Reports

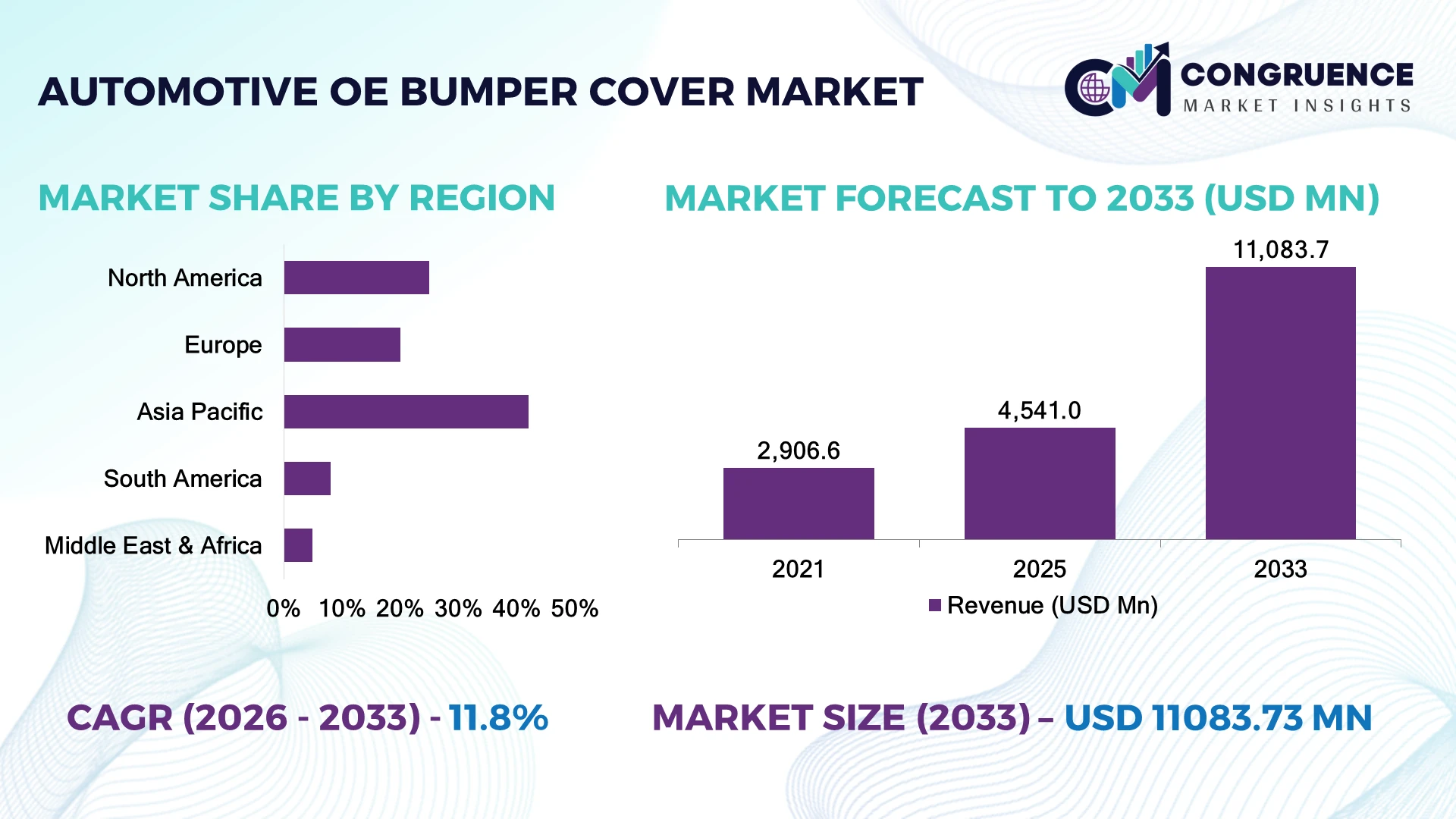

The Global Automotive OE Bumper Cover Market was valued at USD 4,541.0 Million in 2025 and is anticipated to reach a value of USD 11,083.7 Million by 2033 expanding at a CAGR of 11.8% between 2026 and 2033. Growth is driven by rising vehicle lightweighting programs, rapid adoption of advanced polymer composites, and increasing integration of sensor-compatible bumper systems for ADAS-enabled vehicles.

China dominates the market landscape, accounting for nearly 35% of global automotive production capacity with over 30 million vehicles produced annually, supported by major EV manufacturing investments and advanced component ecosystems. The United States follows with strong demand from premium vehicles and autonomous mobility programs, while India is expanding rapidly through local manufacturing initiatives under the “Make in India” automotive push. China’s EV output exceeds 9 million units annually compared with India’s emerging capacity of over 4 million vehicles, highlighting regional scale differences.

Strategic suppliers prioritizing lightweight materials, smart manufacturing, and localized supply chains will gain stronger competitive positioning.

Market Size & Growth: USD 4.54 billion in 2025 to USD 11.08 billion by 2033 at 11.8% CAGR, driven by lightweight vehicle platforms and ADAS-compatible bumper designs.

Top Growth Drivers: Lightweight materials (35%), electric vehicle integration (28%), and automated manufacturing adoption (22%) are shaping market expansion.

Short-Term Forecast: By 2028, manufacturers target 15–20% production efficiency improvements through robotic molding and digital quality systems.

Emerging Technologies: AI-based inspection, automated molding, recycled polymers, and sensor-integrated bumper covers are accelerating advanced automotive production.

Regional Leaders: Asia Pacific reaches approximately USD 5.2 billion by 2033 with EV expansion; North America approaches USD 3.1 billion through autonomous vehicle adoption; Europe exceeds USD 2.4 billion with sustainable material initiatives.

Consumer/End-User Trends: More than 60% of new vehicle platforms prioritize lightweight exterior components to improve efficiency and meet emission standards.

Pilot/Case Example: In 2024, automotive suppliers implementing AI-based defect detection achieved nearly 30% reduction in bumper production quality failures.

Competitive Landscape: Leading suppliers hold significant market influence, including Magna International, Plastic Omnium, Samvardhana Motherson, Flex-N-Gate, and Hyundai Mobis.

Regulatory & ESG Impact: Recycled plastic adoption programs target 25–40% material sustainability improvements across automotive component supply chains.

Investment & Funding: Over USD 10 billion is being directed toward EV component expansion, automation facilities, and localized automotive supply networks.

Innovation & Future Outlook: Next-generation bumper covers will focus on smart sensing, recyclable composites, integrated lighting, and connected vehicle safety systems.

Automotive OE bumper covers are becoming increasingly important as automakers redesign exterior systems for electric mobility, safety technologies, and sustainability requirements. Demand is expanding across passenger vehicles, commercial fleets, and premium segments, with approximately 45% of new vehicle platforms incorporating lightweight polymer-based exterior components. Supply-chain localization in Asia and North America is reshaping supplier strategies as manufacturers strengthen regional production resilience.

The Automotive OE Bumper Cover Market is becoming strategically important as vehicle manufacturers compete on lightweight design, safety integration, and production efficiency. Automakers are restructuring supply chains after recent semiconductor shortages and geopolitical disruptions, increasing investments in regional component manufacturing and advanced polymer processing capabilities.

Technology transformation is creating measurable advantages, with automated injection molding systems reducing production cycle times by nearly 20% compared with conventional manufacturing methods while improving consistency through AI-enabled inspection. Europe emphasizes sustainable materials and circular manufacturing, whereas Asia Pacific leads in production scale through extensive EV manufacturing networks and supplier clusters.

Over the next 2–3 years, automotive suppliers are prioritizing smart factories, recycled composite materials, and sensor-ready bumper platforms. For example, EV manufacturers are increasingly deploying lightweight bumper assemblies that support improved vehicle range and integrated driver-assistance features. Companies are expanding partnerships with polymer producers, automation providers, and vehicle OEMs to secure resilient supply networks.

Strategically, manufacturers that combine material innovation, localized production, and digital manufacturing capabilities will achieve stronger cost control, faster product development cycles, and a durable competitive advantage in the evolving automotive ecosystem.

Rising vehicle lightweighting and safety technology integration are accelerating demand for advanced OE bumper covers, with polymer-based components reducing exterior system weight by nearly 20–30% compared with traditional metal alternatives. Over 60% of new vehicle platforms increasingly incorporate sensor-compatible bumper designs to support ADAS functions. China’s rapid EV production expansion and stricter vehicle efficiency standards are pushing suppliers toward recycled polymers and precision molding technologies. Companies are responding through investments in automated production lines, material partnerships, and localized manufacturing hubs to improve design flexibility, reduce cycle times, and strengthen OEM supply relationships.

Automotive OE bumper cover manufacturers face pressure from fluctuating polymer prices, limited recycled material availability, and dependency on specialized resin suppliers. Raw material costs can account for 40–50% of bumper component production expenses, creating profitability challenges during supply disruptions. European manufacturers continue adapting to stricter recycled-content requirements, while suppliers in Japan and South Korea manage higher compliance and material certification costs. Companies are reducing exposure through multi-source procurement strategies, long-term supplier contracts, and regionalized production networks. A key operational challenge remains balancing sustainable material adoption with cost competitiveness and consistent component performance across high-volume vehicle programs.

Next-generation bumper covers are creating opportunities through smart materials, integrated sensors, and recyclable composite technologies. Advanced polymer adoption is expected to increase as more than 50% of upcoming EV platforms prioritize lightweight exterior architectures to improve efficiency. India’s expanding electric vehicle ecosystem and China’s battery-powered vehicle production provide new opportunities for localized bumper component suppliers. Companies are investing in R&D partnerships focused on self-healing coatings, embedded lighting systems, and AI-supported manufacturing optimization. A significant opportunity lies in developing modular bumper platforms that reduce tooling expenses and enable faster customization across multiple vehicle models.

Automotive OE bumper cover development faces increasing complexity due to sensor integration, material compatibility requirements, and global OEM quality standards. Nearly 35% of advanced vehicle platforms require additional validation processes for radar, camera, and connectivity-enabled bumper systems, increasing engineering timelines. Manufacturers in Germany, the United States, and South Korea are addressing challenges related to precision manufacturing and cybersecurity-linked vehicle components. Companies must invest in digital twins, skilled engineering capabilities, and collaborative development models with OEMs to maintain competitiveness. The critical challenge is achieving scalable production while ensuring consistent performance, recyclability, and compatibility across diverse vehicle architectures.

AI Manufacturing Integration Automotive suppliers are accelerating AI-based inspection and automated production workflows, reducing quality-related rework by approximately 25–35% while improving production consistency. Manufacturers in Japan, Germany, and South Korea are adopting smart factory systems to address labor constraints and improve high-volume bumper production efficiency. Companies are expanding automation investments and digital monitoring capabilities to achieve faster cycle times and stronger OEM quality compliance.

Sustainable Material Transition Bumper cover manufacturers are increasing the use of recycled polypropylene and advanced composite materials, with several vehicle platforms targeting 20–40% recycled content in exterior components. Regulatory pressure in Europe and OEM sustainability targets are reshaping material strategies. Companies are developing partnerships with material innovators and expanding recycling-linked supply chains to reduce environmental impact while maintaining structural performance and cost efficiency.

EV Design Optimization Electric vehicle platforms are driving new bumper cover architectures focused on weight reduction, aerodynamic efficiency, and sensor integration. More than 50% of emerging EV models prioritize lightweight exterior systems to improve driving efficiency. Automotive suppliers in China and India are increasing collaboration with EV manufacturers to develop modular bumper solutions, reduce tooling requirements, and accelerate platform-specific production.

Regional Supply Chain Localization Automotive component producers are restructuring sourcing networks due to logistics volatility and geopolitical supply risks. Localized manufacturing strategies are helping suppliers reduce delivery timelines by 15–20% and improve inventory control. Companies are expanding production capacity near vehicle assembly hubs in China, the United States, and India to strengthen supply resilience and support regional OEM partnerships.

Injection molded bumper covers represent the leading type segment, accounting for approximately 65% of the market due to high-volume manufacturing capability, dimensional accuracy, and compatibility with mass-market passenger vehicles. Their lower production cost, faster tooling cycles, and suitability for thermoplastic materials make them the preferred choice among global OEMs. Thermoformed and composite-based bumper covers hold smaller shares but are gaining attention for specialized applications requiring lightweight structures and premium designs. Composite bumper covers are emerging as the fastest-growing type, supported by increasing EV adoption and demand for weight reduction. These materials can reduce component weight by nearly 15–25% while improving design flexibility. Companies are investing in advanced polymer research, automated molding systems, and supplier partnerships to expand composite production capabilities. The market shift indicates increasing investment toward sustainable, lightweight, and sensor-compatible bumper solutions.

Passenger vehicles represent the leading application segment with approximately 70% market share, driven by large-scale vehicle production, increasing safety requirements, and widespread adoption of standardized bumper systems. Sedans, SUVs, and compact vehicles continue generating strong demand as manufacturers prioritize durable, lightweight, and cost-efficient exterior components. Commercial vehicles maintain steady adoption due to fleet replacement programs and increasing safety compliance requirements. Electric vehicles are the fastest-growing application area as manufacturers redesign bumper systems for improved aerodynamics, sensor integration, and weight optimization. EV-focused bumper applications are expanding as more than 40% of new electric vehicle platforms incorporate advanced exterior component designs. Companies are strengthening partnerships with EV manufacturers and investing in modular bumper technologies to support faster product development.

Automotive OEMs represent the dominant end-user segment, contributing approximately 75% of market demand due to direct vehicle production requirements, design integration, and large-scale procurement contracts. Major manufacturers rely on bumper cover suppliers for customized solutions, quality consistency, and platform-specific development. Tier-1 suppliers and aftermarket providers maintain important roles but operate with lower demand concentration compared with original equipment manufacturers. Electric vehicle manufacturers are the fastest-growing end-user group, supported by new vehicle launches, lightweight design priorities, and increasing supplier collaboration. EV companies are expanding partnerships with component manufacturers to accelerate production and reduce development timelines by nearly 20%. Traditional automakers are also restructuring supplier networks to improve localization and manufacturing flexibility. Companies are increasingly creating long-term supply agreements, expanding engineering collaborations, and developing customized bumper systems to strengthen relationships with global vehicle manufacturers and emerging EV producers.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 13.2% between 2026 and 2033.

North America represents a strategically important automotive OE bumper cover market, supported by strong OEM production networks, electric vehicle investments, and increasing adoption of lightweight exterior components. The region contributes nearly 25% of global automotive component demand, with the United States accounting for the majority of vehicle manufacturing activity. Automakers are accelerating localized sourcing strategies after recent supply-chain disruptions, increasing partnerships with domestic Tier-1 suppliers. More than 50% of new vehicle development programs in the region prioritize weight optimization and integrated safety technologies. Manufacturers are expanding automated molding facilities and digital quality systems to improve production efficiency and reduce dependency on overseas suppliers.

United States Market Outlook: The United States remains the dominant country market due to its large automotive manufacturing base, EV investments, and advanced supplier ecosystem. The country produces over 10 million vehicles annually and is witnessing increased deployment of sensor-compatible bumper systems across premium and electric vehicle platforms. Automotive suppliers are expanding facilities near major assembly hubs to improve delivery efficiency and strengthen OEM partnerships.

Europe maintains a strong position in the Automotive OE Bumper Cover Market due to strict sustainability regulations, premium vehicle production, and advanced material innovation. The region contributes approximately 20% of global automotive component demand, supported by Germany, France, and Italy’s established manufacturing infrastructure. European automakers are increasing recycled polymer usage and integrating environmentally optimized bumper designs to meet carbon reduction targets. Over 30% of new automotive material development programs focus on improved recyclability and reduced component weight. Companies are investing in circular supply chains, automation technologies, and regional partnerships to align with evolving environmental requirements while maintaining production efficiency.

Germany Market Outlook: Germany leads Europe’s automotive component ecosystem through strong OEM presence, engineering expertise, and high automation adoption. The country produces more than 3 million passenger vehicles annually and continues expanding smart manufacturing capabilities for lightweight exterior systems. German suppliers are focusing on advanced polymer solutions, digital production monitoring, and sustainable manufacturing processes to support premium vehicle programs.

Asia-Pacific dominates the Automotive OE Bumper Cover Market through extensive vehicle production capacity, strong supplier networks, and rapid electric vehicle adoption. The region contributes nearly 42% of global market demand, driven by China, Japan, South Korea, and India. China’s automotive ecosystem provides large-scale manufacturing advantages, while India is emerging as a cost-efficient production hub. More than 60% of new vehicle manufacturing capacity additions in the region incorporate advanced automation and lightweight component systems. Companies are expanding production facilities, forming OEM partnerships, and investing in smart molding technologies to support rising domestic and export demand.

China Market Outlook: China represents the largest country market due to its unmatched vehicle production scale and EV manufacturing leadership. The country produces more than 30 million vehicles annually and has a rapidly expanding ecosystem for polymer-based automotive components. Suppliers are increasing investments in automated production lines, recycled materials, and integrated bumper technologies to support domestic EV manufacturers and global export programs.

South America is developing as a strategic automotive production region, supported by Brazil’s manufacturing base and increasing demand for efficient vehicle components. The region contributes approximately 8% of global automotive component demand, with passenger vehicle production concentrated in Brazil and Argentina. Supply-chain localization and regional assembly investments are encouraging suppliers to expand domestic manufacturing capabilities. More than 40% of automotive production activity in the region is concentrated around Brazil’s industrial corridors. Companies are improving operational efficiency through localized sourcing, partnerships with OEMs, and upgraded molding technologies, although infrastructure limitations and import dependency continue influencing production strategies.

Brazil Market Outlook: Brazil leads the South American automotive OE bumper cover landscape due to its established vehicle manufacturing sector and supplier network. The country produces over 2 million vehicles annually and is increasing adoption of locally manufactured exterior components. Automotive companies are strengthening domestic partnerships and expanding production capabilities to reduce import dependence and improve supply reliability.

The Middle East & Africa market is gaining importance through automotive industrial diversification, infrastructure development, and increasing vehicle assembly activity. The region accounts for a smaller share of global demand but is attracting investments in localized manufacturing and mobility transformation programs. Countries such as Saudi Arabia, South Africa, and Morocco are strengthening automotive ecosystems through industrial partnerships and vehicle production initiatives. Regional suppliers are adopting modern manufacturing technologies, with automation investments improving production efficiency by nearly 20% in selected facilities. Companies are focusing on localized component production, strategic alliances, and supply-chain development to reduce import reliance and support long-term automotive growth.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a significant automotive investment destination through industrial diversification programs and new vehicle manufacturing initiatives. The country is developing automotive infrastructure, attracting international partnerships, and supporting EV-related investments. Automotive suppliers are positioning production capabilities near emerging assembly projects to capture future demand for advanced exterior components and lightweight vehicle systems.

Global leaders such as Magna International, OPmobility, and Samvardhana Motherson compete with regional suppliers including Flex-N-Gate and Hyundai Mobis, while OEM-linked manufacturers compete against cost-focused component producers. The top five players collectively account for approximately 35–40% of market share, creating a moderately consolidated structure. Competition is driven by lightweight material expertise, production scalability, customization capability, and supply reliability, with automated manufacturing improving efficiency by 15–25%. Leading companies are expanding facilities, forming EV partnerships, and integrating recycling technologies to secure OEM contracts. Cost leaders compete through localized production, while technology innovators focus on smart bumper systems and sensor integration. The market is shifting toward advanced materials and supply-chain localization as EV platforms reshape procurement strategies. High tooling investment and OEM qualification requirements create entry barriers. Winning requires combining material innovation, manufacturing speed, and long-term OEM collaboration.

OPmobility SE

Samvardhana Motherson International Limited

Flex-N-Gate Corporation

Hyundai Mobis Co., Ltd.

Toyota Industries Corporation

Plastic Components and Modules Automotive Inc.

Tong Yang Industry Co., Ltd.

SMP Deutschland GmbH

Jiangnan Mould & Plastic Technology Co., Ltd.

Toyoda Gosei Co., Ltd.

Ningbo Huaxiang Electronic Co., Ltd.

Advanced injection molding, lightweight polymers, and automated production systems are reshaping bumper cover manufacturing. AI-based inspection platforms are reducing defect detection time by 25–35%, while robotic molding improves production consistency by approximately 20%. Compared with conventional manual inspection processes, smart vision systems deliver faster validation and higher accuracy, giving large suppliers a competitive advantage.

Recycled polymer composites and bio-based materials are becoming increasingly important as automakers target lower lifecycle emissions. More than 40% of new vehicle programs are incorporating sustainable material strategies, encouraging suppliers to develop recyclable bumper solutions. Digital twin technology and predictive analytics are also improving tooling optimization, reducing development cycles by nearly 15%.

From 2026 to 2028, sensor-integrated bumper systems, connected safety components, and modular EV-focused designs will influence supplier competitiveness. Companies investing in automated factories, advanced material research, and OEM technology partnerships will gain stronger positioning. Technology leaders benefit through premium contracts, while cost-focused suppliers must accelerate modernization to maintain relevance in evolving automotive supply networks.

June 2026 OPmobility secured two contracts from Leapmotor International to supply front and rear bumpers and tailgates for European passenger vehicles, with production planned from 2027 at its Spain facilities. The agreement strengthens OPmobility’s global exterior systems footprint and supports Chinese OEM international expansion. Source: www.opmobility.com

May 2026 OPmobility received a major Stellantis contract for its One4you integrated rear module combining rear bumper, thermoplastic tailgate, and lighting technologies for an electric SUV platform. The solution delivers a 20% reduction in CO₂ emissions compared with steel alternatives, strengthening lightweight vehicle component adoption. Source: www.opmobility.com

May 2026 Magna International received five General Motors Supplier of the Year awards, including recognition in exterior moldings, highlighting manufacturing excellence and supplier performance across global vehicle programs. The recognition reinforces Magna’s competitive position in advanced exterior systems and OEM collaboration. Source: www.magna.com

November 2025 OPmobility and Yanfeng strengthened their YFPO joint venture in China by expanding exterior product capabilities, including bumpers, tailgates, modules, and integrated lighting solutions. The partnership enhances product portfolio depth and supports faster development for Chinese automotive manufacturers.

The Automotive OE Bumper Cover Market Report covers detailed segmentation by type, application, and end-user, including injection molded systems, composite materials, passenger vehicles, commercial vehicles, automotive OEMs, and component suppliers. The report evaluates market dynamics across North America, Europe, Asia-Pacific, South America, and Middle East & Africa with emphasis on manufacturing hubs, technology adoption, and supplier strategies.

The study analyzes advanced materials, automation, AI-based manufacturing, sustainable polymers, EV platform integration, and smart bumper technologies shaping industry transformation. Covering leading companies, competitive positioning, regional opportunities, and emerging application areas, the report supports investment decisions, expansion planning, partnership strategies, and long-term positioning between 2026 and 2033. It highlights evolving procurement models, supply-chain localization, and innovation priorities influencing future automotive component development.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,541.0 Million |

| Market Revenue (2033) | USD 11,083.7 Million |

| CAGR (2026–2033) | 11.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Magna International Inc.; OPmobility SE; Samvardhana Motherson International Limited; Flex-N-Gate Corporation; Hyundai Mobis Co., Ltd.; Toyota Industries Corporation; Plastic Components and Modules Automotive Inc.; Tong Yang Industry Co., Ltd.; SMP Deutschland GmbH; Jiangnan Mould & Plastic Technology Co., Ltd.; Toyoda Gosei Co., Ltd.; Ningbo Huaxiang Electronic Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |