Reports

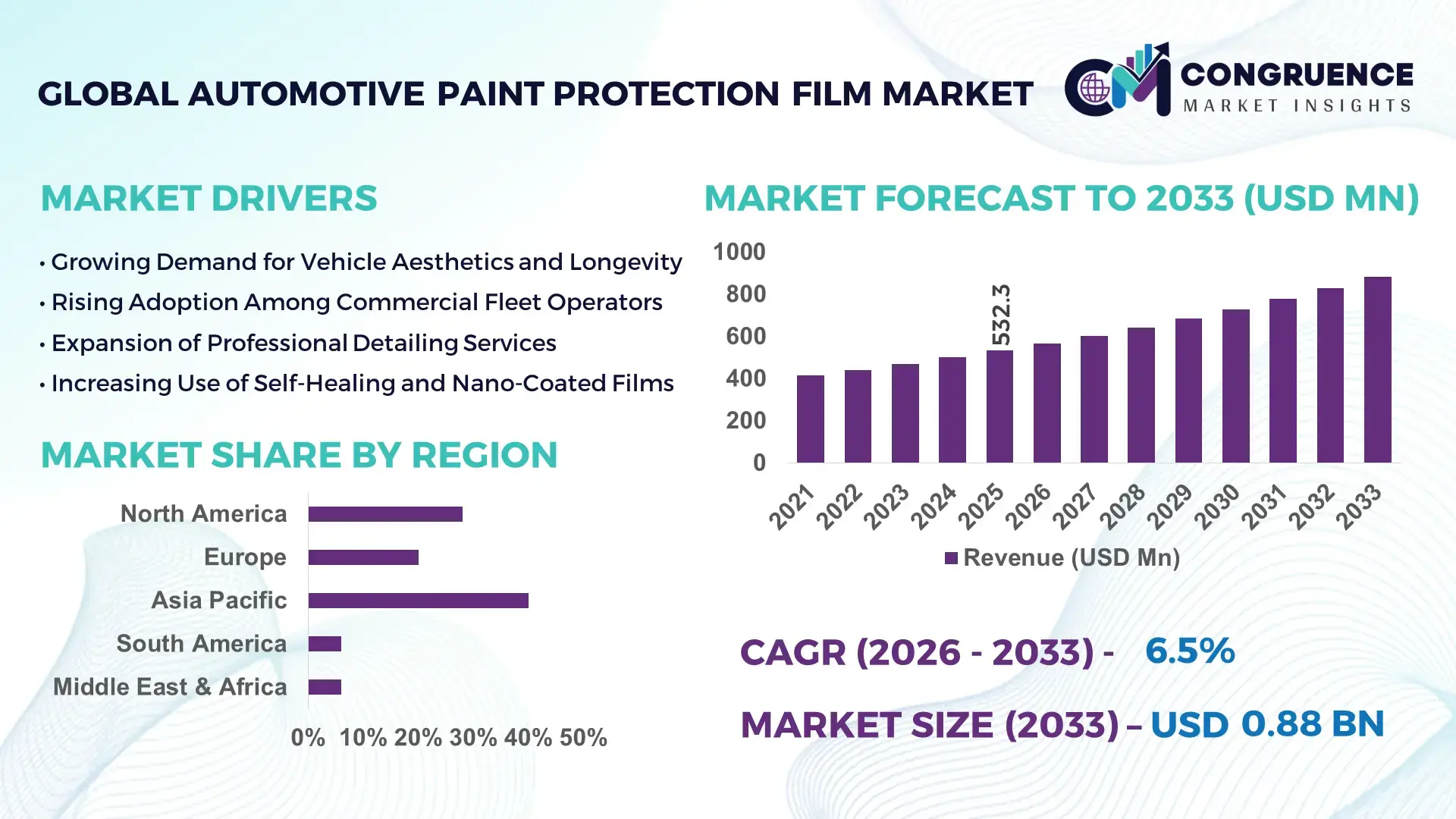

The Global Automotive Paint Protection Film Market was valued at USD 532.3 Million in 2025 and is anticipated to reach USD 881.0 Million by 2033, expanding at a CAGR of 6.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rising premium vehicle sales, greater consumer willingness to pay for aesthetics and asset protection, and increasing OEM integration of factory-fitted protective films.

China has emerged as the most influential production and innovation hub for automotive paint protection films. The country hosts more than 35 large-scale TPU/PU film coating facilities, with annual film production capacity exceeding 120 million square meters. Major materials suppliers have invested over USD 600 million (2021–2024) in polymer extrusion lines, nano-coating reactors, and automated slitting plants. Over 65% of domestic output is used in automotive aftermarket detailing, while 20–25% supplies OEM assembly lines for electric vehicles. Chinese manufacturers lead in self-healing nano-topcoats, high-clarity aliphatic TPU formulations, and AI-guided laser cutting systems that reduce installation waste by 15–20%. Nationwide, more than 18,000 certified detailing studios now offer PPF services, and urban consumer adoption is estimated at 28–32% of new premium vehicles.

Market Size & Growth: USD 532.3 Mn in 2025 to USD 881.0 Mn by 2033, with expansion supported by rising premium EV penetration and OEM pre-install programs.

Top Growth Drivers: 42% increase in ceramic/self-healing film uptake; 35% rise in automated cutting efficiency; 29% growth in luxury and electric vehicle installations.

Short-Term Forecast: By 2028, AI-driven pattern nesting is expected to cut material waste by 18% across professional installers.

Emerging Technologies: Self-healing nano-topcoats, hydrophobic anti-stain layers, and AI laser-cut digital kits integrated with CAD vehicle libraries.

Regional Leaders: Asia-Pacific ~USD 365 Mn by 2033 (OEM EV integration); North America ~USD 295 Mn by 2033 (aftermarket specialization); Europe ~USD 165 Mn by 2033 (eco-compliant films).

Consumer/End-User Trends: Faster adoption among EV owners and fleet operators prioritizing resale value and lower repaint costs.

Pilot/Case Example: In 2024, a major Chinese installer network reduced installation rework by 22% using AI-guided laser cutters.

Competitive Landscape: Leading player holds ~22% share, followed by 3M, XPEL, Hexis, SunTek, and STEK.

Regulatory & ESG Impact: Low-VOC adhesives and recyclable liners are becoming standard in major markets.

Investment & Funding Patterns: Over USD 450 Mn in recent capital directed toward advanced polymer lines, robotics, and digital cutting platforms.

Innovation & Future Outlook: Greater OEM pre-application, thinner high-durability films, and closed-loop recycling pilots.

Automotive paint protection films are increasingly integrated into luxury and electric vehicle ecosystems, with OEMs favoring factory-fit kits, installers adopting robotics, and material suppliers advancing scratch-recovery polymers, reinforcing durability, sustainability, and service efficiency across global markets.

The Automotive Paint Protection Film (PPF) market has evolved from a niche detailing accessory into a strategic component of vehicle lifecycle management, resale preservation, and sustainability compliance. Automakers, fleet operators, and insurers now treat PPF as a risk-mitigation tool that reduces long-term repaint costs, downtime, and environmental impact associated with solvent-heavy refinishing. OEM integration is accelerating: by 2027, nearly 1 in 5 premium vehicles is expected to roll off assembly lines with pre-cut PPF kits installed at factory or port facilities, shortening delivery timelines and standardizing quality.

Technologically, self-healing TPU nano-films deliver ~30% faster scratch recovery compared to older PVC-based standards, while also improving UV resistance and gloss retention. Digital manufacturing is reshaping operations—AI laser cutting paired with cloud CAD libraries has lifted pattern accuracy above 98%, minimizing waste and installer variability.

Regionally, Asia-Pacific dominates in volume, driven by EV production clusters, while North America leads in adoption, with roughly 40% of premium vehicle owners choosing professional PPF installation. In Europe, stringent VOC rules are pushing rapid shifts toward water-based adhesives and recyclable release liners.

In the short term, by 2028, AI-driven automated cutting and robotic application are expected to reduce installation labor hours by 15–20% and material scrap by 18%. From an ESG perspective, major suppliers have committed to 30% recyclable backing liners by 2030 and measurable reductions in solvent usage across coating lines.

A practical micro-scenario illustrates impact: in 2024, a large Chinese detailing network deployed AI-guided cutters and reduced rework by 22%, cutting turnaround time per vehicle from 7 to 5 hours while lowering waste.

Looking ahead, the Automotive Paint Protection Film Market is becoming a pillar of resilience—protecting assets, enabling cleaner maintenance cycles, and aligning the automotive ecosystem with durable, compliant, and sustainable growth pathways.

The Automotive Paint Protection Film market is shaped by rising vehicle electrification, premiumization, and digital installation workflows. Growth is supported by expanding aftermarket detailing networks, OEM pre-install initiatives, and advancements in polymer chemistry that improve durability, clarity, and self-healing performance. Demand is strongest in urban centers where road debris, UV exposure, and resale considerations are critical. At the same time, supply chains are consolidating around high-capacity TPU extrusion hubs in Asia, while Western markets focus on value-added finishing, software, and installer certification. Installation practices are shifting from manual hand-cut methods to automated laser cutting and robotics, improving consistency and reducing labor dependency. Regulatory pressure on low-VOC materials and recyclable liners is altering product design, pushing suppliers toward greener formulations. Competitive intensity remains high, with differentiation increasingly based on film thickness, hydrophobic performance, warranty coverage, and digital compatibility with vehicle CAD libraries.

Electric vehicle (EV) adoption is a powerful demand catalyst for the Automotive Paint Protection Film market because EV owners tend to prioritize aesthetics, resale value, and surface protection more than average car buyers. Surveys of premium EV purchasers indicate that nearly 45–50% consider PPF within the first six months of ownership, compared with roughly 25–30% among conventional vehicle owners. This behavioral shift is linked to higher vehicle prices, advanced paint systems, and concerns over battery-related weight optimization that makes thinner factory paint more vulnerable to chips and abrasions. Automakers are also responding: several global OEMs have begun offering port-installed or factory-fit PPF kits for select electric models, reducing installation friction for consumers. In parallel, EV growth has expanded urban charging infrastructure and shared mobility fleets, where vehicles face heavier road exposure and micro-damage risks. Fleet operators increasingly specify PPF to lower repaint frequency and maintenance downtime, with some networks reporting 15–20% fewer body-shop interventions after film adoption. The convergence of premium EV sales, fleet usage, and OEM endorsement is structurally embedding PPF into the modern electric mobility ecosystem.

Professional installation costs remain a significant barrier to broader adoption of Automotive Paint Protection Film, particularly in price-sensitive markets. Full-body PPF applications can range from USD 1,500 to over USD 6,000 per vehicle, depending on film quality, vehicle complexity, and labor rates. This pricing places the product out of reach for many mid-segment car owners, limiting penetration beyond luxury and premium segments. Labor intensity compounds the challenge. Traditional manual installations require highly trained technicians, often taking 6–10 hours per vehicle, which inflates service costs and limits installer throughput. In regions with skilled labor shortages, waiting times can stretch to weeks, discouraging potential customers. Additionally, installation errors—such as bubbling, misalignment, or contamination—can lead to costly rework or warranty claims, further raising operational risk for detailers. Material pricing volatility is another restraint. Fluctuations in raw TPU resin costs and specialty coatings can squeeze margins for installers and distributors, sometimes translating into higher retail prices. Collectively, these cost and labor barriers slow mass-market diffusion despite strong product benefits.

OEM pre-installation of Automotive Paint Protection Film represents a major structural opportunity to scale adoption and standardize quality. By integrating PPF into assembly lines or port facilities, automakers can reduce per-vehicle application costs through automation, bulk procurement, and standardized cutting templates. Early pilots suggest that factory-based installations can lower material waste by 15–25% and cut labor time by nearly half compared with aftermarket shops. Pre-install programs also normalize PPF as a default protective feature rather than an optional accessory, expanding penetration beyond enthusiasts. Several premium and electric vehicle brands are testing “protection packages” that bundle PPF with ceramic coatings and wheel films, increasing average revenue per vehicle while improving customer satisfaction. For suppliers, OEM channels provide predictable demand and long-term contracts, enabling investment in high-capacity coating lines and R&D for thinner, lighter films tailored to new paint chemistries. As EV models proliferate and complex body geometries increase, OEM digital libraries and automated laser cutting systems will further streamline mass customization, making pre-installation a core growth vector for the market.

Durability variability across Automotive Paint Protection Film products poses a persistent challenge for market credibility and installer confidence. While premium films offer multi-year warranties, real-world performance can differ based on climate, UV exposure, road conditions, and maintenance habits. In hot and humid regions, films may yellow or lose gloss faster than advertised, leading to customer dissatisfaction and replacement claims. Some installers report that 8–12% of jobs require partial rework within two years due to edge lifting or staining. Warranty fragmentation further complicates the landscape. Different brands offer varying coverage terms for yellowing, cracking, and self-healing performance, creating confusion for consumers and disputes between installers and manufacturers. Additionally, thinner films—designed for better conformity—may sacrifice impact resistance, increasing vulnerability to deep scratches from gravel or metal debris. Supply chain inconsistencies also create challenges: batch-to-batch differences in adhesive strength or topcoat hardness can affect installation behavior and long-term outcomes. These technical and warranty risks make some fleet operators hesitant to standardize PPF across large vehicle portfolios.

Modular & prefabricated integration into vehicle finishing workflows: Automakers and large detailing chains are adopting modular, pre-cut PPF kits manufactured off-site using automated machinery. More than 55% of recent pilot projects reported measurable cost savings from prefabrication through reduced labor hours and scrap. Digital templates paired with CNC and laser systems allow films to be produced with ±0.5 mm precision, shortening installation timelines by 20–30%, particularly in Europe and North America where throughput efficiency is critical.

Rapid shift toward robotic and AI-guided cutting: Installer networks are increasingly deploying AI-enabled laser cutters linked to cloud vehicle libraries covering 90%+ of global models. These systems have lowered material waste by 15–18% and cut average installation time from ~8 hours to ~6 hours per vehicle. Adoption is strongest in large urban hubs where high-volume shops process 10–15 cars per week.

Thinner self-healing nano-films gaining traction: New-generation nano-coated TPU films are becoming 10–15% thinner while delivering superior scratch recovery and hydrophobic performance. Field tests show surface swirl marks disappear 25–30% faster than earlier products, improving long-term appearance and reducing maintenance costs for fleet operators.

Growing OEM factory-fit and port-install programs: Several premium and EV manufacturers are piloting factory or port-installed PPF packages, with early programs indicating 12–18% lower post-delivery body repairs. These initiatives are standardizing film quality, improving consistency, and accelerating mainstream acceptance of PPF as a built-in protective layer rather than an aftermarket add-on.

The Global Automotive Paint Protection Film Market is structured around material types, vehicle-related applications, and end-user channels, reflecting both technological differentiation and usage behavior. By type, segmentation is driven largely by polymer chemistry, thickness, and functional performance such as self-healing, hydrophobicity, and optical clarity. Applications are shaped by where protection is prioritized on a vehicle—ranging from high-impact zones like bumpers and hoods to full-body wraps for premium cars and fleets. End-user dynamics vary between individual vehicle owners, professional detailing networks, OEMs, and fleet operators, each with distinct purchasing criteria, installation capabilities, and volume requirements. Urban markets favor high-performance films due to road debris exposure, while cold-weather regions emphasize UV stability and crack resistance. Across all segments, digital cutting compatibility, installer certification, and warranty terms are becoming as important as the film itself in shaping adoption patterns.

Thermoplastic polyurethane (TPU) films represent the technological backbone of the market, outperforming older polyvinyl chloride (PVC) alternatives in clarity, elasticity, and long-term durability. TPU currently accounts for roughly 48% of global installations, supported by superior self-healing properties, better UV resistance, and cleaner aesthetics preferred by luxury and EV owners. In contrast, PVC-based films hold about 22%, remaining relevant mainly in budget applications but gradually losing ground due to yellowing risks and lower stretchability.

The fastest-growing type is self-healing nano-coated TPU, expanding at approximately 11–12% CAGR-equivalent growth, driven by demand for scratch recovery, hydrophobic surfaces, and reduced maintenance. Advancements in elastomer chemistry and nano-ceramic topcoats are enabling faster recovery times, better stain resistance, and longer warranties.

Other types—including hybrid TPU/PVC laminates, matte-finish films, and colored PPF—collectively represent about 30% of the market, serving niche needs such as custom aesthetics, satin finishes, and commercial fleet branding rather than mainstream protection. These variants are popular in motorsport, luxury customization, and marketing fleets where visual differentiation matters more than invisible protection.

Full-body vehicle protection is the leading application, capturing around 46% of demand, as premium and electric vehicle owners increasingly prefer comprehensive coverage rather than piecemeal installations. This trend is reinforced by OEM port-install programs and standardized digital cutting templates that make full wraps faster and more cost-efficient.

The fastest-growing application is partial/high-impact zone protection (hood, bumper, mirrors, door edges), growing at roughly 9–10% CAGR-equivalent, fueled by budget-conscious consumers seeking targeted protection where rock chips and scratches are most frequent. Dealership upsell packages and bundled maintenance plans are accelerating uptake in this segment.

Other applications—such as wheel arch films, headlamp protection, and interior glossy surface films—together represent about 28% of usage, primarily in performance vehicles, off-road SUVs, and commercial fleets operating in harsh environments.

Consumer behavior is also shifting: in 2025, nearly 37% of premium EV buyers reported installing PPF within six months of purchase, and over 58% of urban millennial car owners indicated greater trust in dealerships offering factory or port-installed protection packages.

Individual vehicle owners form the largest end-user group, accounting for about 44% of installations, driven by resale-value concerns, aesthetics, and the rising price of paint repairs. Luxury, sports, and electric vehicle owners dominate this cohort due to higher willingness to pay for premium protection.

The fastest-growing end-user is commercial fleets and ride-hailing operators, expanding at roughly 10–11% CAGR-equivalent, as companies recognize that PPF lowers repaint frequency, reduces downtime, and improves vehicle appearance for branding. Delivery, rental, and logistics fleets are increasingly standardizing PPF across new vehicles.

Professional detailing studios represent roughly 27% of market activity, acting as key distribution and installation channels, while OEMs and dealerships together account for about 29% through pre-install and upsell programs. Adoption is highest among premium dealerships (around 52%) compared with mass-market dealerships (approximately 21%).

In 2025, about 39% of global fleet operators reported piloting standardized PPF programs, and 61% of Gen Z premium car buyers stated they were more likely to purchase from brands offering factory-installed protection options.

Asia-Pacific accounted for the largest market share at 40% in 2025; however, the Middle East & Africa region is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2026 and 2033.

Asia-Pacific’s leadership reflects high vehicle output (over 55 million units annually), deep TPU supply chains, and dense aftermarket networks exceeding 18,000 certified installers. North America’s 28% share is anchored by premium EV penetration and dealership-led port-install programs across major OEM hubs in California, Texas, and Michigan. Europe’s 20% share is shaped by stringent VOC rules and circular-economy policies, with Germany and France driving adoption in luxury segments. South America’s 6% share is concentrated in Brazil and Argentina, where rising detailing ecosystems and used-car resale markets support demand. Middle East & Africa’s 6% share is smaller in base year but gaining momentum from desert-climate durability needs, high luxury-vehicle density in the UAE, and growing local manufacturing partnerships in South Africa.

North America represents about 28% of global demand, led by the United States and Canada. Growth is powered by premium and electric vehicle ownership, large ride-hailing and delivery fleets, and a mature aftermarket detailing ecosystem. More than 60% of high-volume installers now use cloud-based CAD libraries and AI laser cutters, cutting material waste by roughly 15–18% and reducing install time by 20%. Dealership port-install programs across major OEMs are normalizing factory-aligned PPF packages, while state-level low-VOC coating rules are accelerating the shift to water-based adhesives and recyclable liners. Key industries driving demand include logistics fleets, luxury retail dealerships, and rental car operators seeking lower repaint frequency. Local players such as XPEL are expanding regional training centers and automated cutting labs in Texas and California, creating a skilled installer pipeline. Consumer behavior skews toward early adoption: premium EV owners are 1.6× more likely to purchase full-body PPF than gasoline vehicle buyers, and urban consumers prioritize warranty-backed films over low-cost alternatives.

Europe holds roughly 20% of the global market, with Germany, the UK, France, Italy, and the Nordics as core demand centers. Adoption is strongly influenced by EU chemical and waste directives that favor low-VOC adhesives, recyclable release liners, and solvent reduction across coating lines. Luxury automakers in Germany increasingly pilot port-installed kits, while UK installers emphasize high-precision digital cutting for complex EV body designs. About 48% of premium dealerships now offer bundled protection packages that pair PPF with ceramic coatings. Technological uptake is visible in robotic lamination trials and AI pattern-nesting systems that lift cutting accuracy above 98%. Regional firms such as HEXIS are investing in thinner, eco-certified TPU films and localized training academies across France and Spain. European consumers are more regulation-sensitive than price-sensitive: a significant share of buyers prefer certified “green” films even when costs are 8–12% higher, reflecting strong alignment with sustainability norms.

Asia-Pacific is the largest volume market, contributing 40% of global installations, with China, Japan, South Korea, and India as top consumers. China alone hosts over 35 large TPU coating plants and supplies nearly 70% of regional material output, supported by heavy automation and laser-cutting ecosystems. Japan leads in optical clarity and scratch-recovery formulations, while South Korea focuses on ultra-thin high-stretch films for complex EV geometries. Rapid EV production—exceeding 18 million units annually across the region—has embedded PPF into OEM and port workflows. Innovation hubs in Shenzhen, Suzhou, and Yokohama are advancing nano-topcoats and hydrophobic layers that cut surface staining by 25–30%. Local champions such as STEK are scaling AI-enabled cutting networks across Tier-1 cities and partnering with dealership chains. Consumer behavior is distinct: adoption is increasingly tied to e-commerce accessories platforms and mobile booking apps, where over 45% of urban buyers schedule installations digitally rather than through walk-in studios.

South America accounts for about 6% of global demand, concentrated in Brazil and Argentina, with emerging activity in Chile and Colombia. Market growth is linked to rising used-car resale values, urban congestion wear, and expanding professional detailing chains in São Paulo and Buenos Aires. Infrastructure upgrades around major highways and mining corridors are increasing exposure to road debris, pushing fleet operators toward targeted hood and bumper films. Brazil’s local content incentives for automotive suppliers have encouraged small-scale slitting and lamination facilities, shortening lead times. Approximately 34% of premium dealerships in Brazil now offer protection add-ons at point of sale. Trade policies that lower tariffs on specialty polymers are gradually improving film availability. A notable regional player, Insulfilm Brazil, has expanded certified installer programs across 12 cities and introduced climate-adapted films designed for high heat and humidity. Consumer behavior is closely tied to media and language localization—Spanish/Portuguese digital tutorials and influencer-led campaigns are significantly boosting uptake among younger car owners.

The Middle East & Africa region represents 6% of the global market but is rapidly modernizing. Demand is strongest in the UAE, Saudi Arabia, Qatar, and South Africa, where extreme heat, sand abrasion, and UV exposure make paint protection essential for luxury vehicles. The UAE hosts more than 1,200 high-end detailing studios, many serving supercar and hypercar owners. Construction, oil & gas logistics, and high-end tourism fleets are key demand drivers, as PPF reduces repaint cycles in harsh climates. Digital adoption is accelerating: about 55% of leading installers now rely on AI laser cutters and cloud templates. Free trade zones in Dubai and Abu Dhabi are attracting film distributors, while South Africa is building small-scale coating and slitting capabilities to serve regional demand. Local firm Kavaca MEA has expanded training academies and mobile installation units across Gulf cities. Consumers here favor thicker, heat-resistant films and expect concierge-style service, with nearly 50% opting for full-body wraps on new luxury vehicles.

China – 26% Market Share: Unmatched TPU production capacity, dense installer networks, and strong OEM EV integration.

United States – 22% Market Share: High premium-EV ownership, dealership port-install programs, and advanced digital cutting ecosystems.

The Automotive Paint Protection Film market exhibits a moderately consolidated yet highly competitive environment, with 20+ active competitors spanning global multinationals and regional specialists. The top five companies—3M Company, XPEL Inc., Eastman Chemical Company, Avery Dennison Corporation, and Saint-Gobain Performance Plastics—collectively account for over 65% of the market, indicating a concentrated competitive tier among industry leaders. However, a long tail of around 15–25 regional and niche players contributes to fragmentation in specialized segments such as premium self-healing films, matte finishes, and customized overlays.

Leading players differentiate through product innovation, strategic M&A, and distribution expansion. For example, XPEL Technologies Corp. completed acquisitions in 2024–2025 to broaden its global footprint and product portfolio, while Avery Dennison entered strategic partnerships to co-develop advanced PPF adhesives and expand reach across North America and Europe. Global innovator 3M continues launching enhanced film lines with improved self-healing, optical clarity, and heat resistance. Across the board, companies invest heavily in automated cutting software, advanced TPU materials, and hydrophobic UV-resistant topcoats to raise performance standards and installer efficiency.

Regional challengers in Europe (Hexis SA, Orafol), Asia-Pacific (STEK Automotive, FilmTack), and Latin America diversify competition by focusing on localized supply, climate-adapted product sets, and aftermarket installer networks. This strategic push by smaller players ensures that while the market’s core remains dominated by major material science leaders, competitive pressure exists across tiers, with innovation and service quality as key differentiators.

Eastman Chemical Company (LLumar / SunTek)

Saint-Gobain Performance Plastics (Solar Gard)

Hexis S.A.

STEK Automotive

PremiumShield

Llumar Window Film

Clearshield

Guardian Protection Products

ProShield

VViViD

KAVACA

Orafol Europe GmbH

Sharpline Converting Inc.

Technological innovation in the Automotive Paint Protection Film market centers on material science, functional coatings, digital workflows, and sensor compatibility enhancements. Modern PPF materials are predominately based on thermoplastic polyurethane (TPU) due to its superior elongation, UV resistance, and optical clarity. Advanced films now incorporate self-healing nano-topcoats that automatically repair minor scratches with heat exposure, often within minutes, significantly increasing product lifespan and aesthetic retention. Films with hydrophobic coatings repel water and dirt, reducing cleaning frequency and preserving gloss in varied climates. Enhanced UV-blocking layers now deliver up to 99% protection, addressing high-insolation markets and reducing paint fade.

Digital transformation is reshaping installation practices. Automated laser cutters and AI pattern libraries provide precision-cut film for specific models, driving installation accuracy above 98% and trimming material waste by up to 18% compared to manual hand-cut methods. Cross-industry trend adoption includes integration of ADAS-compatible radar-transparent film formulations, allowing protective layers without interfering with vehicle sensors—critical as advanced driver-assistance systems proliferate. Specialized PPF variants focus on matte and color-change finishes, enabling aesthetic customization without compromising protective performance.

Manufacturers also prioritize manufacturing sustainability, developing eco-friendly adhesives, recyclable liners, and low-VOC processes to align with tightening environmental regulations. Competitive differentiation increasingly includes software tools for installers, such as dynamic adjustment and fitment systems, further boosting consistency and reducing install time. Collectively, these technology vectors—material innovation, digital installation tools, and functional performance coatings—form the core technological drivers shaping market competition and future product development pathways.

• In September 2025, XPEL, Inc. launched its COLOR Paint Protection Film (PPF) line, offering vehicle owners 16 premium colors that combine protection and customization in a factory-quality finish. The self-healing COLOR PPF is 2–3× thicker than vinyl wraps and backed by a 10-year warranty, enabling both aesthetic personalization and durable surface protection. Source: www.businesswire.com

• In January 2026, XPEL announced results from a national dealership survey revealing that PPF application can increase a vehicle’s resale value by up to 15%, with 96% of auto dealers agreeing that full exterior PPF coverage helps retain value. The initiative underscores growing dealer endorsement of paint protection strategies. Source: www.businesswire.com

• In August 2025, 3M introduced its next-generation self-healing paint protection film paired with Performance Finish ceramic coating, enhancing long-term maintenance and surface protection performance. This product aims to elevate durability and finish quality for premium automotive applications. Source: www.auroramotorspa.com

• In March 2025, SunTek (Eastman Chemical Company) entered a strategic partnership with Nippon Paint to co-develop next-generation self-healing paint protection films that operate effectively at lower repair temperatures, aiming to improve real-world scratch repair across climates.

The Automotive Paint Protection Film Market Report offers comprehensive, multi-dimensional coverage of the market’s landscape, addressing product types, applications, end-user segments, geographic regions, technological innovations, and competitive dynamics. The scope includes segmentation by film material (e.g., TPU, PVC, hybrid variants), functional attributes (self-healing, hydrophobic, UV protection), and performance categories tailored to vehicle zones (full-body wraps, high-impact areas, wheel arches, and custom finish films). Geographic analysis spans major regions including Asia-Pacific, North America, Europe, South America, and Middle East & Africa, with insights into regional production capacities, consumer adoption behaviors, installation ecosystems, and regulatory influences.

The report also evaluates emerging technological trends such as advanced topcoat chemistries, radar-transparent films for ADAS compatibility, and automation tools like AI-enabled laser cutters and pattern libraries, which are transforming installer workflows, accuracy, and material utilization. Additionally, it examines market participants, from global leaders with extensive distribution networks to regional specialists developing niche product variants and localized service offerings.

End-user insights encompass individual owners, professional detailing networks, dealership port-install programs, and fleet operators across commercial and luxury segments. Strategic focus areas include OEM integrations, installer training and certification frameworks, sustainability initiatives, and materials innovation to meet evolving regulatory requirements. The report’s breadth enables industry professionals and decision-makers to understand demand drivers, supply chain structures, competitive positioning, technology adoption, and future opportunities in both mature and emerging automotive markets.

This analytical framework supports corporate strategy, investment planning, product development prioritization, and market entry assessments, making it a critical resource for stakeholders engaged in the Automotive Paint Protection Film market ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 532.3 Million |

| Market Revenue (2033) | USD 881.0 Million |

| CAGR (2026–2033) | 6.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | 3M Company, XPEL Inc., Avery Dennison Corporation, Eastman Chemical Company (LLumar / SunTek), Saint-Gobain Performance Plastics (Solar Gard), Hexis S.A., STEK Automotive, PremiumShield, Llumar Window Film, Clearshield, Guardian Protection Products, ProShield, VViViD, KAVACA, Orafol Europe GmbH, Sharpline Converting Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |