Reports

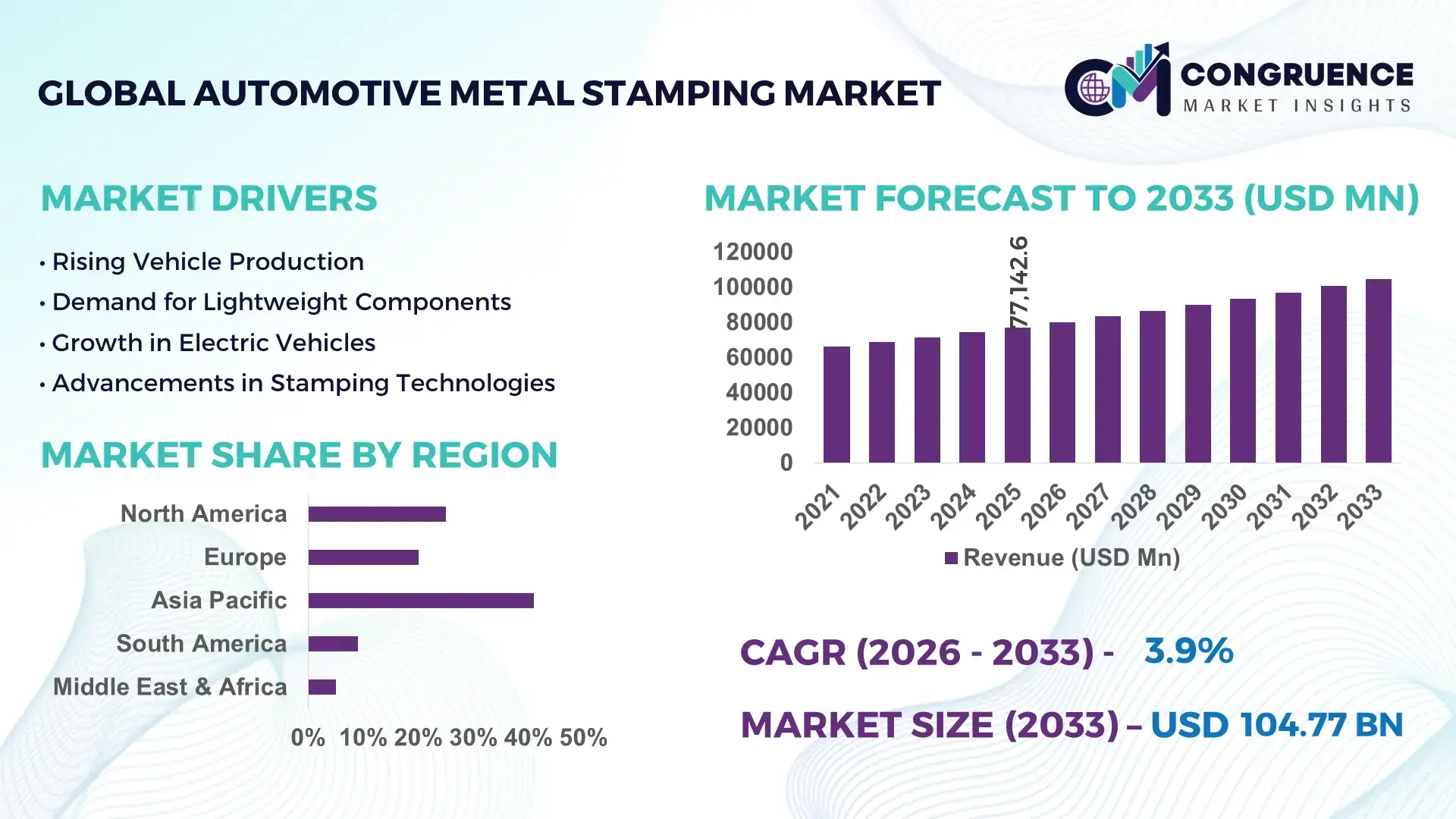

The Global Automotive Metal Stamping Market was valued at USD 77142.57 Million in 2025 and is anticipated to reach a value of USD 104765.54 Million by 2033 expanding at a CAGR of 3.9% between 2026 and 2033. Growth is being driven by rising deployment of lightweight stamped aluminum body structures, giga-press integrated vehicle platforms, and high-volume EV component production across North America, Europe, and Asia-Pacific automotive manufacturing hubs.

China dominates the global automotive metal stamping market with over 34% manufacturing share, supported by more than 26 million annual vehicle production units and large-scale investments exceeding USD 12 billion in automated press line upgrades between 2023 and 2026. Advanced servo stamping adoption in Chinese EV factories has improved production efficiency by nearly 18%, particularly across battery enclosure and chassis applications. In comparison, Germany maintains stronger precision stamping penetration in premium automotive segments, with over 62% of luxury vehicle body components produced using high-tensile steel forming technologies. Ongoing tariff realignments and supply-chain diversification after Red Sea shipping disruptions accelerated regional sourcing strategies among OEMs and Tier-1 suppliers during 2025–2026.

Automotive manufacturers are prioritizing localized high-speed stamping capacity, advanced die automation, and lightweight material integration to secure production resilience and improve cost efficiency in next-generation vehicle programs.

Market Size & Growth: USD 77142.57 Million in 2025 reaching USD 104765.54 Million by 2033, driven by 21% growth in EV structural stamping demand and automated press-line expansion.

Top Growth Drivers: EV platform production up 24%, lightweight aluminum usage increased 19%, and robotic stamping automation adoption crossed 31% globally.

Short-Term Forecast: By 2027, automated die-change systems will reduce production downtime by 16% while improving stamping throughput efficiency by 13%.

Emerging Technologies: AI-driven defect inspection, servo press systems, and digital twin-enabled tooling reduced material waste by nearly 14% in advanced automotive plants.

Regional Leaders: Asia-Pacific exceeds USD 42 billion with EV-focused expansion, Europe surpasses USD 27 billion through lightweight steel adoption, and North America crosses USD 21 billion via localized sourcing strategies.

Consumer/End-User Trends: More than 38% of automakers increased procurement of ultra-high-strength steel stamped components for crash-resistant vehicle architectures.

Pilot/Case Example: In 2025, a multi-plant automated stamping deployment improved production cycle speed by 17% and lowered scrap generation by 11%.

Competitive Landscape: Top manufacturers collectively control nearly 36% market share, with leading participation from Gestamp, Magna, Martinrea, Tower International, and Shiloh Industries.

Regulatory & ESG Impact: Carbon-reduction mandates pushed recycled metal utilization above 28%, while energy-efficient press systems lowered plant electricity consumption by 12%.

Investment & Funding: Global investments exceeded USD 9.4 billion between 2024 and 2026, led by OEM partnerships, smart factory upgrades, and regional expansion programs.

Innovation & Future Outlook: Integrated giga-stamping platforms and hot-forming technologies improved structural rigidity by 20%, strengthening next-generation EV manufacturing competitiveness.

Automotive OEMs are increasingly shifting from multi-supplier stamping procurement toward long-term integrated tooling partnerships to reduce die maintenance delays and improve platform synchronization. Tier-1 suppliers now prioritize modular stamping cells capable of switching between steel and aluminum production within hours, supporting mixed-vehicle manufacturing strategies and reducing idle factory utilization losses.

Automotive metal stamping has become strategically critical as vehicle manufacturers accelerate platform consolidation, localized sourcing, and lightweight component integration across EV and hybrid production lines. More than 41% of global OEM procurement contracts signed during 2025 prioritized regional stamping suppliers to reduce logistics exposure and shorten assembly lead times. Regulatory pressure on vehicle emissions and growing adoption of aluminum-intensive architectures are reshaping investment priorities in China, Mexico, and Germany, while digital press monitoring systems are improving uptime consistency across high-volume automotive plants.

Advanced servo stamping systems now deliver nearly 22% lower energy consumption and 17% faster cycle times compared to traditional mechanical presses, enabling manufacturers to improve throughput without proportional labor expansion. China leads in scale with large-format EV chassis stamping deployments, while Germany focuses on precision hot-forming technologies for premium automotive structures. In the United States, Tier-1 suppliers are integrating AI-enabled die monitoring to reduce unplanned maintenance events by 14%. Over the next two to three years, automated tool-change adoption is expected to cross 35% across newly commissioned automotive stamping facilities.

Automotive suppliers are expanding multi-material stamping capabilities through partnerships with robotics firms and steel producers to secure long-term OEM contracts. A growing number of manufacturers are deploying flexible stamping cells capable of switching between aluminum and ultra-high-strength steel within a single production cycle, reducing idle capacity and supporting mixed-vehicle assembly strategies. Companies that scale intelligent stamping infrastructure and localized tooling ecosystems will secure stronger pricing leverage, operational resilience, and long-term positioning in next-generation vehicle manufacturing.

Automotive manufacturers are accelerating adoption of lightweight stamped components to improve vehicle efficiency, battery range, and crash performance across EV and hybrid platforms. High-strength steel usage in vehicle structures increased by 27% between 2023 and 2026, while aluminum stamping demand rose nearly 19% in battery enclosure production. China and South Korea expanded giga-press and automated stamping investments following tighter vehicle emission standards and rising EV exports. This transition is pushing suppliers toward servo-driven press systems and advanced die engineering capable of reducing material waste by 12%. In response, major stamping companies are expanding localized production facilities near OEM assembly hubs and entering strategic tooling partnerships to secure long-term contracts and reduce logistics dependency across global automotive supply chains.

Automotive metal stamping manufacturers continue facing margin pressure from fluctuating steel and aluminum prices, with industrial-grade aluminum costs rising over 14% during peak supply disruptions in 2025. Dependence on imported flat steel and specialty alloys has increased procurement uncertainty for manufacturers in India and Eastern Europe, particularly after Red Sea shipping disruptions extended lead times by nearly 18%. These cost swings directly affect tooling utilization, production scheduling, and contract profitability for Tier-1 suppliers operating under fixed-price OEM agreements. Companies are responding through long-term material contracts, localized supplier diversification, and recycled metal integration programs. Several automotive stampers are also shifting toward digital inventory forecasting systems to improve purchasing precision and reduce exposure to short-cycle commodity volatility.

The integration of AI-driven quality inspection, digital twins, and robotic material handling is creating new operational opportunities across automotive metal stamping facilities. Automated defect detection systems have reduced inspection time by nearly 31%, while predictive maintenance platforms lowered unplanned press downtime by 16% in advanced manufacturing plants. Japan and Germany are leading deployment of flexible stamping cells capable of switching between multiple vehicle platforms without extended tooling recalibration. Governments supporting industrial automation and localized EV manufacturing are accelerating smart factory investments through tax incentives and infrastructure modernization programs. Automotive suppliers are increasingly investing in modular press lines and collaborative robotics partnerships to support mixed-material production, faster tooling changeovers, and lower per-unit manufacturing costs in high-volume assembly operations.

Automotive metal stamping companies face increasing execution complexity as multi-material vehicle platforms require specialized tooling, precision calibration, and digitally connected production systems. More than 32% of manufacturers report skilled labor shortages in die engineering, robotic maintenance, and automated press programming, particularly across North America and Southeast Asia. Simultaneously, processing ultra-high-strength steel and aluminum within shared production environments increases tooling wear rates by nearly 15%, raising maintenance frequency and operational costs. Germany and the United States are experiencing pressure to modernize aging stamping infrastructure while maintaining production continuity for legacy vehicle programs. To sustain competitiveness, companies must invest in workforce reskilling, AI-assisted process optimization, and next-generation tooling technologies capable of supporting high-mix, high-precision automotive manufacturing requirements.

AI-Driven Press Optimization Automotive manufacturers are deploying AI-enabled stamping analytics to improve die lifespan, reduce scrap rates, and stabilize production output. Smart monitoring systems lowered unplanned downtime by 15% and improved defect detection accuracy by 28% across high-volume facilities in Germany and Japan. Labor shortages and rising maintenance costs accelerated adoption of predictive press management platforms. Companies are restructuring workflows through cloud-based production monitoring and integrating sensor-equipped tooling systems to improve operational continuity and reduce manual inspection dependency.

Localized Multi-Material Production OEMs are increasing localized stamping operations to reduce logistics exposure and support mixed-material vehicle platforms. More than 37% of newly commissioned automotive stamping lines in 2025 were configured for both aluminum and ultra-high-strength steel processing. Mexico and India expanded localized component manufacturing after supply-chain disruptions increased imported material lead times by 18%. Automotive suppliers are responding through regional tooling partnerships, modular production cells, and flexible die systems capable of supporting multiple vehicle architectures within a single manufacturing environment.

Hot Stamping Capacity Expansion Demand for crash-resistant lightweight vehicle structures pushed hot stamping deployment higher across EV and premium vehicle manufacturing. Hot-formed component utilization increased by 21% in structural assemblies, while energy-efficient furnace systems reduced thermal processing costs by nearly 11%. South Korean and Chinese manufacturers accelerated investment in automated hot-forming lines to support battery protection requirements and stricter safety regulations. Companies are scaling integrated press-hardening operations to secure long-term OEM supply contracts and improve high-strength component consistency.

Digital Tooling Lifecycle Management Automotive stampers are shifting toward digitally connected tooling ecosystems to reduce maintenance delays and improve production scheduling precision. Real-time die tracking platforms shortened tooling setup time by 19% and improved asset utilization rates by 14% in large-scale North American facilities. Rising complexity in EV chassis platforms triggered stronger investment in digital twin-assisted die engineering. Companies are partnering with industrial software providers to standardize tooling databases, improve simulation accuracy, and reduce production interruptions linked to manual tooling calibration processes.

Progressive Die Stamping dominates the automotive metal stamping market due to its high-speed production capability, lower per-unit manufacturing cost, and compatibility with automated assembly systems. More than 44% of mass-produced automotive structural and body components now rely on progressive die operations because of their ability to support continuous multi-stage forming with minimal manual intervention. Blanking remains critical for large-scale sheet metal preparation, particularly across chassis and body panel manufacturing, while Bending continues gaining relevance in lightweight structural integration. Progressive Die Stamping also benefits from rising EV platform standardization, where manufacturers require consistent component precision across large production runs. Coining and Embossing maintain strategic importance in precision detailing, branding structures, and reinforcement applications, especially in premium vehicle segments. Companies are investing in servo-enabled progressive tooling systems and automated die monitoring platforms to improve throughput efficiency by nearly 16% while reducing tooling downtime across large automotive production facilities.

Structural Parts represent the leading application segment due to increasing demand for lightweight crash-resistant vehicle platforms and battery-protection architectures. More than 39% of newly developed EV platforms in 2025 integrated advanced stamped structural assemblies using ultra-high-strength steel and aluminum alloys. Body Panels continue holding strong production volumes because of large-scale exterior manufacturing requirements, while Chassis Components maintain operational importance in suspension and underbody reinforcement systems. Structural Parts are also the fastest-growing application segment as automakers accelerate integration of modular EV platforms requiring precision-formed load-bearing components. Engine Parts and Transmission Components remain mature segments but are experiencing gradual production optimization as electrified powertrains reduce traditional mechanical complexity. Interior Components are increasingly incorporating thinner stamped assemblies to improve cabin space efficiency and reduce overall vehicle weight. Automotive manufacturers are expanding robotic welding integration and automated hot-stamping deployment to improve dimensional consistency and reduce production cycle variability.

Passenger Vehicle Manufacturers remain the dominant end-user group due to their large-scale production volumes, platform diversification, and continuous body structure demand across compact, sedan, and SUV segments. However, Electric Vehicle Manufacturers represent the fastest-growing buyer category as battery enclosure systems, lightweight chassis structures, and reinforced safety assemblies require advanced precision stamping capabilities. More than 34% of newly installed automated stamping lines during 2025 were dedicated to EV-focused component production. Automotive Component Suppliers are strengthening long-term procurement agreements with OEMs to secure localized sourcing advantages and reduce inventory risk. Commercial Vehicle Manufacturers continue investing in high-durability stamped chassis systems, while Heavy Vehicle Manufacturers prioritize thicker high-strength steel processing for structural reinforcement applications. Aftermarket Parts Providers maintain stable demand through replacement body panels and structural repair components. Companies are increasingly targeting EV manufacturers through customized tooling ecosystems, integrated robotics partnerships, and flexible production contracts designed to support mixed-platform vehicle manufacturing requirements.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.6% between 2026 and 2033.

Localized EV Supply Chains Reshaping Production Networks

North America is strengthening its automotive metal stamping ecosystem through localized EV manufacturing, automated production upgrades, and nearshoring strategies across the United States and Mexico. The region contributes over 24% of global automotive stamping output, supported by expanding battery vehicle assembly programs and increasing demand for lightweight structural components. More than 33% of newly installed servo press systems in 2025 were deployed across North American automotive plants to improve production precision and reduce downtime. OEMs are accelerating supplier partnerships for localized die manufacturing and robotic material handling integration following logistics disruptions and rising import dependency concerns. Mexico continues expanding as a key cross-border manufacturing hub due to lower operational costs and strong OEM assembly concentration.

United States Market Outlook: The United States leads North American automotive metal stamping through advanced manufacturing infrastructure, large-scale EV investments, and high automation penetration across automotive assembly networks. More than 41% of automotive stamping facilities in the country integrated AI-assisted press monitoring systems by 2026 to reduce defect rates and improve tooling efficiency. Domestic suppliers are expanding high-strength steel and aluminum forming capabilities near EV battery manufacturing corridors in Michigan, Tennessee, and Texas to strengthen localized production resilience.

High-Strength Lightweight Engineering Driving Modernization

Europe maintains strong positioning in advanced automotive metal stamping through premium vehicle manufacturing, sustainability-driven material innovation, and precision hot-forming technologies. The region accounts for nearly 27% of global deployment concentration, supported by strict vehicle emission regulations and increasing adoption of ultra-high-strength steel structures. Germany, France, and Italy continue modernizing stamping infrastructure with energy-efficient press systems and digitally connected tooling operations. In 2025, several European automotive suppliers expanded hot-stamping capacity by over 18% to support EV structural reinforcement requirements. Automotive manufacturers are also prioritizing recycled metal integration and closed-loop production systems to improve material utilization efficiency while meeting tightening industrial sustainability standards.

Germany Market Outlook: Germany remains the strategic center of Europe’s automotive metal stamping industry due to its premium automotive production scale, engineering expertise, and advanced automation deployment. More than 58% of German automotive body structures now utilize hot-formed high-strength stamped components to improve crash performance and reduce vehicle weight. Domestic suppliers are investing heavily in AI-enabled quality inspection and digital twin-assisted tooling simulation to support high-precision EV and luxury vehicle manufacturing operations.

Mass Manufacturing Scale Accelerating EV Integration

Asia-Pacific dominates the automotive metal stamping market through large-scale vehicle production, vertically integrated supply chains, and aggressive EV manufacturing expansion. The region contributes approximately 46% of global automotive stamping activity, with China, Japan, South Korea, and India serving as major industrial hubs. More than 39% of global EV-related stamping line installations during 2025 occurred in Asia-Pacific manufacturing facilities. Chinese and South Korean suppliers are expanding giga-press operations and automated multi-material processing systems to improve chassis production efficiency and battery enclosure integration. India is also strengthening domestic stamping infrastructure through industrial corridor investments and localized automotive component manufacturing incentives designed to reduce import dependency and improve export competitiveness.

China Market Outlook: China leads the global automotive metal stamping market through unmatched vehicle production capacity, advanced EV ecosystem integration, and aggressive manufacturing automation. The country produced over 26 million vehicles annually while expanding high-speed servo press deployment across EV structural component facilities. Chinese manufacturers are strengthening integrated stamping and battery platform production capabilities through smart factory investments, enabling faster production cycles and improved supply-chain coordination for domestic and export-oriented automotive programs.

Industrial Localization Supporting Component Demand

South America is gradually strengthening its automotive metal stamping sector through localized vehicle assembly expansion and rising demand for cost-efficient structural components. Brazil and Argentina remain the primary automotive manufacturing centers, collectively contributing over 70% of regional automotive production activity. Manufacturers are investing in upgraded press lines and flexible tooling systems to support mixed-model vehicle assembly and improve operational efficiency. In 2025, multiple automotive suppliers in Brazil expanded localized chassis and body panel production capacity by nearly 12% to reduce imported component dependency. However, inconsistent logistics infrastructure and currency volatility continue limiting large-scale automation deployment across smaller manufacturing clusters.

Brazil Market Outlook: Brazil leads South America’s automotive metal stamping industry through established automotive assembly infrastructure, domestic supplier networks, and expanding localization initiatives. More than 45% of Brazil’s automotive component manufacturers increased investment in automated sheet metal forming systems during 2025 to improve productivity and reduce scrap generation. Domestic suppliers are prioritizing flexible stamping operations capable of supporting both combustion-engine and hybrid vehicle assembly requirements across regional production programs.

Industrial Diversification Expanding Manufacturing Investments

The Middle East & Africa automotive metal stamping market is evolving through industrial diversification programs, automotive assembly localization, and infrastructure modernization projects. The region currently represents a smaller share of global deployment but is attracting growing investment in vehicle component manufacturing hubs, particularly in Saudi Arabia, the United Arab Emirates, and South Africa. Governments are supporting industrial expansion through economic diversification initiatives and automotive manufacturing incentives. In 2025, several regional industrial zones introduced automated fabrication and metal-forming facilities designed to improve domestic vehicle component production capacity by over 10%. Limited supplier ecosystems and high dependence on imported tooling systems continue affecting scalability across certain African markets.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a strategic automotive metal stamping destination through industrial diversification programs and large-scale automotive manufacturing investments. The country is strengthening localized component production through integrated industrial zones connected to EV and commercial vehicle assembly initiatives. More than 30% of newly approved automotive manufacturing projects in 2025 included advanced metal-forming and stamping infrastructure development, reflecting the country’s broader push toward domestic industrial capability expansion and reduced import reliance.

Global leaders including Gestamp, Magna International, Martinrea, Tower International, and Shiloh Industries compete aggressively against regional precision stampers and vertically integrated OEM suppliers. The top five players collectively control nearly 36% of global market activity, with competition centered on automation capability, tooling speed, lightweight material expertise, and localized supply-chain integration. European manufacturers dominate hot-forming technologies, while Chinese and Mexican suppliers compete through cost-efficient high-volume production. Advanced servo press deployment improved production efficiency by 18% in leading facilities, while AI-enabled quality monitoring reduced defect rates by nearly 14%, intensifying the technology gap between premium and mid-tier suppliers. Companies are expanding through EV-focused partnerships, regional stamping hubs, and integrated die engineering operations to secure long-term OEM contracts. Rising tooling costs, skilled labor shortages, and multi-material processing complexity are increasing entry barriers. Winning requires scalable automation, localized manufacturing resilience, precision engineering expertise, and deep integration with next-generation vehicle platform ecosystems globally.

Gestamp

Magna International

Martinrea International

Tower International

Shiloh Industries

Aisin Corporation

Benteler International

Hirotec Corporation

Thyssenkrupp Automotive Body Solutions

Cosma International

Voestalpine Automotive Components

CIE Automotive

Dura Automotive Systems

JBM Group

Advanced servo press systems, AI-enabled quality monitoring, and robotic material handling are reshaping automotive metal stamping operations. Servo-driven stamping lines improve production precision by nearly 18% while lowering energy consumption by 15% compared to conventional mechanical presses. More than 36% of newly commissioned automotive stamping facilities integrated predictive maintenance systems during 2025–2026 to reduce unplanned downtime and stabilize tooling performance. Automotive OEMs benefit from faster production cycles, lower scrap generation, and improved consistency across EV structural component manufacturing.

Hot stamping and giga-stamping technologies are accelerating adoption across lightweight vehicle architecture production. Compared with traditional multi-part welding methods, giga-stamped assemblies reduce component count by over 30% and shorten assembly workflows by nearly 20%. China, Germany, and South Korea are leading deployment of ultra-high-strength steel forming systems integrated with digital twin-assisted die engineering. Premium automotive manufacturers gain competitive advantage through stronger crash performance, reduced vehicle mass, and faster platform scalability for EV production.

Between 2026 and 2028, AI-assisted tooling simulation, modular flexible stamping cells, and real-time digital production analytics will become operational priorities. Automated defect detection systems already improve inspection accuracy by approximately 28%, while cloud-connected tooling platforms reduce setup delays by 16%. Suppliers investing early in integrated smart stamping ecosystems will secure stronger OEM partnerships, higher localization relevance, and greater production resilience against supply-chain disruption.

January 2025 – Gestamp introduced GES-GIGASTAMPING® structural components at Bharat Mobility Global Expo, integrating multiple body parts into single assemblies while reducing production and assembly time significantly for lightweight EV manufacturing efficiency.

June 2024 – Martinrea International invested nearly USD 35 million to expand its Ontario facility with a 3000-ton stamping press, increasing capability for larger battery enclosures and complex chassis structures. Source: martinrea.com

May 2025 – Gestamp showcased G-Weld Overlap technology in Japan, delivering welding speeds up to five times faster than conventional spot welding while lowering assembly complexity for advanced automotive structures. Source: gestamp.com

October 2025 – Gestamp and Hydnum Steel signed a clean-steel partnership using renewable energy and green hydrogen processing, strengthening circular automotive supply chains and accelerating ultra-low CO₂ component manufacturing deployment. Source: gestamp.com

The Automotive Metal Stamping Market report delivers comprehensive analysis across major production technologies, applications, end-user categories, and regional manufacturing ecosystems shaping automotive component supply chains between 2026 and 2033. The report evaluates operational trends across Blanking, Embossing, Bending, Coining, and Progressive Die Stamping while assessing demand concentration in body panels, structural parts, chassis components, transmission systems, and interior assemblies. More than 45% of the assessment focuses on EV-driven manufacturing transitions, lightweight material integration, and automated press-line modernization strategies.

The study covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa with detailed country-level insights on manufacturing capacity, localization trends, infrastructure investment, and industrial deployment priorities. It analyzes adoption patterns for AI-enabled quality inspection, hot stamping, giga-stamping, and digital tooling systems while benchmarking strategic initiatives from leading automotive stamping suppliers and OEM-linked manufacturers. The report supports investment planning, supplier positioning, expansion strategy, sourcing optimization, and technology adoption decisions across evolving automotive production networks.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 77142.57 Million |

|

Market Revenue in 2033 |

USD 104765.54 Million |

|

CAGR (2026 - 2033) |

3.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Gestamp, Magna International, Martinrea International, Tower International, Shiloh Industries, Aisin Corporation, Benteler International, Hirotec Corporation, Thyssenkrupp Automotive Body Solutions, Cosma International, Voestalpine Automotive Components, CIE Automotive, Dura Automotive Systems, JBM Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |