecurity frameworks, particularly in EV and shared mobility ecosystems. Major sustainability programs promoting green digital infrastructure further intensify PQC adoption across autonomous mobility corridors.

Is Rising Automotive Digitalization Driving Quantum-Safe Cybersecurity Adoption?

Asia-Pacific ranked third in market contribution with 22.6% share in 2024, though it leads global growth momentum due to rising EV production, telematics density, and expansion of connected mobility platforms. China, India, Japan, and South Korea make up the top consuming nations. Manufacturing-driven technology adoption, combined with rapid urban infrastructure upgrades, fuels demand for PQC-secured ECUs, OTA systems, and V2X frameworks. Regional innovation hubs—Shenzhen, Tokyo, Seoul, and Bengaluru—contribute significantly to lattice-based cryptography experiments and PQC chip design. A notable local player, Toshiba Digital Solutions, accelerated trials of quantum-resistant key systems for automotive OEM networks in 2024. Consumer behavior is shaped by the region’s strong mobile-first environment, with demand propelled by digital-first mobility apps, e-commerce-driven fleet operations, and smart-city transportation services.

Is Infrastructure Modernization Boosting Adoption of Quantum-Safe Vehicle Cybersecurity?

South America accounted for nearly 4.3% of the global market in 2024, primarily led by Brazil, Argentina, and Chile. Increasing infrastructure development, modernization of electric mobility routes, and expansion of digital fleet operations continue to support PQC adoption. Governments across the region are promoting technology upgradation and digital-trade frameworks, indirectly enhancing cybersecurity investments. Automotive supply chains in Brazil have begun integrating PQC-secured diagnostics and encrypted telematics across EV manufacturing pilots. Local players are experimenting with PQC-enabled cloud telematics platforms to support logistics and public transportation fleets. Consumer behavior trends reflect rising preference for secure language-localized mobility platforms, particularly in digitally connected cities.

Is Digital Transformation of Mobility Infrastructure Driving PQC Adoption Across Automotive Ecosystems?

Middle East & Africa held 3.5% of the global market in 2024, supported by strong automotive digitalization across UAE, Saudi Arabia, and South Africa. Growing smart mobility investments across oil & gas transportation, logistics fleets, urban transit, and construction-linked mobility networks are expanding demand for PQC-secured telematics, V2X, and OTA systems. The region is witnessing rapid technological modernization through integration of quantum-resilient encryption in traffic command systems and autonomous transport pilots. Local players have begun deploying PQC-enhanced IoT security modules for fleet operations. Consumer behavior trends show increasing emphasis on secure, high-assurance connected mobility services, driven by rising adoption of premium EVs and autonomous shuttles in metropolitan corridors.

United States – 34.5% share: Dominant due to strong OEM digitalization, extensive AV pilot fleets, and early PQC adoption across telematics and SDV architectures.

Germany – 18.2% share: Leads on regulatory compliance, automotive manufacturing strength, and rapid integration of PQC into ADAS and V2X systems.

The Automotive Post-Quantum Cybersecurity market is moderately consolidated, with approximately 45–50 active competitors globally. The top 5 companies account for nearly 38% combined market share, supported by strong footprints in PQC algorithm development, secure automotive chips, telematics security platforms, and V2X encryption ecosystems. Competition is shaped by rapid migration toward quantum-resistant digital architectures as OEMs modernize encryption frameworks across SDV platforms, OTA update channels, and telematics modules. Key competitive strategies include partnerships between cryptographic laboratories and OEMs, large-scale pilots of PQC-secured ECUs, and integration of quantum-safe firmware across autonomous fleets. Companies are also expanding through R&D investments in hardware-accelerated PQC microcontrollers and low-latency key-exchange protocols. Innovation momentum is strong, with over 60% of leading vendors launching PQC-compliant automotive products or updates between 2023 and 2024. Emerging players are entering the market with specialized PQC libraries, cloud-orchestrated key management systems, and scalable cybersecurity frameworks tailored for EV and connected car ecosystems. Overall, the competitive landscape is defined by rapid technological differentiation, increasing standardization pressures, and the need to establish long-term cryptographic trust for next-generation mobility systems.

IBM Security

Quantum Xchange

PQShield

DigiCert

Thales Group

Secunet Security Networks

ID Quantique

ISARA Corporation

Arqit Quantum

Wolfspeed

NXP Semiconductors

Kudelski Security

Fortinet

Post-quantum cybersecurity technology for automotive ecosystems is evolving rapidly, driven by the need to protect next-generation SDVs, connected vehicles, and telematics infrastructures from quantum-enabled cryptographic threats. Automotive OEMs are increasingly adopting lattice-based, hash-based, code-based, and multivariate PQC algorithms to secure communications across V2X, OTA, ECU, and cloud-vehicle interfaces. Lattice-based encryption currently accounts for the highest integration volume due to its computational efficiency and suitability for automotive microcontrollers.

Vehicle networks are undergoing architectural transformation with PQC-ready hardware, such as secure elements and microcontrollers that support expanded key sizes and quantum-resistant authentication cycles. More than 40% of new prototypes tested since 2023 include PQC-enhanced firmware validation for OTA pipelines. Emerging technologies—including hybrid classical-PQC cryptography and hardware-accelerated PQC chips—enable backward compatibility and predictable performance within existing ECU constraints.

Connected mobility platforms are adopting PQC-enabled key management systems to secure vehicle identities and multi-cloud orchestration layers. V2X deployments incorporating quantum-safe digital signatures have shown measurable improvements in message integrity and tamper resistance across high-load environments. Automotive cybersecurity frameworks are also integrating zero-trust protocols combined with PQC authentication to reduce attack surfaces in autonomous navigation systems. Across global R&D centers, innovations such as PQC-secured digital twins, quantum-resistant telematics stacks, and SDV cybersecurity orchestration tools are shaping long-term technological direction for the automotive sector.

• In May 2024, IBM Security expanded its quantum-safe cryptography portfolio by integrating PQC algorithms into its automotive-grade secure key management platform, enabling OEMs to protect telematics and OTA workflows at scale. Source: www.ibm.com

• In February 2024, PQShield launched a new suite of embedded PQC libraries optimized for automotive microcontrollers, enabling low-latency key exchange for V2X and ECU networks across multiple OEM test fleets. Source: www.pqshield.com

• In December 2023, Thales Group partnered with a European automotive manufacturer to deploy quantum-resistant digital signatures across SDV firmware pipelines, enhancing long-lifecycle protection for millions of connected vehicles. Source: www.thalesgroup.com

• In August 2023, NXP Semiconductors initiated pilot integration of PQC-enabled secure elements in EV platforms, improving authentication integrity for battery systems and high-speed vehicle communication networks. Source: www.nxp.com

The Automotive Post-Quantum Cybersecurity Market Report provides a comprehensive assessment of quantum-safe digital protection frameworks designed for connected vehicles, electric mobility platforms, SDVs, autonomous fleets, and V2X ecosystems. The report covers key market segments including PQC-enabled hardware (secure microcontrollers, encryption chips, secure elements), PQC software frameworks (cryptographic libraries, hybrid encryption stacks), and cloud-based PQC key management systems. It further analyzes applications spanning telematics, OTA updates, autonomous driving modules, smart mobility services, infotainment systems, and predictive maintenance platforms.

Geographically, the study includes detailed assessments of North America, Europe, Asia-Pacific, South America, and Middle East & Africa, outlining region-specific adoption drivers, regulatory structures, and OEM integration patterns. It also highlights technological advancements such as lattice-based encryption, hardware acceleration, zero-trust architectures, quantum-secure V2X frameworks, and SDV cybersecurity orchestration. The report evaluates market influencers including regulatory bodies, automotive cybersecurity mandates, digital infrastructure upgrades, and long-lifecycle encryption requirements. Additionally, it incorporates competitive profiling, emerging innovation pathways, investment trends, and strategic opportunities supporting long-term quantum resilience across global automotive digital ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 325.4 Million |

|

Market Revenue in 2032 |

USD 1,952.0 Million |

|

CAGR (2025 - 2032) |

25.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Infineon Technologies, BlackBerry QNX, Toshiba Digital Solutions, IBM Security, Quantum Xchange, PQShield, DigiCert, Thales Group, Secunet Security Networks, ID Quantique, ISARA Corporation, Arqit Quantum, Wolfspeed, NXP Semiconductors, Kudelski Security, Fortinet |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |