Reports

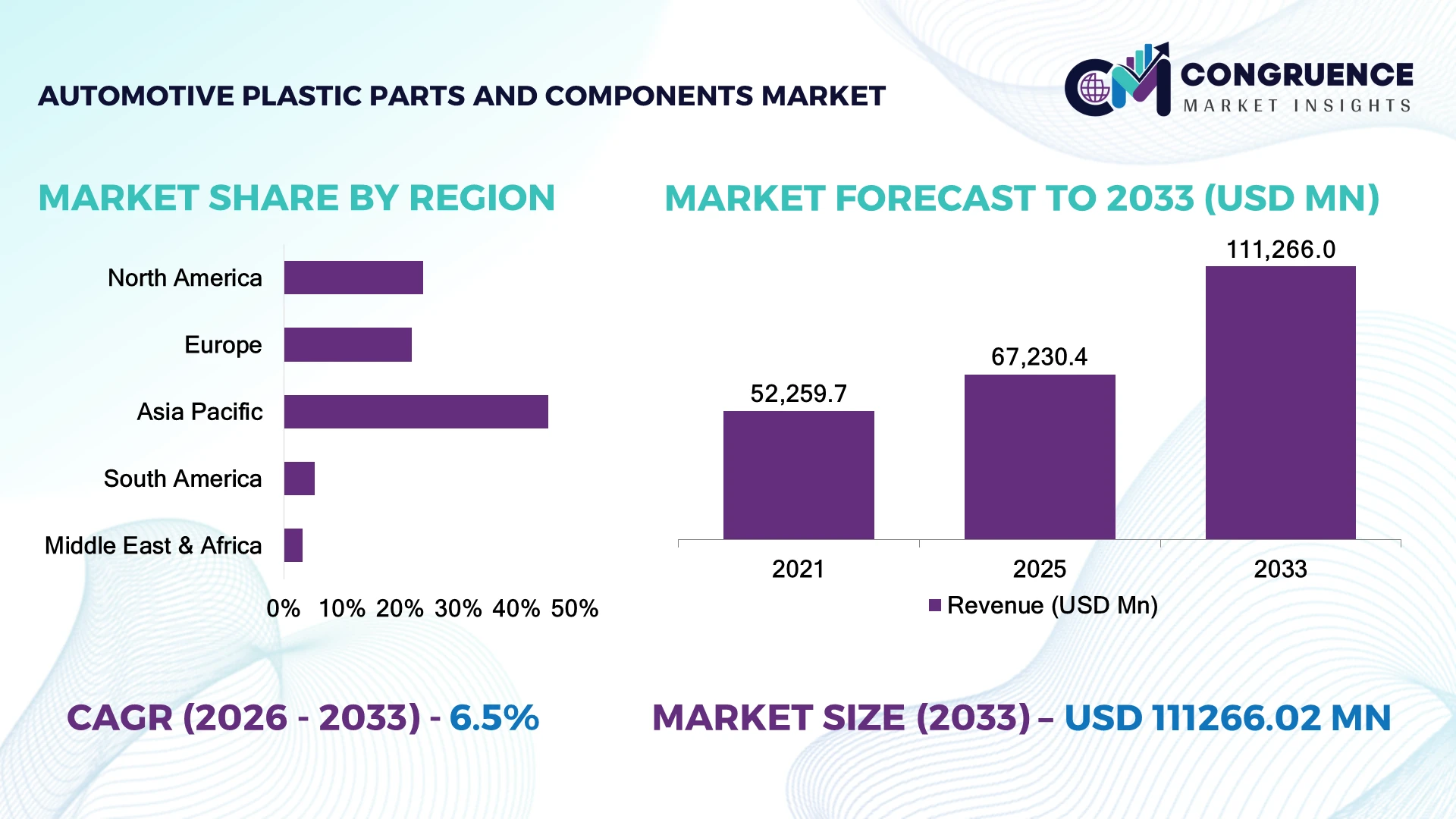

The Global Automotive Plastic Parts and Components Market was valued at USD 67,230.4 Million in 2025 and is anticipated to reach a value of USD 111,266.0 Million by 2033 expanding at a CAGR of 6.5% between 2026 and 2033. Growth is driven by vehicle lightweighting initiatives, accelerating electric vehicle production, and increased adoption of engineered polymers replacing metal components across structural and interior automotive applications.

China accounts for approximately 34% of global automotive plastics production, supported by large-scale vehicle manufacturing, integrated polymer processing, and expanding electric vehicle investments. More than 61% of domestic EV production utilizes advanced lightweight polymer components, while Germany leads Europe in high-performance engineering plastics for premium vehicles. Ongoing global supply-chain realignment and localized manufacturing strategies following geopolitical trade shifts have accelerated investments in regional component production, improving sourcing resilience and manufacturing flexibility.

Manufacturers investing in advanced polymer technologies, localized supply chains, and sustainable materials will secure stronger long-term competitive advantages.

Market Size & Growth: USD 67,230.4 million in 2025, reaching USD 111,266.0 million by 2033 at 6.5% CAGR, driven by vehicle lightweighting and EV expansion.

Top Growth Drivers: Electric vehicle production (+28%), lightweight component adoption (+24%), recycled polymer utilization (+18%).

Short-Term Forecast: By 2028, component manufacturing efficiency improves by approximately 15% through automation and digital molding.

Emerging Technologies: AI-driven quality inspection, bio-based polymers, and advanced injection molding accelerate production.

Regional Leaders: Asia-Pacific (~USD 50 billion), Europe (~USD 25 billion), North America (~USD 22 billion), supported by EV manufacturing expansion.

Consumer/End-User Trends: Around 72% of new passenger vehicles incorporate lightweight plastic-intensive designs.

Pilot/Case Example: In 2026, smart molding systems reduced production defects by approximately 17% across automotive facilities.

Competitive Landscape: Top suppliers control nearly 49% of market demand through material innovation and OEM partnerships.

Regulatory & ESG Impact: Recycled plastic content increased by approximately 21% in newly developed automotive components.

Investment & Funding: More than USD 6.5 billion supports polymer innovation, manufacturing expansion, and regional supply-chain localization.

Innovation & Future Outlook: High-performance composites and circular material strategies strengthen next-generation vehicle platforms.

Automotive plastic parts and components are becoming increasingly critical across electric vehicles, lightweight body structures, battery systems, and advanced interiors. High-performance engineering polymers improve vehicle weight reduction by approximately 30% compared with conventional metal components while supporting stricter efficiency requirements. Increasing localization of automotive supply chains and recycled material integration are reshaping procurement strategies, setting the stage for the strategic market developments outlined below.

The automotive plastic parts and components market has become strategically important as vehicle manufacturers pursue lightweight platforms, electrification, and resilient supply chains simultaneously. Increasing localization of component production, evolving vehicle efficiency regulations, and digital manufacturing investments are transforming supplier selection and competitive positioning. Engineering plastics have evolved from secondary materials into essential structural and functional components supporting next-generation vehicle architectures.

Advanced glass-fiber-reinforced thermoplastics reduce component weight by approximately 32% compared with conventional stamped steel while lowering manufacturing cycle times by nearly 18%. China leads global production through integrated electric vehicle manufacturing ecosystems, whereas Germany focuses on high-performance engineering polymers for premium vehicles and advanced safety systems. Over the next two to three years, approximately 37% of newly introduced vehicle platforms are expected to expand polymer integration across battery enclosures, interior modules, and exterior body components.

Automotive suppliers are expanding polymer compounding facilities, strengthening OEM partnerships, and investing in recycled engineering plastics to support circular manufacturing objectives. Automated injection molding, digital quality inspection, and modular component production improve manufacturing consistency while reducing process waste. Companies combining advanced material innovation, localized production capabilities, and collaborative OEM relationships will secure stronger competitive positioning as vehicle platforms continue transitioning toward lightweight, sustainable, and electrified mobility.

Automotive manufacturers are expanding the use of engineering plastics to reduce vehicle weight, improve energy efficiency, and extend electric vehicle driving range. Lightweight polymer components lower vehicle mass by approximately 25–35% compared with conventional metal parts, while nearly 58% of newly launched EV platforms incorporate high-performance plastics in battery systems and structural assemblies. Tightening vehicle emission regulations and efficiency standards in China have accelerated the substitution of metal with advanced thermoplastics across both passenger and commercial vehicles. This structural shift is driving greater demand for engineered polymers, prompting suppliers to expand compounding facilities, invest in advanced material development, and establish long-term OEM partnerships to secure high-value vehicle programs and strengthen competitive positioning.

Price fluctuations in engineering resins and dependence on petrochemical feedstocks continue to pressure automotive component manufacturers. Raw materials account for approximately 52% of component production costs, while specialty polymers have experienced price variations exceeding 18% during recent supply-chain disruptions. Germany's automotive suppliers also face higher processing costs resulting from elevated industrial energy prices, reducing manufacturing flexibility for complex molded components. These structural constraints compress supplier margins and complicate long-term pricing agreements with OEMs. Companies are reducing exposure by diversifying resin procurement, localizing polymer compounding operations, negotiating strategic supply contracts, and increasing recycled engineering plastic usage to stabilize costs while maintaining component quality and production continuity.

The transition toward circular automotive manufacturing is opening new opportunities for high-performance recycled and bio-based engineering plastics. Approximately 27% of automotive manufacturers have expanded recycled polymer integration across interior and under-the-hood components, while advanced material formulations reduce virgin resin consumption by nearly 20% without compromising structural performance. Japan is accelerating development of chemically recycled automotive plastics to support sustainable vehicle production and material traceability. Suppliers are investing in closed-loop recycling systems, collaborative material innovation, and digital material certification platforms that strengthen OEM sustainability targets. Companies establishing circular material ecosystems today will secure preferred supplier status as sustainability increasingly influences procurement decisions.

Integrating advanced plastics with aluminum, steel, and composite materials across modern vehicle architectures presents growing engineering complexity. Nearly 43% of next-generation vehicle platforms utilize hybrid material assemblies requiring specialized joining technologies, while component validation cycles have lengthened by approximately 16% due to increasing design complexity. The United States automotive sector continues expanding electric vehicle production, placing additional pressure on suppliers to meet stricter thermal, structural, and safety requirements. Companies must invest in simulation-driven engineering, automated inspection systems, and collaborative product development with OEMs to ensure consistent component performance while maintaining scalable production across increasingly sophisticated vehicle platforms.

Recycled Polymer Adoption Expands Automotive manufacturers are increasing recycled engineering plastic usage, with recycled content rising by approximately 21% across newly developed components and material recovery efficiency improving by nearly 17%. Tightening vehicle sustainability requirements are encouraging suppliers to expand recycling partnerships, redesign material flows, and strengthen closed-loop manufacturing systems that reduce raw material dependence.

Digital Molding Optimization AI-enabled injection molding and predictive process monitoring have improved production efficiency by approximately 15% while reducing molding defects by nearly 19%. Smart factory deployment is accelerating across China as manufacturers automate quality control, optimize machine utilization, and shorten production cycles to improve delivery performance for global vehicle manufacturers.

Battery Housing Innovation Electric vehicle manufacturers are replacing metal battery enclosure components with glass-fiber-reinforced thermoplastics, achieving weight reductions of approximately 28% and lowering assembly complexity by nearly 14%. Suppliers are expanding material partnerships and specialized molding capacity to support high-volume EV platform production and improve thermal management performance.

Regional Supply Localization Automotive suppliers are restructuring production networks, with approximately 32% expanding localized polymer compounding and component manufacturing to reduce logistics exposure and improve supply security. Ongoing geopolitical trade adjustments and OEM sourcing diversification are driving investment in regional manufacturing hubs, strengthening production resilience and shortening component delivery lead times.

Engineering plastics accounted for approximately 46% of the automotive plastic parts and components market in 2025, making them the leading material category due to superior mechanical strength, thermal resistance, and compatibility with electric vehicle architectures. Polyamide (PA), polycarbonate (PC), acrylonitrile butadiene styrene (ABS), polyoxymethylene (POM), and polybutylene terephthalate (PBT) remain widely adopted across battery housings, structural brackets, lighting systems, and interior assemblies. Their ability to replace metal while reducing vehicle weight by nearly 30% has accelerated OEM adoption. Material suppliers continue expanding specialty resin production, investing in flame-retardant formulations, and collaborating with automakers to develop application-specific compounds that meet evolving safety and performance requirements.

High-performance composites represent the fastest-growing segment as manufacturers seek lightweight solutions for electric vehicles and premium passenger cars. Commodity plastics, including polypropylene (PP), polyethylene (PE), polyurethane (PU), and PVC, continue serving high-volume interior trims, bumpers, and dashboard applications where cost efficiency remains essential. Approximately 38% of new polymer development programs now focus on recyclable engineering plastics and glass-fiber-reinforced materials. Companies are strengthening advanced material portfolios, expanding regional compounding facilities, and accelerating product qualification to capture growing demand for next-generation automotive platforms.

A 2026 automotive materials assessment reported that engineering plastics remained the preferred material category for lightweight vehicle applications, with OEMs increasing specification of reinforced thermoplastics for structural and electrified vehicle components.

Interior components accounted for approximately 35% of total demand in 2025, supported by widespread use of plastics in dashboards, door panels, center consoles, seating systems, and instrument clusters. Their design flexibility, weight reduction capability, and cost-efficient manufacturing continue to drive large-scale adoption across passenger and commercial vehicles. Approximately 67% of newly launched passenger vehicles incorporate advanced soft-touch polymers and recycled interior materials. Automotive suppliers are investing in decorative molding technologies, sustainable polymers, and integrated electronic interfaces to improve aesthetics, functionality, and manufacturing efficiency.

Battery systems and under-the-hood components represent the fastest-growing application segment as electrification increases demand for lightweight, heat-resistant engineering plastics. Exterior components, lighting systems, powertrain parts, and seating structures remain strategically important, balancing durability with weight optimization. Around 29% of recent product development programs target thermal management applications for electric vehicles through advanced polymer engineering. Manufacturers are expanding automated molding capacity, integrating digital simulation into product development, and strengthening OEM partnerships to support increasingly complex vehicle architectures.

According to a 2025 enterprise survey conducted within the automotive manufacturing sector, interior plastic modules remained the highest-volume application, while battery-related polymer components recorded the strongest increase in engineering design activity.

Passenger vehicle manufacturers accounted for approximately 72% of market demand in 2025, reflecting high production volumes, increasing electrification, and continuous adoption of lightweight materials across virtually every vehicle subsystem. Plastic components are extensively integrated into interiors, exteriors, battery systems, and structural assemblies to improve efficiency and manufacturing flexibility. Approximately 61% of newly introduced passenger vehicle platforms feature expanded engineering plastic content compared with previous generations. Material suppliers continue customizing polymer formulations, strengthening OEM partnerships, and expanding localized production to support evolving vehicle development programs.

Electric vehicle manufacturers represent the fastest-growing end-user segment as battery safety, thermal management, and weight optimization become increasingly critical. Commercial vehicle manufacturers, aftermarket component suppliers, and specialty vehicle producers continue expanding polymer adoption for durability and operational efficiency. Nearly 34% of supplier investments are now directed toward EV-focused plastic component manufacturing, including battery enclosures and high-voltage system applications. Companies are developing dedicated EV material portfolios, implementing collaborative engineering programs, and expanding regional technical support centers to strengthen long-term competitive positioning across rapidly evolving mobility markets.

A 2026 industry assessment found that passenger vehicles remained the largest consumers of automotive plastic components, while electric vehicle manufacturers recorded the fastest increase in engineering plastic utilization across battery, structural, and thermal management applications.

Asia-Pacific accounted for the largest market share at 45.4% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.9% between 2026 and 2033.

Advanced Lightweighting Accelerates OEM Integration

North America accounted for approximately 24% of the global market, supported by strong electric vehicle production, advanced automotive manufacturing, and increasing adoption of engineering plastics across structural, battery, and interior applications. Automakers are replacing conventional metal assemblies with high-performance polymers to improve vehicle efficiency while simplifying production. Nearly 64% of newly developed EV platforms in the region integrate advanced thermoplastics in battery enclosures and lightweight body systems. Suppliers continue expanding injection molding capacity, digital manufacturing, and localized polymer compounding to strengthen supply resilience. Recent investments in automated production facilities have improved component manufacturing efficiency by approximately 16%, enabling suppliers to meet increasing OEM localization requirements and reduce production lead times.

United States Market Outlook: The United States dominates the regional market through its large automotive production base, expanding electric vehicle manufacturing, and strong engineering capabilities. Approximately 72% of regional engineering plastic demand originates from U.S. vehicle assembly operations. Automotive suppliers continue investing in advanced molding technologies, recycled polymer development, and collaborative OEM product engineering to support lightweight vehicle platforms, battery safety requirements, and domestic manufacturing expansion.

Sustainable Materials Redefine Vehicle Manufacturing

Europe represents approximately 22% of the global market, driven by strict vehicle emission standards, premium automotive manufacturing, and rapid integration of recycled engineering plastics. Vehicle manufacturers increasingly specify lightweight polymers to improve efficiency while supporting circular manufacturing objectives. Around 31% of newly developed automotive plastic components in Europe incorporate recycled or bio-based materials. Material suppliers are expanding advanced compounding facilities, strengthening collaborations with premium OEMs, and introducing low-carbon production technologies that enhance manufacturing sustainability and regulatory compliance.

Germany Market Outlook: Germany remains Europe's largest automotive plastics market due to its concentration of premium vehicle manufacturers, advanced polymer engineering, and high-value automotive supply chains. Approximately 43% of European engineering plastic demand is generated by German automotive production. Companies continue expanding lightweight composite development, precision molding technologies, and automated production systems to strengthen competitiveness across premium passenger vehicles and next-generation electric mobility platforms.

Integrated Manufacturing Ecosystems Strengthen Global Leadership

Asia-Pacific contributes approximately 45.4% of the global market, supported by extensive automotive production, integrated polymer manufacturing, and rapidly expanding electric vehicle supply chains. China, Japan, South Korea, and India continue strengthening regional competitiveness through large-scale manufacturing and localized raw material availability. More than 69% of automotive plastic component production is supported by automated molding technologies, improving production consistency and reducing processing waste. Suppliers are expanding technical centers, increasing engineering polymer output, and investing in smart manufacturing infrastructure to meet growing domestic and export demand.

China Market Outlook: China leads the global automotive plastic parts and components market through its unmatched vehicle production scale, integrated petrochemical industry, and rapidly expanding electric vehicle ecosystem. Approximately 34% of global automotive plastic component manufacturing capacity is concentrated in China. Domestic suppliers continue investing in advanced engineering plastics, battery-grade polymers, and intelligent production facilities while strengthening partnerships with leading vehicle manufacturers to improve localization and export competitiveness.

Regional Manufacturing Supports Import Substitution

South America accounts for approximately 5.3% of the global market, with automotive production increasingly supported by localized plastic component manufacturing and expanding supplier networks. Vehicle manufacturers are replacing imported plastic assemblies with regionally produced components to improve supply continuity and reduce logistics costs. Nearly 27% of new supplier investments focus on localized injection molding and interior component manufacturing. Infrastructure modernization and OEM localization programs continue strengthening regional production capabilities despite periodic raw material supply constraints and currency-related cost pressures.

Brazil Market Outlook: Brazil represents the largest automotive plastics market in South America due to its well-established vehicle manufacturing industry and diversified supplier base. Around 58% of regional automotive plastic component production is concentrated in Brazil. Manufacturers continue expanding engineering plastic processing capacity, improving localized tooling capabilities, and strengthening partnerships with international OEMs to enhance production efficiency and reduce dependence on imported automotive components.

Industrial Diversification Expands Component Manufacturing

The Middle East & Africa accounts for approximately 3.8% of the global market, supported by automotive industrial diversification, growing vehicle assembly operations, and investments in polymer processing infrastructure. Governments are encouraging domestic manufacturing through industrial development programs that strengthen local automotive supply chains. Approximately 19% of recent automotive manufacturing investments in the region include plastic component production and processing capabilities. Suppliers are expanding regional partnerships, improving logistics infrastructure, and establishing localized molding operations to support emerging vehicle manufacturing activities.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's most strategically important automotive plastics market through large-scale industrial diversification, petrochemical integration, and investments in vehicle manufacturing. Approximately 24% of new automotive industrial projects announced in the country include plastic component production or polymer processing facilities. Companies are leveraging domestic feedstock availability, advanced industrial zones, and strategic partnerships to build competitive automotive supply chains serving both domestic manufacturers and export markets.

Global material innovators including BASF, SABIC, Covestro, Celanese, and LANXESS compete directly for high-value OEM programs, while regional compounders challenge them through cost efficiency and localized supply. Tier-1 automotive suppliers compete on integrated component design rather than resin production, creating parallel competition between material developers and system integrators. The top five players collectively account for approximately 48% of the market. Competition is driven by material performance, lightweighting capability, supply reliability, and development speed, with advanced polymers reducing component weight by nearly 30% and automated compounding improving production efficiency by approximately 16%. Companies are expanding regional manufacturing, forming joint development agreements with automakers, investing in recycled engineering plastics, and vertically integrating compounding capabilities. Competitive advantage is shifting from commodity resin supply toward application-specific material engineering and circular solutions. Strict automotive qualification requirements, lengthy validation cycles, and OEM certification remain major entry barriers. Success depends on technical collaboration, localized manufacturing, sustainable innovation, and rapid commercialization.

BASF SE

SABIC

Covestro AG

Celanese Corporation

LANXESS AG

LyondellBasell Industries N.V.

Borealis AG

Asahi Kasei Corporation

LG Chem Ltd.

Mitsubishi Engineering-Plastics Corporation

Solvay SA

DuPont de Nemours, Inc.

RTP Company

Avient Corporation

Advanced engineering plastics, glass-fiber-reinforced thermoplastics, and precision injection molding dominate current automotive component manufacturing. Approximately 66% of newly developed electric vehicle platforms integrate engineering plastics across battery systems, interior modules, and structural applications. AI-enabled process monitoring improves molding consistency by nearly 15%, while digital quality inspection reduces production defects by approximately 18%. Automated compounding and simulation-driven material design enable suppliers to shorten development cycles and improve manufacturing flexibility for complex vehicle architectures.

Emerging technologies include chemically recycled engineering plastics, carbon-fiber-reinforced thermoplastics, and additive manufacturing for rapid tooling and prototype validation. Compared with conventional stamped steel components, reinforced thermoplastics reduce weight by approximately 32% while lowering manufacturing energy consumption by nearly 20%. Global material innovators such as BASF, SABIC, Covestro, and Celanese gain competitive advantages through proprietary formulations, integrated compounding capabilities, and collaborative development with automotive OEMs seeking lighter, safer, and more sustainable vehicle platforms.

Between 2026 and 2028, digital material passports, AI-assisted polymer formulation, automated inline inspection, and closed-loop recycling systems will reshape automotive plastics manufacturing. Nearly 39% of advanced material investment programs now prioritize recyclable engineering plastics and battery-compatible polymers. Early adopters will strengthen OEM partnerships, accelerate vehicle qualification, reduce lifecycle emissions, and secure long-term supply agreements as electrification and lightweight vehicle design continue redefining competitive requirements.

March 2025 BASF Coatings expanded polyester and polyurethane resin production capacity at its Caojing facility in Shanghai from 8,000 to 18,800 metric tons annually, strengthening automotive materials supply across Asia-Pacific and improving support for growing OEM production programs. Source: basf.com

October 2025 BASF signed a binding agreement with Carlyle for its automotive OEM coatings and surface treatment businesses in a €7.7 billion transaction, sharpening strategic focus while establishing an independent coatings business dedicated to automotive customers. Source: basf-coatings.com

March 2026 SABIC introduced new LNP ELCRIN recycled compounds and KONDUIT thermal management materials for automotive applications, expanding sustainable material solutions with high post-consumer recycled content for electric vehicle and advanced mobility components. Source: sabic.com

July 2026 Covestro signed a strategic partnership with BYD covering advanced materials for mobility, energy, and technology applications, strengthening long-term material collaboration and accelerating development of next-generation lightweight automotive components. Source: covestro.com

The report provides comprehensive analysis of automotive plastic parts and components across engineering plastics, commodity plastics, high-performance composites, and specialty polymers. It evaluates applications including interior components, exterior systems, under-the-hood assemblies, battery systems, lighting, seating, and structural modules across passenger vehicles, electric vehicles, commercial vehicles, and aftermarket demand. Regional coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by country-level manufacturing trends, material adoption, and supply-chain dynamics. More than 45% of the assessment focuses on engineering plastics and lightweight vehicle technologies driving next-generation mobility.

The study also examines injection molding, polymer compounding, recycled engineering plastics, digital manufacturing, AI-enabled quality inspection, and advanced composite technologies shaping industry competitiveness. It benchmarks leading companies, evaluates deployment patterns, localization strategies, and material innovation, while providing actionable insights for investment planning, manufacturing expansion, supplier selection, competitive positioning, and strategic decision-making across the automotive plastic parts and components market between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 67,230.4 Million |

|

Market Revenue in 2033 |

USD 111,266.0 Million |

|

CAGR (2026 - 2033) |

6.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, SABIC, Covestro AG, Celanese Corporation, LANXESS AG, LyondellBasell Industries N.V., Borealis AG, Asahi Kasei Corporation, LG Chem Ltd., Mitsubishi Engineering-Plastics Corporation, Solvay SA, DuPont de Nemours, Inc., RTP Company, Avient Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |