Reports

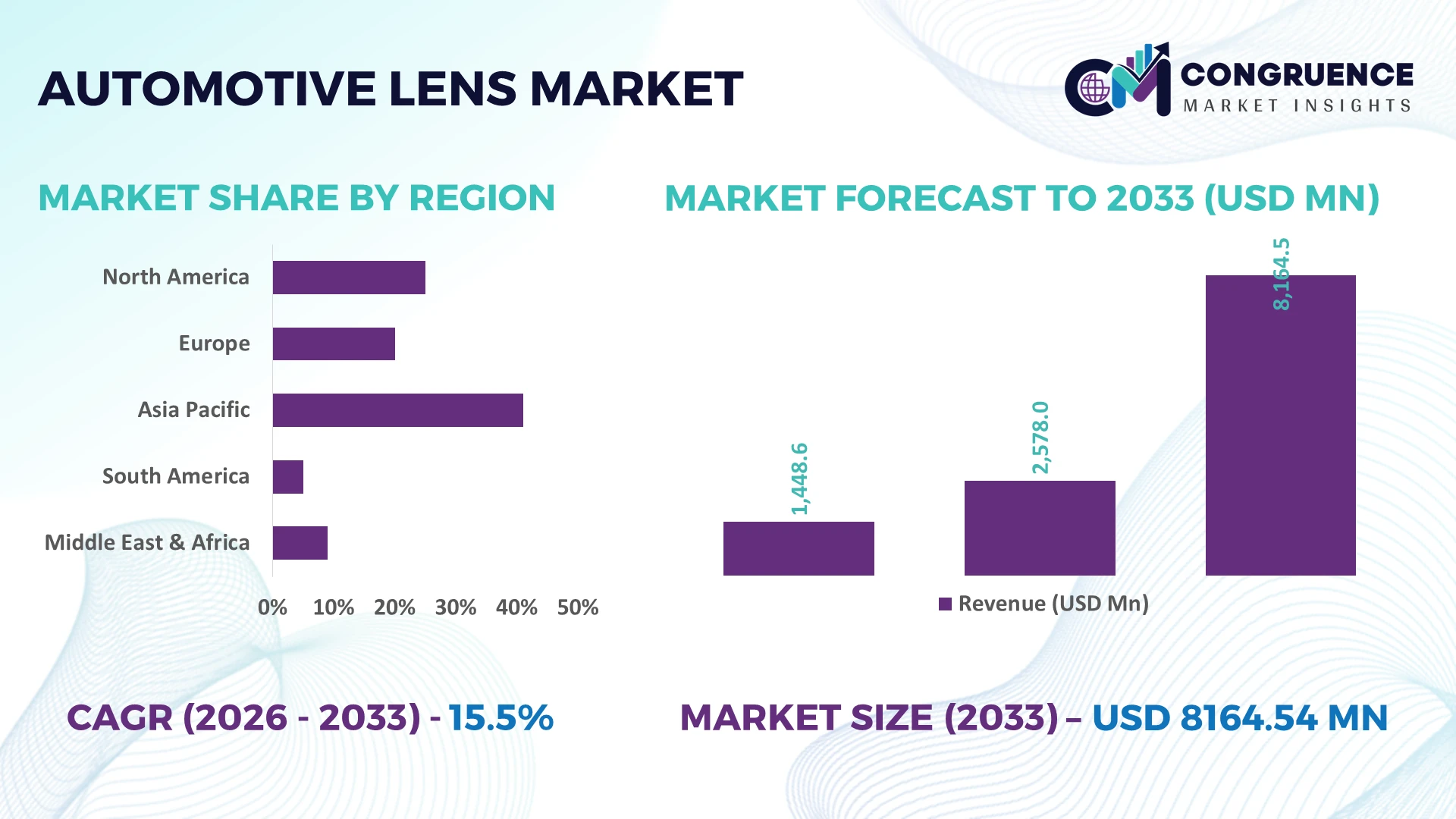

The Global Automotive Lens Market was valued at USD 2577.96 Million in 2025 and is anticipated to reach a value of USD 8164.54 Million by 2033 expanding at a CAGR of 15.5% between 2026 and 2033.

Growth is being accelerated by the rapid integration of ADAS cameras, surround-view systems, digital mirrors, and high-resolution optical sensors across passenger and commercial vehicles.

China remains the dominant manufacturing and adoption hub, accounting for approximately 36% of global automotive production while supplying a significant share of precision optical components through large-scale electronics and automotive clusters. Germany continues to lead premium automotive optics innovation, with advanced driver-assistance integration exceeding 70% across newly launched premium vehicle platforms. Ongoing semiconductor supply-chain diversification following geopolitical disruptions has further strengthened regional manufacturing resilience.

Manufacturers prioritizing advanced optical precision, localized production, and next-generation sensor compatibility are positioned to secure stronger long-term contracts across global automotive OEM supply chains.

Market Size & Growth: USD 2577.96 million in 2025 reaching USD 8164.54 million by 2033 at 15.5% CAGR, supported by expanding ADAS camera integration and intelligent vehicle platforms.

Top Growth Drivers: ADAS camera adoption exceeds 28%, EV production expands above 22%, and autonomous testing programs increase over 30% across major automotive economies.

Short-Term Forecast: By 2028, automated lens manufacturing reduces production defects by nearly 18% while improving assembly efficiency by approximately 20%.

Emerging Technologies: AI-based optical calibration, wafer-level optics, and advanced polymer lenses improve imaging accuracy by over 25% in next-generation automotive vision systems.

Regional Leaders: Asia-Pacific exceeds USD 3400 million, Europe surpasses USD 1900 million, and North America crosses USD 1500 million through expanding intelligent mobility adoption.

Consumer/End-User Trends: More than 65% of newly introduced premium vehicles integrate multi-camera vision systems supporting parking, safety, and driver assistance functions.

Pilot/Case Example: In 2025, AI-enabled lens inspection deployment improved optical quality consistency by approximately 22% while reducing manual inspection requirements.

Competitive Landscape: Top manufacturers collectively control around 48% of the global market, with leading participation from Sunny Optical, Sekonix, AGC, Kantatsu, and Ricoh.

Regulatory & ESG Impact: Vehicle safety regulations increase camera deployment by nearly 30%, while lightweight optical materials reduce component weight by approximately 15%.

Investment & Funding: More than USD 1.8 billion supports optical manufacturing expansion, strategic partnerships, and regional supply-chain localization following global trade realignments.

Innovation & Future Outlook: High-resolution multi-lens modules, infrared optics, and hybrid glass-polymer technologies strengthen next-generation autonomous mobility strategies through higher imaging performance.

Advanced automotive lens solutions are increasingly deployed across ADAS, autonomous driving, digital mirror systems, and in-cabin monitoring platforms. Manufacturers are introducing lightweight hybrid optics, AI-assisted calibration, and high-transmission coatings that improve imaging performance by approximately 25%. Growing localization of optical component production amid evolving automotive supply-chain strategies and stricter vehicle safety requirements continues to reshape procurement priorities, setting the stage for broader strategic market developments.

Automotive lens technology has become a strategic differentiator as vehicle manufacturers compete through software-defined mobility, advanced driver assistance, and automated safety platforms. Optical performance now directly influences object detection accuracy, driver monitoring reliability, and autonomous perception. Supply-chain restructuring after semiconductor disruptions has encouraged OEMs to localize optical component sourcing and establish multi-country manufacturing networks, reducing procurement lead times by nearly 20% while strengthening production resilience.

Compared with conventional single-element optical systems, advanced multi-element aspherical lenses improve image clarity by approximately 30% while lowering optical distortion by nearly 25%, enabling more reliable AI-powered vision processing under varied driving conditions. China leads high-volume manufacturing through integrated electronics ecosystems, whereas Germany emphasizes premium optical engineering and precision validation for luxury vehicle platforms. Over the next two to three years, camera-equipped vehicle penetration is expected to exceed 75% in newly introduced mid-range passenger models, supported by expanding intelligent safety requirements and digital vehicle architectures.

A practical example is the deployment of AI-assisted automated optical inspection within lens production, reducing defect rates by nearly 18% and improving manufacturing consistency. Companies are expanding cleanroom production capacity, strengthening partnerships with image sensor suppliers, and investing in lightweight optical materials. Organizations that integrate advanced optics with scalable manufacturing and localized supply networks will secure stronger competitive positioning as intelligent vehicle platforms become the industry benchmark.

Mandatory vehicle safety features and intelligent mobility programs are rapidly increasing demand for high-performance automotive lenses. More than 70% of premium vehicle launches now integrate multiple camera modules, while ADAS installation rates continue expanding by over 25% across key automotive manufacturing countries. China has accelerated domestic optical production through investments in precision manufacturing, reducing component dependency on overseas suppliers. This structural shift improves delivery reliability while supporting faster vehicle development cycles. Leading companies are expanding automated optical assembly lines, investing in advanced coating technologies, and partnering with semiconductor and image sensor manufacturers to deliver higher imaging precision with lower production variability, strengthening long-term OEM relationships.

Production scalability remains constrained by fluctuations in optical-grade glass, engineering polymers, and specialized coating materials, with raw material prices experiencing periodic swings exceeding 15%. Japan continues to dominate several precision optical processing capabilities, creating supplier concentration for critical components. High manufacturing tolerances increase inspection complexity and extend production qualification cycles by approximately 20% for new lens platforms. These factors pressure production efficiency and contract profitability for tier-one suppliers. Companies are reducing operational risk by diversifying material sourcing, increasing localized polishing and coating capacity, and adopting alternative polymer-based optical solutions that improve manufacturing flexibility while reducing dependency on limited specialist suppliers.

The rapid expansion of AI-powered perception systems creates significant opportunities for advanced automotive lenses designed for autonomous driving and intelligent cabin monitoring. Automated optical inspection improves production accuracy by nearly 22%, while lightweight hybrid lens materials reduce component weight by approximately 15%, supporting vehicle efficiency objectives. South Korea is strengthening investments in next-generation automotive imaging ecosystems through collaborations between electronics and mobility manufacturers. Companies are accelerating R&D for infrared-compatible optics, wafer-level manufacturing, and high-resolution multi-camera platforms while forming strategic partnerships across software, sensor, and optics ecosystems. These integrated solutions create differentiated value beyond traditional hardware supply and strengthen long-term technology positioning.

Maintaining consistent optical quality across rapidly expanding production volumes remains a critical execution challenge. Multi-camera vehicle architectures require micron-level manufacturing precision, while calibration complexity has increased by nearly 30% compared with earlier vehicle platforms. Germany's premium automotive sector continues demanding tighter validation standards for safety-critical imaging systems, increasing production qualification requirements. Workforce shortages in precision optics and advanced metrology further limit manufacturing scalability. Companies must invest in AI-driven quality control, digital manufacturing platforms, workforce development, and collaborative engineering partnerships to maintain product consistency, accelerate qualification timelines, and preserve competitiveness as intelligent vehicle platforms become increasingly sophisticated.

AI-Driven Optical Calibration AI-enabled calibration is replacing manual validation across high-volume automotive lens production, reducing inspection time by nearly 35% and improving optical consistency by approximately 20%. Japan and South Korea are expanding automated metrology facilities as labor shortages and stricter safety validation increase process complexity. Manufacturers are integrating machine vision with production analytics to accelerate qualification cycles and reduce quality variation across multi-camera vehicle platforms.

Localized Precision Manufacturing Networks Automotive lens suppliers are restructuring production footprints closer to OEM assembly plants, cutting logistics lead times by around 18% and lowering inventory requirements by nearly 15%. Supply-chain diversification following semiconductor disruptions has accelerated investment in China, Mexico, and Eastern Europe. Companies are expanding regional polishing, coating, and assembly operations through long-term manufacturing partnerships to strengthen delivery resilience and operational flexibility.

Lightweight Hybrid Lens Adoption Glass-polymer hybrid lens designs are gaining commercial traction, reducing component weight by approximately 15% while maintaining high optical transmission for ADAS and digital vision systems. Stricter vehicle efficiency requirements are encouraging broader material innovation. Leading manufacturers are increasing investment in advanced coatings, precision molding, and integrated optical engineering to improve production scalability without compromising durability or imaging performance.

Multi-Sensor Platform Integration Vehicle platforms increasingly combine camera, LiDAR, and driver-monitoring optics into unified sensing architectures, improving perception accuracy by nearly 25% while reducing integration complexity by approximately 18%. Germany and the United States continue accelerating intelligent mobility programs supporting sensor fusion. Automotive lens suppliers are expanding strategic collaborations with semiconductor and imaging companies to deliver standardized optical modules that simplify vehicle development and shorten product launch timelines.

Camera lenses represent the dominant product segment because they serve as the primary optical interface for ADAS, surround-view, driver monitoring, and automated parking systems. More than 60% of newly introduced passenger vehicles now incorporate multiple camera modules, making this category central to automotive safety architectures. Glass lenses retain strong demand in high-temperature and premium applications due to superior optical stability, while plastic lenses continue expanding through lightweight construction and lower manufacturing costs. Manufacturers are strengthening precision molding capabilities and investing in advanced optical coatings to improve image quality and production efficiency.

LiDAR lenses are the fastest-growing segment as intelligent driving programs increasingly require long-range environmental sensing. Deployment of LiDAR-equipped vehicle platforms has increased by over 30% across premium electric vehicle programs, encouraging suppliers to accelerate optical innovation. Headlamp lenses continue evolving through adaptive lighting technologies, supporting improved visibility and styling differentiation. Companies are prioritizing product portfolios that integrate camera, LiDAR, and lighting optics, enabling broader OEM partnerships and stronger long-term competitive positioning.

ADAS remains the leading application because advanced safety systems increasingly rely on high-resolution automotive lenses for lane keeping, emergency braking, traffic recognition, and parking assistance. Camera-equipped safety systems are now installed in over 70% of premium vehicle launches, while intelligent perception functions continue expanding into mid-range vehicle categories. Headlighting applications remain an important mature segment through adaptive beam technologies, and surround-view systems continue strengthening demand across urban mobility platforms. Manufacturers are scaling optical module production and integrating AI-assisted calibration to improve imaging consistency.

Autonomous driving represents the fastest-growing application as sensor-rich vehicle platforms require advanced optics with greater precision and durability. Driver monitoring systems are also expanding rapidly following enhanced vehicle safety regulations and occupant monitoring requirements. Companies are increasing investment in integrated sensing platforms combining cameras with LiDAR and infrared optics, enabling higher operational accuracy while reducing system integration complexity. This shift is strengthening long-term demand for specialized automotive lens technologies across intelligent mobility ecosystems.

Passenger vehicles remain the largest end-user segment because high-volume production supports widespread deployment of ADAS cameras, digital mirrors, surround-view systems, and driver monitoring technologies. More than 65% of newly introduced passenger vehicle platforms now integrate multiple optical sensing systems, increasing demand for precision automotive lenses. Automotive OEMs continue investing in platform standardization to reduce engineering complexity, while the aftermarket maintains steady replacement demand for camera and lighting components. Suppliers are strengthening OEM partnerships through customized optical modules and long-term development agreements.

Electric vehicles represent the fastest-growing end-user segment as software-defined vehicle architectures require additional optical sensing capabilities for intelligent driving functions. Commercial vehicles are steadily increasing camera deployment to improve fleet safety and operational visibility, particularly in logistics applications. Companies are expanding dedicated production lines, localized manufacturing, and collaborative development programs to address evolving OEM requirements. Competitive strategies increasingly emphasize modular optical platforms that support both conventional and electric vehicle production while improving manufacturing efficiency.

Asia-Pacific accounted for the largest market share at 46.8% in 2025 however, North America is expected to register the fastest growth, expanding at a 16.3% CAGR between 2026 and 2033.

Advanced ADAS Manufacturing and Optical Innovation

North America is strengthening its position through rapid deployment of advanced driver assistance systems, software-defined vehicle development, and localized optical component manufacturing. The region represents approximately 24% of global automotive lens demand, supported by strong investment from vehicle manufacturers and technology suppliers. Production of high-resolution camera modules continues to expand alongside electric vehicle programs, while automated optical inspection has improved manufacturing efficiency by nearly 20%. Strategic partnerships between automotive OEMs, semiconductor developers, and optics manufacturers are accelerating integrated sensor development. Companies are increasing regional assembly capacity and precision coating capabilities to shorten supply cycles and improve production resilience as intelligent mobility platforms become standard across new vehicle launches.

United States Market Outlook: The United States leads the regional market through large-scale automotive innovation, advanced semiconductor capabilities, and expanding autonomous vehicle testing. More than 75% of newly launched premium vehicle models incorporate multiple camera-based safety systems, driving demand for precision automotive lenses. Domestic manufacturers continue investing in automated production, AI-assisted quality control, and collaborative engineering with image sensor companies, strengthening localized manufacturing while reducing dependence on overseas optical component suppliers.

Premium Engineering Drives Optical Precision

Europe maintains a strong market position through premium automotive manufacturing, advanced optical engineering, and stringent vehicle safety requirements. The region contributes approximately 22% of global automotive lens deployment, supported by luxury vehicle production and continuous investment in intelligent driving technologies. Adaptive lighting, driver monitoring, and camera-based perception systems are becoming standard across premium platforms, while advanced optical validation improves product reliability by approximately 18%. Manufacturers continue expanding precision coating technologies and digital production processes to support increasingly complex sensing systems. Sustainability initiatives also encourage lightweight optical materials that improve vehicle efficiency without compromising imaging performance.

Germany Market Outlook: Germany remains Europe's strategic center for automotive optics due to its concentration of premium vehicle manufacturers, precision engineering expertise, and advanced supplier ecosystem. More than 70% of newly introduced premium domestic vehicle platforms integrate sophisticated camera-based safety technologies. Companies continue expanding collaborative research programs focused on optical sensing, LiDAR integration, and automated manufacturing, strengthening the country's leadership in next-generation automotive imaging solutions.

Manufacturing Scale Supports Global Leadership

Asia-Pacific dominates the automotive lens market through unmatched manufacturing capacity, vertically integrated electronics supply chains, and high-volume vehicle production. The region accounts for nearly 46.8% of global market activity, supported by strong automotive clusters across China, Japan, and South Korea. Precision optical manufacturing continues expanding, with automated production improving output efficiency by approximately 25%. Local suppliers increasingly integrate lens production with semiconductor packaging and camera module assembly, reducing logistics complexity and accelerating product delivery. Investments in intelligent mobility infrastructure and domestic component localization continue strengthening the region's long-term competitive advantage.

China Market Outlook: China serves as the world's largest production base for automotive optics, supported by extensive electronics manufacturing infrastructure and strong domestic vehicle demand. The country contributes more than one-third of global vehicle production and continues expanding high-precision optical manufacturing through automated facilities. Automotive lens suppliers are strengthening partnerships with electric vehicle manufacturers and image sensor developers while increasing exports of advanced optical modules to international automotive OEMs.

Localized Vehicle Production Expands Demand

South America is experiencing steady market development as automotive production recovers and manufacturers increase adoption of modern vehicle safety technologies. The region contributes approximately 4% of global automotive lens deployment, with demand primarily supported by passenger vehicle assembly and commercial fleet modernization. Investments in localized automotive manufacturing have improved regional supply capabilities, while production efficiency has increased by nearly 12% through greater automation. Infrastructure constraints and imported precision components continue affecting manufacturing costs, encouraging suppliers to establish regional distribution and assembly operations that improve delivery performance and inventory management.

Brazil Market Outlook: Brazil represents the largest automotive manufacturing hub in South America, supported by established vehicle assembly operations and expanding supplier networks. Domestic production continues integrating additional camera-based safety features into passenger vehicles, while automotive component manufacturers increase investment in localized assembly and technical partnerships. Growing industrial capability is strengthening Brazil's position as the region's primary market for advanced automotive optical technologies.

Industrial Modernization Supports Market Development

The Middle East & Africa market is progressing through industrial diversification, automotive manufacturing investments, and expanding intelligent transportation initiatives. The region accounts for approximately 3.2% of global automotive lens demand, with growth supported by vehicle assembly expansion and infrastructure modernization. Investments in industrial zones and advanced manufacturing facilities have improved component localization, while deployment of modern production technologies has increased operational efficiency by nearly 15%. International automotive suppliers continue forming strategic partnerships with regional manufacturers to improve supply reliability and technical capability as mobility infrastructure evolves.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's most significant automotive investment destination through industrial diversification initiatives and expanding vehicle manufacturing capacity. New automotive production projects are increasing demand for locally supplied precision components, including advanced optical systems. Companies are prioritizing technology partnerships, workforce development, and automated manufacturing capabilities to establish a competitive domestic automotive supply chain supporting future intelligent vehicle production.

Competition in the automotive lens market centers on Sunny Optical Technology, Sekonix, AGC, Kantatsu, and Ricoh competing against regional precision optics manufacturers and specialized camera module suppliers. Global leaders compete through optical engineering, manufacturing scale, and long-term OEM programs, while regional players emphasize cost efficiency, localized production, and rapid customization. The top five companies collectively account for approximately 48% of global market activity, creating a moderately consolidated structure. Performance leadership increasingly depends on imaging precision, production automation, and integrated supply networks rather than pricing alone. Automated optical inspection improves manufacturing consistency by nearly 20%, advanced coating technologies enhance light transmission by approximately 15%, and localized production reduces delivery cycles by around 18%. Companies are expanding cleanroom facilities, forming partnerships with image sensor developers, and vertically integrating precision molding with coating operations. Competition is shifting toward AI-enabled optical platforms and sensor integration, raising qualification standards for new entrants. Success requires scalable precision manufacturing, strong OEM relationships, rapid product validation, and resilient localized supply ecosystems.

Sunny Optical Technology

Sekonix Co., Ltd.

AGC Inc.

Kantatsu Co., Ltd.

Ricoh Company, Ltd.

Largan Precision Co., Ltd.

Genius Electronic Optical Co., Ltd.

Asia Optical Co., Inc.

Fujifilm Corporation

Kinko Optical Co., Ltd.

Calin Technology Co., Ltd.

Ningbo Yongxin Optics Co., Ltd.

Current technology development is centered on high-resolution aspherical optics, AI-assisted optical calibration, and automated precision inspection. AI-driven inspection reduces manufacturing defects by approximately 20%, while advanced anti-reflective coatings improve optical transmission by nearly 15% under low-light conditions. More than 65% of premium vehicle camera modules now incorporate automated calibration before final assembly, improving production consistency and reducing manual intervention. Manufacturers integrating optical engineering with digital manufacturing achieve faster validation cycles and stronger OEM qualification performance.

Emerging technologies include wafer-level optics, hybrid glass-polymer lens construction, infrared-compatible optics, and integrated sensor fusion platforms. Compared with conventional molded optical assemblies, wafer-level manufacturing reduces assembly complexity by approximately 25% while improving dimensional consistency by nearly 18%. Automotive OEMs and tier-one suppliers benefit through lower production variability, lighter components, and simplified multi-camera integration. These technologies also improve compatibility with LiDAR, driver monitoring, and surround-view platforms that increasingly define intelligent vehicle architectures.

Between 2026 and 2028, competitive differentiation will increasingly depend on software-enabled optical systems, automated metrology, and sensor-integrated lens platforms. Deployment of AI-supported manufacturing is expected to exceed 70% among leading automotive optics suppliers, strengthening process stability and accelerating product launches. Companies investing early in precision automation, advanced materials, and integrated optical ecosystems will secure stronger long-term supply agreements, shorter development timelines, and greater resilience against evolving automotive technology requirements.

April 2024 Sunny Optical Technology partnered with Renxin Technology at Auto China to showcase a high-performance in-vehicle HD camera module using a 16Gbps high-speed SerDes solution, strengthening next-generation ADAS imaging capabilities and accelerating intelligent vehicle integration.

April 2024 Sunny Automotive Optech received FORVIA's Best Supplier Award after expanding collaboration across automotive lenses, smart headlamps, and sensing modules, supported by its self-developed automated production lines that improved manufacturing efficiency and supply reliability.

October 2024 Researchers published a comprehensive industry review highlighting surround-view fisheye optical systems, emphasizing their role in automated driving while identifying optical artifact reduction as a critical requirement for 360° vehicle perception and safer computer vision deployment.

April 2026 Sekonix accelerated its strategic transition toward automotive camera lenses through vertically integrated manufacturing covering optical design, molding, coating, assembly, and inspection, positioning the company to benefit from expanding autonomous driving platforms and higher automotive imaging demand.

The report delivers comprehensive analysis of the global automotive lens market across Glass Lenses, Plastic Lenses, Camera Lenses, Headlamp Lenses, and LiDAR Lenses, while evaluating demand across ADAS, Headlighting, Surround View Systems, Driver Monitoring, and Autonomous Driving applications. End-user assessment covers Passenger Vehicles, Commercial Vehicles, Automotive OEMs, Aftermarket, and Electric Vehicles. Regional evaluation spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by competitive benchmarking of major optical manufacturers and technology providers.

The study examines deployment trends, precision manufacturing developments, AI-enabled optical inspection, advanced coatings, hybrid optical materials, and sensor-fusion technologies shaping industry evolution between 2026 and 2033. It incorporates operational indicators such as adoption rates, production concentration, and supplier positioning to support investment planning, product portfolio optimization, manufacturing expansion, partnership strategy, competitive benchmarking, and long-term decision-making across automotive optics and intelligent mobility value chains.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 2577.96 Million |

Market Revenue in 2033 | USD 8164.54 Million |

CAGR (2026 - 2033) | 15.5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Sunny Optical Technology, Sekonix Co., Ltd., AGC Inc., Kantatsu Co., Ltd., Ricoh Company, Ltd., Largan Precision Co., Ltd., Genius Electronic Optical Co., Ltd., Asia Optical Co., Inc., Fujifilm Corporation, Kinko Optical Co., Ltd., Calin Technology Co., Ltd., Ningbo Yongxin Optics Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |