Reports

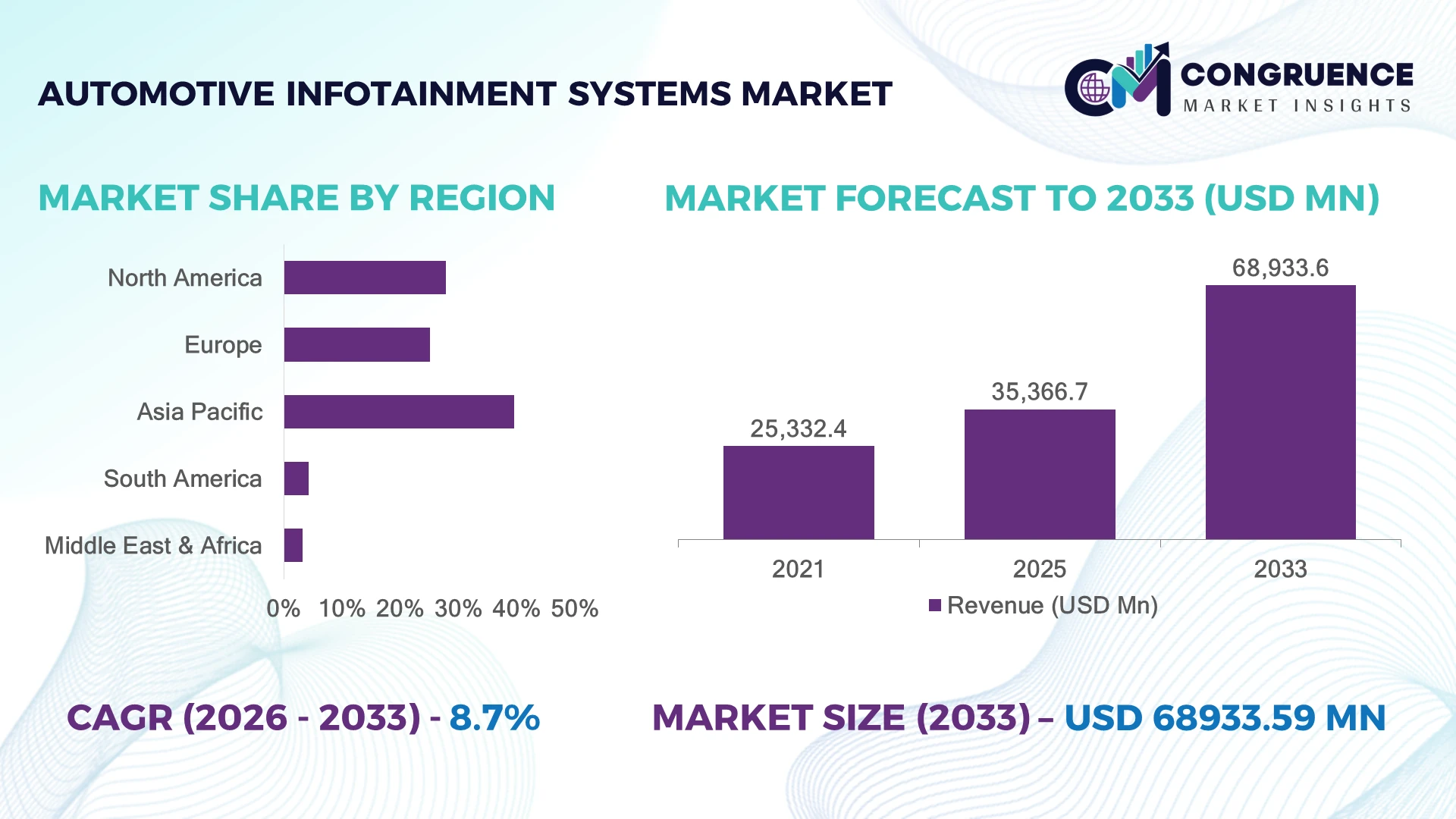

The Global Automotive Infotainment Systems Market was valued at USD 35,366.7 Million in 2025 and is anticipated to reach a value of USD 68933.6 Million by 2033 expanding at a CAGR of 8.7% between 2026 and 2033. Rising integration of connected vehicle platforms, AI-enabled interfaces, and software-defined automotive architectures is accelerating adoption of advanced infotainment ecosystems.

China dominates the Automotive Infotainment Systems Market with nearly 32% share, supported by rapid electric vehicle penetration, smart cockpit adoption, and large-scale automotive electronics manufacturing. Compared with Germany’s premium vehicle-focused ecosystem, China leads in mass deployment, with over 55% of newly launched vehicles integrating connected infotainment features. Ongoing automotive technology competition and supply-chain localization trends are strengthening domestic innovation capabilities.

Automotive manufacturers and technology providers prioritizing intelligent user experiences, scalable software platforms, and connected mobility integration are positioned to gain long-term competitive advantages.

• Market Size & Growth: Global market reached USD 35,366.7 Million in 2025 and is projected at USD 68,933.6 Million by 2033 with 8.7% CAGR, driven by connected vehicle adoption.

• Top Growth Drivers: AI-powered interfaces, EV integration, and connected mobility platforms are improving adoption momentum by 35%, 42%, and 30%, respectively.

• Short-Term Forecast: By 2028, advanced infotainment processors are expected to improve response efficiency by 25% through software optimization.

• Emerging Technologies: AI assistants, augmented reality displays, and cloud-based infotainment platforms are reshaping digital cockpit experiences.

• Regional Leaders: Asia-Pacific, North America, and Europe continue expansion through EV platforms, premium vehicles, and software-defined mobility adoption.

• Consumer/End-User Trends: Over 60% of vehicle buyers prioritize connected navigation, smartphone integration, and personalized digital features.

• Pilot/Case Example: 2026 smart cockpit deployments improved driver interaction efficiency by nearly 28% through AI-based personalization.

• Competitive Landscape: Leading players hold nearly 45% share, including Panasonic, Harman, Bosch, Continental, and Denso.

• Regulatory & ESG Impact: Software standardization and energy-efficient electronics development are improving automotive digital system efficiency by nearly 20%.

• Investment & Funding: Multi-billion-dollar investments are focused on automotive software platforms, semiconductor partnerships, and digital cockpit expansion.

• Innovation & Future Outlook: Next-generation infotainment is shifting toward AI-driven, cloud-connected, and fully integrated mobility ecosystems.

The Automotive Infotainment Systems Market is transforming through intelligent cockpit platforms, connected services, and vehicle software innovation. Automakers are integrating AI, voice control, and advanced displays to enhance user experience, with over 50% of new vehicles adopting connected infotainment capabilities. Semiconductor localization and software-defined vehicle strategies are creating a stronger foundation for future automotive digital ecosystems.

The Automotive Infotainment Systems Market is becoming a strategic pillar of vehicle differentiation as automakers shift from hardware-focused design toward connected, software-defined mobility experiences. Growing consumer preference for digital interfaces, real-time connectivity, and personalized vehicle ecosystems is reshaping product development strategies. Automotive companies are restructuring technology partnerships and semiconductor supply chains to secure long-term digital platform capabilities.

Advanced infotainment architectures provide significant improvements compared with traditional standalone systems, with cloud-connected platforms reducing software update complexity by nearly 30% and improving feature deployment speed by approximately 25%. Asia-Pacific leads large-scale adoption through high-volume EV manufacturing, while Europe emphasizes premium digital cockpit integration and regulatory-focused software reliability.

Automakers are deploying AI-based assistants, over-the-air updates, and integrated vehicle operating systems to strengthen customer engagement. Leading companies are expanding collaborations with semiconductor firms, software developers, and connectivity providers. Future competitiveness will depend on scalable infotainment ecosystems that combine performance, personalization, cybersecurity, and continuous feature evolution.

Rising demand for connected mobility platforms is driving rapid transformation in automotive infotainment systems. More than 55% of newly manufactured vehicles now include connected features, while AI-enabled interfaces are improving user interaction efficiency by nearly 30%. Increasing adoption of electric vehicles has accelerated integration of larger displays, cloud connectivity, and intelligent navigation systems. Automakers are responding through software investments, partnerships with technology providers, and development of centralized vehicle computing platforms. The shift toward software-defined vehicles is transforming infotainment from a convenience feature into a strategic platform supporting personalization, subscriptions, and long-term customer engagement.

Advanced infotainment systems face challenges from semiconductor dependency, software complexity, and rising electronic component requirements. Modern connected platforms require high-performance processors and sensors, increasing system development complexity by nearly 25%. Supply-chain disruptions have encouraged automakers to reassess sourcing strategies as critical chip availability affects production flexibility. Integration of multiple operating systems, connectivity standards, and cybersecurity requirements increases validation timelines by approximately 20%. Companies are reducing risks through semiconductor partnerships, localized sourcing strategies, modular architectures, and improved software development processes to maintain stable deployment across vehicle platforms.

Artificial intelligence, cloud connectivity, and software-driven services are creating new opportunities across automotive infotainment ecosystems. AI-based personalization can improve user engagement by nearly 35%, while over-the-air update capabilities reduce service dependency by approximately 25%. Automakers are shifting toward subscription-based digital features, intelligent assistants, and connected entertainment platforms to create recurring customer value. Growth in electric and autonomous vehicle technologies is expanding demand for immersive cockpit experiences. Companies are strengthening R&D investments, forming software alliances, and building scalable infotainment platforms designed for future mobility applications.

Increasing vehicle connectivity creates long-term challenges related to cybersecurity, software reliability, and lifecycle management. Connected infotainment platforms generate larger data exchange volumes, increasing security monitoring requirements by nearly 40%. Automakers must manage frequent software updates, compatibility issues, and evolving digital safety expectations across multiple vehicle generations. Differences in connectivity infrastructure and regulatory frameworks create deployment complexity across countries. Companies are investing in secure vehicle operating systems, advanced encryption, continuous monitoring tools, and technology partnerships to ensure reliable digital experiences while protecting consumer data and brand reputation.

• AI-Powered Digital Cockpits: Automakers are expanding intelligent cockpit platforms with AI assistants, predictive controls, and personalized interfaces. Adoption of AI-enabled infotainment features has increased by nearly 35%, improving driver interaction and system responsiveness by 25%. Companies are partnering with software developers and semiconductor providers to accelerate next-generation user experiences.

• Software-Defined Vehicle Integration: Infotainment systems are becoming central components of software-defined vehicles through cloud connectivity and over-the-air capabilities. Nearly 50% of new connected vehicles support remote feature updates, reducing service dependency by 20%. Manufacturers are restructuring development models around scalable software platforms and digital ecosystems.

• Advanced Display Technologies: Larger touchscreens, augmented reality displays, and immersive interfaces are replacing traditional control layouts. Premium vehicle segments report over 40% adoption of advanced cockpit displays, enhancing navigation accuracy and passenger engagement. Suppliers are investing in lightweight, energy-efficient display technologies optimized for electric vehicles.

• Connected Services Expansion: Subscription-based features, integrated applications, and real-time connectivity are transforming infotainment business models. Digital service adoption has increased by nearly 30% as automakers focus on long-term customer relationships. Companies are expanding cloud infrastructure and strategic partnerships to support continuous feature delivery and connected mobility platforms.

Embedded infotainment systems dominate the Automotive Infotainment Systems Market due to their strong integration capabilities, reliability, cybersecurity advantages, and compatibility with advanced vehicle architectures. Embedded systems account for nearly 48% of adoption, supported by automakers integrating factory-installed connected platforms, navigation, and digital cockpit functions. Tethered systems continue to serve cost-sensitive vehicle categories by enabling smartphone-based connectivity, while integrated systems are gaining importance through seamless interaction between infotainment, vehicle controls, and driver assistance technologies.

Integrated infotainment systems represent the fastest-growing type as software-defined vehicles increase demand for unified digital ecosystems. Adoption is rising by nearly 32% as manufacturers prioritize centralized computing, cloud connectivity, and over-the-air feature upgrades. Automotive technology providers are expanding software partnerships, AI-enabled interfaces, and modular infotainment platforms to improve scalability. Investment priorities are shifting toward systems that combine entertainment, connectivity, personalization, and vehicle intelligence within a single digital experience.

• According to the 2026 Consumer Technology Association (CTA) mobility technology assessment, more than 50% of new connected vehicles globally are expected to feature advanced embedded digital platforms, reflecting increasing integration of smart cockpit technologies.

Passenger vehicles represent the leading application segment in the Automotive Infotainment Systems Market due to high production volumes, increasing consumer expectations, and rapid adoption of connected mobility features. Passenger vehicle applications contribute nearly 72% of infotainment deployment, supported by growing integration of touchscreen displays, voice assistants, navigation platforms, and smartphone connectivity. Commercial vehicles continue adopting infotainment solutions for fleet management, driver assistance, and operational connectivity, creating demand for durable and productivity-focused systems.

Electric vehicles are emerging as the fastest-growing application area as automakers position digital interfaces as a central part of the mobility experience. EV infotainment adoption is expanding by nearly 40%, driven by larger displays, charging integration, energy monitoring, and software-based services. Companies are adapting through cloud-based ecosystems, AI-driven personalization, and strategic technology collaborations. Demand is increasingly shifting toward platforms that combine entertainment, vehicle management, connectivity, and intelligent user interaction.

• A 2025 International Energy Agency (IEA) mobility analysis highlighted that electric vehicle adoption exceeded 20% of global new vehicle sales, accelerating integration of advanced connected cockpit and digital mobility solutions.

Automotive OEMs dominate the Automotive Infotainment Systems Market due to large-scale vehicle integration, direct technology partnerships, and increasing focus on software-defined automotive platforms. OEMs represent approximately 68% of infotainment system demand, supported by factory-installed digital cockpit solutions and connected vehicle strategies. The aftermarket segment maintains relevance through replacement displays, upgrades, and smartphone-compatible solutions, particularly across older vehicle fleets and emerging automotive markets.

Mobility service providers and fleet operators are becoming the fastest-expanding end-user category as connected vehicle management and digital service integration gain importance. Adoption among fleet-focused users is increasing by nearly 28% due to demand for navigation, remote monitoring, and driver communication capabilities. Companies are targeting these segments through customized interfaces, subscription-based services, and ecosystem partnerships. Future competition is shifting toward software capability, user experience differentiation, and long-term digital service opportunities.

• The 2026 World Economic Forum connected mobility outlook indicated that digital vehicle ecosystems and software-enabled services are becoming key investment priorities as automakers transition toward intelligent transportation platforms.

Asia-Pacific accounted for the largest market share at 39.6% in 2025 moreover, Asia-Pacific is also expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

Software-Defined Vehicles and Connected Cockpit Integration Transform Mobility Experience

North America’s Automotive Infotainment Systems Market is driven by strong adoption of connected vehicles, premium digital cockpit technologies, and advanced automotive software ecosystems. The region accounted for nearly 27.8% market share in 2025, supported by high penetration of AI-enabled interfaces, cloud connectivity, and over-the-air update platforms. More than 60% of newly launched vehicles in the region integrate connected infotainment capabilities as automakers transition toward software-defined architectures. Technology companies and automotive manufacturers are strengthening collaborations around voice assistants, vehicle operating systems, and personalized digital services. Investments in semiconductor partnerships and automotive software platforms are reshaping product development strategies while improving infotainment performance, security, and long-term feature scalability.

United States Market Outlook: The United States leads regional adoption due to strong automotive technology innovation, connected vehicle infrastructure, and presence of leading software providers. More than 65% of new vehicles sold in the country include advanced connectivity features, supporting demand for intelligent infotainment ecosystems. Automakers are expanding AI integration, digital services, and cloud-based platforms to strengthen user engagement and competitive differentiation.

Premium Vehicle Innovation and Digital Regulations Accelerate Smart Cockpit Development

Europe’s Automotive Infotainment Systems Market is shaped by premium automotive engineering, software integration, and increasing focus on connected mobility standards. The region represented nearly 25.1% market share in 2025, supported by advanced infotainment adoption across luxury and electric vehicle platforms. Nearly 50% of European vehicle launches now include enhanced digital cockpit features such as intelligent navigation, voice control, and connected applications. Automakers are investing in cybersecurity, software compliance, and modular infotainment platforms to improve digital reliability. The shift toward electric mobility is increasing demand for integrated displays, energy management interfaces, and connected driving experiences.

Germany Market Outlook: Germany dominates European demand due to its strong automotive manufacturing base, premium vehicle ecosystem, and advanced engineering capabilities. The country produces over 4 million vehicles annually, creating significant demand for next-generation infotainment platforms. German manufacturers are accelerating software-defined vehicle strategies through digital cockpit development, AI integration, and technology partnerships.

High-Volume Vehicle Production and Smart Mobility Adoption Strengthen Leadership

Asia-Pacific’s Automotive Infotainment Systems Market leads global adoption due to large-scale vehicle manufacturing, rapid EV expansion, and strong consumer demand for connected features. The region captured nearly 39.6% market share in 2025, supported by China, Japan, South Korea, and India’s expanding automotive technology ecosystems. Over 55% of vehicles produced by leading Asian automakers include connected infotainment functions, reflecting faster integration of digital mobility platforms. Companies are expanding software development centers, semiconductor partnerships, and localized infotainment manufacturing to support demand for affordable and intelligent vehicle experiences.

China Market Outlook: China represents the strongest country-level market due to its leadership in electric vehicles, automotive electronics, and smart cockpit deployment. The country produced more than 30 million vehicles in 2025, creating extensive demand for infotainment technologies. Domestic automakers are accelerating AI assistants, large-display interfaces, and connected vehicle ecosystems to strengthen global competitiveness.

Connected Vehicle Adoption Expands Through Digital Feature Accessibility

South America’s Automotive Infotainment Systems Market is developing through increasing demand for connected features, smartphone integration, and modern vehicle interfaces. The region accounted for nearly 4.3% market share in 2025, with adoption primarily driven by passenger vehicle upgrades and improving automotive technology availability. Entry-level infotainment systems with navigation, connectivity, and multimedia capabilities are gaining traction among cost-sensitive consumers. Automakers are adapting through localized vehicle configurations and affordable digital solutions, although advanced software deployment remains influenced by infrastructure limitations and price sensitivity.

Brazil Market Outlook: Brazil leads South American adoption due to its established automotive manufacturing ecosystem and expanding connected vehicle penetration. The country produces more than 2 million vehicles annually, supporting infotainment system integration across passenger cars. Automakers are introducing touchscreen displays, smartphone connectivity, and localized digital services to match changing consumer expectations and strengthen market competitiveness.

Premium Mobility Expansion and Digital Infrastructure Development Support Adoption

Middle East & Africa’s Automotive Infotainment Systems Market is supported by rising premium vehicle demand, smart mobility initiatives, and improving connected infrastructure. The region represented approximately 3.2% market share in 2025, with adoption concentrated across luxury vehicles, fleet modernization, and advanced mobility projects. Increasing deployment of 5G networks and smart city programs is supporting connected vehicle technologies. Automakers and technology providers are expanding digital service ecosystems, navigation platforms, and advanced user interfaces to address demand for intelligent mobility solutions across developed automotive hubs.

United Arab Emirates Market Outlook: The United Arab Emirates represents a key market due to high luxury vehicle adoption, digital infrastructure investment, and smart transportation initiatives. Premium vehicles account for a significant share of automotive demand, increasing adoption of advanced infotainment systems. Government-backed mobility modernization programs are encouraging connected platforms, intelligent navigation, and integrated vehicle technologies.

The Automotive Infotainment Systems Market is driven by competition between global technology leaders such as Bosch, Harman International, Panasonic Automotive, Continental, and Denso against specialized software providers and regional electronics manufacturers. Leading companies compete through integrated cockpit platforms, while emerging players challenge with cloud-native software, AI interfaces, and cost-efficient solutions. The top 5 players collectively control nearly 48% of the market, reflecting strong technology and OEM relationship advantages. Competition is based on software capability, connectivity performance, and customization, with AI-enabled systems improving user interaction efficiency by nearly 25% and modular platforms reducing development cycles by around 18%. Companies are expanding through automotive software partnerships, semiconductor alliances, and vertical integration of hardware-software ecosystems. The market is shifting toward software-defined vehicles, increasing barriers around cybersecurity expertise, data integration, and OEM certification. Winning requires advanced software ownership, scalable platforms, and deep automotive ecosystem partnerships.

• Harman International

• Robert Bosch GmbH

• Continental AG

• Denso Corporation

• Panasonic Automotive Systems Co., Ltd.

• Visteon Corporation

• Aptiv PLC

• Pioneer Corporation

• Garmin Ltd.

• Alpine Electronics, Inc.

• LG Electronics

• Marelli Holdings Co., Ltd.

• TomTom N.V.

Automotive infotainment technologies are advancing through AI-powered interfaces, connected operating systems, voice assistants, and integrated digital cockpit architectures. Touchscreen displays, smartphone integration, navigation platforms, and cloud-based services remain core technologies, with connected infotainment deployed across nearly 65% of new passenger vehicles. AI personalization improves interaction accuracy by approximately 20%, enabling automakers to deliver safer and more adaptive in-vehicle experiences.

Emerging technologies including augmented reality displays, 5G connectivity, edge computing, and over-the-air software updates are transforming infotainment from hardware-based systems into continuously upgradeable platforms. Compared with traditional embedded infotainment units, software-defined architectures improve feature deployment speed by nearly 30% and reduce dependency on physical upgrades. Premium automakers and technology-focused suppliers benefit most by creating recurring digital service ecosystems and differentiated user experiences.

Between 2026 and 2028, generative AI assistants, vehicle app ecosystems, and unified cockpit platforms will redefine competition. Around 45% of next-generation vehicle programs are expected to prioritize centralized computing architectures. Companies investing in cybersecurity, cloud integration, and flexible software platforms will gain stronger OEM partnerships and faster innovation cycles.

• January 2025 Harman International enhanced its Ready Display technology portfolio with HDR10+ Automotive certification, improving in-vehicle visual performance and adaptive display capability. The innovation strengthened premium cockpit experiences and next-generation infotainment differentiation across connected vehicles. Source: harman.com

• January 2025 Continental advanced its next-generation cockpit and display technologies, introducing larger integrated vehicle interfaces exceeding 40 inches. The development improved digital interaction, personalization, and software-defined vehicle experiences while strengthening automaker adoption of intelligent infotainment ecosystems. Source: continental.com

• March 2024 Qualcomm expanded Snapdragon Digital Chassis adoption with global automakers, supporting connected cockpit, infotainment, and vehicle computing integration across millions of vehicles. The expansion accelerated centralized automotive software platforms and scalable digital mobility ecosystems. Source: qualcomm.com

• April 2024 Hyundai Motor Group accelerated software-defined vehicle development initiatives, focusing on connected infotainment platforms and centralized architectures with enhanced update capabilities. The strategic shift improved digital service deployment efficiency and strengthened long-term intelligent mobility competitiveness. Source: hyundaimotorgroup.com

The Automotive Infotainment Systems Market Report analyzes industry trends across system types, components, connectivity technologies, vehicle categories, applications, and end-user adoption patterns. The study covers embedded systems, connected platforms, navigation, multimedia, voice assistance, and emerging AI-enabled cockpit technologies across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report evaluates competitive positioning, technology adoption, supply chain strategies, and investment opportunities between 2026 and 2033. With over 60% of new vehicles integrating connected infotainment features, analysis highlights software-defined mobility, digital ecosystems, and user experience transformation. Insights support automakers, suppliers, investors, and technology companies in planning expansion strategies, innovation priorities, partnerships, and future market positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 35,366.7 Million |

|

Market Revenue in 2033 |

USD 68,933.6 Million |

|

CAGR (2026 - 2033) |

8.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Harman International, Robert Bosch GmbH, Continental AG, Denso Corporation, Panasonic Automotive Systems Co., Ltd., Visteon Corporation, Aptiv PLC, Pioneer Corporation, Garmin Ltd., Alpine Electronics, Inc., LG Electronics, Marelli Holdings Co., Ltd., TomTom N.V. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |