Reports

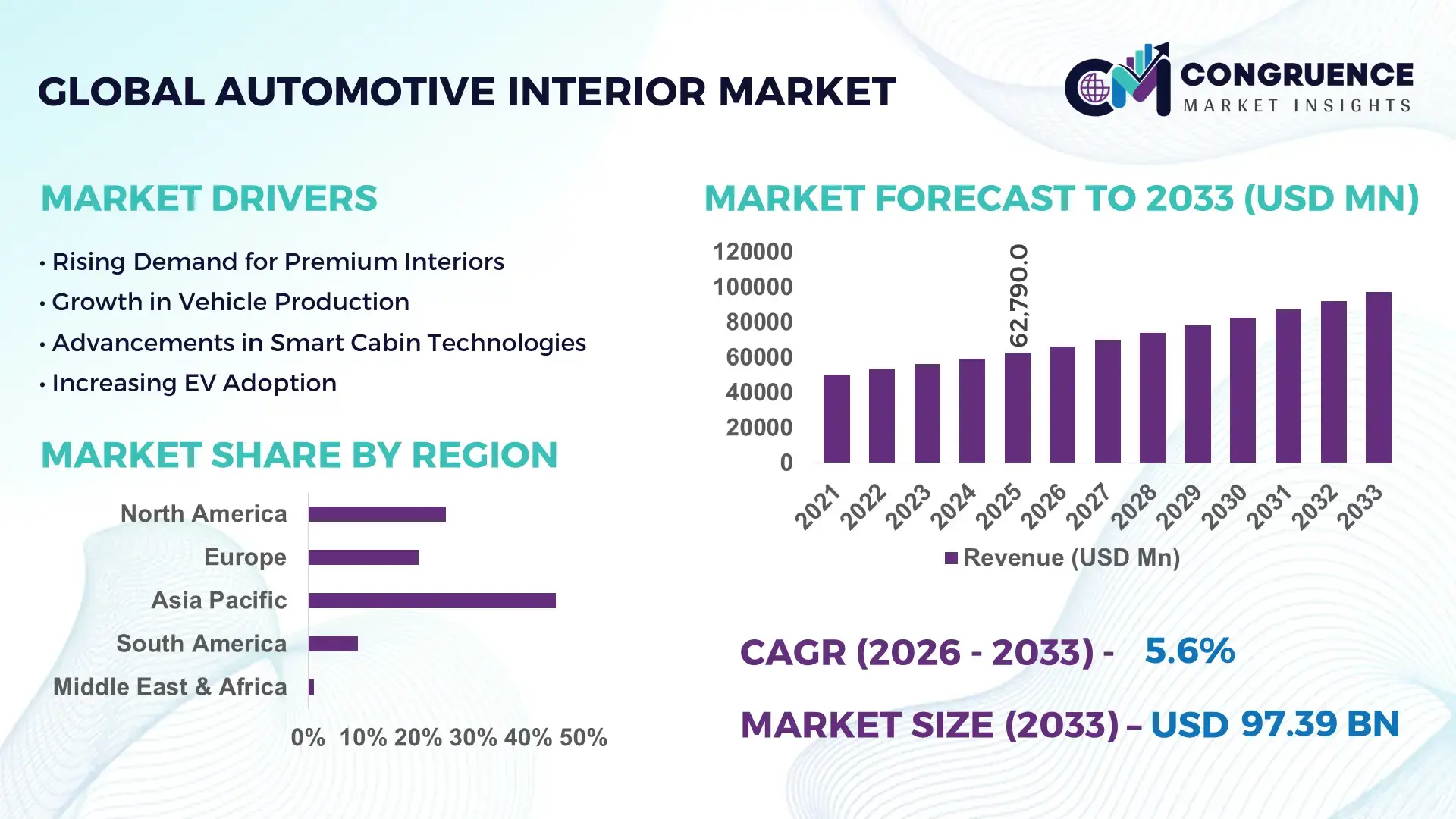

The Global Automotive Interior Market was valued at USD 62790 Million in 2025 and is anticipated to reach a value of USD 97390.73 Million by 2033 expanding at a CAGR of 5.64% between 2026 and 2033. Growth is being driven by accelerating integration of digital cockpits, lightweight interior materials, connected vehicle interfaces, and premium cabin technologies across passenger and electric vehicle platforms.

China remains the dominant automotive interior manufacturing hub, accounting for approximately 32% of global vehicle production and supported by multi-billion-dollar investments in electric mobility and smart manufacturing ecosystems. The country’s digital cockpit adoption exceeds 45% in newly launched passenger vehicles, compared with roughly 28% in India, where localization initiatives and production-linked incentives are expanding component capacity. Ongoing supply-chain realignments following Red Sea shipping disruptions have further strengthened regional sourcing strategies across Asia.

Manufacturers prioritizing advanced interior electronics, sustainable materials, and localized supply networks are positioned to secure stronger OEM partnerships and higher-value program allocations through 2033.

Market Size & Growth: USD 62,790 million in 2025 to USD 97,390.73 million by 2033 at 5.64% CAGR, supported by digital cockpit deployment and vehicle electrification.

Top Growth Drivers: Smart cockpit adoption (+18%), premium vehicle interior demand (+15%), lightweight material integration (+12%).

Short-Term Forecast: By 2028, interior module assembly efficiency improves 14% while component integration costs decline 9%.

Emerging Technologies: AI-enabled HMIs, OLED displays, and sustainable composites deliver up to 20% better cabin functionality.

Regional Leaders: Asia-Pacific exceeds USD 43 billion, Europe surpasses USD 24 billion, North America approaches USD 19 billion; connected interior adoption accelerates across all regions.

Consumer/End-User Trends: More than 52% of new vehicle buyers prioritize digital displays, connectivity, and personalized cabin experiences.

Pilot/Case Example: In 2026, integrated smart-cabin deployments reduced wiring complexity by 17% and assembly time by 11%.

Competitive Landscape: Top manufacturers control roughly 38% market share, led by Adient, Lear, Faurecia, Yanfeng, and Toyota Boshoku.

Regulatory & ESG Impact: Recycled and bio-based interior materials reduce component carbon footprints by up to 25%.

Investment & Funding: Over USD 8 billion supports capacity expansion, localization programs, and advanced material development amid global supply-chain diversification.

Innovation & Future Outlook: Next-generation immersive cabins, AI assistants, and software-defined interiors are reshaping competitive differentiation strategies.

Automotive Interior Market demand is expanding across digital instrument panels, premium seating systems, ambient lighting, smart surfaces, and sustainable cabin materials as automakers focus on vehicle differentiation. Recent innovations include AI-enabled cockpit controls and integrated display ecosystems that improve user interaction efficiency by over 20%. Growing adoption of recycled materials and regionalized component sourcing reflects evolving regulatory requirements and supply-chain resilience priorities, setting the stage for broader strategic transformation across the industry.

Automotive interiors have evolved from comfort-focused components into strategic differentiators that influence vehicle purchasing decisions, software integration strategies, and OEM profitability. As electric vehicle adoption accelerates and software-defined vehicle architectures expand, manufacturers are increasing investment in intelligent cabins, advanced materials, and integrated digital interfaces. Supply-chain restructuring following recent logistics disruptions has also intensified localization efforts, making interior systems a critical element of manufacturing resilience and competitive positioning.

Technology transformation is reshaping cost and performance benchmarks. Integrated digital cockpit platforms reduce wiring complexity by nearly 18% compared with conventional distributed systems while lowering assembly time by approximately 12%. China leads large-scale deployment through vertically integrated EV production ecosystems, whereas Germany maintains an innovation advantage in premium cockpit engineering and sustainable material development. More than 45% of newly launched passenger vehicles now feature connected interior functions, reflecting rapid adoption of software-enabled cabin technologies.

Over the next two to three years, manufacturers are expected to expand partnerships across electronics, software, and materials value chains to accelerate deployment cycles. For example, automakers increasingly integrate AI-based voice controls with centralized computing platforms to simplify cabin architecture and improve user engagement. Companies prioritizing smart interiors, localized sourcing, and scalable digital ecosystems will strengthen competitive positioning, improve operational flexibility, and capture higher-value vehicle programs.

The strongest growth catalyst is the rapid integration of smart cockpit technologies that combine connectivity, infotainment, digital displays, and personalized user interfaces into a unified vehicle experience. More than 50% of premium vehicle launches now incorporate advanced digital cockpit features, while adoption of large-format display systems has increased by approximately 20% over the past three years. China’s electric vehicle manufacturing expansion and government-backed intelligent mobility initiatives have accelerated deployment of connected interior technologies. This shift increases component value per vehicle and strengthens OEM differentiation strategies. In response, suppliers are expanding software capabilities, investing in display technologies, and forming partnerships with semiconductor and electronics firms. A notable strategic outcome is the transition from component-based competition toward integrated cabin ecosystem development, creating higher switching costs and longer supplier engagement cycles.

Persistent volatility in specialty polymers, semiconductor content, and advanced upholstery materials continues to constrain operational efficiency. Material input costs for selected interior components have fluctuated by 10–15% annually, while lead times for certain electronic modules remain approximately 20% higher than pre-disruption levels. Germany and Japan-based manufacturers face additional pressure from energy-intensive production processes and stricter compliance requirements for sustainable materials. These factors compress margins and complicate long-term sourcing decisions. Companies are mitigating exposure through supplier diversification, regional procurement networks, and localized manufacturing strategies. A key operational challenge is balancing premium interior innovation with cost discipline, particularly as automakers seek to maintain competitive vehicle pricing while incorporating increasingly sophisticated cabin technologies.

A significant opportunity is emerging through software-defined interiors and sustainable material innovation. Recycled and bio-based materials are achieving adoption rates above 25% in selected vehicle programs, while AI-enabled personalization systems can improve user interaction efficiency by nearly 20%. India is becoming an attractive development hub due to expanding automotive electronics production and localization incentives supporting advanced component manufacturing. Future cabin platforms will increasingly integrate over-the-air updates, adaptive interfaces, and intelligent occupant monitoring systems. To capture this opportunity, manufacturers are increasing R&D spending, establishing technology alliances, and investing in material science capabilities. A less obvious advantage lies in reducing platform complexity through software upgrades, enabling automakers to extend product lifecycles while lowering redesign and engineering costs.

The primary long-term challenge involves integrating software, electronics, sensors, displays, connectivity modules, and interior hardware into a seamless operating environment. Modern smart cabins can contain over 30 interconnected digital functions, increasing validation requirements and development complexity. Cybersecurity compliance requirements have expanded by approximately 25% as connected vehicle architectures become more sophisticated. In the United States, manufacturers are facing growing pressure to secure vehicle data while maintaining seamless user experiences across multiple digital platforms. These integration demands increase engineering costs, testing cycles, and deployment timelines. Companies must address this through investment in centralized computing architectures, software expertise, and strategic technology partnerships. Organizations that successfully manage interoperability and cybersecurity challenges will establish stronger long-term competitiveness and more scalable interior technology platforms.

• Software-Centric Cabin Architectures Automotive manufacturers are consolidating multiple control units into centralized cockpit platforms, reducing electronic module counts by nearly 15% and cutting wiring complexity by approximately 18%. Adoption of integrated display ecosystems has exceeded 40% in newly launched passenger vehicles in China and Germany. This transition improves assembly efficiency and accelerates feature deployment cycles. Suppliers are expanding software engineering teams and partnering with semiconductor firms to support scalable cabin computing platforms amid growing vehicle digitalization requirements.

• Localized Material Supply Networks Ongoing logistics volatility and procurement risks are pushing manufacturers toward regional sourcing strategies. Interior component suppliers have increased local procurement ratios by 20–25% in key production hubs, while inventory lead times have declined by nearly 12%. India and Mexico are attracting new investments for upholstery, polymer, and trim manufacturing. Beyond risk reduction, localized sourcing is improving production scheduling accuracy, prompting companies to restructure supplier ecosystems and establish long-term procurement agreements.

• Sustainable Interior Material Adoption Automakers are increasing deployment of recycled fabrics, bio-based polymers, and low-emission cabin materials. Sustainable material penetration has surpassed 25% in selected vehicle programs, while interior component carbon footprints have declined by nearly 20%. Regulatory scrutiny around lifecycle emissions is accelerating implementation. Companies are scaling material innovation programs and forming partnerships with specialty material producers to meet compliance targets without compromising durability or cabin aesthetics.

• Immersive User Experience Expansion Demand is shifting toward adaptive lighting, intelligent seating, and personalized cabin environments. Advanced ambient lighting installations have increased by over 30%, while AI-driven personalization functions are improving user interaction efficiency by approximately 20%. A less obvious trend is the use of occupant behavior analytics to optimize interior settings automatically. Vehicle manufacturers are integrating sensor technologies and expanding collaborations with software developers to strengthen customer retention and premium feature differentiation.

Seats represent the leading segment due to their high content value, integration across every vehicle platform, and direct influence on comfort, safety, and brand differentiation. More than 35% of interior system spending remains concentrated in seating technologies, supported by growing demand for ventilation, memory functions, and lightweight structural designs. Manufacturers in China and the United States are increasing investment in modular seat architectures that reduce assembly complexity by nearly 12%. Dashboard systems continue evolving through digital integration, while door panels maintain strategic importance through material innovation and acoustic performance enhancements.

Infotainment Systems are the fastest-growing segment as automakers prioritize connected vehicle experiences and software-enabled functionality. Adoption of large-format displays and integrated infotainment platforms has increased by over 25% in new vehicle launches. Interior Lighting is also gaining traction, particularly in premium and electric vehicle categories where personalized cabin experiences support product differentiation. Companies are responding through software partnerships, display technology investments, and next-generation cockpit development programs. Investment priorities are gradually shifting from conventional trim enhancements toward intelligent interior ecosystems that combine hardware, software, and user experience capabilities.

Passenger Cars remain the dominant application segment due to large production volumes, broad consumer demand, and continuous interior feature upgrades. More than 60% of advanced interior technology deployments are concentrated within passenger vehicle platforms, supported by increasing consumer preference for connected and personalized cabin experiences. Automakers are expanding digital dashboard integration, advanced seating systems, and premium material offerings to strengthen product differentiation. Luxury Vehicles continue influencing innovation trends, often serving as early deployment platforms for new interior technologies before broader market adoption.

Electric Vehicles represent the fastest-growing application segment as manufacturers redesign cabin layouts around software-defined architectures and user-centric experiences. Connected cockpit deployment rates in EV models exceed 45%, while smart interior feature adoption is growing approximately 20% faster than in conventional vehicle programs. Commercial Vehicles are increasingly incorporating ergonomic seating and digital monitoring systems to improve driver productivity. Autonomous Vehicles remain an emerging segment where interior design is evolving toward multifunctional cabin concepts. Companies are scaling platform integration strategies and expanding technology partnerships to address changing mobility requirements and maximize operational flexibility.

Automotive OEMs remain the largest end-user group because they control vehicle platform development, technology specifications, and large-scale procurement decisions. More than 70% of interior system demand originates from OEM-led production programs, making them the primary drivers of innovation and deployment. Vehicle Manufacturers continue increasing investments in digital cockpit systems, sustainable materials, and modular interior architectures. Automotive Dealers support demand through premium feature packaging and vehicle customization offerings, while Aftermarket Suppliers maintain relevance through replacement components and upgrade solutions.

Mobility Service Providers are emerging as the fastest-growing end-user segment as shared mobility operators prioritize durability, connected services, and passenger experience optimization. Fleet Operators are also increasing procurement of advanced seating and cabin monitoring technologies, with connected interior adoption rising by nearly 18% in commercial mobility fleets. Companies are targeting these segments through subscription-based feature models, strategic partnerships, and tailored interior solutions designed for higher utilization rates. Future demand is gradually shifting toward service-oriented vehicle ecosystems where interior functionality directly influences user satisfaction, retention, and operational efficiency.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

Software-Integrated Cabin Modernization Driving Premiumization

North America represents a significant automotive interior innovation hub, supported by advanced vehicle manufacturing, connected mobility deployment, and increasing demand for premium cabin experiences. The region accounts for approximately 24% of global market activity, with strong concentration across the United States and Mexico production corridors. Automotive manufacturers are accelerating deployment of AI-enabled cockpit systems, digital displays, and sustainable interior materials. A notable operational trend is the expansion of localized component manufacturing, reducing selected procurement lead times by nearly 15%. Strategic partnerships between automakers, electronics suppliers, and software developers are strengthening product differentiation while improving platform scalability across passenger vehicle and electric vehicle programs.

United States Market Outlook: The United States remains the region’s technology leader due to its advanced automotive R&D ecosystem, software integration capabilities, and strong electric vehicle manufacturing base. More than 50% of newly launched premium vehicle programs incorporate advanced digital cockpit features and connected interior platforms. Automakers are investing heavily in intelligent seating systems, AI-assisted cabin controls, and centralized vehicle computing architectures. The country's strong semiconductor ecosystem and growing domestic manufacturing incentives continue supporting interior technology localization and deployment efficiency.

Sustainable Material Innovation Reshaping Interior Design

Europe maintains a strong position through premium vehicle production, regulatory leadership, and advanced material engineering capabilities. The region contributes approximately 22% of global automotive interior demand and leads adoption of sustainable cabin materials. Vehicle manufacturers are increasingly deploying recycled polymers, bio-based textiles, and low-emission interior components to align with evolving environmental requirements. Interior material carbon reduction initiatives have improved lifecycle performance by nearly 20% across several vehicle platforms. Strong collaboration between automakers and material science companies continues accelerating innovation while supporting premium vehicle differentiation and regulatory compliance objectives.

Germany Market Outlook: Germany serves as the technological center of the European automotive interior ecosystem. The country benefits from a highly integrated supplier network, advanced manufacturing infrastructure, and global leadership in premium vehicle engineering. More than 40% of luxury vehicle interior innovation projects within Europe originate from German manufacturers and suppliers. Investments in smart cockpit technologies, sustainable material development, and software-defined vehicle platforms continue reinforcing the country's competitive position across global automotive value chains.

Manufacturing Scale and Smart Cabin Adoption Leadership

Asia-Pacific remains the largest automotive interior market due to its unmatched vehicle production scale, integrated supply chains, and accelerating deployment of advanced cabin technologies. The region contributes roughly 46% of global market activity and hosts major manufacturing clusters across China, Japan, South Korea, and India. Vehicle manufacturers are increasing investment in digital cockpit systems, lightweight materials, and intelligent interior electronics. Production localization initiatives and expanding electric vehicle output have improved supply-chain efficiency by approximately 18% in several industrial hubs. Strong export capabilities and large domestic vehicle demand continue supporting long-term operational advantages.

China Market Outlook: China dominates global automotive interior production through its extensive manufacturing ecosystem and rapid technology adoption. The country accounts for more than 30% of global vehicle production and leads deployment of connected cockpit technologies in mass-market vehicle segments. Large-scale investments in electric vehicles, automotive electronics, and intelligent mobility platforms continue creating opportunities for interior suppliers. Strong vertical integration across materials, electronics, and assembly operations provides cost and deployment advantages that are difficult for competing manufacturing hubs to replicate.

Localized Manufacturing Supporting Demand Recovery

South America is strengthening its position through gradual industrial modernization, vehicle production recovery, and increased localization of automotive components. The region contributes approximately 5% of global automotive interior demand, with activity concentrated around established manufacturing centers. Manufacturers are investing in upgraded assembly operations and localized sourcing strategies to reduce import dependence and improve operational stability. Recent industrial expansion programs have improved selected component localization rates by nearly 12%. While infrastructure constraints and currency volatility continue influencing investment decisions, suppliers are focusing on operational flexibility and cost optimization to improve competitiveness.

Brazil Market Outlook: Brazil remains the most influential automotive interior market in South America due to its large vehicle production base and established supplier ecosystem. The country continues attracting investment into seating systems, trim components, and interior plastics manufacturing. Automotive production clusters support efficient supplier integration and domestic market access. Increasing localization efforts and modernization of production facilities are improving manufacturing resilience, while demand for connected vehicle features is gradually expanding opportunities for advanced interior technology suppliers.

Industrial Diversification and Mobility Investment Momentum

Middle East & Africa is emerging as a high-priority market supported by industrial diversification initiatives, infrastructure modernization, and expanding mobility investments. The region accounts for approximately 3% of global demand but is experiencing accelerating deployment of advanced vehicle technologies. Governments are promoting automotive manufacturing and assembly investments to strengthen industrial capabilities and reduce import dependence. Several modernization projects have increased automotive industrial capacity utilization by nearly 10% across selected markets. Growing demand for premium vehicles and connected mobility solutions is creating new opportunities for interior component suppliers and technology providers.

Saudi Arabia Market Outlook: Saudi Arabia is establishing itself as the region’s strategic automotive investment hub through industrial diversification programs and large-scale mobility initiatives. The country is attracting investment into vehicle assembly, electric mobility infrastructure, and advanced manufacturing facilities. National industrial development strategies are encouraging localization of automotive components and supplier networks. Increasing deployment of smart mobility solutions and premium vehicle platforms is creating demand for advanced cockpit systems, intelligent seating technologies, and sustainable interior materials, strengthening the country’s long-term market relevance.

The competitive landscape is led by Adient, Lear Corporation, Forvia, Yanfeng Automotive Interiors, Toyota Boshoku, and Magna International, with global technology leaders competing directly against cost-efficient regional manufacturers and vertically integrated suppliers. The top five players collectively control approximately 42% of market activity. Competition centers on digital cockpit integration, lightweight materials, supply-chain efficiency, and customization capabilities. Advanced interior platforms can reduce assembly complexity by 12%, while localized sourcing strategies improve procurement responsiveness by nearly 15%. Leading companies are expanding manufacturing footprints in China, India, and Mexico while forming partnerships with software, semiconductor, and material technology firms. Vertical integration is increasing as suppliers seek greater control over electronics, displays, and sustainable materials. The current competitive shift favors intelligent cabin ecosystems rather than standalone components, creating pressure on traditional manufacturers. High development costs, validation requirements, and software integration complexity remain major entry barriers. Success increasingly depends on combining scalable manufacturing, digital innovation, and resilient supply-chain execution.

Adient plc

Lear Corporation

Forvia

Yanfeng Automotive Interiors

Toyota Boshoku Corporation

Magna International Inc.

Grupo Antolin

Hyundai Transys

TS Tech Co., Ltd.

Grammer AG

NHK Spring Co., Ltd.

TACHI-S Co., Ltd.

Faurecia Clarion Electronics

Sage Automotive Interiors Inc.

Digital cockpit platforms currently represent the most influential technology shift within automotive interiors. Integrated display ecosystems, AI-enabled voice interfaces, and centralized computing architectures are now deployed in more than 45% of newly launched passenger vehicles. Compared with traditional distributed cockpit systems, centralized platforms reduce wiring complexity by approximately 18% and lower assembly time by 12%. These technologies improve software update capability, streamline manufacturing workflows, and strengthen vehicle differentiation. OEMs and Tier-1 suppliers benefit through faster feature deployment, lower integration costs, and improved platform scalability across multiple vehicle models.

Emerging technologies are focused on intelligent personalization and sustainable material innovation. Occupant monitoring systems, adaptive ambient lighting, and smart seating solutions are improving user interaction efficiency by nearly 20%, while recycled and bio-based interior materials reduce component carbon footprints by up to 25%. Adoption of advanced cabin sensing technologies has exceeded 30% in premium vehicle programs. Manufacturers are integrating sensors, software, and lightweight materials into unified cabin ecosystems to enhance comfort, safety, and operational performance while meeting evolving regulatory and consumer expectations.

Disruptive technologies between 2026 and 2028 will center on software-defined interiors, immersive display environments, and AI-driven cabin automation. Intelligent cockpit systems are expected to exceed 55% deployment across new electric vehicle platforms, while predictive personalization functions can improve user engagement by nearly 15%. Companies investing early in software integration, advanced electronics, and smart material ecosystems will gain stronger competitive positioning, shorter development cycles, and greater control over future interior innovation roadmaps.

January 2026 – Adient introduced its ModuTec modular seating manufacturing solution, enabling seat module assembly to shift offline and reducing assembly time from minutes to seconds. The innovation supports higher automation levels and simplified production workflows, improving manufacturing efficiency and lowering operational costs. Source: adient.com

June 2025 – FORVIA received the German Innovation Award 2025 for its Cockpit UX Engine platform, which utilizes driver-monitoring technology to reduce distraction and improve in-cabin interaction. The software leverages existing hardware infrastructure, supporting lower integration costs and faster deployment across vehicle programs. Source: forvia.com

February 2025 – Lear Corporation announced integration of its ComfortMax Seat technology with General Motors vehicles, embedding thermal comfort systems directly into trim covers. The solution improves occupant comfort while streamlining manufacturing processes, strengthening Lear’s position in advanced seating engineering and OEM collaboration. Source: lear.com

April 2026 – FORVIA agreed to sell its interiors business to Apollo Funds, transferring 59 manufacturing sites and 8 R&D centers as part of a strategic portfolio restructuring initiative. The transaction sharpens focus on higher-value technology segments and strengthens capital allocation priorities.

This report provides comprehensive analysis of the automotive interior ecosystem across Seats, Dashboard, Door Panels, Infotainment Systems, and Interior Lighting segments. It evaluates demand patterns across Passenger Cars, Commercial Vehicles, Electric Vehicles, Luxury Vehicles, and Autonomous Vehicles while assessing purchasing behavior among Automotive OEMs, Aftermarket Suppliers, Fleet Operators, Vehicle Manufacturers, Mobility Service Providers, and Automotive Dealers. The study examines technology adoption trends including digital cockpits, AI-enabled cabin systems, smart seating, sustainable materials, and connected vehicle interfaces, with deployment penetration exceeding 40% in selected advanced vehicle programs.

The report delivers region-wise assessment across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, covering manufacturing concentration, localization strategies, supply-chain developments, and investment priorities. Analysis includes competitive positioning of leading suppliers, innovation pipelines, partnership activity, and emerging opportunities in software-defined interiors and intelligent cabin platforms. Strategic insights support expansion planning, product development, technology investment decisions, market entry evaluation, and long-term competitive benchmarking between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 62790 Million |

|

Market Revenue in 2033 |

USD 97390.73 Million |

|

CAGR (2026 - 2033) |

5.64% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Adient plc, Lear Corporation, Forvia, Yanfeng Automotive Interiors, Toyota Boshoku Corporation, Magna International Inc., Grupo Antolin, Hyundai Transys, TS Tech Co., Ltd., Grammer AG, NHK Spring Co., Ltd., TACHI-S Co., Ltd., Faurecia Clarion Electronics, Sage Automotive Interiors Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |