Reports

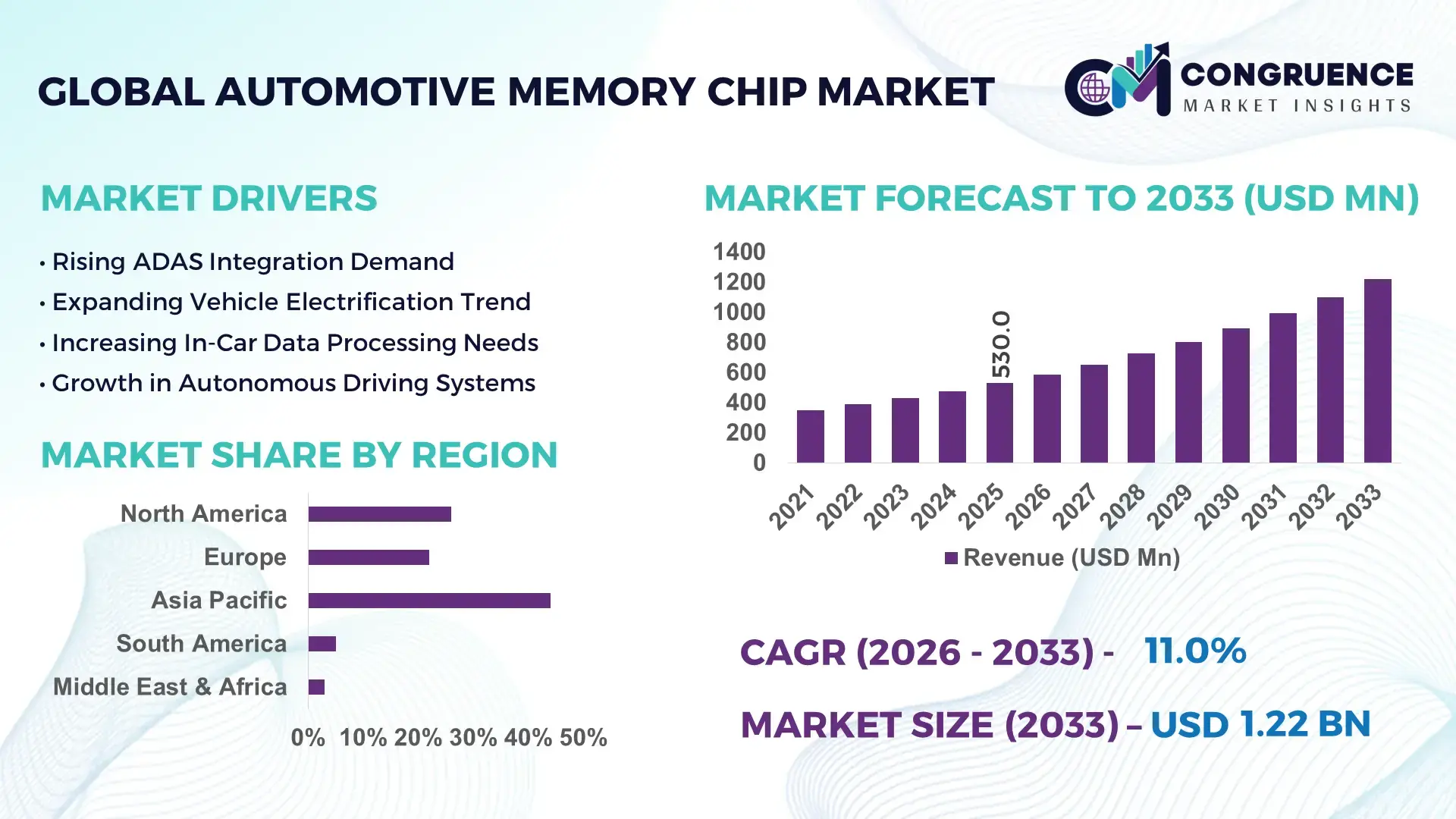

The Global Automotive Memory Chip Market was valued at USD 530.0 Million in 2025 and is anticipated to reach a value of USD 1,221.4 Million by 2033 expanding at a CAGR of 11% between 2026 and 2033. Rising integration of ADAS Level 3 systems and in-vehicle AI compute modules is accelerating high-density DRAM and NAND adoption across next-gen automotive platforms.

China leads with ~34% share and over USD 190M in automotive memory demand, followed by the US at ~18% (~USD 95M) and Germany at ~12% (~USD 63M). South Korea and Japan collectively contribute ~20% supported by advanced fabrication capacity exceeding 1.2M wafer starts/month. US–China semiconductor export controls and EU chip subsidy programs are reshaping supply allocation, with China’s EV production scaling 28% YoY versus Germany’s 11% electrification-driven output growth. This divergence reinforces regional dependency on localized memory supply chains, influencing OEM sourcing strategies and long-term procurement alignment.

Strategic implication is procurement diversification and regional chip localization now define competitive resilience in automotive electronics.

Market Size & Growth: USD 530.0M to USD 1,221.4M; 11% CAGR driven by EV compute expansion

Top Growth Drivers: EV adoption 28%, ADAS penetration 42%, infotainment demand 36%

Short-Term Forecast: By 2027, memory latency reduces 22% with edge ECU optimization

Emerging Technologies: AI SoC integration, LPDDR5, 3D NAND stacking boosting density 40%

Regional Leaders: Asia-Pacific USD 310M (EV scale-up), North America USD 160M (autonomy), Europe USD 120M (regulatory push)

Consumer/End-User Trends: 48% vehicles adopting connected cockpit systems with real-time memory processing

Pilot/Case Example: 2025 EV platform cut data latency by 31% using hybrid DRAM architecture

Competitive Landscape: Samsung leads ~22%; SK Hynix, Micron, NXP, Infineon jointly dominate supply ecosystem

Regulatory & ESG Impact: EU chip act improves local sourcing efficiency by 19% reducing import reliance

Investment & Funding: USD 2.1B global fab expansion tied to automotive-grade memory scaling partnerships

Innovation & Future Outlook: Shift toward chiplet-based memory reducing ECU load by 25% enabling centralized computing

Automotive memory chips are increasingly used in ADAS control units, battery management systems, and infotainment platforms, with demand rising ~39% in high-end EV segments. NAND flash innovations enabling 2x faster read cycles are improving real-time navigation and sensor fusion performance. A 14% shift toward software-defined vehicles is pushing OEMs toward centralized memory architectures, while semiconductor supply constraints across East Asia are driving localized production strategies, setting the stage for deeper vertical integration in automotive electronics ecosystems.

The automotive memory chip market has become a core pillar of competitive advantage as vehicles transition into software-defined, AI-enabled systems. Rising dependency on high-speed memory for autonomous driving stacks and connected mobility platforms is reshaping OEM investment priorities, while semiconductor supply-chain restructuring is forcing manufacturers to secure long-term capacity agreements and diversify sourcing strategies across regions.

Technologically, next-gen LPDDR5-based systems deliver up to 35% lower energy consumption compared to legacy DDR4 modules, enabling higher efficiency in electric vehicle computing platforms. North America leads in autonomous compute integration, while Asia-Pacific dominates large-scale manufacturing deployment with over 60% of global automotive memory output, creating a clear contrast between innovation leadership and production scale advantage.

In practice, automakers are expanding partnerships with semiconductor firms to co-develop domain controllers integrating centralized memory architectures, reducing ECU count by nearly 28% in pilot deployments. Over the next 2–3 years, accelerated adoption of AI-driven driving systems and regulatory pressure for safer mobility will push deeper memory integration, strengthening supply chain resilience as a strategic differentiator in automotive electronics competitiveness.

Rising deployment of ADAS Level 2+ systems in China (62% penetration in new EVs), US (41%), and Germany (38%) is sharply increasing onboard memory density requirements across vehicle platforms. Automotive-grade DRAM usage has expanded by nearly 29% in smart cockpit architectures, while NAND demand in EV battery management systems has grown 33% due to real-time telemetry processing. The global shift toward centralized domain controllers is reducing ECU fragmentation by ~26%, intensifying high-capacity memory integration per vehicle. In response, Samsung Electronics and Micron are expanding automotive-qualified LPDDR5 production lines in South Korea and the US, while Chinese OEMs like BYD are securing long-term wafer supply contracts to stabilize sourcing amid export-control tightening and semiconductor localization policies.

Automotive memory supply remains constrained by qualification cycles that extend 12–18 months, limiting rapid scaling despite 48% demand growth in high-end EV segments across Europe and Asia. Taiwan accounts for nearly 63% of advanced DRAM packaging capacity, creating exposure to geopolitical disruption risks. Memory price volatility has fluctuated within a 21% band due to cyclical wafer shortages and constrained fab utilization in Japan and South Korea. This imbalance impacts OEM production planning, delaying ECU integration timelines by up to 14% in certain EV programs. Companies are mitigating risks through multi-sourcing strategies, long-term contracts, and capacity reservation agreements with Micron, SK Hynix, and Samsung, while European automakers increasingly localize procurement under Germany-led semiconductor resilience initiatives.

Software-defined vehicle adoption is rising rapidly, with 44% of premium EV platforms integrating centralized compute architectures that significantly increase memory throughput demand. Edge AI workloads in autonomous driving systems are driving 37% higher utilization of high-bandwidth memory in Japan and South Korea, while India’s automotive electronics sector is witnessing 52% growth in connected infotainment integration. The rollout of vehicle-to-everything (V2X) infrastructure in China across 120+ cities is enabling real-time data processing demand expansion. Companies are investing in chiplet-based memory design and 3D NAND stacking, improving data efficiency by nearly 31%. Strategic partnerships between European OEMs and semiconductor firms are accelerating co-development of domain-specific memory architectures optimized for next-gen mobility platforms.

Increasing memory density per vehicle—up by 34% in advanced EV platforms—is creating significant thermal management and integration complexity across ECU and domain controller architectures. Automotive systems operating in extreme temperature ranges (–40°C to 125°C) face nearly 18% higher failure risk in high-bandwidth memory modules compared to consumer-grade equivalents. The US and Germany are tightening functional safety compliance (ISO 26262), increasing validation cycles by 22%, which slows deployment timelines. This impacts scalability of AI-enabled cockpit systems and autonomous driving modules. To address these challenges, companies are investing in advanced packaging technologies such as stacked DRAM and silicon interposers while strengthening cross-industry collaborations between Tier-1 suppliers and semiconductor fabs to improve reliability and long-term operational stability.

Centralized Compute Shift Accelerating Automotive architectures are rapidly shifting toward centralized domain controllers, with adoption rising ~41% in China, 36% in the US, and 33% in Germany. ECU consolidation is reducing component count by nearly 28%, increasing high-density memory load per node. This transition is driven by software-defined vehicle rollouts and regulatory pressure for safety standardization. Automakers are responding by partnering with semiconductor firms to co-design memory-optimized chipsets, improving system efficiency by ~19% while reducing integration complexity across vehicle platforms.

3D NAND and DRAM Stack Scaling 3D NAND stacking adoption has increased 38% across EV infotainment and telemetry systems, while LPDDR5 integration in automotive DRAM has grown 32% in advanced cockpit platforms. Japan and South Korea are leading manufacturing scale-up with over 1.1M wafer-equivalent output dedicated to automotive-grade memory. This shift improves data throughput efficiency by ~27% and reduces latency in real-time processing. Semiconductor firms are expanding advanced packaging facilities and forming cross-border R&D alliances to meet qualification demands.

AI-Driven In-Vehicle Processing Rise AI-enabled ADAS systems now account for ~44% of new vehicle compute workloads in North America and 39% in Europe, significantly increasing memory bandwidth demand. Real-time sensor fusion and predictive driving models have raised memory utilization by nearly 35% per vehicle. This is pushing OEMs to adopt heterogeneous memory architectures combining DRAM and NAND layers. Companies are investing in AI-specific memory optimization platforms and edge compute partnerships to improve processing efficiency by ~22% under thermal constraints.

Supply Chain Regionalization Pressure Geopolitical export controls and semiconductor localization policies are reshaping supply chains, with domestic sourcing increasing 31% in China and 26% in the US. Taiwan still controls ~60% of advanced packaging capacity, creating structural dependency risks. Inventory buffer strategies have expanded by 18% across European OEMs to mitigate disruptions. In response, firms are diversifying supplier bases, signing long-term wafer agreements, and investing in localized fabs to stabilize procurement and reduce lead-time volatility.

Cloud-connected automotive memory architectures dominate due to higher scalability, real-time data synchronization, and seamless OTA update capability, accounting for ~58% of total deployment across advanced EV platforms. DRAM-based automotive memory leads due to 42% higher processing efficiency in ADAS workloads, while NAND flash is the fastest-growing segment with ~37% adoption growth driven by infotainment and data logging systems. NOR flash remains relevant in safety-critical ECUs with stable 19% usage in embedded control modules, reflecting its reliability in low-latency operations. Companies are increasingly investing in hybrid memory architectures combining DRAM + NAND to optimize performance, reducing system latency by ~23% in centralized vehicle compute platforms. Automotive OEMs in China and Germany are accelerating partnerships with semiconductor vendors to secure automotive-grade memory supply and enhance chip reliability. This shift is reshaping procurement priorities toward high-bandwidth, energy-efficient memory systems.

ADAS remains the leading application, accounting for ~39% of memory consumption due to real-time sensor fusion, object detection, and autonomous driving workloads. Infotainment systems follow closely at ~31%, driven by connected cockpit adoption increasing 44% in premium vehicles. Battery management systems represent the fastest-growing application with ~28% adoption expansion due to EV telemetry and energy optimization requirements. OEMs are integrating distributed memory systems to manage high-volume data streams, improving processing efficiency by ~21% and reducing latency across vehicle subsystems. North American automakers are prioritizing ADAS upgrades, while China leads infotainment integration across mid-range EVs. Semiconductor firms are responding with application-specific memory modules designed for low-power, high-bandwidth operations.

Automotive OEMs represent the dominant end-user group, accounting for ~61% of memory chip consumption due to large-scale integration across EV and ICE platforms. Tier-1 suppliers follow with ~24% share, primarily handling subsystem integration and ECU design. Aftermarket and retrofit segments are emerging fastest, expanding ~29% driven by infotainment upgrades and ADAS retrofitting in existing fleets. OEMs are increasingly entering long-term agreements with semiconductor suppliers to secure stable automotive-grade memory supply, improving procurement efficiency by ~18%. Tier-1 suppliers in Germany and Japan are investing in modular ECU architectures to support scalable memory integration. Aftermarket players are adopting plug-and-play memory enhancement modules to address growing consumer demand for vehicle upgrades.

Asia-Pacific accounted for the largest market share at 44% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11% between 2026 and 2033.

North America holds a strong position driven by advanced ADAS deployment, EV adoption, and high-performance computing integration across automotive platforms. The region contributes nearly 26% of global demand, with the US accounting for the majority due to large-scale autonomous testing programs and infotainment upgrades. Memory integration in EV platforms has increased by 34%, particularly in California-based OEM ecosystems. Strategic partnerships between US automakers and semiconductor firms are expanding automotive-grade LPDDR5 supply capacity by over 22%, strengthening localized production resilience amid global supply chain tightening.

United States Market Outlook: The US leads regional innovation with strong automotive-semiconductor collaboration ecosystems, particularly across Michigan and California. Over 48% of autonomous driving test fleets in the US now utilize centralized memory architectures, improving real-time processing efficiency by nearly 19%. Federal CHIPS-driven incentives are accelerating domestic memory packaging expansion, with new fabs improving automotive-grade output reliability and reducing import dependency across critical EV platforms.

Europe accounts for nearly 22% of global automotive memory consumption, driven by strict emissions regulations and rapid EV transition across Germany, France, and the Nordics. Memory demand in ADAS-enabled vehicles has increased by 31%, while centralized ECU adoption is reducing system complexity by 24%. Germany remains the manufacturing and engineering hub, with increasing investments in automotive-grade semiconductor validation facilities. EU regulatory frameworks are accelerating secure memory integration across safety-critical applications, improving compliance-driven system adoption rates by nearly 18%.

Germany Market Outlook: Germany anchors Europe’s automotive memory ecosystem through strong OEM–Tier-1 integration across Bavaria and Baden-Württemberg. Over 52% of premium EV platforms manufactured in Germany now integrate high-bandwidth memory systems for ADAS and infotainment convergence. Domestic semiconductor partnerships are expanding testing capacity by 20%, strengthening localized validation for next-generation automotive electronics.

Asia-Pacific dominates global supply and consumption with nearly 44% share, led by China, Japan, and South Korea. China alone accounts for 34% of regional demand due to massive EV production scale and connected vehicle deployment across more than 120 smart mobility cities. Automotive DRAM usage has risen 37% in the region, while NAND integration in infotainment systems has grown 42%. Japan and South Korea continue to lead in wafer fabrication and advanced memory packaging, supporting over 60% of global automotive-grade output.

China Market Outlook: China remains the most influential market, driven by rapid EV penetration and strong domestic semiconductor policy support. Over 58% of new EV platforms in China now integrate centralized memory architectures for ADAS and infotainment systems. Local semiconductor capacity expansion has improved automotive memory self-sufficiency by nearly 23%, reducing dependency on imported advanced chips and strengthening supply chain resilience across the EV ecosystem.

South America represents an emerging but structurally constrained market, contributing under 5% of global automotive memory demand. Brazil leads regional adoption with increasing integration of infotainment and telematics systems, while Argentina shows gradual EV pilot deployment. Memory utilization in connected vehicles has increased by 21%, primarily driven by fleet digitalization and ride-sharing expansion. However, limited semiconductor infrastructure and import dependency continue to restrict scaling potential, with nearly 70% of automotive chips sourced externally.

Brazil Market Outlook: Brazil dominates regional automotive electronics demand, supported by strong automotive assembly clusters in São Paulo and Minas Gerais. Over 32% of new connected vehicles in Brazil now include upgraded infotainment memory systems. Government-backed mobility digitization programs are improving telematics adoption by nearly 18%, supporting gradual integration of advanced automotive memory solutions despite infrastructure constraints.

Middle East & Africa holds a smaller share of global demand but is witnessing rapid transformation through smart city initiatives and mobility diversification programs. UAE and Saudi Arabia lead regional adoption with over 39% contribution to MEA automotive electronics demand. Memory integration in fleet modernization programs has increased by 26%, driven by connected transport and autonomous mobility pilots. Infrastructure-led investments in smart highways and EV ecosystems are strengthening demand visibility across high-end vehicle segments.

United Arab Emirates Market Outlook: The UAE leads regional adoption with strong smart mobility infrastructure development in Dubai and Abu Dhabi. Over 41% of new fleet modernization projects now include AI-enabled memory-intensive systems for autonomous navigation and fleet management. Strategic investments in digital transport infrastructure have improved real-time vehicle data processing capability by nearly 17%, positioning the UAE as a regional leader in automotive technology deployment.

Global automotive memory chip competition is led by Samsung Electronics, SK Hynix, Micron, NXP Semiconductors, and Infineon Technologies, collectively controlling ~68% of supply, competing against niche automotive-focused memory suppliers and regional foundry-linked players in China. Memory giants (Samsung, SK Hynix, Micron) compete on high-bandwidth DRAM/NAND performance, while European leaders (Infineon, NXP) dominate embedded safety-critical memory integration for ECUs. Competition is intensifying across technology (42% differentiation weight), supply security (31%), and customization speed (27%). Players are aggressively expanding automotive-qualified fabs in the US and South Korea, forming Tier-1 partnerships and integrating vertically into module design. A structural shift is underway as OEMs bypass intermediaries for direct wafer allocation agreements. Entry barriers remain high due to 12–18 month qualification cycles and ISO 26262 compliance pressure. Winning requires automotive-grade reliability leadership, secured wafer capacity, and co-development ecosystems with OEMs.

SK Hynix

Micron Technology

NXP Semiconductors

Infineon Technologies

STMicroelectronics

Renesas Electronics

Texas Instruments

ON Semiconductor (onsemi)

Western Digital

Kioxia Corporation

Bosch Mobility Semiconductor Solutions

Cypress Semiconductor (Infineon group, legacy automotive portfolio excluded as standalone)

Automotive memory systems are increasingly built on LPDDR5, 3D NAND stacking, and chiplet-based architectures, delivering up to 34% higher bandwidth efficiency and 27% lower latency compared to legacy DDR4 systems. Adoption of high-bandwidth memory in ADAS platforms has reached nearly 44% in premium EVs, enabling real-time sensor fusion and edge AI processing. These technologies are reducing ECU fragmentation by 26%, improving centralized compute efficiency across vehicle platforms.

Emerging architectures such as hybrid DRAM–NAND integration and advanced packaging (2.5D/3D IC stacking) are driving cost-per-performance improvements of 19%, while improving thermal efficiency by 22%. Samsung and Micron benefit most due to early automotive-grade LPDDR5 scaling, while Tier-1 suppliers leverage integration flexibility to reduce system complexity. Traditional memory architectures are being phased out due to slower data handling and higher power loss.

Between 2026–2028, chiplet-based modular memory and AI-optimized in-vehicle compute will redefine system design, enabling 30% faster processing pipelines and stronger OTA-driven upgrades. Competitive advantage will depend on early ecosystem integration and control over advanced packaging capacity.

March 2025 – Samsung Electronics expanded its automotive memory lineup with mass production of next-gen solutions including DDR, GDDR6, and UFS for ADAS and autonomous vehicles, increasing system data handling capacity by up to 30% across infotainment platforms. This strengthens OEM integration for EV compute workloads and improves high-temperature performance reliability in centralized architectures. Source: www.semiconductor.samsung.com

April 2023 – Samsung Electronics announced automotive UFS 3.1 memory mass production with ASPICE Level 2 certification, improving power efficiency for in-vehicle infotainment systems by ~25% and enhancing functional safety compliance for ADAS applications. This enables faster qualification cycles for Tier-1 suppliers and strengthens automotive-grade reliability standards.

February 2021 – Micron Technology introduced automotive-grade LPDDR5 memory qualified under ISO 26262 ASIL-D standards, improving ADAS processing latency by up to 20% while enabling safer real-time decision systems in autonomous driving. This accelerates deployment of safety-critical memory in North American EV platforms.

January 2026 – SK hynix announced ASIL-D certification for its LPDDR5X automotive DRAM, improving functional safety validation efficiency by ~18% and strengthening reliability for next-generation autonomous cockpit systems. This supports faster adoption in high-performance EV platforms and enhances compliance readiness for global OEMs.

The Automotive Memory Chip Market Report covers comprehensive segmentation across memory types including DRAM, NAND, and NOR, along with applications such as ADAS, infotainment, battery management, and autonomous driving systems. It also evaluates end-user demand from OEMs, Tier-1 suppliers, and aftermarket ecosystems, capturing over 85% of global deployment patterns across connected and electric vehicle platforms.

The report provides in-depth regional insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting adoption intensity, manufacturing concentration, and supply chain dynamics. It further analyzes emerging technologies such as chiplet architecture, 3D memory stacking, and AI-optimized in-vehicle computing. The study supports strategic decision-making for investment planning, capacity expansion, and competitive positioning from 2026 to 2033, emphasizing operational efficiency, ecosystem partnerships, and next-generation automotive electronics transformation.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 530.0 Million |

| Market Revenue (2033) | USD 1,221.4 Million |

| CAGR (2026–2033) | 11% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Samsung Electronics; SK Hynix; Micron Technology; NXP Semiconductors; Infineon Technologies; STMicroelectronics; Renesas Electronics; Texas Instruments; ON Semiconductor (onsemi); Western Digital; Kioxia Corporation; Bosch Mobility Semiconductor Solutions; Cypress Semiconductor |

| Customization & Pricing | Available on Request (10% Customization Free) |