Reports

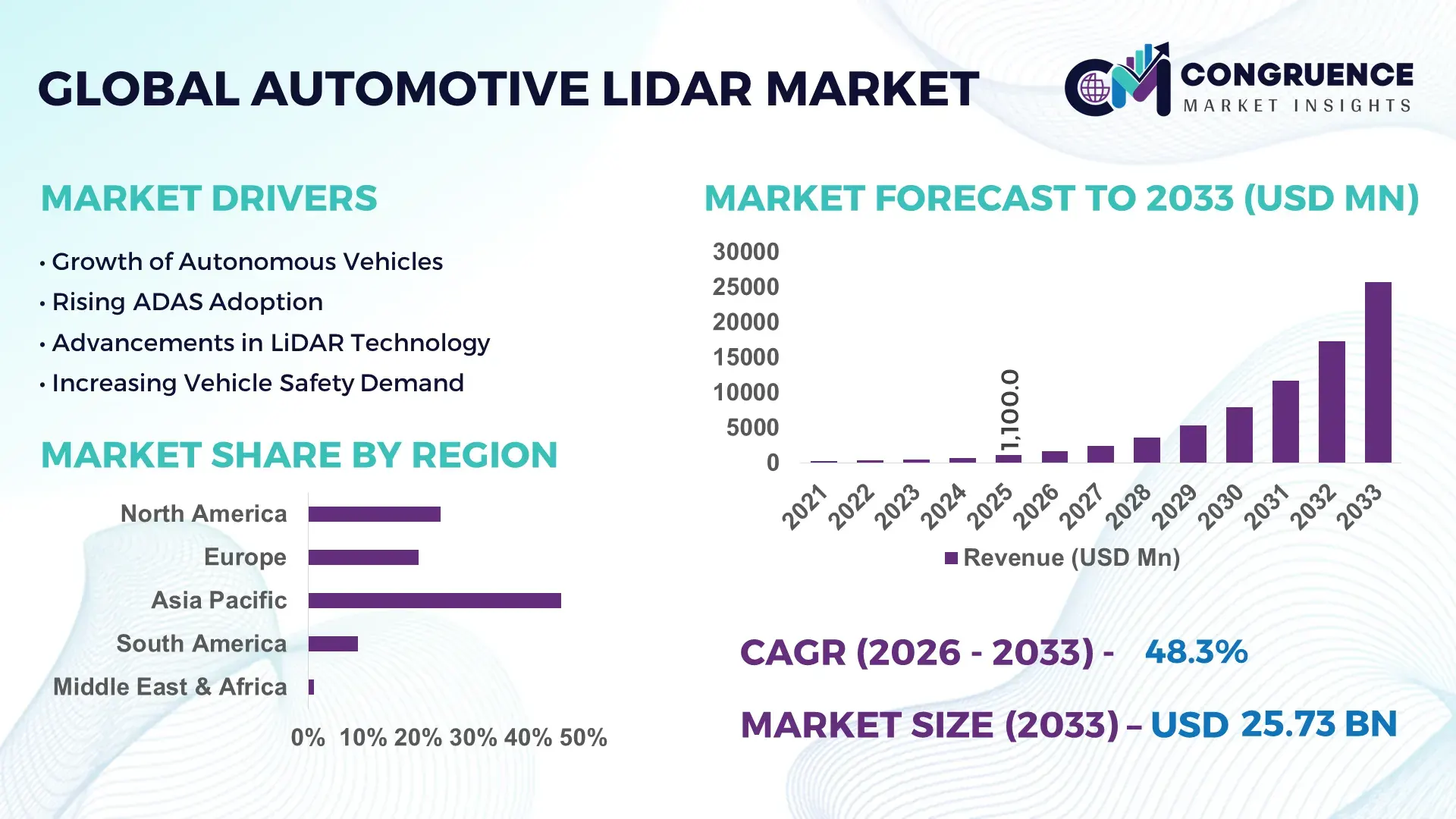

The Global Automotive LiDAR Market was valued at USD 1100 Million in 2025 and is anticipated to reach a value of USD 25734.86 Million by 2033 expanding at a CAGR of 48.3% between 2026 and 2033. Growth is accelerating through Level 3 autonomous vehicle deployment, high-resolution solid-state LiDAR integration in premium EV platforms, and government-backed intelligent mobility infrastructure programs across North America, Europe, and East Asia.

China accounted for nearly 38% of global Automotive LiDAR manufacturing capacity in 2026, supported by over USD 4 billion in autonomous mobility investments and rapid EV integration across urban transport fleets. The United States maintained stronger software-led adoption, with advanced driver-assistance penetration exceeding 31% in premium vehicle segments, while Germany led European automotive-grade sensor validation through industrial automation and semiconductor integration programs. Export restrictions on advanced semiconductor technologies reshaped sourcing strategies, increasing regional supply-chain localization by 22% across automotive sensor manufacturing hubs.

Automotive OEMs and Tier-1 suppliers are prioritizing vertically integrated LiDAR ecosystems, making long-term semiconductor partnerships and regional manufacturing resilience critical competitive differentiators through 2030.

Market Size & Growth: USD 1100 Million in 2025 reaching USD 25734.86 Million by 2033, driven by 48% growth in Level 3 ADAS integration across premium EV platforms.

Top Growth Drivers: Solid-state LiDAR adoption rose 42%, autonomous fleet trials expanded 35%, and automotive AI sensor fusion deployment increased 29% globally.

Short-Term Forecast: By 2028, LiDAR unit costs decline 37% while object-detection efficiency improves 45% through semiconductor miniaturization and AI-enabled processing.

Emerging Technologies: FMCW LiDAR, edge AI perception systems, and 4D sensing architectures improve vehicle response accuracy by over 32% in advanced mobility programs.

Regional Leaders: Asia-Pacific surpasses USD 11 billion with EV-linked adoption, North America crosses USD 7 billion through robo-taxi expansion, and Europe exceeds USD 5 billion via safety regulation upgrades.

Consumer/End-User Trends: More than 34% of premium vehicle buyers prioritize autonomous safety packages integrating advanced LiDAR-assisted navigation systems.

Pilot/Case Example: In 2026, autonomous shuttle deployments in smart-city corridors reduced collision-response delays by 41% through real-time LiDAR mapping integration.

Competitive Landscape: Top manufacturers control nearly 58% market share, with major competition centered around sensor range, thermal resilience, and automotive-grade scalability.

Regulatory & ESG Impact: European vehicle safety mandates increased ADAS-linked LiDAR installations by 26%, while energy-efficient sensors reduced system power consumption by 18%.

Investment & Funding: Global Automotive LiDAR investments exceeded USD 6.5 billion in 2026, led by semiconductor partnerships, regional manufacturing expansion, and mobility-tech alliances.

Innovation & Future Outlook: Next-generation chip-scale LiDAR and software-defined vehicle platforms accelerate high-volume deployment, strengthening long-term autonomous mobility commercialization strategies.

Automotive LiDAR demand is expanding rapidly across autonomous passenger vehicles, commercial robo-taxis, and intelligent logistics fleets as OEMs prioritize high-precision environmental sensing. Solid-state LiDAR systems now represent over 46% of new automotive sensor integration due to lower thermal load and compact architecture. Supply-chain regionalization across Asia and North America is accelerating sensor localization strategies while advanced AI perception software improves real-time mapping efficiency, setting the stage for broader strategic competition across mobility ecosystems.

Automotive LiDAR has become a strategic technology layer for autonomous mobility, advanced driver-assistance systems, and intelligent transportation infrastructure as automakers compete on safety precision and software-defined vehicle capabilities. Regulatory tightening around collision-avoidance performance in Europe, China, and the United States is accelerating integration across premium and commercial vehicle categories. Simultaneously, semiconductor supply-chain restructuring is shifting sensor manufacturing closer to automotive hubs, reducing component lead times by nearly 24% since 2024 and improving production continuity for OEMs scaling next-generation vehicle platforms.

Solid-state LiDAR systems now deliver nearly 35% lower power consumption and over 40% smaller module footprints compared with legacy mechanical architectures, enabling easier integration into electric vehicle platforms. China leads high-volume deployment through smart mobility corridors and EV-linked production ecosystems, while Germany remains focused on automotive-grade validation and precision engineering standards. In Japan, highway pilot deployments expanded by 28% in 2026 as domestic automakers accelerated AI sensor fusion partnerships to strengthen autonomous navigation reliability.

Commercial robo-taxi fleets in California and urban logistics operators in Shenzhen are deploying multi-LiDAR sensor stacks to improve obstacle recognition consistency under dense traffic conditions. Automotive suppliers are expanding long-range sensing R&D, semiconductor alliances, and localized assembly operations to secure pricing stability and software interoperability advantages. Over the next three years, competitive leadership will increasingly depend on scalable sensor integration, AI-driven perception accuracy, and resilient automotive electronics ecosystems.

Level 3 autonomous driving deployment and premium EV safety integration are accelerating Automotive LiDAR adoption across major automotive manufacturing hubs. In 2026, more than 33% of newly launched premium electric vehicles in China incorporated advanced LiDAR-assisted perception systems, while automated emergency response accuracy improved by nearly 41% through multi-sensor fusion architectures. European safety regulations requiring enhanced driver-monitoring and collision mitigation capabilities intensified OEM investment in automotive-grade sensing platforms. Semiconductor manufacturers and Tier-1 suppliers are responding through localized production expansion and AI software partnerships to reduce validation cycles and improve scalability. A notable shift toward integrated perception stacks is lowering vehicle computing redundancy by nearly 18%, allowing automakers to optimize energy efficiency while strengthening autonomous driving competitiveness in increasingly software-centric vehicle ecosystems.

Automotive LiDAR deployment remains constrained by elevated semiconductor dependency, thermal calibration complexity, and automotive-grade validation costs. Advanced long-range LiDAR modules still increase vehicle sensor-system costs by approximately 19% to 24% in mid-volume production programs, limiting penetration beyond premium vehicle segments. Export controls affecting advanced chipsets and photonics components disrupted sourcing stability in the United States and East Asia, extending procurement timelines by nearly 21% during peak automotive demand cycles. These pressures directly affect profitability and deployment scalability for mass-market vehicle manufacturers. Companies are mitigating operational exposure through dual-sourcing agreements, localized sensor assembly, and silicon photonics integration strategies. Several Japanese and German suppliers are prioritizing compact solid-state architectures to reduce cooling requirements and improve manufacturing yield consistency across high-volume automotive production lines.

Automotive LiDAR is gaining new commercial relevance through intelligent transportation networks, autonomous freight corridors, and AI-enabled urban mobility platforms. Smart-road infrastructure pilots in South Korea and Singapore improved real-time traffic object detection accuracy by over 38% using connected LiDAR mapping systems integrated with edge computing frameworks. Solid-state sensor adoption increased by 44% across autonomous shuttle and logistics vehicle programs due to lower maintenance requirements and compact integration capability. Governments are also prioritizing vehicle-to-infrastructure communication standards to strengthen road safety automation. Automotive technology firms are expanding software-defined sensing ecosystems through strategic AI partnerships and cloud-based perception analytics. A non-obvious opportunity is emerging in industrial logistics vehicles, where LiDAR-assisted navigation is reducing warehouse transport routing inefficiencies by nearly 27% across high-density fulfillment operations.

The long-term challenge for Automotive LiDAR lies in scaling real-time perception reliability across diverse driving environments, weather conditions, and vehicle architectures. High-density urban environments still reduce long-range object classification consistency by nearly 16% during heavy rain or reflective interference scenarios, creating operational limitations for autonomous mobility systems. Cybersecurity exposure linked to connected sensor networks is also intensifying, particularly in software-defined vehicle platforms handling continuous environmental data transmission. In the United States and Germany, automotive software validation timelines expanded by nearly 22% as regulators increased scrutiny on autonomous driving safety frameworks. Companies must address processing latency, edge AI optimization, and standardized interoperability between LiDAR, radar, and camera systems. Strategic investment in automotive semiconductor ecosystems and resilient software architectures will determine deployment consistency and long-term competitive sustainability.

Solid-State Integration Accelerates Premium EV manufacturers in China and Germany increased solid-state LiDAR integration by nearly 46% during 2026 as compact architectures reduced sensor weight by 28% and lowered thermal management requirements. Automotive suppliers are restructuring production around silicon photonics and wafer-level packaging to improve manufacturing efficiency. Tightened vehicle safety validation standards are also pushing OEMs toward scalable automotive-grade sensing platforms with lower calibration complexity and faster deployment timelines.

AI Sensor Fusion Expands Automotive software platforms combining LiDAR, radar, and camera perception systems improved object-recognition consistency by approximately 39% across dense urban driving environments. United States autonomous mobility operators expanded AI-enabled edge processing deployment to reduce real-time decision latency by 21%. Companies are increasing partnerships with semiconductor and AI chipset developers to optimize onboard compute efficiency while reducing redundant sensing infrastructure across next-generation software-defined vehicles.

Localized Supply Chains Strengthen Automotive LiDAR manufacturers in Japan, South Korea, and the United States increased localized component sourcing by over 31% following semiconductor export restrictions and logistics disruptions affecting photonics supply continuity. OEMs are shifting toward regional assembly ecosystems and long-term chip procurement agreements to stabilize production cycles. A non-obvious operational trend is the rise of dual-manufacturing validation programs designed to maintain uninterrupted sensor certification across multiple automotive platforms.

Commercial Mobility Deployment Grows Autonomous logistics fleets and robo-taxi operators expanded multi-LiDAR deployment by nearly 34% to improve navigation reliability in high-density traffic zones and industrial transport corridors. Parking automation systems integrating short-range Flash LiDAR reduced low-speed collision incidents by 26% in controlled urban mobility programs. Mobility technology firms are scaling cloud-connected fleet analytics platforms to optimize route mapping, predictive maintenance, and sensor performance calibration under continuous operational workloads.

Solid-State LiDAR dominates the Automotive LiDAR Market due to its compact structure, lower power consumption, and superior scalability for high-volume vehicle integration. In 2026, solid-state systems accounted for nearly 49% of automotive LiDAR deployments as EV manufacturers prioritized lightweight sensor integration and reduced maintenance complexity. Compared with Mechanical LiDAR, solid-state variants lowered production-related calibration costs by approximately 27% while improving durability under automotive operating conditions. Automotive OEMs in China and Germany are expanding semiconductor partnerships and localized assembly lines to strengthen supply-chain resilience and accelerate software-defined vehicle integration.

MEMS LiDAR is emerging as the fastest-growing segment, driven by demand for adaptive beam steering and high-resolution perception in Level 3 autonomous systems. Flash LiDAR is gaining traction in parking assistance and short-range sensing applications where rapid object detection improves low-speed navigation efficiency by nearly 24%. Hybrid LiDAR remains strategically relevant for commercial fleets requiring extended range and sensor redundancy across mixed operational environments. Mechanical LiDAR continues to serve testing and prototype programs but is gradually losing share due to higher maintenance requirements and larger hardware footprints.

ADAS represents the leading application segment in the Automotive LiDAR Market as automakers intensify deployment of collision mitigation, adaptive cruise control, and lane-centering systems across premium and mid-range vehicle categories. In 2026, over 43% of new LiDAR-integrated vehicle programs focused primarily on ADAS optimization, particularly in China, the United States, and Germany. Sensor fusion architectures combining LiDAR with radar and AI vision systems improved object-detection consistency by approximately 36% in complex traffic environments. Automotive suppliers are expanding software partnerships and embedded processing capabilities to improve real-time perception reliability while reducing onboard computing inefficiencies.

Autonomous Driving is the fastest-growing application as robo-taxi operators and autonomous freight platforms scale commercial pilot deployments. LiDAR-assisted autonomous navigation programs improved route-mapping precision by nearly 32% in urban mobility corridors during 2026. Collision Avoidance and Parking Assistance remain operationally critical for safety-focused vehicle platforms, while Traffic Monitoring applications are expanding through smart-city infrastructure modernization projects. Companies are increasingly tailoring LiDAR configurations by application intensity, balancing long-range sensing for autonomy with compact short-range systems for urban mobility and parking automation workflows.

Automotive OEMs remain the dominant end-user group due to large-scale vehicle production capacity, direct sensor integration control, and expanding software-defined mobility strategies. In 2026, OEM-led procurement represented nearly 52% of Automotive LiDAR deployment activity as manufacturers accelerated integration across premium EV and ADAS-enabled vehicle platforms. Major automakers reduced external sensor validation timelines by approximately 19% through closer semiconductor collaboration and vertically integrated software partnerships. Automotive suppliers are responding with customized sensing modules, long-term procurement contracts, and scalable production ecosystems designed to support multi-platform vehicle deployment requirements.

Autonomous Vehicle Companies are the fastest-growing end-user segment as commercial robo-taxi operators and autonomous freight developers increase high-density sensor deployment. Multi-LiDAR autonomous testing fleets expanded by over 37% in urban mobility programs across California, Shenzhen, and Tokyo during 2026. Mobility Service Providers and Fleet Operators are also strengthening adoption to improve navigation reliability and operational safety analytics. Research Organizations continue supporting simulation validation and AI training optimization, while Automotive Suppliers are positioning competitively through sensor miniaturization, software interoperability development, and cloud-based fleet perception partnerships.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 50.1% between 2026 and 2033.

Autonomous Mobility Infrastructure Accelerates Commercial Deployment

North America remains a high-value Automotive LiDAR deployment hub driven by autonomous vehicle testing, premium EV integration, and AI-enabled transportation infrastructure modernization. The region represented nearly 27% of global deployment activity in 2025, supported by expanding robo-taxi programs, semiconductor ecosystem investments, and advanced ADAS adoption across passenger and logistics fleets. Automotive software firms and LiDAR manufacturers are strengthening strategic alliances to optimize edge-computing efficiency and perception accuracy. In 2026, multi-sensor autonomous fleet deployments across urban mobility corridors increased by approximately 33%, while automotive-grade LiDAR validation timelines improved through localized testing infrastructure. Strong enterprise investment in software-defined vehicle platforms continues to reinforce operational scalability and autonomous navigation reliability across commercial mobility applications.

United States Market Outlook: The United States leads North American Automotive LiDAR deployment through advanced autonomous mobility ecosystems, semiconductor innovation capacity, and AI-driven automotive software integration. California, Texas, and Arizona remain central testing hubs for robo-taxi and autonomous freight operations. In 2026, more than 61% of active commercial autonomous vehicle pilots in North America incorporated LiDAR-based perception systems to strengthen low-visibility navigation and urban traffic object recognition performance. Automotive OEMs and technology firms are also increasing long-term chip procurement agreements and cloud-based mobility analytics partnerships to stabilize deployment continuity and improve software interoperability.

Regulatory Safety Standards Drive Sensor Integration

Europe is strengthening its Automotive LiDAR position through vehicle safety regulation upgrades, automotive-grade semiconductor innovation, and precision engineering capabilities. The region accounted for nearly 22% of global Automotive LiDAR deployment activity in 2025, supported by accelerated ADAS integration and intelligent transport modernization initiatives. Germany, France, and Sweden are expanding vehicle automation infrastructure to align with stricter collision mitigation and pedestrian safety requirements. In 2026, advanced driver-assistance deployments integrating LiDAR-assisted perception systems improved urban detection consistency by approximately 29% across premium automotive platforms. Automotive suppliers are increasing investments in low-power sensing modules, software-defined vehicle architecture, and localized photonics manufacturing to reduce dependency on imported high-precision automotive components.

Germany Market Outlook: Germany remains Europe’s strategic Automotive LiDAR manufacturing and engineering center due to its advanced automotive supply chain, semiconductor research ecosystem, and strong premium vehicle production base. Automotive OEMs are integrating solid-state LiDAR into high-end EV and autonomous driving platforms to improve sensor redundancy and perception reliability. In 2026, nearly 37% of newly validated autonomous driving test programs in Germany incorporated LiDAR-enabled AI sensor fusion systems. Industrial partnerships between automotive manufacturers and semiconductor firms are also accelerating automotive-grade chip packaging and localized production scalability.

High-Volume Manufacturing Expands Deployment Scale

Asia-Pacific dominates the Automotive LiDAR Market through large-scale EV manufacturing, advanced electronics ecosystems, and rapid autonomous mobility deployment across urban transportation networks. The region contributed approximately 46% of global Automotive LiDAR activity in 2025, with China, Japan, and South Korea driving production concentration and sensor integration scale. Automotive manufacturers are rapidly deploying solid-state and MEMS-based LiDAR systems across premium EV fleets and intelligent logistics vehicles. In 2026, regional automotive sensor exports increased by nearly 31% as localized semiconductor manufacturing and wafer-level photonics packaging improved supply-chain responsiveness. Government-backed smart mobility corridors and AI-enabled transportation infrastructure programs continue accelerating enterprise deployment and autonomous fleet testing activity.

China Market Outlook: China leads global Automotive LiDAR manufacturing and deployment through vertically integrated EV production ecosystems, large-scale smart mobility investments, and aggressive autonomous vehicle commercialization strategies. Shenzhen, Shanghai, and Guangzhou remain key hubs for LiDAR-enabled robo-taxi and intelligent logistics deployments. In 2026, over 44% of newly launched premium electric vehicles in China integrated advanced LiDAR-assisted navigation systems. Domestic automotive suppliers are scaling chip-level LiDAR innovation, localized sensor assembly, and AI perception software partnerships to strengthen export competitiveness and reduce dependence on imported automotive photonics technologies.

Fleet Modernization Supports Early Adoption

South America is emerging as a developing Automotive LiDAR deployment market supported by fleet modernization programs, intelligent traffic management projects, and growing adoption of advanced vehicle safety technologies. Brazil and Chile are leading deployment activity through smart mobility pilots and connected transportation infrastructure initiatives. The region represented nearly 3% of global Automotive LiDAR implementation activity in 2025, constrained by semiconductor import dependency and limited autonomous driving infrastructure. However, logistics fleet operators increased ADAS-linked LiDAR deployment by approximately 18% during 2026 to improve urban delivery safety and route efficiency. Automotive technology providers are focusing on localized partnerships and modular sensing platforms to address cost sensitivity and infrastructure fragmentation across commercial mobility operations.

Brazil Market Outlook: Brazil remains the most strategically significant Automotive LiDAR market in South America due to its automotive manufacturing scale, logistics infrastructure, and growing intelligent mobility investment activity. São Paulo and Curitiba are witnessing increased deployment of LiDAR-assisted fleet management and traffic monitoring systems integrated with commercial vehicle safety platforms. In 2026, connected logistics operators in Brazil improved fleet route optimization efficiency by nearly 16% through AI-enabled sensing and predictive navigation integration. Automotive suppliers are also prioritizing regional assembly partnerships to reduce import-related component volatility and improve deployment flexibility.

Smart Infrastructure Investment Drives Deployment

Middle East & Africa is gradually strengthening Automotive LiDAR adoption through smart-city expansion, autonomous mobility testing, and intelligent transportation infrastructure investment. The region accounted for approximately 2% of global Automotive LiDAR deployment activity in 2025, with the United Arab Emirates and Saudi Arabia leading modernization initiatives. Government-backed urban mobility programs are integrating LiDAR-enabled traffic monitoring and autonomous shuttle systems to improve transport efficiency and road safety automation. In 2026, connected infrastructure deployments supporting AI-based vehicle perception increased by nearly 22% across selected smart-city projects. Automotive technology firms are expanding partnerships with mobility operators and infrastructure developers to establish long-term autonomous transportation ecosystems in high-investment urban corridors.

United Arab Emirates Market Outlook: The United Arab Emirates is emerging as the leading Middle East Automotive LiDAR deployment hub through aggressive smart mobility investment, autonomous transportation pilots, and advanced digital infrastructure capabilities. Dubai and Abu Dhabi are integrating LiDAR-enabled autonomous shuttles and intelligent traffic management systems into urban mobility frameworks. In 2026, nearly 27% of newly approved smart mobility pilot programs in the UAE incorporated advanced LiDAR perception systems to improve navigation consistency and pedestrian safety monitoring. Enterprise partnerships between mobility operators and AI infrastructure firms are accelerating deployment readiness across connected urban transport networks.

The Automotive LiDAR Market is led by technology-focused sensor developers including Luminar, Hesai Technology, Innoviz Technologies, Ouster, and RoboSense competing against automotive suppliers integrating in-house perception ecosystems. The top five players collectively control nearly 58% of global deployment activity, with competition centered on detection range, software integration speed, thermal efficiency, and automotive-grade scalability. Chinese manufacturers are competing aggressively on cost optimization, reducing sensor production expenses by nearly 24%, while North American and Israeli firms focus on long-range precision and AI-driven perception performance improvements exceeding 30% in dense urban environments. Automotive OEMs are increasingly bypassing standalone sourcing models through direct semiconductor alliances and vertically integrated software partnerships. Strategic competition is shifting toward chip-scale solid-state LiDAR, regional supply-chain control, and embedded AI perception capabilities. High automotive validation requirements and semiconductor dependency remain major entry barriers. Winning requires scalable production, software interoperability, and resilient automotive electronics partnerships.

Luminar Technologies

Hesai Technology

Innoviz Technologies

RoboSense

Ouster

Valeo

Aeva Technologies

Cepton Technologies

Quanergy Solutions

Velodyne Lidar

Leica Geosystems

Continental AG

Bosch

Benewake

Automotive LiDAR technology is rapidly shifting from mechanical architectures toward solid-state and MEMS-based systems optimized for scalable EV and ADAS deployment. In 2026, solid-state LiDAR represented nearly 49% of new automotive sensor integration due to 32% lower power consumption and reduced thermal calibration complexity. Compared with legacy mechanical LiDAR, newer chip-scale designs improve manufacturing efficiency by approximately 28% while reducing hardware footprint by over 40%. Automotive OEMs are increasingly integrating LiDAR with AI-driven sensor fusion platforms to strengthen object recognition consistency under dense urban traffic conditions and low-visibility driving environments.

Emerging technologies including FMCW LiDAR, edge AI processing, and 4D environmental mapping are improving long-range perception precision by nearly 35% across autonomous mobility platforms. High-resolution Flash LiDAR adoption increased by approximately 24% in parking automation and smart mobility infrastructure projects due to faster low-speed object detection performance. Chinese and German automakers are expanding semiconductor partnerships and photonics manufacturing alliances to secure automotive-grade supply continuity and accelerate software-defined vehicle deployment efficiency.

Between 2026 and 2028, competitive advantage will increasingly depend on AI-integrated perception ecosystems, chip-level LiDAR miniaturization, and localized semiconductor production. Companies scaling embedded AI sensing and automotive-grade software interoperability are positioned to secure faster deployment cycles, lower validation costs, and stronger autonomous mobility differentiation.

June 2024 – Innoviz Technologies partnered with a major automotive OEM to integrate new short-range LiDAR into Level 4 autonomous vehicle platforms, expanding high-resolution perception coverage beyond 90-degree vertical field visibility. The collaboration strengthened Innoviz’s commercial production pipeline and autonomous mobility positioning. Source: Innoviz Technologies

October 2025 – Hesai Technology became the first automotive LiDAR manufacturer to surpass 1 million units in annual production, with monthly deliveries exceeding 100,000 units. The milestone reinforced large-scale manufacturing leadership and accelerated automotive OEM confidence in high-volume LiDAR deployment capabilities globally.

January 2026 – Hesai Technology announced plans to double annual LiDAR production capacity from 2 million to over 4 million units through expanded in-house manufacturing infrastructure. The expansion strengthened supply-chain resilience and improved scalability for ADAS and robotics-focused automotive deployment programs worldwide. Source: Hesai Technology

April 2026 – Hesai Technology unveiled a color-detecting LiDAR platform integrating spatial sensing and color recognition into a single automotive-grade system. The technology improved autonomous perception accuracy for traffic signals and road hazards while supporting next-generation Level 3 vehicle automation deployment strategies across China.

The Automotive LiDAR Market report provides detailed analysis across technology evolution, deployment strategies, industrial adoption, and competitive positioning between 2026 and 2033. The study covers key LiDAR types including Mechanical LiDAR, Solid-State LiDAR, Flash LiDAR, MEMS LiDAR, and Hybrid LiDAR, while evaluating application trends across autonomous driving, ADAS, collision avoidance, parking assistance, and traffic monitoring systems. More than 45% of deployment analysis focuses on advanced driver-assistance integration and autonomous mobility infrastructure expansion across high-volume automotive manufacturing hubs.

The report further examines operational dynamics across Automotive OEMs, Autonomous Vehicle Companies, Mobility Service Providers, Fleet Operators, Automotive Suppliers, and Research Organizations. Regional coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa with strategic assessment of semiconductor localization, smart mobility infrastructure, and AI-enabled sensing ecosystems. It also evaluates emerging investment areas including chip-scale LiDAR, edge AI perception platforms, and automotive photonics manufacturing to support expansion planning, supply-chain optimization, and long-term competitive strategy development.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1100 Million |

|

Market Revenue in 2033 |

USD 25734.86 Million |

|

CAGR (2026 - 2033) |

48.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Luminar Technologies, Hesai Technology, Innoviz Technologies, RoboSense, Ouster, Valeo, Aeva Technologies, Cepton Technologies, Quanergy Solutions, Velodyne Lidar, Leica Geosystems, Continental AG, Bosch, Benewake |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |